This is an ad for the entry level flagship newsletter from Stansberry Research, called Stansberry’s Investment Advisory (currently pitched at $49/yr, renews at $199), and it’s an interesting sign of either sentiment shift or a lack of brand-name pundits that they’re turning the sales pitch for this advisory over to Dan Ferris — Ferris has helmed the Extreme Value newsletter for Stansberry for close to 20 years now, and for a while also ran another more accessible newsletter called the 12% Letter that ended up folding but, at the time (a decade ago or so), focused on finding “world dominator” companies and dividend payers during the post-crash turmoil years. Stansberry’s Investment Advisory has been a more general newsletter under Porter Stansberry, but with Porter mostly retired or having retreated from the bylines now that his publishing company is publicly traded (MarketWise (MKTW)), it hasn’t been promoted as much and hasn’t had a high-profile editor.

That newsletter is still sold with the description, “A monthly advisory that shows you how to make money from the most promising emerging trends and the most influential economic forces affecting the market,” and it kind of sounds like the use of Dan Ferris in these ads, instead of that letter’s lead analyst Alan Gula, means they’re trying to take advantage of the “shift to value” being that next “emerging trend.”

Or maybe they just saw that Dan Ferris got some good attention and solid Extreme Value signups for his “Ten Stock Inflation-Protection Portfolio” pitch a few months ago, and they want to lean into that theme again.

And that’s what this presentation feels like, a junior version of the big “the next crash has already begun” pitch from Ferris that ran a few months ago, with a lot of the same “be prepared” language and big-picture concern about the world falling apart, and inflation remaining critical for a long time.

It’s not just a copy of the Extreme Value ad, however, it’s peddling a less expensive newsletter, and a five-stock investment portfolio instead of ten… and two of those, to meet the rising interest in energy over the past few months, since the Russian invasion of Ukraine upset the oil and gas markets, are oil stocks (we guessed at a couple oil stocks he might like in our last article, but he didn’t really specifically hint at any).

So… shall we begin?

This is how the interviewer, fellow Stansberry editor Daniela Cambone, introduces the Dan Ferris plan…

“So if you’re at all worried about what’s about to happen next in the markets… this interview is for you.

“You’ll get, for free, the details of a dead-simple, one-step investment approach that could show you a series of triple-digit gains or higher, starting right now.

“Using only regular stocks – nothing unusual or complicated.

“A way to not just beat inflation – but benefit from it.”

And the big-picture warning that the markets still feel like they’re at a “top” is pretty similar to last time around, even starting with the same script for the introduction…

“What we’re seeing today is exactly what a big, long-term TOP in the markets looks and feels like.

“We’re watching the bubble burst in front of our eyes, and people are just shrugging at it – which is terrifying.

“The attitude in the markets, at least until very recently, has been that it’s impossible to lose.

“It’s a mania. ‘Buy buy buy.’

“The drugmaker AstraZeneca is trading for 447 times earnings.

“MercadoLibre, the so-called Amazon of South America, 583 times earnings in recent days.

“But that’s nothing.

“The business software company Workday, a $50 billion company is trading at over 2,000 times earnings.

“This is madness.

“But stocks only go up, supposedly.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“So you have meme stocks like AMC, whose actual business is in steep decline, and was up 2,000% for no reason.”

So that’s mostly the same thing he was saying back in February, when Workday was a $50 billion company (it’s down to about $40 billion now), though the market has, of course, already done some correcting from those near-peak valuations. And some of it is just shock value, of course — AstraZeneca was technically at 447 times earnings, but that was because of some one-time charges, when it comes to the adjusted earnings that most people watch it’s at about 25X trailing earnings (and MercadoLibre (MELI) is a comparative bargain, down to “only” about 100X earnings now).

And yes, that downturn has taken with it some of Ferris’ ten-stock portfolio at that time, most of those stocks have fallen pretty similarly to the market, other than the gold names, which are up 10% or so. That doesn’t necessarily mean anything, this is an inflation-fighting portfolio he said should be put away and ignored for years, so we should suspend judgement for now, but I guess we can at least conclude that he doesn’t think the ~10% drop in the markets since his last piece means we’ve gotten the worst behind us.

