I’m sure this sounds like a hugely appealing promise, especially for folks who are getting close to retirement age and worrying whether their portfolio will be big enough to support them in the years to come… here’s how Tim Plaehn is selling his Dividend Hunter newsletter these days:

“Collect legal ‘backdoor’ income from pre-IPO Silicon Valley startups…

“90% earnings paid to shareholders (without corporate income tax)…

“Over $2 Billion in managed assets & 530+ new companies funded….

“This little-known tech stock paid a massive, special dividend the entire year in 2023…

“Making it one of the highest-yielding stocks on the market.

“2024 will be no different.

“To put it bluntly…

“If I could only recommend one income stock to retire on, this is it.”

And this is how he describes the “one stock retirement” potential…

“If you’re younger, you can start today with just $25,000 and set yourself up for a cushy retirement with this tech stock.

“But if you’re at retirement age with more money to invest …

“It works in just 36-months, and I estimate you can collect upwards of $55,715/year in passive income.

“Plenty to pay your bills for life and retire comfortably.

“You simply “Buy, Hold, & Retire” – as easy as it gets.

“Because unlike other single stock retirements…

“This tech stock…

– Doesn’t require going ‘all in’ on one tech idea…

– Won’t crush your retirement in an inevitable stock market wobble or crash…

– Has the potential to pay your bills for life in as little as 36-months!”

So what’s he talking about?

Well, he teases an “Obscure 1940 Law” and makes reference to the fact that 90% of earnings are paid to shareholders, without corporate income tax, means he’s pitching a Business Development Company (often abbreviated BDC).

BDC’s are special investment vehicles that are supposed to make it easier to gather capital for investing in small and midsize companies, the ones who are too small to really go to Wall Street for financing but also maybe too large for their local bank. They are generally required to focus their lending on smaller companies, they can’t use a lot of leverage (debt can’t exceed equity), and if they pay out 90% of their taxable earnings to shareholders as dividends, they don’t have to pay corporate taxes (the payouts are usually well above that level, as is the case with REITs, which offer a similar tax-free “pass through” structure where the taxes get paid by shareholders in the form of dividend taxes, not by the corporation itself).

Most BDCs are what’s frequently called “mezzanine” lenders, often cooperating with the Small Business Administration to facilitate small business lending and offering loans that also take on some of the risk of the business, and may be exposed to the equity or cash flow of the borrowing companies in various ways… but there are other kinds of BDCs, too, with a sector focus or a different strategy, and this appears to be one of the outliers.

"reveal" emails? If not,

just click here...

And here are a few hints about this specific company:

“… what’s happening here is they’re taking the hard part off your plate – finding the right companies to invest in…

“The experts are already on their team, working for you…

– Folks like the CEO who hails from UBS Investment Bank…

– The Chief Financial Officer (CFO) with over 25 years of strategic and international business experience…

– And a Managing Director who was once part of the famous team that took NVIDIA from startup to multi-billion dollar company.

“In short, it’s the perfect stock to retire on.

“This is the investing equivalent of the ‘60s Packers, the ‘79-’84 Islanders, or the Jordan-led ‘89-’98 Bulls — a dynasty of success.”

Well, that CEO is Scott Bluestein, who was indeed an analyst at UBS a long time ago… the CFO teased is Seth Meyer… and that Managing Director is Michael Hara, who does their investor relations work… and played much the same role at NVIDIA in their early days.

And yes, that means this Hercules Capital (HTGC), the same stock that Tim Plaehn also called his “#1 Buy, Hold, and Retire Stock of 2022”

Hercules Capital is a BDC that specializes in “venture lending” — essentially, using BDC-style lending, but to earlier stage venture technology companies who sometimes don’t have a lot of cash flow to repay traditional loans, so they often have an equity “kicker” that lets them participate when their customers do very well (with a big IPO, for instance).

That’s not the core of the business, to be clear, they are overwhelmingly a lender — they have about $3 billion in outstanding loans they’ve made to 125 companies… but they also do have $150-200 million in equity investments and warrants, often attached to lending deals, which helps to juice the returns a bit sometimes.

