I guess this is shaping up to be another “marijuana week” here at Stock Gumshoe… this latest pitch talks up a chance at making five times your money on “a marijuana stock opportunity that almost NO ONE is talking about yet.”

Which, of course, is music to our ears — we do love a good mystery!

The newsletter being pitched is Alpha Investor Report (“on sale” for $47/yr) from Charles Mizrahi, who has teased some interesting stocks for us in the past (the two that stick in my mind are Xilinx (XLNX) a couple years ago and Huntington Ingalls Industries (HII) several years ago, mostly because I missed those appealing long-term growers and was grouchy about it… though I do own some XLNX shares now).

And, like some other pot stock pitches we’ve seen, this one is sold to us using the “picks and shovels” metaphor — the idea being that in a gold rush, you want to be the one selling the picks and shovels to the miners, not the guy digging a hole in the wilderness and hoping for a score. It’s an appealing story, and one that has become easy shorthand for investors (we’ve been teased about “picks and shovels” plays on bitcoin, iPhones, actual miners, you name it), though, of course, it doesn’t always mean you’re going to get rich. After all, the shovel salesman doesn’t take nearly as much risk, but he does make a lot less money than the guy who discovers the gold.

Here’s a bit from the ad:

“The best way to reap true, lasting, life-changing profits is to identify the pick-and-shovel stocks that are fueling it.

“Like the company I’m going to shed light on for you in just a moment.

“My analysis indicates that this one stock alone has the potential to hand you up to 500% as the legalization of marijuana continues to unfold — with a greater degree of safety and dependability than any wild-eyed penny stock can ever give you.”

OK, so I’d get that 500% out of your mind… though he’s probably not too far wrong on the “safer and more dependable” bit, at least if you’re comparing this to profitless penny stocks. What else?

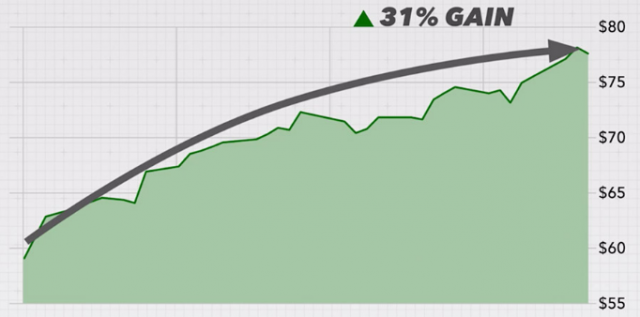

“My #1 Pick-And-Shovel stock has posted a 31% gain in less than two months”

From the chart he shows in the presentation, that means it went from about $59 to $78 over some recent period of time.

What kind of “picks and shovels” does this company sell? Apparently it’s something to do with security. Of marijuana companies, he says that…

“… their runaway success has created two huge problems.

“The first is finding a safe place to store the mountains of money they’re making.

“The second is finding a safe way to move the marijuana itself….

“All of that cash on hand makes for a VERY tempting target for thieves.

“Likewise, with marijuana fetching as much as $3,000 a pound in some states, the marijuana itself makes for an irresistible target as well.

“As California edibles producer Mark Mason told Rolling Stone magazine: ‘We carry more cash than banks. You can’t walk into a bank and get $300,000 in cash. You’d make more money robbing us. It just feels like, wow, now that my business is completely legal, it’s more dangerous than ever.'”

OK, so if you’re writing a hardboiled mystery about thieves, you’re probably thinking that marijuana is one of the last great cash businesses, and maybe that’s who your gang of robbers should target (sorry, I still miss Donald Westlake, his Parker and Dortmunder gangs would have had a field day with legal pot shops bursting with cash)… but what does that mean in terms of investing?

OK, so if you’re writing a hardboiled mystery about thieves, you’re probably thinking that marijuana is one of the last great cash businesses, and maybe that’s who your gang of robbers should target (sorry, I still miss Donald Westlake, his Parker and Dortmunder gangs would have had a field day with legal pot shops bursting with cash)… but what does that mean in terms of investing?

Well, we’re being teased with a security company of some kind… from the ad:

“This Virginia-based company has the ability to provide marijuana businesses a safe, guarded way to store all their cash.