And he says as much…

“So the first thing I want to say to your viewers is this: This is it. This is the moment when you must act. Now. Not when stocks are down 50% or 70%.

“This is when you take action that saves you from having to feel the way you did in 2008.

“And I don’t know, of course, where the market will be when you see this. The volatility’s been so high, and we’ve had some brutal days… weeks… even months here and there.

“But until this market falls 80% or more – in my view – the fat lady hasn’t sung.”

That would be a dramatic fall, indeed — that would mean the S&P 500 would have to keep falling for a long time — the SPY ETF (the most popular ETF tracking that index) has already dropped from about $475 to $411, and an 80% drop would mean dropping below $100, for the first time since 2009. If he means the more richly-valued growth stocks in the Nasdaq, that would mean the QQQ ETF, which tracks the Nasdaq 100 and was the huge winner during COVID, would have to keep falling much further… it’s down about 25% now, but to reach 80% it would have to get back to levels we last saw in late 2013.

I don’t know where Dan gets his 80% prediction from, but that’s a rough drop — the broad market really fell “only” about 50% during the 2000 and 2008 crashes, so that really gets us back to the truly remarkable market implosions: the Dow’s wild drop during the crash of 1929 and the Great Depression, when the market fell almost 90% from peak to trough and took more than 20 years to recover and reach those “roaring 20’s” highs again, or the dot-com crash for the Nasdaq, which lost roughly 80% of its value from the peak in 2001 to the trough a couple years later, and took about 15 years to recover. And that’s just the broad market, many individual stocks did far worse or never recovered (like Cisco Systems (CSCO), which is a fairly popular “value” stock recommendation today, and has been a strong and successful company for 25 years, but has still never retaken its dot-com highs of 20 years ago).

So that’s the fear… that the most radically overvalued market in our memory will lead to the most radical crash in 90 years. What do we do about it? Well, his primary concern is inflation…

“Because here’s the key thing. If inflation over the next decade plays out the way I’m expecting, it’s a financial disaster even without a crash.

“Think about that, even if I’m completely wrong – and most of your guests are completely wrong – and a crash doesn’t materialize anytime soon… which I seriously doubt, by the way – but even then if growth stocks sort of hold their altitude and the market as a whole is just choppy and moves sideways on average, you’re going to start losing money.

“Inflation is going to eat the value of your cash, and it’s going to eat some of the value of every business on the planet.”

So that’s the deal… he wants us to buy into the assets he’s recommending that will offer crash protection and inflation protection. He repeats his “freebie” recommendation to own gold, with his recommendation being the Sprott Physical Gold ETF (PHYS), same as it was in February in his ad for his pricier newsletter, and then the part introducing the “hard assets” he recommends seems like a copy of the previous ad:

“You absolutely must own the assets that benefit during inflation. That hold their value – first of all. And better yet that actually soar when all of this is happening.

“That starts with so-called hard assets like oil… gold… land… timber… Things like our food supply… things like the real, physical mines that keep our world up and running.

“Why? Well for one thing, no matter what kind of calamity strikes… we don’t stop needing food. We don’t stop needing energy. These things keep operating and keep generating cash, if they’re run well, or the world stops.”

Interestingly, the one thing that’s in that snippet which wasn’t in his February ad is oil, the commodity that has outpaced all others since February. That’s no Ferris’ fault, of course, oil isn’t rising because of inflation or because it’s a hard asset, it’s rising because of the supply shock of the Russian invasion, but it’s still interesting.

So yes, the general theme for fighting inflation is still “commodities” … more from Ferris:

“Commodities are the cheapest they’ve been relative to stocks since the lows of the dot-com bubble. Not the housing crisis… the dot-com bubble.

“They’re in almost exactly the same place as they were 20 years ago!

“And the last time we had this setup they went on a 500% run.”

Beyond that repeated recommendation of the Sprott Physical Gold (PHYS) ETF, though this is mostly still an equity strategy — buying companies that are exposed to those commodities, not trading the commodities themselves…

“What most people don’t know is that have there are handful of unique stocks that have the qualities I’m talking about baked in.

