Nick Giambruno is helming the Crisis Investing letter for Casey Research now, which must come with a fairly high degree of attention because Doug Casey really made his name with his bestselling book of the same name in the late 1970s (later revised a couple times).

And after all this time you know what you’re going to get with Doug Casey, who has been a pretty consistent and strong-voiced libertarian: He thinks government has far outlived its usefulness, that we’re on the brink of a catastrophic collapse (and have been, at least much of the time, since 1979), and that you need to embrace “alternative” investments to protect yourself. Presumably those “alternatives” have morphed somewhat over the years, but gold has almost always been a factor, as has foreign real estate and investment in foreign countries — he’s very well-traveled, and many of the anecdotes that crop up in ads for Doug Casey’s work revolve around buying deeply discounted companies or real estate in countries that are hated or avoided by most investors.

Doug Casey has spent the past few months opining in interviews that we’re leaving the eye of the financial hurricane — that the first waves hit with the financial crisis of 2008, we’ve been enjoying the becalmed eye, and now the back end of the hurricane is going to hit us harder still. Here’s how today’s ad quotes Casey, from March:

“Right now, we are exiting the eye of the giant financial hurricane that we entered in 2007, and we’re going into its trailing edge. It’s going to be much more severe, different, and longer lasting than what we saw in 2008 and 2009.”

That’s a lovely metaphor, and it makes sense that there would be a negative backlash, eventually, to the huge monetary stimulus programs of the past eight years — particularly from inflation, though that hasn’t yet reared is head, but probably also from the great imbalances and strange incentives that have been created by holding interest rates at zero (or, most absurdly, by negative rates).

But the timing of big turns in the economy is, obviously, easy to opine about and almost impossible to accurately forecast. Doug Casey was saying much the same thing, about a likely “exit from the eye of the hurricane” within months back in the Spring of 2014. And he wasn’t alone, people have been predicting disaster pretty much every year since the US Government and the Federal Reserve stepped in in 2008 and 2009 with their various “rescue” programs and set us on the “easing” and stimulus path. The Fed has done unprecedented things in pushing liquidity, and is obviously the major global driver of investor sentiment these days — as we can see every time (including last week) that a hint of possible rate hikes hits the ears of Wall Street traders.

So even when we think that a pundit is making a rational argument, it’s important not to nod your head so vigorously that you forget to be skeptical about their ability to accurately predict the future.

And, like I said, we know the prevailing sentiment — they put it in the first couple paragraphs of the ad letter:

“As Dispatch readers know, America has been in decline for decades. The 2008-2009 financial crisis only accelerated the country’s downfall, thanks to the Federal Reserve.”

There is quite clearly another way of looking at America’s progress over the past few decades, but debating the point is not why I’m writing to you. Instead, I thought we’d try to identify for you what Casey’s analyst Nick Giambruno is pitching as his play on this “Biggest threat no one is talking about.”

And Giambruno notes that his readers are already “prepared for this coming crisis” because they’ve stockpiled cash and sold most of their US stocks, and because they own gold.

But this particular hinted-at recommendation is a buy based on the “major economic event” of a new superpower being born… here’s a bit more from the ad:

“With America in rapid decline, China will soon become the world’s biggest and most important economy. And it could happen faster than most people think….

“Like Doug, Nick is a contrarian. He likes to buy assets other investors hate. This simple approach often gives you the chance to buy world-class businesses for cheap.

“According to Nick, China is one of the most hated markets on the planet right now. Investors are worried about its slowing economy… a potential property bubble… and China’s volatile stock market….

“Nick thinks China’s long-term potential far outweighs these risks.”

So what did Nick find on his trip to China “in search of opportunities?”

Apparently, in his June issue of Crisis Investing he covered what he calls the “new silk road,” which is “all about tying Eurasia together with infrastructure… high-speed rails, modern highways, fiber optic cables, energy pipelines” and etc. He calls this “new silk road” a “direct threat to U.S. global supremacy” and a “huge opportunity for investors.”

So what should those investors buy? More from the ad:

“‘A-shares’ are shares of Chinese companies that trade in mainland China. If MSCI adds A-shares to the Emerging Market index, China’s weighting could jump from 2.7% to 20%.

“In other words, money could soon start pouring into China’s mainland stock market.

“Nick found a way to profit before China opens its flood gates…”

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...