“Plus, they also give growers a safe, guarded way to get their harvest to the dispensaries that buy their crops.”

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...

And they’re international, too…

“… they’re set up to do it not only across the U.S., but throughout all of North and South America.

“They’re already a major player in Canada, where marijuana was legalized nationwide late last fall…

“… one of the largest cannabis companies in Canada, if not the world, has already inked a multi-year deal with them….

“… they are poised to dominate the market in both North America and South America. Two ENTIRE continents.”

So who is it? This is, sez the Thinkolator, the name on the armored car fleets that probably make their way around your city: The Brink’s Co. (BCO)

And in case you want an illustration of the match… here’s my version of the chart that I’m pretty sure Mizrahi is using in his ad, which would be “within two months” from the December 24th lows…

And here’s a snippet of the chart he used in his ad, just for comparison’s sake (you can see the whole ad here if you like):

This is what the stock has looked like over a longer period of time, in case you’d like some context (this is total return over 25 years or so):

So you can see that Brink’s has been recently dominated by a huge move that the stock made in 2016… where did that come from? Is that a marijuana story? The big stuff like share count, revenue and earnings didn’t dramatically peak in any way in 2016, so it must be some kind of change in the story.

I haven’t ever researched this one before, but it looks like it was a restructuring, forced at least partly by activist pressure from Starboard starting in 2015, that got the Brinks truck rolling, jolting it out of the 5+ year period of relatively flat performance following the financial crisis by replacing the CEO, borrowing money to do some buybacks and bolt-on acquisitions, and perhaps improving the operations to some degree.

And it has been working pretty well, at least according to their latest investor presentation, with acquisitions (particularly of competitor Dunbar) and margin improvement helping to boost cash flow and earnings.

The challenge, I suppose, is that security solutions like this are generally pretty low-margin — even one of the largest companies in the world like Brinks ends up netting a very low net profit margin, usually 2-3% or so. There are presumably economies of scale in the security business, particularly when it comes to systems and branding and the network effect, but there aren’t necessarily huge opportunities to get dramatically more efficient when it comes to actually providing the service… you need to have the armored trucks and the people and the security monitoring, and cutting back too much on the service to compete on price means you’re going up against smaller companies who are much less worried about risking their reputation.

They do have some good international breadth, though, and there is certainly some value in having a large network of people and equipment that can provide assurance, particularly to larger companies who have growing footprint in the industry, so I guess the hope is that they’ll lever the route business they already have with banks and jewelry stores and other cash-heavy retailers and just tack on some pot business on top.

On the flip side, we’re also likely going to be moving to a less cash-intensive marijuana industry — security will still be important, just like it is for a liquor store, but as banking rules are relaxed marijuana companies will be able to accept credit cards and cut down on their reliance on cash, and cash management is really the core service that Brink’s offers. That might be a gradual thing, since not everyone is going to want to see the “High Times Dispensary Co.” on their credit card statement, but I assume we’ll move to a less cash-dominated business.

Securing the actual crop and the product will be important, too, but that will probably also evolve. Presumably we’ll end up with some kind of security presence that puts the transport and logistics for marijuana somewhere inbetween those used by liquor distributors and pharmaceutical distributors — I’m guessing that in ten years we won’t see every marijuana dispensary getting their shipments by armed guard, but for the next few years we certainly might.

That’s all my guessing, though, what we’re dealing with is a large international security company, mostly an operator of armored truck routes that provide cash management, that’s being teased as a marijuana “picks and shovels” play. Marijuana is a vanishingly small part of their business in revenue terms right now, though that could, of course, shift over time if they can grow that segment… so how do the financials of Brink’s look now?

Well, the international part has been a drag… as you might expect. Reporting South American or European earnings in US$ has been a negative of late, thanks to the strength of the dollar, and a few of the countries where they have long had a substantial presence have certainly been going through hard times — notably Venezuela and, to a lesser degree, Argentina (though it might be that the worst is over for those businesses, at least in terms of currency-related writedowns).

Marijuana companies are not big enough customers yet that they get any emphasis from the company in its reporting, but they did just sign a large partnership deal with Canopy Growth back in November to provide secure logistics and cash management services… with part of that deal meaning that Brink’s gets to cross-sell to Canopy’s growers and retailers, so that could bring some growth in the Canadian market.