“I’m talking about high-quality businesses that you’d want to own anyway… that are often backed by world-class physical assets… and whose business essentially give you leveraged upside to the prices of things like food… energy… and commodity prices.

“So you can get the same kind of upside, potentially, as using options to play this boom… but in simple, ultra high-quality stocks.”

So what are the five stocks he recommends for inflation protection and crash protection? The clues are light, but let’s see what we can come up with. More from Ferris:

“… every one is the kind of overlooked or backdoor play that most people will never find, that gives you potentially 3x more upside than the obvious thing that people will buy, if they’re smart enough even to use this strategy at all.”

And unlike last time, when oil was mostly an afterthought in the inflation story pre-Ukraine, it’s the headliner today…

“We’ve identified what we believe is the No. 1 Inflation Protection stock in the world. Hands down….

“We consider it one of the best opportunities of the next five years… and one of the best stocks we’ve EVER found in more than 20 years of publishing research.

“In this environment, it could climb by hundreds of percent if things go right.

“We call it the Best Oil Business on Earth – and with good reason….”

This is an oil royalty stock, and we get some oblique hints about this company by way of reference to a second secret company…

“And keep in mind, readers of our flagship publication… the one that everyone should start out with… are sitting on a potential triple right now in a similar stock. But it’s not our absolute favorite.”

And it’s not clear that he means the same stock, but he goes on to provide this example:

“… there’s an extraordinary company in Texas. I can’t mention the name because I have to protect it for subscribers.

“All it does is own a huge swath of oil-rich land. This is key. It doesn’t do any of the work of building rigs and extracting oil. And it doesn’t take any of the associated risk, either. Instead, it lets other folks do that, and simply collects a stream of royalty payments in exchange.

“So while Exxon has 63,000 employees… this company has less than 100, because essentially all they do is cash checks.

“And, Dani, this company is up as high as 4,000% since 2011.”

So that’s clearly Texas Pacific Land Corp. (TPL), which they don’t name because it’s presumably a current recommendation of one Stansberry newsletter or another. That’s a massive landowning company that came out of the bankruptcy of a Texas railroad decades ago, largely ignored and forgotten until the Permian Basin, where a lot of their land happens to be, turned out to be the fracking-fueled bonanza oil field of the 21st century. It would be pretty easy to have a triple in TPL right now if you bought it anytime before 2021, it’s been on a tear.

But we’re told that their favorite company is similar… and smaller…

“Very similar, but it’s around one-fifth the size. One reason we think the biggest upside is still to come….

“But if you could wave a magic wand and create the perfect stock for a rise in oil prices… this is pretty darn close to what you’d get.

“Nobody knows about it.

“It’s a royalty company. One of the best setups we’ve ever found… in what’s probably our favorite type of business that we’ve ever shared with readers….

“I think it’s 10 times better than any commodity play you’ve likely every heard of or considered.”

And that’s the heart of the pitch, for this special recommendation that they say is “The No. 1 Stock on Earth to Beat Inflation”, though it sounds like that one stock is also one of the plays in the “five-stock inflation protection portfolio.”

What other clues do we get about this? Just that it has recently had a dividend yield of about 6%. And that there are actually two oil royalty companies in this five-stock portfolio… this is what they say about the other one:

“There are five stocks in total. And besides “the Best Oil Business on Earth” there’s another oil royalty play that’s very similar. It’s neck-and-neck for the best.

“These are THE guys you want on your team in the next supercycle. They have nearly 24,000 royalty acres. And all they do is sit back and collect the royalties for years, sometimes decades.”

The first one is about one-fifth the size of TPL, which would mean a market cap of something like $3-4 billion, and pays a yield of something near 6%, the second one has “nearly 24,000” royalty acres, and that’s it. So we’re left with a little bit of guessing….

For the first one, we’ll go with Black Stone Minerals (BSM), which I actually think is one of the more interesting energy royalty companies out there. It does have a market cap of about $3.5 billion today, and the trailing dividend yield is a little over 6%… though the forward yield, assuming oil and gas prices stay pretty elevated, is likely to be closer to 10%.

