This is how a recent ad from Louis Navellier begins…

“For the First Time in Over 40 Years…

“Wall Street’s ‘King of Quants’ Reveals His Secret $6 BILLION

AI Blueprint

“‘If you apply my “Secret Blueprint” to the red-hot AI market, the next 12 months could be extremely lucrative… even if you’ve only got $500 to start with!'”

Navellier is one of many who says he sees an “explosion in new wealth” coming from AI, and he’s selling his Growth Investor newsletter by promising a few “special reports” that highlight his favorites in this space. And this letter has gotten inexpensive now, they’ve cut the sale price to $29, so presumably it’s being pushed as a feeder subscription to get more folks into the marketing funnel (Navellier’s name is attached to half a dozen “upgrade” letters and packages at InvestorPlace, including the Power Portfolio ($1,799) and AI Revolution ($2,799) projects that combine picks from Luke Lango, Eric Fry and Navellier).

And there’s a long sales pitch about how artificial intelligence is going to be the next great tech revolution, mirroring the growth of the internet, or of mobile computing, and maybe exceeding the growth of those… which is essentially the same as the big-picture spiel we get from almost everybody, though in Navellier’s case, at least, we have a pundit who was around for the first internet boom and was picking growth stocks in the 1990s.

But what we’re interested in, of course, are the “secret” stocks he hints at… so let’s skip ahead and get to those clues.

The main “special report” he’s peddling is called “Three Incredible AI Stocks… for a Six-Figure Payday” … and he drops a few hints about those three stocks, so let’s put the Thinkolator to work…

“… there are over 6,000 companies that trade on the major stock exchanges…

“Only a few hundred of these are pure AI plays…

“And I’ve run every single one of these AI companies through my eight-part filtering system…

“Based on my stringent eight-part assessment of the companies in the AI industry, I’ve pinpointed exactly three AI stocks that meet all eight criteria for explosive growth potential…”

I don’t know what he means by a “pure” AI play, but I’d say there are only a couple dozen of those, at most — and none of them are making money exclusively from AI, so the “purity” varies. But certainly there are hundreds of stocks who are interested in AI, or building something using AI, or trying to convince people that they’re “AI pure plays”.

What’s the first one? Hints:

“The ‘Stealth’ Firm Securing America’s AI Dominance….

“Remember, the heart of the AI Revolution comes in the form of computational power.

“In order to make AI a reality, you need very powerful computers.

“And that power boils down to one thing… highly specialized computer chips.

“This is exactly why companies producing groundbreaking computer chips have been exploding over the past few years.

“Nvidia began skyrocketing last year shortly after unveiling its 144-core CPU Superchip. Shares are up roughly 1,000% as a result.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“There’s not enough supply to meet demand.

“It’s the same story with the semiconductor firm Advanced Micro Devices (AMD), whose share price has been going vertical over the past few years. They recently unveiled their most powerful AI chip to date… called the MI300x….

“According to McKinsey, specialized memory for AI has 4.5X the bandwidth than does traditional memory. Customers are willing to pay a pretty penny for that type of performance upgrade — about $25 per gigabyte versus $8 for regular memory chips.

“Profit margins are ‘off the charts’ for the semiconductor companies that can produce chips with enough memory and storage capacity to handle the enormous data sets needed to advance AI technology.”

That’s hit or miss at this point, mostly because most chipmakers make more than one kind of chip, for more than one market. NVIDIA has record profit margins right now, which is also a risk for this company, since they seem destined to come back down at some point… but Micron (MU), for example, which provides some of the memory chips for some AI chipsets, has unusually weak margins in recent quarters, largely because demand has dipped for other kinds of electronics (laptops, smartphones, etc.). Not every market moves at the same speed, and a lot of companies were caught a little flat-footed by how fast the demand for AI chips grew this year.

Then some more specifics…

“And on Page 2 of my newest AI report, you’ll get the full details of a semiconductor company that is set to challenge Nvidia and AMD for AI chip supremacy.