That was worth a quote from the CEO of Brink’s, but since Marijuana has not yet come up in their forecasts and wasn’t in the latest conference call, I’d hesitate to change my expectation for the future of the Brink’s business just because they’re trying to get more into serving the Canadian pot business.

I can see why they’d be interested in jumping on the pot business — after all one of the great risks to Brink’s and its competitors is that their services become less necessary as the world becomes more cashless (while they haven’t issued any press releases about marijuana, they did about the argument that followed Amazon’s flip-flop over going cashless with its “Amazon Go” stores) — but the notion that it’s going to transform the company dramatically in the short term seems very over the top. Doesn’t mean Mizrahi is wrong, but I think his ad pretty absurdly overhypes the marijuana connection and its ability to drive results… the only analyst note I’ve seen about Brink’s and cannabis guessed that it might provide as much as $250 million in revenue by 2022, which sounds impressive and would, I’m sure, be a welcome new growth avenue for Brink’s, but that would also represent only about 6-8% of the business at that point. We’ll see how it turns out.

They will not, by the way, be getting into the United States pot business unless we get a much clearer legalization decision from the feds — Brinks has major relationships with all the big banks that are worth a lot to them, and I’m sure they won’t jeopardize that by dabbling in semi-legal businesses. So that’s another possible growth driver, though probably still of marginal near-term importance, if we see federal legalization make some real progress.

They will not, by the way, be getting into the United States pot business unless we get a much clearer legalization decision from the feds — Brinks has major relationships with all the big banks that are worth a lot to them, and I’m sure they won’t jeopardize that by dabbling in semi-legal businesses. So that’s another possible growth driver, though probably still of marginal near-term importance, if we see federal legalization make some real progress.

Brink’s is not particularly expensive, probably partly because investors are hesitant about the declining importance of cash — it remains a bit cheaper than most of the companies it considers peers (business-to-business service companies that offer regular route services, like Cintas, Waste Management, Rollins or Stericycle), and if you like the look of their strategic plan (they outline it pretty well in the latest presentation) you can probably justify buying the shares based either on the relatively sane PE ratio (14X next year’s earnings forecast) or the anticipated growth in cash flow that they see following the third year of their restructuring/turnaround plan, but betting on a 100% return is well outside the consensus (analysts on average expect about a 30% return over the next year — which is pretty impressive in itself, but not quite at “newsletter hype” levels). There’s a good but slightly-dated summary of Brink’s in a December Bloomberg article that can give you a quick backgrounder.

So there you have it… an interesting stock, a rational valuation, but the connection to marijuana is a bit tenuous and not likely to be the reason for the shares soaring unless that takes hold as a new “narrative” in the market. Sound like one you’d like to dabble in, either for marijuana or non-marijuana reasons? Let us know with a comment below.

Disclosure: Of the stocks mentioned above I own shares of Xilinx. I will not trade in any covered stock for at least three days, per Stock Gumshoe’s trading rules.

Brinks as a “pick and shovel” play for Pot has got to be the silliest “buy my newsletter to find out the name of the stock” ploy ever. What a joke, and thank you Travis (as usual) for shedding light on this absurdity.

Congress is in the process of considering a fair banking act that will allow banks in the federal system to do business with pot companies that are in states that have made them legal.

Yep, I think most folks expect that to pass eventually, and for the US market to keep moving toward at least full medical legalization, but the timeframe and specifics are still awfully hard to predict. For Brinks, they have too much to lose to push the envelope for what would be a smallish business, they can easily afford to wait. Not all service providers will wait, of course.

With our most profound thanks, I think we can all agree that Travis continues to teach everyone about the “real world” and save us from the unscrupulous “pitchsters.” I believe his three words, “…. pretty absurdly overhypes ….” applies universally to all these types of pitches, webinars (what a joke!) and other devious means these people use to get the unsuspecting, naive, greedy and unknowledgeable to part with their money, regardless of the industry in which a subject “mystery” company is involved. There oughta be a law — maybe there is! Again, fellow investors, CAVEAT EMPTOR.