I find this interesting because it has such massive scale, with 7.4 million net acres of mineral right ownership, and that gives it long-term potential — they’re spread out with mineral rights in almost every state that has any energy production at all, and with particular concentration in the Haynesville, Bakken and Permian basins, and they’ve spent decades acquiring those mineral rights around the country, starting from Black Stone’s roots as a lumber company in East Texas that shifted to focusing on mineral rights in the late 1960s… but only about a quarter of their rights are currently under lease or producing. They are more levered to natural gas than to oil (about 75% gas production last quarter, 25% oil), so they benefit from rising LNG exports as well as from the continuing replacement of coal plants with natural gas plants, though that does mean the explosive returns of high oil prices do not have quite the same impact on their revenue.

The shares have done very well of late, as you might imagine, since all energy stocks have soared following the Russian invasion of Ukraine, so they’re now trading at about 10X revenue, which is pretty close to the top of the range for their seven years as a public company, and the trailing dividend yield is pretty low, historically… though that’s because investors are looking forward, not backward, and the company increased the distribution dramatically last quarter, to 40 cents, reflecting both a higher level of production and some optimism about the high levels of activity in the Haynesville shale that should lead to more production in the future. They do have some hedging in place for gas and oil prices, which will mean that if prices keep soaring they will not maximize their income… but that should also help stabilize revenue if prices fall back down (if, for example, the Ukraine war comes to an end and Russia is suddenly welcomed back to the community of nations). If they can keep up this 40-cent distribution, which was well-covered by their cash flow in the first quarter, that would be a yield of over 9% at the current price.

And what’s the second one? Well, the only clue we get is “24,000 acres” — and that does actually help narrow it down a bit, since that’s quite small for a royalty company or a trust. There are two possibilities that stand out… one is PermRock Royalty Trust (PRT), which is very small and owns net profit interests on about 23,000 net acres in the Permian Basin, most of them operated by Boaz Energy (which created the trust about five years ago). And the other is Viper Energy Partners (VNOM), which is a limited partnership, not a trust, and owns about 24,000 acres of mineral interests in the Permian that were spun out by the operator, Diamondback Energy, in 2014.

Given that oil trusts are a little tricky, mostly because they are far more passive than limited partnerships (a trust can never buy or invest in another property, they exist just to pass through the cash flow to shareholders, while partnerships can and do reinvest some cash flow in growth or issue more shares or borrow money to expand), I’d guess that VNOM is the more likely pick here. That’s essentially a wild guess.

I think BSM stands out as being the most interesting name in this space, mostly because it’s far more diversified and has more open-ended potential than a royalty play that’s primarily tied to just one region, or mostly to just one operator, but I don’t own any of these at the moment.

For what it’s worth, VNOM has also been lifting its payout rapidly, it has more than doubled in the past year and the first quarter distribution was 67 cents per share, up from 47 cents last quarter — that distribution is well covered by their 96 cents of cash available for distribution, so they also did buy back some shares, and they expect production to rise by 1-2% this year on their royalty lands, which, given the much higher oil prices, should allow their cash flow to keep increasing nicely. The stock has reacted very positively to all these growth numbers, so right now, if the distribution stays steady, they would provide a distribution yield of about 7.7% at the current price of $35.

Do keep in mind that partnerships like VNOM or BSM often distribute cash in excess of their taxable profits, thanks to depletion charges, so a big chunk of the distribution is a return of capital that is tax-deferred until you sell the shares (more than half of the payouts this year for VNOM should be in that category, for example), though you lose some of that tax benefit if you hold shares in a tax-deferred account (like an IRA), and you do also have to deal with the hassle of the K-1 filings when you do your tax returns.

If oil and gas prices stay high, all of the oil royalty names will likely do very well. I’d pick BSM out of that bunch, if forced to choose today, mostly because of the more open-ended potential for their huge inventory of un-leased mineral rights over the long term, but in the short term they’ll all likely trade together.