“In fact, it’s the only company of this type accredited by the U.S. Department of Defense as a Trusted Supplier in the AI chip sector….

“Its tools are so powerful that the government recently shut down China’s access to them.

“Not only that, but large amounts of money have been flowing into this companies coffers lately.

“In fact, they are expecting revenue to top $4 billion for 2023.

“I wouldn’t be surprised if this little-known AI firm becomes the next trillion-dollar Wall Street darling in the years to come as the AI Revolution unfolds.”

Our best bet there? This is very likely to be Marvell (MRVL), which I believe is the only accredited semiconductor supplier for the Defense Department that’s also got an AI-related business (though there are almost no real “pure play” AI companies just yet), has fallen under some of the China export restrictions, and which has revenue somewhere in the neighborhood of $4 billion.

Those clues are somewhat limited and vague, it’s true, so we should hesitate to say this is a 100% certain match… but it’s as good as we get for the Thinkolator today. The only other stock that’s fairly close to being a match on revenue is Cadence Design Systems (CDNS), but they don’t really sell or design chips, they just sell the chip design systems and software. You could also stretch and make Skyworks Solutions (SWKS) fit some of the clues, but they’re really not even a side play on AI at this point and the match is a bit of a stretch in most ways — SWKS is still primarily dependent on the volume of iPhones sold, which has been both a blessing and a curse over the past decade, depending on the year.

For what it’s worth, Louis Navellier isn’t just a pundit, he also runs a money management business, there are separate accounts under his name, and those accounts are quite large so he his firm has to file 13F updates each quarter. That means we do get a little bit of an idea, beyond the newsletter recommendations and teaser picks and free articles that are everywhere attached to his name, about what his firm is actually buying and selling for its investors (he doesn’t manage mutual funds anymore — he did for a long time, but my recollection is that they were pretty consistently terrible, since his system takes such huge hits in down markets, and have faded away).

Marvell hasn’t made that list of Navellier & Associates holdings in any of the quarters so far this year, so it is not among the top 300 or so stocks that his firm recommends owning to its own investors. The only companies that might be described as offering AI “hardware” in some way that are in the latest 13F filings for Navellier’s managed accounts are NVIDIA (NVDA), server maker Super Micro Computer (SMCI), Microsoft (MSFT), diversified chipmaker Broadcom (AVGO), data center switchmaker Arista Networks (ANET)… some of those have been reduced of late, though, so the ones he’s been buying as of the last quarter (ending September 30, reported on the mid-November 13F) are MSFT, SMCI and AVGO. None of those come close to matching the clues here, that’s just an FYI.

So what’s the story with Marvell? They do have a nice business building chips for the high-end servers that are in demand for AI work, and that is expected to grow dramatically over the next year… but it was slower to spool up than expected in the first couple quarters of this year, and it’s balanced by the much weaker industrial and consumer electronics businesses at the moment. Here’s the quote from the CEO in the last quarterly press release that pretty well sums it up:

“Marvell delivered third quarter fiscal 2024 revenue of $1.419 billion, growing 6% sequentially, above the midpoint of guidance. Revenue from our datacenter end market grew over 20% sequentially in the third quarter, and we expect growth of over 30% sequentially in our fourth quarter. The diversification of our portfolio is serving us well, with strong growth from AI and cloud carrying us through a softening demand environment in other end markets. These dynamics are reflected in our forecast for overall revenue to be flat sequentially in the fourth quarter at the midpoint of guidance.”

To parse through that word salad, the summary is, “AI is growing fast, but everything else is shrinking, and that means revenue will be about the same this quarter as it was last quarter.”

