Markel hosts a brunch each year following the Berkshire Hathaway Annual Meeting, and has done so for 25 years now — during which time the company has grown considerably, from a small $100 million family-controlled specialty insurance company just starting to explore value investing with their new portfolio manager, Tom Gayner, to a $12 billion international and diversified insurer that, though it still has significant participation from the Markel family, now features Tom Gayner as co-CEO.

I’ve held Markel for a decade or so, almost as long as I’ve owned Berkshire Hathaway, and this weekend was my second time participating in the Markel Brunch. It’s held at the Hilton in Omaha, just across the street from the giant arena where Buffett and Munger held court for six hours the day before, and it is, in substance, essentially designed to do the same thing as the Berkshire meeting: give Markel shareholders a chance to understand the company better by asking questions and listening to the opinions and answers of Markel leadership. This is a nice thing to do, but it’s also good for the company — Markel’s business model, with their focus on long-term results and patient growth with little regard for quarter-to-quarter fluctuations, requires a base of capital (investors like you and I) who have “bought in” to the plan. Hearing from the horse’s mouth makes it a lot easier to buy in, and since there’s heavy overlap between Markel and Berkshire shareholders it’s no surprise that there were about 1,000 people at the brunch… or that Tom Gayner estimated that they represented a large portion of the equity owners of Markel.

I really like the company and their management and their culture, which they try very hard to institutionalize, but the stock has been disserved, I think, by their fairly constant promotion as the “next Berkshire” — people are so obsessed with finding the next Berkshire Hathaway that they occasionally get too excited about Markel and drive the shares up to what I think are unsustainably high price/book valuations.

Why price/book value? Well, mostly because book value growth is the metric Markel uses, and because it is, as they reiterated today, the “least bad” way of simply assessing the value and progress of the company. Markel has a large insurance operation that has been consistently profitable and that they’ve grown (mostly through acquisition) over the years, they have a large portfolio of both fixed income and equity investments, including their insurance “float” (premiums paid in that they haven’t yet paid out as claims), and they have a growing (but still small) subsidiary of controlled non-insurance businesses. It’s not necessarily true that book value is a fair approximation of Markel’s real worth, but it’s in the ballpark — and growth in book value over time is the best way to assess their performance — and that growth has tailed off considerably as the company has grown.

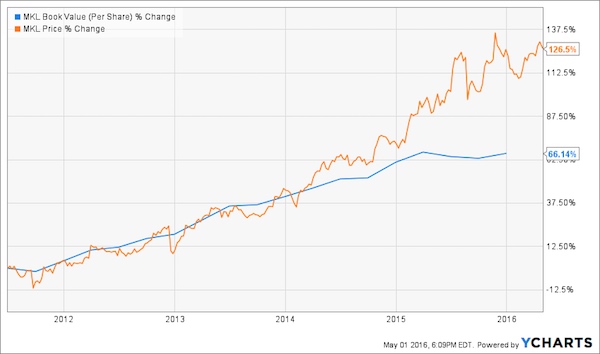

This is the chart of Markel’s growth in book value (blue line) over the long term, which gives me quite a bit of confidence that owning Markel will likely continue to be wise. I’m certainly not selling.

And this is the chart that gives me some qualms about buying more Markel RIGHT NOW — you can see that over the past year or two, the stock has become unhinged from book value growth and has taken off to new levels, it’s now trading at 1.6x book value, as high as almost any of the somewhat similar large specialty insurers, almost all of whom have also had a tremendous run over the last year or two… and quite a bit higher than most.

That doesn’t necessarily mean Markel is going down — it has traded at well over 2X book value for extended periods of time in the past when enthusiasm was high, and I bought some of my shares in the mid-2000s during such a time (though Markel was far smaller then)… and have no complaints about “overpaying” for that position, since it has increased in value several fold — but investing for the long term doesn’t mean you should ignore the price you pay, and Markel at $900+ is quite close to what I think is likely to be a peak valuation.

I will probably never tell anyone to sell this stock, since I’ve bought in to their model and their plan and their culture and I think they’ll continue to be excellent long-term stewards of my capital (and, importantly, because I don’t trust myself to sell in 2006 at 2X book and buy back in 2010 at 1X book — I’ve rarely been so nimble or well-timed in my trading), and I suspect that those who are thinking about a 20-year time horizon will still find Markel a profitable investment even at this elevated valuation, as I was after buying some of my shares near the 2006 highs and waiting several years for them to recover… but I wouldn’t “go big” with a new Markel position here.