What other clues do we get about what’s in this portfolio?

“There’s also a world-class gold play. Best of the best.”

I would guess that they’re probably not recommending Sprott (SII) here, since that’s Dan’s Extreme Value favorite in the gold space, and they probably want to keep it to the higher-priced letter… and there’s no hinting about it being a gold royalty company, which is a strange omission given the talk throughout the presentation about the value of royalties, so I’d go out on a limb and guess that they’re actually pitching a fairly inexpensive global gold miner this time around.

Might as well go right to the top, so we’ll pencil in Barrick Gold (GOLD) for that. They’ve been paying down debt and getting a little religion on cost cutting, and have tremendous reserves, and they’re certainly a lot cheaper than gold royalty companies (trailing PE about 19, EV of only about 6X EBITDA). That’s just a guess, really, since “world-class gold play” is pretty much the only thing they say by way of clues. I’d personally stick with the royalty companies for long-term gold exposure, even though they’re always more expensive than the miners — they don’t face inflationary pressures like producers do (diesel fuel, employee costs, etc.), and they tend to survive downturns much better, but if you want to go with more leverage to gold from an actual miner, Barrick is certainly one of the best and biggest.

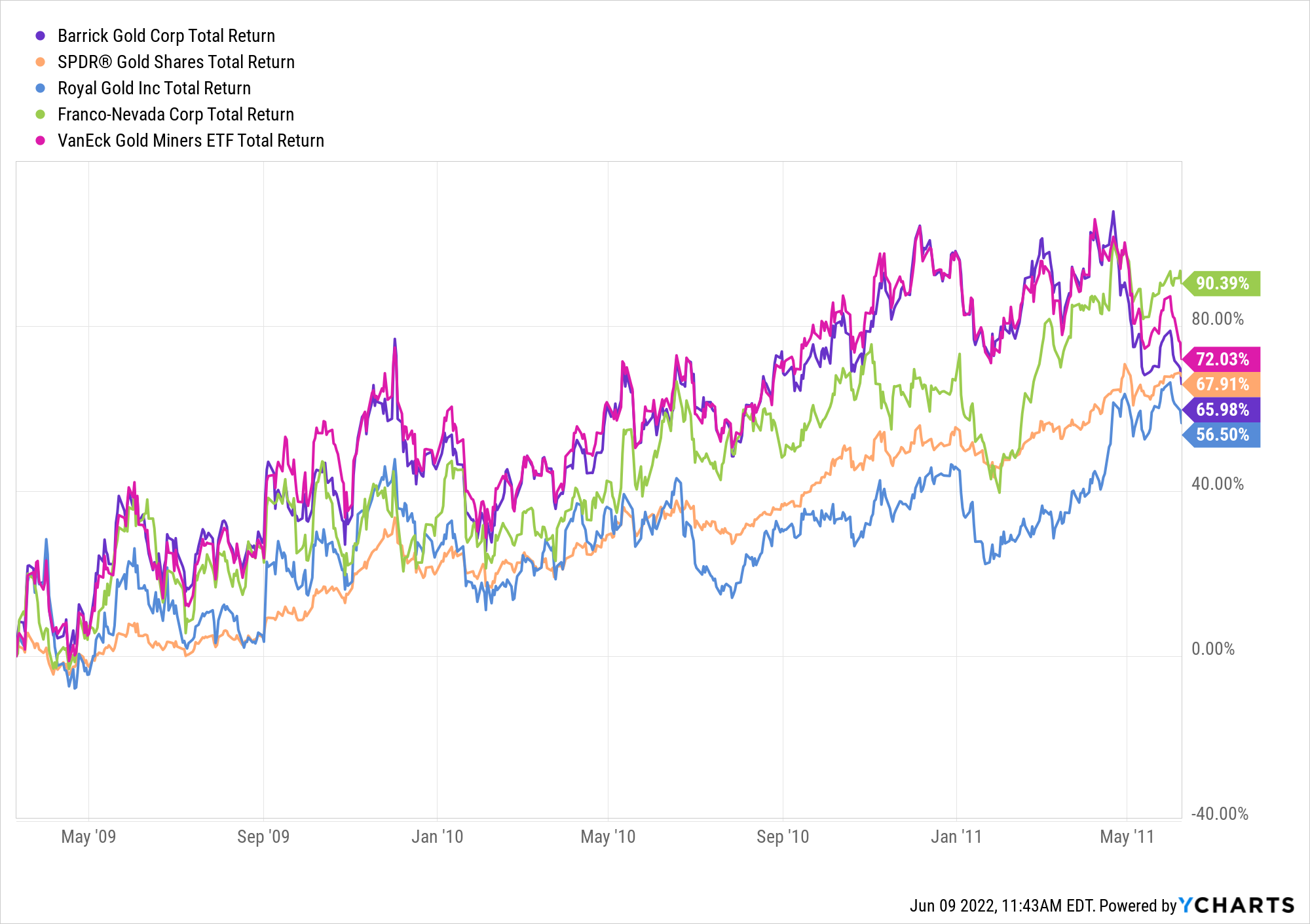

I own Sandstorm Gold (SAND) and Royal Gold (RGLD) in this space, mostly because they’re perennially cheaper than industry leader Franco-Nevada (FNV)… I think various Stansberry letters have recommended all three of those at one point or another, but I’m guessing they’re not going the royalty route with this one. In case you’re wondering where to get gold exposure, here’s the relative performance of a few of those over the past decade — gold itself is up about 10%, Barrick is down about 40%, a bit worse than the average large mining stock (the Van Eck Gold Miners EF is down about 25%), Royal Gold is up 65%… and Franco-Nevada is up about 270%… it’s hard to buy miners when you see that kind of history.

Though, to be fair, sometimes the miners, even big miners, do a better job of keeping up with gold prices when they’re moving quickly — coming out of the 2009 crash, when gold soared 60-70% over the space of a couple years, there were times when the gold miners were the better bet — here’s that period of early 2009-mid 2011 when gold soared, at one point Barrick and the other big miners were