In numbers terms, MRVL is in the same situation as a lot of companies who surged with the electronics hardware demand of the work-from-home years — their earnings are going to fall this year from last year, but the expectation is that AI and other factors (but mostly AI, and mostly big buying to beef up data centers for AI, specifically) will get them back to earnings growth next year. In adjusted earnings terms, that means MRVL posted $2.12 in earnings per share last year, is expected to have $1.51 this year, and will get to growing again from this base, to $2.02 in 2025 and $2.78 in 2026. Those are all adjusted numbers, and MRVL has always had a huge stock-based compensation number so the “adjustment” is big — over the past four quarters, MRVL had a GAAP net loss of $556 million, so it’s mostly just by ignoring the non-cash expense of $585 million in stock-based compensation that they can report an “adjusted” profit.

So if we live with that “adjusted” nature of those earnings, as we often have to with tech companies, then that means MRVL is in the middle of a period when adjusted earnings will grow by about 10% per year, on average ($2.12 to $2.78 in three years). If we just accept the new starting point of $1.51 in earnings this year, then it’s far more dramatic growth of 36% per year… you can make those numbers tell whichever story you like, but they should, at least have good growth from here. For that, the current valuation today is just under 30X next year’s estimated adjusted earnings.

It might work out, but by those measures NVDA, at about 25X next year’s forecast for adjusted earnings, is actually quite a bit cheaper than Marvell. There is some potential upside for Marvell when it comes to ASIC production for AI, I think — it seems likely that we’ll transition to a world where not every AI project needs big and overpowered GPUs like NVIDIA’s that can do everything, but that many AI inferencing or processing tasks will end up using customized ASIC hardware. Marvell makes those custom ASICs for AI, and that could become a surprisingly huge business, faster than we think… but it’s not yet a big deal. I guess that’s the area where analysts are most likely to underestimate the potential, if you’re looking for a surprise… but moving to custom ASICs and building out new kinds of hardware like that for new applications often takes a long time, so it might not happen quickly (and there is, of course, no guarantee that Marvell will dominate in custom ASICs for AI).

Interesting company, I don’t think I understand the breadth of their portfolio well enough to go much deeper than that, but at 30X forward earnings there’s clearly a high AI expectation built in — maybe they can exceed that, maybe not, it’s going to be an interesting year. As of November, Marvell gets a “B” in Navellier’s public PortfolioGrader system.

What’s next? The clues get even thinner for the next two…

“… an AI company that currently boasts a portfolio of 1,250 issued patents and 251 pending patents.

They’re based in Silicon Valley and provide unified security solutions that can be deployed over digital networks to protect users against malware, spam and network intrusions.“Even though very few people know about this company yet, they entered the AI space a few years ago through the unveiling of a new cybersecurity system that automatically examines billions of code “features” in order to determine if unknown files are legitimate or malicious.

“They’ve quickly managed to ship more security solutions than any other cybersecurity firm worldwide.

“And the money is flowing in BIG TIME.

“This company is still in the early stages of growth. I wouldn’t be shocked to see share prices surge by 500% or more over the next few years.”

This could be several of the big cybersecurity firms, many of which are based in Silicon Valley… most of them are highlighting their AI chops these days, talking up the ways in which they’re using machine learning to improve the fight against the black hats (and counter the AI that intruders are using to try to breach networks)… but that “1,250 issued patents and 251 pending patents” tells us this is Fortinet (FTNT). Those numbers are not particularly up to date, so I doubt they’re accurate now, but the company has cited them in the past and, more importantly for our purposes, the InvestorPlace writers have often highlighted those specific patent numbers in their throwaway articles, including this undated Special Report from Louis Navellier himself.

And Fortinet has had two very poorly-received earnings reports in a row, leading to big drops in both early August and early November from which it hasn’t yet recovered, so it’s a little surprising that it still has even a “B” rating in Navellier’s PortfolioGrader system… I guess the key is that Navellier’s system is driven more by reported earnings “beats” than by weak guidance, since it’s been guidance that has disappointed of late.

And yes, Fortinet is in the 13F for Navellier’s managed accounts business… though it’s not a huge position, less than 0.5% of their 13F portfolio.