There was a good Morningstar critique of Markel a couple weeks ago, if you’d like a more pessimistic take (they think Markel is overvalued because of the “baby Berkshire” comparison, and that W.R. Berkley (WRB) is a better bet) — here’s a taste of their analysis:

“We think the primary reason Markel draws interest is how it differentiates itself in terms of capital allocation. Most insurers actively return the bulk of their free cash flow, given the maturity of the industry. Markel retains the vast majority of its capital; its goal is to compound this capital at high rates of return over a long period and create value for shareholders. However, this is easier said than done, and we think the company’s record is mixed. We think expecting the company to repeat Berkshire Hathaway’s performance is overly optimistic. In recent years, the company’s largest moves have been to acquire Alterra and a variety of noninsurance operations. We’re skeptical that these moves have created value. The addition of Alterra dramatically increased the company’s exposure to reinsurance, a highly volatile area where we think it is difficult to build a moat. Further, based on industry overcapacity and recent pricing in reinsurance trends, we’re concerned this acquisition could prove ill-timed. The company’s noninsurance acquisitions do not appear to have created shareholder value, with these operations earning about a 6% return on invested capital over the past four years….

“We believe the company’s perceived ability to generate alpha on the investment side is the primary attraction for many investors. CIO Tom Gayner has an impressive record, as he has beaten the S&P 500 by almost 2 percentage points on average over the past 10 years. We like his investing approach, as it closely mirrors our methodology. However, we think the company’s asset-allocation decisions (and the bull market) have been a much bigger factor in driving book value growth in recent years. We estimate that even if Gayner is able to replicate the alpha he has generated historically, this would add only about 1 percentage point to annual book value growth, suggesting his investment skill is not enough to significantly affect our view of the company’s prospects. Further, the company acquires noninsurance operations as part of its investment strategy. In recent years, returns on invested capital for these acquisitions have averaged about 6%. While Markel believes these companies can grow over time to justify the prices paid, at this point we think a skeptical view of potential value creation in this area is warranted.”

Morningstar places a fair value of $715 on the shares — which, coincidentally, is right around where I’ve said I’d consider buying more Markel. That would be 1.3X book value.

What are the pros and cons that stand out from me, including those that caught my ears during the meeting? Here’s a summary from my notes:

Pros:

Reinsurance is not as bad a business as Buffett and others consistently say it is. Tom Gayner describes reinsurance as a “volatility absorption machine” as strong companies can offer their customers the ability to absorb blows. Historically, though there is too much supply in the market right now, it’s been a solid business and it helps Markel develop and maintain relationships — and, importantly, it moves in cycles and reinsurance has much lower overhead costs than primary insurance and it is, in broad strokes, a permanent business that will always be needed at some level… so it’s not very expensive to keep a strong reinsurance division on “care and maintenance” while you wait for better cycles.

Markel, thanks largely to the large, long-term shareholder base that was well represented at the brunch, is effectively managed like a private company, with long-term incentives for employees and a focus on long-term growth and relationship building with their customers, employees, vendors and shareholders. Employees and management are incentivized to provide profitable growth over three and five year periods, incentives are not built to maximize quarterly stock price returns or net income, which means that quarters are lumpy but also that the company doesn’t cut corners to boost short-term profitability.

Markel Ventures, though it remains small, is producing some success stories. Their first acquisition, AMF baking, is the example they consistently trot out to validate the idea of acquiring private companies — that was a situation where a local manufacturer of baking equipment had a good business but a bad balance sheet, and Markel’s balance sheet power and backing allowed them to become a better business and to grow (thanks partly to some further acquisitions) fivefold in a decade, while retaining the CEO who was leading the company when Markel acquired them. That’s a very Berkshire-like story. Unfortunately, their other acquisitions have not been as strong — but they are actively learning from those investments, and they have been small so far.

Tom Gayner is still a good investor, even though he’s no Warren Buffett. Gayner has beaten the S&P 500 over a long period of time by a meaningful but not huge margin, and Markel’s allocation of capital to riskier investments (like equities) has been a big part of their ability to provide higher returns for shareholders than some other insurers who invest more cautiously. And he has a long view — Markel does not have anywhere near the resources of Berkshire Hathaway (Markel has an equity portfolio of about $4 billion, Berkshire routinely has to decide how to allocate ten times that amount), but they do share Berkshire’s sentiment that they want to be ready for opportunities. Gayner said, “We will do everything we can to make sure that we have money when others have maybe not so much.”

Cons:

Reinsurance is not very profitable right now and is not likely to become dramatically more profitable in the near future, just because there’s so much capacity from financial companies who want that “float” exposure. That’s about 20% of Markel’s written premiums each year.