showing roughly 2X leverage to the gold price, up roughly 100% when gold was up 50%. If you want to be nimble and bet on rising gold, you might do better with a big miner, or even more spectacularly with a small and growing gold miner that has the good fortune of opening a mine or making a big discovery around the time that prices are soaring, but if you want to just bet on gold and let your holdings compound over time, the royalty companies tend to be more appealing, mostly because they don’t go bankrupt or have massive cost overruns during the hard times.

OK, so that’s guesses for our first three stocks– what about the others?

Here’s what we get for clues:

“One is a large company that I can almost guarantee you wouldn’t think of as an inflation hedge. It’s an elite global business. We cannot live without it. If it disappeared tomorrow, the world economy would have a heart attack.

“This is the infrastructure behind keeping your lights on… getting your groceries… your Amazon purchases… you name it.

“And the key thing is – when prices go up, this company makes more money.

“It’s actually very similar to the royalty model.

“But not just in resources. A royalty on practically everything.”

Hmmm… OK, a royalty on everything. I’ll bite, what else can you tell me about it, Dan?

“… this company owns very valuable assets that connect businesses, banks, governments, and billions of people worldwide every single day. Assets that provide big time protection for the share price, because they don’t just evaporate in tough times, like the financially engineered so-called profits of a lot of companies.”

OK, so again we’re pretty short on clues here… but this sounds like a digital infrastructure company, and if it connects billions of people worldwide every day, I would guess it’s one of the major financial networks — probably a payment network.

The two obvious global leaders there are Mastercard (MA) and Visa (V), and Visa is a little bigger and a little cheaper, so we’ll throw that out as our guess. It could be that we’re dealing with something a little more esoteric, like a data center or cell tower REIT, or a telecom provider, but if we’re looking for simply riding with inflation, and really touching billions of people, it’s pretty hard to beat a ubiquitous credit card and money transfer network — as inflation goes up and the prices for goods and services rise, the little slice that Visa collects as their fee for the transaction rises exactly in tandem. Yes, kind of like a royalty on almost all retail commerce, everywhere.