Excellent analysis as always, Travis — thank you very much. While we’re talking about really future possibilities for a company like Brinks to enhance shareholder value, try this idea on for size. Should the cannabis side of its business really take off, but, at the same time show signs of hindering customer retention and acquisition because of laws, stigma, etc., for its core client base, why not spin off Brinks Cannabis into a separate, publicly-held company and distribute those shares to existing shareholders? The new company could be called CannaBrinks Depository (symbol CBD)!

Sharks swimming in the water waiting for the get rich quick to jump in.

So far as crime, most of the pot dispensaries in my city (medical- State only) get broken into on a regular basis.

Must be a tempting target for both the drugs and the cash, this is definitely a big security opportunity that a lot of small companies are trying to address… and eventually the biggies like Brink’s will get in and take a meaningful share of the business from the larger operators, too, I’m sure, though the cash dependence of the industry will probably get smaller over time.

Saw something on Baron’s about pot stocks getting a lot of competition from Latin America. Sounds like a glut is on its way.

Competition or collaboration? Maybe both? Latin America has the upper hand in labor costs and suitable land (rather than expensive greenhouses) to grow cannabis. An example of this scenario would be Khiron Life Sciences (KHRNF) headquartered in Canada, with a Mexican ex-president on its Board, but core operations in Colombia.

Your kidding right ????

This dude is trying a different approach to finding a way to make money in the Marijuana industries, I never really ever heard of this guy. But why not a stock suggestion? Just a story that everyone knows is a different area of the stock to take into. I haven’t even got into extractors yet and looks like it will be a while since the U.S. will legalize marijuana on the 21st of June 2019. So that’s what I am waiting for. I’m going all in on the stock that I will post on Matt McCall IPO when I get it for all you Gum Shoers. Take all those gains and put them on the 4 penny IPO’s Matt McCall is going to give me. I will also place those 4 on Matt McCall’s IPO again for all you Gum Shoers. Those will be for the @!st of June. So you can use them or decide not to. I just can’t see how someone could put up 4 penny IPO’s and have them fail? Don’t make any sense. I know I will be dividing all my cash to those 4 penny IPO’s.

Thank-You

FRANK8 MORRISS

Not convinced that Brink’s is a picks-and-shovels stock worthy of naming it the #1 pot stock pick for 2019, but I would not undermine Mizrahi’s insight into the role it could possibly play in the transportation & distribution chain of a fully-legalized cannabis industry. There was a time when Brink’s armored trucks ruled city streets during graveyard shifts carrying cash to cover employees’ paychecks, stock & bond physical certificates with dollar values worth so much more than payroll cash, gold & silver bars, precious jewelry and various commodities that needed to be delivered to company vaults. While it’s true that payroll and securities have gone paperless, Brink’s seems to have adjusted its business to the tech era while still serving the demand for transporting highly-valuable, physical assets. As cannabis is being perceived as a precious commodity in the not-so-distant future, Brink’s already has the safety blueprint and logistics experience to deliver it by land from Point A to Point B should it choose to be involved in the cannabis space. (More like gravy, really, rather than the meat of the business.)

Brink’s is fairly rated by analysts despite not having a stellar Earnings Report in the last quarter. Viewing its price chart over recent months, the stock has reached a slightly oversold level for its normal price range and is starting to turn back up. So I’m thinking fuhgeddabout the pot… the stock is at a good buying point right now and worth considering. Best of all, it has nothing to do with China, the bane of my investing experience this past week.

Travis The Brinks company isn’t a new thought in the cannabis industry not familiar with mizrahi and pretty much have dismissed 95 pct of any of the investment firms cannabis articles personally most have dismissed any breaking ideas in this market after all but one or two claiming the same boots on the ground nonsence in the cannabis industry or traveling the world interviews with just about every company for years comments with the majority being fictitious They mostly took advantage of the investors who were investing at the wrong time or chasing cannabis stocks as you would a normal new tech break threw again here it’s old needs time was found better spent making our own calls to every company of interest who are always happy to discuss any questions everyday people would have,