Huh, so this is a little bit like Dr. David Eifrig’s pitch about REITs a couple weeks ago — he argued that more money would flood into REITs because of MSCI’s sector rebalancing, which would force more institutional money to flow into that investment class… and Giambruno is saying much the same thing, with the implication that as China’s domestic share markets become more open, global investors will have to add more China exposure or risk being “underweight” a major part of the global indices.

And at that time, Eifrig hinted at a couple REITs he thought people should buy — but also really implied that buying a REIT ETF would work out well. So what’s Giambruno saying? Does he want us to buy some specific Chinese companies that trade mostly on the domestic market?

Not really — he’s got a fund in mind. Here are the hints:

“He recommended a fund that offers direct exposure to the New Silk Road. It holds a company that builds bridges and toll roads… a major Chinese railroad… and a company that’s bankrolling many ‘Silk Road’ projects.

“Best of all, this fund is easily accessible. It trades on the New York Stock Exchange.”

And some financial metrics that we can check:

“… this fund is trading at a 15% discount-to-liquidation value.”

and

“Nick’s China investment has already returned 15% since June.”

There are now some ETFs that track the Chinese domestic “A Share” market, those have slowly rolled out over the past few years as that market has opened up a little bit to foreign institutional investment (you still really can’t, as an individual US investor, go and buy individual stocks on the Chinese exchanges… other than Hong Kong, which is a separate beast entirely and is much more tied into global markets)… but Giambruno clearly isn’t talking about one of the ETFs, because they don’t generally trade at significant discount or premium prices to the value of the indexes they cover and the stocks they own.

No, if you’re talking about trading at a discount, particularly if that discount is persistent and not just the result of a day’s shock, then you’re talking about Closed End Funds. Which means, sez the Mighty, Mighty Thinkolator, that Nick Giambruno’s China fund investment is the Morgan Stanley China A Share Fund (CAF).

A few years ago, CAF was a bit of an odd bird — Morgan Stanley got special permission to create a limited fund of these stocks, so when this closed-end fund went public in the mid-2000s it was really the only way that US investors could get access to A Shares stocks in China on the Shanghai or Shenzhen exchanges. When enthusiasm for China was high, the fund traded at a huge premium to the NAV of the stocks it owned; when enthusiasm waned, it often traded at a steep discount. That’s the way of all closed-end funds, they are effectively leveraged investments because they trade not just on the value of the underlying investments, but also on the sentiment that drives investors to either oversell or overbuy that particular sector… and since that was the only fund available for a while, it was crazier than most.

Now, things have settled down somewhat and there are probably about a dozen ways to invest in the A Shares segment of the China market through ETFs — the first ETFs started popping up in 2011 or so, and more new ones come out each year that follow either the A shares market or some subset or variation the domestic Chinese stock market (small caps, internet stocks, etc.). But even though all those ETFs pretty routinely trade within a few tenths of a percent of net asset value, CAF still trades at a substantial discount to NAV… it may not ever get to trade at a premium to NAV again like it has for a few brief moments in the past decade, but it could certainly return to a more “average” closed-end fund discount of 5-10% if investors are pleased by the fund’s performance and optimistic about the sector.

If we assume that you’re interested in having exposure to the domestic Chinese stock market, either because you think it will attract more institutional money as it opens up further to the world or just because you think the stocks will become more valuable over time, what should you do? Should you pay the lower expense ratio of an ETF and get a return that pretty much matches the performance of the index, or buy a fund that’s actively managed, costs more in terms of expense ratio, and trades at a discount?

Well, since the ETF that I most often check for this market was introduced in November 2013, the db X-trackers Harvest China ETF (ASHR), the NAV of that ETF and of the Morgan Stanley A Shares CEF (CAF) have followed almost exactly the same path… but that gives the edge to CAF, because it payed a substantially larger distribution last December so has had a stronger total return (a distribution cuts the NAV, as you would expect, since that cash is sent to shareholders and is no longer part of the fund). So the total return since November 2013 has been about 60% for CAF versus 30% for ASHR.

This year, the difference has been less stark — but a narrowing of the discount has helped CAF to do a bit better than ASHR since January 1 as well — CAF has lost 5% of its value, ASHR has lost 12%. Both have done quite well over the past few months, but that hasn’t been nearly enough to counter the huge swoon they took back in February, when pretty much all markets around the world were crashing.