Markel Ventures makes a bunch of mistakes, they are in an extremely competitive environment for acquiring smallish private companies, and from what I can tell they have not yet successfully acquired any real cash-gushers. They have mostly acquired small companies that are pretty capital intensive, and that are difficult to scale aggressively. They also made only one acquisition last year, and it was a small services company, so this isn’t going to be a case where Markel Ventures scales up rapidly or accounts for a lot of Markel’s profits in the near future… the insurance operation is substantially more profitable than the other businesses they’ve invested in thus far, my expectations for Markel Ventures remain low — and, frankly, I wish Tom Gayner spent more of his time on the investment portfolio.

Returns have been dropping pretty consistently as Markel has grown — a little bit of that is because of reinsurance and because of the lack of large profits from Markel Ventures, their non-insurance segment, but mostly it’s probably just because their investments and insurance operations have not done quite as well since they’ve grown to be a $8, $10, $12 billion company as they did when Markel had a market cap of $2 or $3 billion several years ago. It continues to be harder and harder to move the needle, both because of competition in insurance and a generally soft market for premium pricing of late, and because it’s harder to generate large returns from a large portfolio than it is from a smaller portfolio.

The real “con” for Markel, though, is not that they’re doing anything wrong — it’s that the stock is, in my opinion, a bit overvalued right now. Being perhaps 20% over my “buy” price is not a good enough reason for me to sell the shares right now, but if I were a more active trader I’d probably look for ways to sell in the low-$900s and buy back in when some bad news hits, or when the market digests the fact that Markel had a pretty weak year last year, has not been able to grow book value by much recently, and is getting too much of a premium price. The risk, of course, is that perhaps that doesn’t happen, Markel’s core investors hold on, the enthusiasm for insurance stocks builds again, and MKL goes to $1,200 over the next couple years. There’s no rule that says an insurance company can’t trade for 2X book value, and sometimes some of them have in the past — including Markel in its younger days.

At current valuations, I think Berkshire Hathaway is more appealing than Markel, and has a substantially more limited downside — but over the next decade, Markel as a $12 billion company has more potential for real transformative growth than Berkhire Hathaway does as a $350 billion company.

Markel management is incentivized to keep making good insurance and investing decisions that grow the company’s book value, and I expect the power of incentives and the “Markel Style” cultural focus on value and profitable underwriting to keep the company pretty strong and healthy — and I’m not selling here, as I didn’t sell at their last peak valuation in 2008 near $500, but that’s largely because I’ve bought in to the philosophy at Markel and am willing to be patient. Your mileage may vary, of course, and the requirement for patience is real — it took Markel stock almost five years to regain its peak 2008 share price after the financial crisis, so there was a very long time of feeling foolish for shareholders until the stock really started to grow nicely again about four years ago.

Disclosure: I own shares of both Markel and Berkshire Hathaway, and both are among my five largest individual stock holdings. I won’t trade them, or any other stock mentioned here, for three days following publication.

Travis: Thanks for the cogent, thorough explanation of Markel. It sure has been a winner for me and seems like a good bet to continue that way. Do you have any thoughts on WRB?

I have not looked at the details for WRB, but the analysis from Morningstar is fairly compelling. I know Porter Stansberry also had it as one of his favorite insurance companies when his firm did a big data dive on insurance a couple years ago, and that it’s generally a well-respected insurer — the price hasn’t taken off like Markel’s has over the past year and a half or so, though their book value growth in the past five years is also substantially lower than Markel’s.

They have about the same price/book valuation as Markel right now, according to ycharts, and also had a bit of a flattening of book value growth over the past year or so, so it perhaps hasn’t gotten overheated as I suspect Markel has, but it’s also not compellingly cheaper. But I haven’t looked at WRB’s specifics other than to browse the financials and compare the charts of book value and share price growth.

For what it’s worth, the market still doesn’t think Markel is overvalued — the stock is up another 6% this week and at an all-time high. Their quarterly numbers came out this week and they were roughly as expected, good but not surprisingly so, with continued profitable operations and a new book value per share at about $590. The bump up in shares keeps the valuation at about 1.6X book value, still quite rich, but the appealing buy zone for me near 1.3X book value would now be about $766.

Gumshoe, Have your heard any details about their microcap stock that is suppose to take over wireless energy? There is supposed to be an announcement in early June that if you own the stock prior you will more than triple your investment, It has something to do with wireless energy that will effct smartphone I-pads and ettc, they want 2500 for a subscription to their newsletter Financial microcap Millionaires this published by Agora Financial? I just do not have that kind of money to subscribe. Respy, ,Lee

,

Sounds like more pushing of WATT, but I don’t remember covering that specific ad.