A few month before brinks squired Dunbar the Canadian govt. was just adding to the safety regulations for example the Grade level Safe’s required to own and use for licensed companies worrying about crime with such large amounts of cash being stored brinks made a few deals with some of the larger players to provide cash transport they weren’t able to qualify to transport any thing other than just the cash parliament shot brinks down transporting cannabis with the cash . Brinks was actively trying to take over all security in the Canadian market which never happen due to the picture painted that Canada is this smaller country completely open for business when it is the opposite of the USA the govt. provides threw there own regulated stores . Out of the govts greed just started with the lottery process selling off licenses to open a retail location. 80 pct currently of actual retail sales are limited to online only still to this day . The pie charts of who is the largest retailer of cannabis is a complete joke and useless and all claim different amounts per company factoring in the Providence’s selected contracts with the companies they decided on who they knew were capable of meeting the yearly amounts. Forgetting the aurora haters and faithful the one thing no other company did to push back against the govt. not offering retail licenses till after the recreational legal passed but causing a delay of being open for recreational purchases that really caused a lot of volatility. True volatility not the volatility published not understanding the simplest of all concepts that so many mused out on very easy to understand gains and gains that no wall street analysts could understand based on strictly hype of the very idea that pot would be legal which for some is like trying to believe cocaine will be avable for sale to the public. Every vote made every company the cheaper the better in the beginning go from less than a penny 5 month prior to the first of seven votes to go up thousands of pct the day of the vote which up until the last vote making Canada a recreational legal country always passed as soon as J.T. The prime minster of pot was placed into office the only unknown was how many days or hours before a stock that went from .0050 to 2.50 would it return back to just a bit higher than a penny . Only greed caused people to not sell anywhere in the three digit range especially on the below a penny or a 5-10 cent unprofitable to no revenue to date stocks that like clock work followed the next vote tied into other providences medical or recreational and the few states following the same date made for anyone with a calander and the less knowledge about stocks the better being none of the stock formulas applied. Volatile just ment while waiting for a vote to approach a simple comment from Jeff sessions could cause a strictly Canadian company only share price to loose 30 pct for the day and the few days to follow as long as you didn’t panic the vote came and the hype unheard of gains happen every time and that included every single company that was publicly traded. With no major definitive dates now profiting while waiting for announcements about banking and removing pot from being a controlled substance takes a little more than a calander and buy and hold is now only for a dozen current stocks excluding ipo’s that pop up from week to week . Volatility now is a fair word when the trump tariffs bouncing around effects the majority of pot stocks as well as unrelated to tariffs related companies . But back to brinks they are a big thumbs down even a actual investments active company like Scott’s miracle grow the numbers from this tease are beyond insulting and only shows how still to this day true analysts need not apply and asking for money taking advantage of hard working people that see the hand selected companies with 5,000 plus gains in three years makes people desperate to invest unfortunately none of us have came up with anyone who claims to have had there boots on the ground to make you confident enough to invest in pot usually ends bad especially now when the market and how to profit isn’t more than keeping track of the month and day. Here are the notes from the opinions after the ceo of brinks was working trying to set up deals with Canada and the active companies . Which unlike my aweful typing and disregard for spell check should be easy to read but being very clear brinks will not make you a fortune or even a profit with its attempts in the past to assist with money transport just like banks certain regulations and a armored cash company and marijuana doesn’t work at all.:

Brinks CEO Douglas Pertz said that the company is talking to some of the largest players in the cannabis industry in Canada to manage their deliveries and cash after marijuana becomes legal there.

Canada is only the second country in the world to legalize cannabis nationwide, which provides Brinks with the opportunity to see how its business profits from marijuana when it’s legal throughout an entire country.

Brinks closed its acquisition of Dunbar Armored, one of its top rivals, on Monday. This to be followed with Kramer’s opinions as well: mind you it is a lot of words to save you time if you are questioning if brinks will be rising in value making you rich let alone loosing money this is a blip on the cannabis market from before Canada went legal and is just a old interview pretending to be breaking wall street new behind there back garbage:

We are the largest player globally in high-value transportation, that’s one piece of it, and the second piece of it is the cash payments,” Pertz said. “We’re in the best position for that as well.”

However, the drug has only been legalized on a state-by-state basis in the U.S. Canada will give Brinks the chance to test how its business can profit from cannabis when it’s legal throughout an entire country.

One factor that might help the Richmond-based business make the most of the opportunity is its deal with Dunbar Armored, previously one of its top rivals, which closed on Monday.