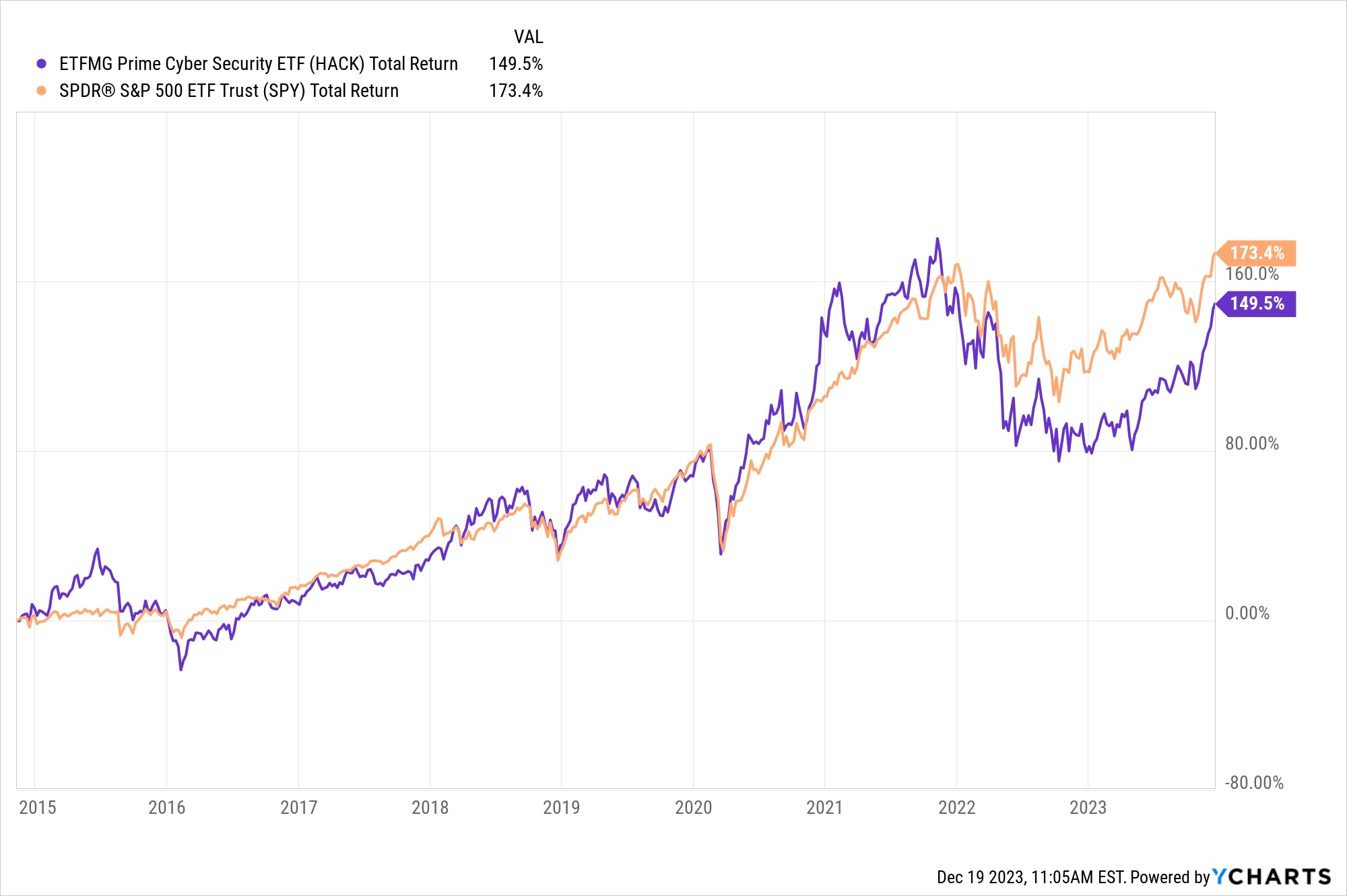

For me, I own some companies that are at least partially involved with cybersecurity, like Cloudflare (NET), but the pure cybersecurity stocks that fight malware and deal with network protection and firewalls are in the “too hard” pile. It seems like it should be a great growth industry, since almost every company is willing to pay almost any price to avoid the worst cyberattacks and ransomware efforts… but it’s also an industry where the competition is dramatic, and it’s too hard for me to understand what winners might emerge (and, more importantly, it’s hard to guess which company will have a dramatically terrible year as a product fails or a competitor eats their lunch). In the past I’ve sometimes used the oldest Cyber Security ETF (HACK) for exposure to this sector, but, as you can see, that rising tide of cybersecurity spending has not necessarily lifted that sector enough to offset the competition within the sector — this is HACK’s total return since inception, it has had a good year in 2023, and before that did very well in 2021, but the bad years hit hard and it is still trailing the S&P 500 over the past nine years.

Incidentally, Fortinet is a huge underweight in that HACK ETF, for whatever reason — it is the second-largest “pure” cybersecurity firm these days, I think, the market cap at $44 billion is second only to Crowdstrike (CRWD, $62 billion), but it is not even in the top ten holdings of the ETF. Here are the top 20, it’s a pretty good sum-up of the larger players in the industry, including the big government contractors Leidos (LDOS) and Booz Allen Hamilton (BAH) as well as the big firewall, intrusion detection and identity management companies. I bet they’re all talking up their spending on AI at this point.

Fortinet may be special and primed to be an unusually strong grower in this space, though that’s not the investor consensus right now. They have been a leader over the past decade, despite having a weak year in 2023. Today, the analysts think they’re in the middle of a multi-year period that will average earnings growth of 15-20%, and the stock is current valued at a little over 30X next year’s adjusted earnings (37X GAAP earnings), so it’s pretty close to the top end of a “growth at a reasonable price” valuation in my book.

And one more…

“Because of the relative obscurity of this company… and the unique position they’re in, I can’t go into much detail right now.