There is likely to be more volatility for CAF than for the various ETFs that track Chinese domestic indices, not just because of the closed-end fund premium/discount variability, but because the fund is much less diversified. The top ten holdings of CAF represent make up about 68% of the fund, with near-10% stakes in China Resources Sanjiu Medical, Jiangsu Expressway, and Industrial and Commercial Bank of China… whereas the ASHR portfolio looks much more like a typical index ETF, with the top holdings being about 2.5% positions in Ping An Insurance, China Minsheng Banking, and Industrial Bank and the top ten holdings making up less than 20% of the fund. That’s good if the managers are particularly adept at choosing stocks, but it’s obviously risky if they make a mistake with one of those larger holdings.

No big surprises there, active management always provides a different (and higher) risk than indexed investment funds — but active management is also the only way to do better than the index, if that’s your goal (no matter how many academic papers and long-term studies tell us that seeking to beat the market is a fool’s game, we are all, at heart, fools in that regard… if you didn’t want to beat the market with at least some play money, you wouldn’t spend so much time researching stocks and investments).

So do you find the Morgan Stanley A Shares fund compelling? It has done well over the last few months, so it looks like Nick’s pick in June was certainly well-timed, at least in the short term… though the Hong Kong shares (usually referred to as “H shares”) of big Chinese companies have generally done better than the domestic A shares in recent months. The fund generally moves in sympathy with the broader Chinese domestic A shares index, but will certainly be more volatile than the index because of concentration, manager risk, and the natural leverage that CEFs often provide because of the swings in the premium or discount valuation. And yes, it trades at a big discount today — as of the last close, the shares were trading at about a 15.5% discount to NAV.

The fund often pays out large distributions, too, though you probably shouldn’t count on that huge distribution paid out last year being a regular thing (CAF paid out about a 30% cash distribution last December, ASHR paid out about 22% thanks to the big capital gains both enjoyed as the China market boomed for a while in 2015). Over the past few years, the management fee has been earned by CAF through index-beating performance (the annual management fee is about 1.6%, roughly twice as high as the expense ratio for ASHR), but who knows whether that will continue to be the case in the future. Morgan Stanley’s last semiannual report for the CAF fund is available here if you’d like to see it, it also includes the basic letter from the managers about their strategy and weightings.

And with that, I’ll leave you to your own musings — is the domestic China market likely to outperform the US market in the coming years, or do you have other favorite sectors for investment? Let us know with a comment below.

This particular teaser makes more sense than most of them. China shares can be rather volatile, but investing in a large basket of them at more than a 15% discount and staying in over time is a pretty good play IMO.

“The main beneficiaries will be *Chinese train manufacturers, *nuclear power companies, *telecoms equipment manufacturers and *banks, because they will be the preferred contractors and financiers for the projects,” (Karine Hirn, partner at the emerging and frontier market specialist, East Capital).

China is the largest global developer of high speed trains, that will be leading in Silk Road development. China just merged its largest railway developers into a major company capable of taking on the huge task, with China Railway Development, CRRC (00390.HK) likely to be one of the biggest winners, selling on the Hong Kong exchange for about $1.50.

I would add to the road and port constructions companies that are likely to be big winners. These include the biggies like China Communication and Construction (CCCC) also on the Hong Kong exchange for about $1.50.

Port developers also should be big winners, with China’s COSCO and CCCC (fully owned unlisted subsidiary, China Harbor Engineering).

Regarding internet companies, Alibaba, Baidu, and TenCent tops the listed, all listed on the HK exchange.

No real need here as most of these can be purchased directly.

One can make a case for China over the U.S. At the same time China’s Govt. Is much more manipulative than the Fed in my opinion. Plus Chinese Govt debt is greater, although their economy has more growth potential.

If Casey or any others thinks there is a financial disaster looming by saying – “the back end of the hurricane is going to hit us harder still” – Then why recommend any stock or ETF? – Seems like he would recommend a short ETF or gold.

I’m a subscriber to their free “Casey’s Daily Dispatch” and while they’re definitely more click-baity with hints of Dent Research at times since Olivier Garret left, Doug Casey still harps a lot on why you shouldn’t be in the stock market at all right now. Main recommendation has been to buy more gold and build up cash reserves for when the crash comes (supposedly some time in early 2017).

I used to be a paid subscriber to the Casey Report so I don’t know what they’re recommending now, but I’ve heard E.B. – their new editor – is recommending more shorts and puts.