And while there are plenty of disruptive forces in “fintech” that aim to supplant or replace the credit card networks, from cryptocurrencies to proprietary networks like Square or Paypal, and we have heard for years that some new tech will beat out Mastercard and Visa, well, it hasn’t happened yet. Not even close. And as cash slowly dies and cryptocurrencies experience their growing pains (including transfers that often cost more than credit card fees), it seems unlikely to happen anytime soon.

Visa is still growing, still sharing a near monopoly with MasterCard in many countries, and still has a billion or more cardholders using its service every day (I think there are close to 4 billion Visa cards out in the world right now, though many people obviously carry several of them). The company is not cheap when it comes to the PE ratio, but, as you would expect for a near-monopoly with unlimited scalability, it has almost never been cheap in its 14 years as a public company… and it is, by most measures, a hair cheaper than the smaller Mastercard, and has generally bottomed out with a valuation of 25-30X earnings, so the downside is probably fairly limited (it’s at about 33X trailing earnings right now, and earnings have been growing nicely as in-person commerce and international travel pick back up — if it falls to 25X expected 2022 earnings, that would be about $175, a drop of about 15-20% from here).

If you want to step out into something a little more aggressive, PayPal (PYPL) is the most established and, valuation-wise, probably the most interesting of the “upstart” fintech names that has a broad enough global reach and strong enough brand to be a serious competitor, and, after the collapse from their highs back in November, it’s similarly valued to Visa and Mastercard, at about 28X forward earnings, and might end up growing faster.

And… that’s it, those are the clues we get from Ferris. We get to four guesses for you, among five stocks, assuming that the PHYS gold ETF isn’t actually one of his five — and they might not be the precise stocks Ferris is teasing, since he doesn’t drop many clues, but they all should provide some inflation protection for a portfolio. Oil royalty companies see their payouts rise with oil and gas prices, gold miners or royalty companies hold up well because gold typically keeps its value during long periods of inflation (though it’s not any great shakes as a short-term inflation protection asset, and it also tends to fall, in dollar terms, when interest rates are rising), and core financial infrastructure companies who essentially take a tiny percentage cut of almost all consumer activity will naturally keep pace with inflation as long as consumer spending doesn’t fall off a cliff.

The only thing missing from that list, if you’re thinking of a typical “inflation protection” handbook, is probably real estate, which has historically been a good asset during inflationary times… but is also coming out of some wild swings in different segments, with manic home prices and empty urban office buildings throwing off valuations for a little while. Some names there that I own and like would include Brookfield Asset Management (BAM), which also benefits from interest in infrastructure, or Kennedy-Wilson (KW) on the smaller side.

Or maybe timber, which has already had a wild run and come back down a bit as the housing market is flashing warning signs — the big remaining timber play is still Weyerhauser (WY), which has a trailing yield of close to 6% but might not repeat the big special dividends that got them there (the “regular” dividend is only about 2% now). Or farmland, which is a popular “crisis” investment even though the two publicly traded REITs in that space got a bit overheated earlier this year (that’s Farmland Partners, FPI, and Gladstone Land, LAND).

Still, though, the best broad asset class to own during periods of inflation tends to be… stocks. And particularly, the stocks of strong companies who have very manageable (or no) debt and own powerful brands that allow them to keep pricing power, raising their prices to keep up with their input costs without hurting demand very much — which, of course, is why those kinds of companies, PepsiCo (PEP) and Hershey (HSY) and Coca Cola (KO) and Altria (MO) and Diageo (DEO) and whatever other big brand-owner you can think of, have seen their stocks mostly hold up pretty well during the recent upheaval. Such companies are rarely cheap, but they also rarely fail. Similar to Visa (V), actually, which has held up very well this year despite some negative attention, which might lead to tighter regulation, following the recent increase in their swipe fees.

And, of course, the best way to protect your savings from inflation remains the Series I Savings Bonds from the Treasury department — I’ve been pounding the table on those for a few years, they’re one of the few ways that the little guy gets a better deal (they’re limited to $10,000 a year, and will provide a compounding return that at least matches the rate of inflation, with no real downside risk, though there are some other limitations and rules — I last wrote about I Bonds back in April if you want more background on that, right now they’re earning 9.62% interest for the first six months if you buy before October, when the rate resets again).