“Essentially, this company is one of the few in the world that makes the equipment necessary to inspect semiconductor chips.

“The company’s earnings have been on a tear for the past four quarters, and I expect earnings will likely continue to soar as the company continues to improve its AI capabilities.”

That’s obviously not a lot in the way of clues, but the Thinkolator offers us some hope…

There are several fairly large semiconductor inspection equipment companies, so it’s not especially easy to narrow it down just by the kind of work they do — if you’re just looking at US-listed stocks this could feasibly be one of the giants like Lam Research (LRCX) or KLA Corp (KLAC), either of which will benefit from increasingly complex chips and higher sales volumes of chips, over time… or a smaller firm in testing like AEHR Systems (AEHR) or Onto Innovation (ONTO). Those four are not the only companies who sell equipment related to chip testing, of course, there are smaller firms, too, like Formfactor (FORM), and some Japanese firms that don’t have easy US trading and presumably wouldn’t make it into Navellier’s letters, like Visco Technologies or Lasertec. But that’s probably the universe Navellier is picking from.

So what’s our best match? Well, given that he says “earnings have been on a tear for the past four quarters,” which probably means he’s starting in mid-2022, then there’s one choice that really jumps out — AEHR Test Systems (AEHR) has indeed grown earnings rapidly over the past 4-6 quarters, while most of the others have actually seen their profits flatten out or decline during that particularly time period. AI hasn’t had much of an impact on the operations or fundamentals of these semiconductor equipment companies this year, mostly just because the rest of the semiconductor industry has been pretty moribund… though the future enthusiasm about AI is probably helping their share prices. Here’s the earnings-per-share growth for all of those firms over the past two years:

Of course, that has also been reflected in the share prices, to at least some degree, so AEHR leads the pack there, too… though it has come down sharply since the highs of the Summer:

AEHR has also been one of the highest-ranked semi equipment companies in Louis Navellier’s portfolio grader system all year, usually given an “A”, though it has bumped down to “B” as of November. So we’ll pencil that in as our likely match. Lam Research and KLA Corp are both in the Navellier & Associates 13F filing for last quarter, for what it’s worth, AEHR is not.