Stansberry’s Steve Suggerud is also pushing CAF in his True Wealth publication.

Travis that is a lot of ground covered even by your standards. For starters the “Silk Road” is a wet dream supported by Lyndon Larouche. This was in part to connect continents by the paleo land bridge track from Siberia to Alaska. Good luck with that. A Sino-Russian continuous infrastructure over some of the most hostile environment on the planet is to say the least challenging. It is the Panama Canal to the10^12 power.

I always get my guffaws over ideas conjured up by experts who never built anything in their lives but Lincoln Logs.

The state of the Monopoly Money System in the US which was anchored by gold after WWII when we held 22,000 Tons of the stuff has mysteriously deteriorated to less than 6,000 Tons at present. IMHO Fort Knox only holds metal owned by others –no longer ours.

On top of the $19+ Trillion Debt, the $42 Trillion of off-book account, including $200 Trillion of promises and guarantees and you don’t need to be a genius why a World Currency is about to replace the Almighty Dollar. Our World Credit Card will be suspended. Yes our World Power demise has been predicted for sometime but it is still in our future God help us all. Sorry

Hi Mr. Bigfoot,

I agree with your post in reverse order.

Sorry state of US financial position…agree 100%.

Dwindling of gold reserves and questions about Fort Knox…50%.

Silk Road…0% percent. The Silk Road does not include a land bridge to Alaska. It is the route of trade from the far east to the west and has been in continuous use for over 1000 years. With the Chinese need to import raw materials and oil and to export manufactured goods, it is not at all absurd to imagine a big effort in by the Chinese to improve the transit infrastructure.

The “silk road” referenced in the ad is a metaphor, not a specific development — it’s just a way to describe what China is doing to finance and build ports, telecom infrastructure, energy transport infrastructure, roads and bridges and rail, etc. both in China and in connection with their neighbors in SE Asia and Eurasia.

https://www.larouchepac.com/20151229/us-joins-new-silk-road

I am well aware of the road that you refer to–but the scope and magnitude of the proposed “Silk Road” and cultures in conflict including the hostile environment of the current “road” IMHO does not lend itself to the expansion proposed. My estimate of the cost is in the 100s of TRILLIONS—tough to justify.

I think of it more generally, along the lines of “China is going to keep spending a lot on infrastructure.”

You may be right about the unreasonable cost, but China will do and has done things involving construction and infrastructure regardless of cost. A megaproject would be to their liking and enhance their strategic position on both imports and exports. To say nothing of putting thousands of people to work and using coal and iron ore.

Neither one of you read the link. You can lead a Horse to water but you can’t make him drink.

The water in the link is not fit for drinking.

I agree the worldwide scheme proposed is a pipe dream; you just referenced “Silk Road” in your original post.

We can’t even get a pipeline approved through Canada.

https://worldlandbridge.com/ I don’t know what you are describing–last shot at clarity.

I am saying that I agree with you that the world-wide infrastructure project as described by Laroche is a pipe dream.

However I think that the Chinese will spend a lot on infrastructure on the traditional Silk Road transit routes from the far east to Europe, European Russia included.

That type of project is consistent with Chinese import and export aspirations, and would employ thousands of people in heavy construction and transportation, which are also areas that are favored for development and subsidy in the Chinese system.

RE: Chinese investments in transport infrastructure

See second paragraph.

Australia’s busiest container port leased for $7.3 billion

4:21 AM ET, 09/19/2016 – Associated Press

SYDNEY (AP) — An Australian-led consortium has won a 50-year lease on the country’s busiest container port for 9.7 billion Australian dollars ($7.3 billion), officials announced Monday.

The Lonsdale consortium, which includes multinational firm Global Infrastructure Partners LLC and Australia’s sovereign wealth fund, among others, secured the lease for the Port of Melbourne…

The lease is the latest in a series of port privatizations in Australia in recent years. Last year, the prime minister was forced to defend the leasing of the strategically important port of Darwin on the country’s north coast to the Chinese government-linked Landbridge Group. The Darwin deal attracted criticism because the port is near an important military base where up to 2,500 U.S. Marines train as part of increasing U.S. defense resources in the Asia-Pacific region.