So… a somewhat disappointing outing for the Thinkolator, no 100% certain answers on the five inflation fighters Ferris is teasing this time around… but hopefully we’ve given you something to chew on. For more ideas along those lines, check out our story from the the earlier Ferris pitch, when he sold his 10-stock inflation protection portfolio for Extreme Value subscribers (we were able to name about half of those, and provide some other interesting ideas along the way).

Have any favorite places to hide during inflation? Other ideas that might be a better match for Ferris’ limited clues here? Let us know with a comment below… thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of Brookfield Asset Management, Kennedy Wilson, Sandstorm Gold, Royal Gold

Visa and Barrick are correct.

Thanks… I’ll take a .500 batting average on the guesses 🙂

.400 but who’s counting?

I only guessed at four, so I’m being generous with myself 🙂

Does that mean the other guesses are incorrect — if so what are the other three

Stansberry Investment Advisory: 5 stocks

The stocks are as follows: Barrick Gold (GOLD), Texas Pacific Land (TPL), Visa (V), PayPal (PYPL), and Freehold Royalties (TSX:FRU or OTC:FRHLF).

Sneaking TPL in there as one of the picks, too, eh? Dastardly move. Thanks for the feedback.

Interestingly enough, Freehold was one of the stocks I tossed out as a possible idea for Ferris’ last inflation pitch in February. I’d likely take BSM over FRU.TO/FRHLF, but there are quite a few similarities in valuation and geographic diversity, and Freehold is more weighted to oil than BSM, it’s about 40% natural gas vs. 75% for BSM.

I’m holding both BSM & FRU…happy w/performance of both so far!

Three of his “picks” (GOLD, V and TPL) have been in the portfolio since 2020. You get partial credit Travis for PYPL as that is one of his new ones. lol

Freehold Royalties is on the list of five. TSX:FRU isn’t available from my brokerage account and this keeps me out of this position.

i was able to get it using ((FRHLF).

I am wanting to know what the “”Next Gen Coin”, is that is being hyped.

etherium

Travis covered that one here: https://www.stockgumshoe.com/reviews/strategic-fortunes/whats-kings-the-next-gen-coin-tease-says-musk-dalio-and-cuban-are-loading-up/

I guess it would be uncharitable of me to mention that PYPL has been a disaster as an inflation protection or any other kind of long investment this year. But there’s always better days ahead, I suppose.

Indeed, to have any optimism for that one you’d have to look at the potential future… not at what the price was last Fall. Their income might be inflation-protected, but that doesn’t necessarily mean their valuation always is.

Agree – I cannot find anything at all compelling about PYPL at the moment.

Thanks for your great work that keeps many of us with you FOR YEARS. I have a lot to say but little time except to share my best hiding place this year. The stock is SAFM, a chicken producer in Mississippi. Bought 3/15/22 @ $178 after my former billionaire boss bought over half a million shares. It’s gained nearly 5% a month & closed today 6/9 @ $202.74. After hours, it’s up to $203.72. It beat 2nd Qtr earnings by a dazzling $6.77 and Zacks and others claim it’s significantly undervalued.

It’s been a good year for chicken!

way back when Dan Ferris was pushing the 10 stock letter i decided to go for the commodity’s that he was recommending and that i knew about from your letter. it seemed like a good idea to me. but i went overboard. i bought the five that you came up with plus Peabody Energy (BTU), Gladstone (LAND) and Freehold Royalty (FRHLF). plus a few share’s of Gold since that was going to save everybody. the big winner here is Peabody although i haven’t checked today.

p.s. need a bigger place to type

“Haven’t checked today” is probably the best advice for any investment — I guess they have to pitch the urgency of inflation, but it really compounds over time and most investments that do well in inflationary times will not perfectly respond to the CPI in any given quarter, they’ll probably need a lot of time, too.

Well, other than oil stocks during an oil shock, I guess. Those perk up right quick 🙂