AEHR is relatively small, with a market cap of $800 million and only one or two analysts covering the company, so the estimates are not going to do us any good — but they have posted tremendous earnings growth this year, have quickly become very profitable, and have almost doubled their sales over the past year, so they have some growth chops and they believe that growth will continue. They’re trading at a growth valuation, too, with a trailing PE of about 45… but if the business is going to keep up the recently dramatic growth that’s pretty easy to justify.

The challenge is that AEHR’s specialty is in testing equipment for silicon carbide chips, which are used for higher voltage and higher temperature applications… so it has been considered by investors to be largely a play on electric vehicles, which suddenly seemed to be “topping out” this year as demand for EVs has been disappointing, perhaps partly because of higher interest rates and the still pretty slow rollout of high-speed charging infrastructure… and it’s also a very concentrated business, with most of its business this year coming from On Semiconductor (ON), by far its largest customer. Both ON and AEHR issued guidance that the market considered to be disappointing last quarter.

So is Navellier pitching AEHR, which this year has been the fastest growing semiconductor test equipment company… but is also extremely small and volatile? Or might he be pitching one of the stalwart leaders like KLAC and LRCX? I’ll stick with AEHR as my guess, but it’s probably the least exposed to high-end AI chips among the testing companies so far… and that’s really a guess.

They’ve all been popular ideas this year as the expectation of investment in more semiconductor foundries leads people to expect more investment in equipment for all those foundries, though perhaps there’s some reality check settling in, as investors realize how many years it takes to build these big chip facilities in the US. The big guys have been doign well, despite the drop in earnings this year, both KLAC and LRCX are expected to grow earnings at a 15-25% pace from here, and they’re both trading at 25-30X earnings, so they could slip pretty easily into a “growth at a reasonable price” portfolio if the analysts turn out to be right in their projections — LRCX has been a “B” in Navellier’s Portfolio Grader for most of the year, and KLAC has been at “B” all year.

So… think those will be the big AI winners? Semiconductor equipment? Chipmakers who might benefit from data center spending and the emergence of customized AI chips? Cybersecurity companies who use AI (and fight AI malware)? None of the above? It’s your money, so you get to make the call — we’d love to hear what you think if you’ve got a moment to enter a comment in the happy little box below…

Disclosure: Of the companies mentioned above, I own shares of NVIDIA and Cloudflare. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Thanks as always for your excellent write-ups, Travis!

Thanks for the information above. Great research and great value.

Thanks for the info Travis. I like the fact that MRVL has a dividend so it pays us to make a play on it’s future a little bit.

I subscribe to Growth Investor and have the report – his 3 stocks are Cadence Design Systems (CDNS), Fortinet (FTNT) and KLA Corp (KLAC). They also have another report for scalable AI companies – AXON, MSFT, NVO, PCAR, SMCI, and OPRA

Thanks durango… CDNS is certainly a steadier company than MRVL.

And I’d choose KLAC over AEHR, too, glad he’s got a more rational large cap leader for that pick. Even if you can’t call this chart “explosive earnings growth” over the past year (growth has been excellent for a long time, just not this year):

KLAC Normalized Diluted EPS (TTM) data by YCharts

Does the report have a date on it? Just curious, sometimes they get very long in the tooth while they’re still being actively teased and promoted.

no date that I can find on the report. For what it is worth it is near the top of the listing of Special Reports.

I think two of the most misleading clues in tease-dom are “Almost no one has heard of this company” and “The company is so obscure I can’t give any details about it.” Large cap KLAC is the opposite of that, of course…and it’s earnings tear appears to be old news, as you’ve shown. Latest 12-month-out price targets I could dig up for them range from 550 to 700. I’ll pass.

@durangorandy which are “The top rated AI home run stocks”? They were mentioning this report in the teaser for growth investor.

The 3 are EXTR OPRA and PERI

I’m doing very well with C3.ai and plan on buying more today.