It’s likely that the Silk Road costs will be in trillions, but it’s important to note that China intends only to provide seed funding, while developing financial partnerships with international banking, and corporations. Several of the largest planned projects already have partnership agreements with the Asian Development Bank (Japan), the World Bank, the European Banks for Reconstruction, and the BRICs Bank.

I’ll be VERY surprised if we make it to Nov w/o a global market crash, WAR, or both!

There is always an October Surprise during election years

The main driver behind all the tipsheets seems to be that the Yuan will become the next and fifth reserve exchange currency at the end of this month. The pundits of the tipsheets profess that gargantuan sums of money will flow into China and the stock exchange because of this catalyst! On the other hand, at least nine major countries have bypassed the normal exchange process and agreed direct exchange rates with the Yuan and their currency. Others may have some different perspective?

China is trying to keep their currency value down to help exports, but also trying to open up and internationalize it’s economy, albeit slowly and without giving up much control if they can help it. The switch in SDR components is one small part of the yuan becoming more internationally viable, but I think the talk about that switch being monumental and economy changing in short order is hooey. It won’t impact exchange rates much if at all, nor will it have any impact on the international presence of the dollar or cause the yuan to be widely accepted as a reserve currency… Those things will probably continue to change and evolve and rotate toward China if they continue “opening,” but I suspect it will be quite slow.

How much of the speculation that the reserve change sooner rater than later is motivated (directly or indirectly) by a profit motive (as in more subscriptions)?

A huge percentage of it, I expect — deadlines and catalyst dates that have at least some ring of reality to them are great for selling newsletters.

China’s yuan in the SDRs…a few thoughts. The proportion of US dollars in the IMF SDR’s is remaining constant at 41%. The GBP, JY and Euro are being reduced to make room for the yua So even though it is probable that the USD should have its weight reduced in the SDR, it is not.

Other things being equal (which they never are) this would imply short term strength for USD and Yuan, weakness in GBP, JY, and Euro.

Also China has a lot of direct swap currency arrangements with major trading partners. There was a lot of ink about these agreements a while back, though not recently.

China is also easing now. They have some ways of doing it that are different from ours and they are starting at higher rates. But they are also easing.

As far as Chinese stocks are concerned, I have no conviction opinions. I made some money on a few last year but have no position at the moment.

I suppose the A shares are as good a way in as any, if one wants exposure to China.

I think assuming that the change in the SDR will impact real exchange rates or the real economy in a meaningful way is a mistake — the SDR “market” is tiny and not particularly consequential, especially for large economies. The SDR change is a gradual reflection of the reality of the rise of China, and the need to build the Yuan into the international economic picture more over time, I don’t think it’s something that will change the global economy.

I could be wrong, and we continue to see folks predicting “doomsday” because of the SDR change (like Jim Rickards), but that seems dumb to me. The dollar should weaken, but something else has to rise for that to happen and there isn’t a major economy on earth that wants to strengthen its currency against the dollar — and China is still trying to stop outflows because all the people who have money in China want to get it out of Yuan and foreign investment into China is much smaller than it has been in the past.

This year the dollar has been moderating a bit, at least, and gold is the sensible choice when all currencies seem to be in a “race to the bottom”, but if the US raises rates a few times and no other major economy raises rates, the dollar could easily strengthen again in a big way — “money goes where it’s treated best” is an old saying that isn’t always particularly helpful, but global investors and institutions in search of returns will buy even more dollar-debt if the yields are better.

China…one simple idea on China that I do believe is that one should have what China wants to buy, and one should be out of what China wants to sell, can produce, or can manipulate.

China has been buying hard assets. They have been selling dollars.

They are into battery and nuclear energy.

Another idea to keep in mind is that in certain industries, Chinese political and employment strategy dictates that certain businesses will be supported, no matter what the underlying fundamentals of profit and loss might be. There are vested interests and employment that will be considered.

This is especially the case in construction, and in certain commodity businesses like coal and steel. So overproduction is likely to continue there.

One thing the Chinese will demand for sure is food. There does not seem to be a lot of price inflation yet in food prices, but it is sure to come.

I am actively looking for ways to invest in this sector, but so far I am not satisfied. Two possible picks are WHGBY and CRESY. WHGBY is more to the point as they are the ones who bought USA’s Smithfield, and they are the largest pork supplier in China. CRESY is a South American land and cattle

enterprise.

Democracy, globalization and the nation-state…incompatible ?