However, in a blow to Brinks, the Canadian province of Ontario also announced on Monday that recreational marijuana will only be available to consumers online when cannabis becomes legal. Regulated privately-owned retail stores will be allowed to start selling the drug in April 2019.

The decision means that Brinks’ services will likely be less in demand than originally anticipated as Ontario is Canada’s most populous province.

Unless you believe armored car business is the new 5 g if I was you Travis remove this tease that it’s wrighter should be fired

What are the 12 stocks to hold and what are some good upcoming IPOs?

Thanks

https://3sixtysecure.com/news

This link will take you to the site of a similar outfit based in Canada

SAFE on the CSE exchange. It’s at C$.040 (jumped 25% this week

500% is quite possible.

They just bought an American company, which gives them immediate access

to the U.S.

They are also under contract to Canopy Growth plus a few banks.

I own shares.

RW

Thank you I appreciate that. Really not looking for any security or money transport plays though I saw them when they ipo”d on Canadian exchange . I would though if I was you look to take your profits out this week there pre earning spike will either bump them back down the pre earning realease and unfortunately baring anything crazy coming out of a first earning security company in the cannabis industry would keep a eye on the candles don’t give the gains back. Now that the Canadian voting date game has ended , with all that’s going on with China not expecting any one in the USA mentions pot at all until election talk at the end of the year we have been just playing the earning gains selling of the first day stock turns nuetrsl following positive announcement. Then doing the reverse betting against them pretty much knowing where they will drop back to always playing that way a little safer to avoid a acquisition on the way back down which has been doing very well playing with the same companies that have a pretty steady rueteen.would be really selective and limit depending hw many cannabis stocks you are working with to if any no more that one or two if you really got in at a price that never comes close to returning to and your opinion is ride that one till the end . Just don’t fall in love with anyone company unfortunately the 5 cents to a few buck jumps during the voting process is gone for good you should have a couple or a few accounts open allowing you to buy on the Canadian market as well as separate your holdings with similar earning dates makes it a lot easier to stay organized and after running threw the week leading to and the earnings call your portfolio will recalling grow quickly . Just our opinion though taking out profits after big news or earnings you will find buying and holding past a earning period isn’t a good idea. But thank you for that was just putting that out there for brinks which bothered most of us not just because it wasn’t anytype of news and especially more so than we have seen a insulting amount for a non market high prided company.

Best of fortune to you always.

Thanks

Do a little research on the small ipo’s that came threw especially that aren’t unique and don’t come near the plant too many people bought into the buy every ipo that comes threw doesn’t matter if it’s a reverse merger not a true ipo or not there will not be a tilray situation that was just what happens when all the executives bank rolled a company buying share of a established private company at 50 cents a share then the secret comes out to some that Mr amazon has a billion of his own cash invested when invested means sell after the stock turns a billion dollars into a discussing amount would very much expect that to drop way past it original ipo price very soon. . Watch the progress of world lass extractions after wuadron combined giving two shred for ever one providing the share holders of wuadron votes it in which seems to be the decession neither will budge upwards at all until deal goes threw and you will see how predictable they have been and taking out after the 25 -50 ct gains buying back in and doing it with all the holdings pays out Nicley with no major secessions being made.you can double your portfolio even without buying on the way down hopefully putting you in a much different tax bracket if you are a believer cannabis will be removed from the cocain and heroine classifaction followed by the govt taking over for the states which we all have been waiting on ever since Justin T was planted as prime minster .

Altucher is pushing a “weed-tirement” scheme, as a low risk way to get income from the cannabis craze. Anyone know what he’s talking about?

A real pick-and-shovel company for the cannabis industry is Enwave, ENW on the Toronto Venture exchange. Oil extraction. https://www.newswire.ca/news-releases/aurora-cannabis-and-enwave-corporation-enter-global-licensing-arrangements-841681980.html Now also starting cooperation with US Army.

What about Halo Fi touted on Stansberry? Does anyone have an idea what it is?

That Halo Fi pitch has been circulating for over a year and a half now, they keep updating it with new dates but not changing much else. We covered Halo-Fi and the array of companies involved here.

They just want to sell their newsletter