The country has gotten into a lot of trouble listening to Harvard PhDs but I found it interesting. Should be on another thread, I apologize.

http://rodrik.typepad.com/dani_rodriks_weblog/2007/06/the-inescapable.html

I love all the experts on China, especially those who have never visited and haven’t a clue why Shanghai works and Beijing doesn’t. Folks you can’t make generalizations about China and sector groupings within China. The politics, culture, and economics of different regions can be and often are dramatically different. If I am investing there I want independent analysts with boots on the ground, and I’ll still follow it up with my own visit.

China is a wonderful place with great opportunities, however it is not for the ignorant or those who are easily misled.

Hi Joe D, any specific suggestions on how to invest there, or do you think it is inadviseable ?

IMHO, while you have many other good options, why bother invest in China? I believe Confucius would not invest there if he was alive.

yclin6…what are some of “the many good options [to invest in]”

that you refer to ?

HN, you have done very well with your metals stocks. That’s good enough.

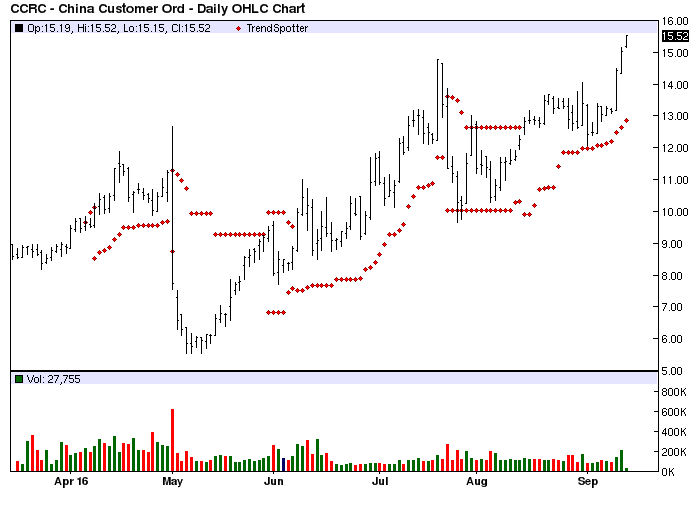

$CCRC np – From Barchart This morning China Customer Relations Centers (CCRC) is the Chart of the Day. Today selection was made by default. At 10 AM this is the only stock in the Barchart data base to hit an All Time High. Since the Trend Spotter signaled a buy on 8/15 the stock gained 19.94%.

China Customer Relations Centers, Inc. provides call center business process outsourcing. The company focuses on the voice-based segment of customer care services. It offers customer relationship management, technical support, sales, customer retention, marketing surveys and research services. China Customer Relations Centers, Inc. is headquartered in Tai’an, the Peoples Republic of China.

The status of Barchart’s Opinion trading systems are listed below. Please note that the Barchart Opinion indicators are updated live during the session every 10 minutes and can therefore change during the day as the market fluctuates. The indicator numbers shown below therefore may not match what you see live on the Barchart.com web site when you read this report.

Barchart technical indicators:

100% technical buy signals

Trend Spotter buy signal

Above its 20, 50 and 100 day moving averages

9 new highs and up 25.04% in the last month

Relative Strength Index 69.48%

Technical support level at 14.00

Recently traded at 15.59 with a 50 day moving average of 12.46

Fundamental factors:

Market Cap $283.75 million

Since no analysts are following this company there are not revenue or earnings projections

This is not yet a stock you can analyze

All you can do is benefit from the price momentum

Chinese stocks can collapse in a second so always be prepared to sell or have a stop loss in place

Barchart’s Chart of the Day is a free email newsletter providing commentary and analysis on one ticker symbol or commodities contract each trading day. In order to assure consistent delivery of the newsletter into your inbox, add newsletters@barchart.com to your Address Book.

What Casey and his fellow doomsayers not seem to realize is that if the US economy goes to hell in a hand basket as they’ve predicted for years, China will not be the shining market in the hill – pardon the metaphor – but be pretty much down as well with other global markets.

and the elephant keeps on moving!

Why am I in this basket and why is it so hot in here ?

i have seen them making a highway in Ceylon using pris. in return for….

Remember FXI,HAO,YAO…some survived: expl. : SIN&BAIDU.I do no invest

in any road what so ever. Seen most of them.

I think that is the 2nd biggest threat. The biggest threat is the people that will vote for Hillary Clinton !!