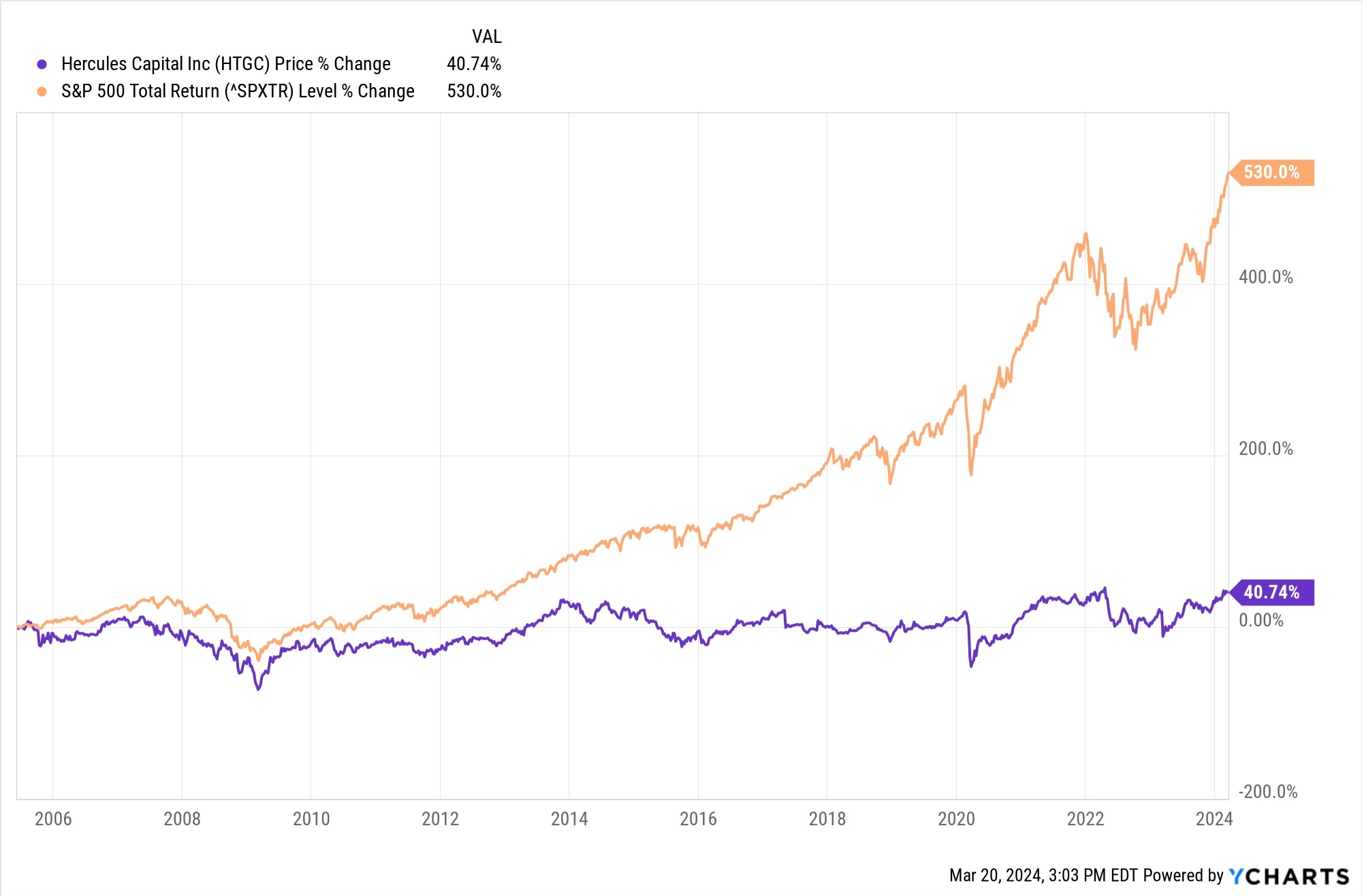

This one has been around for a long time as a tempting “venture” style investment that also pays a solid dividend, I’ve written about it being teased a few times over the past 15 years or so, and the long-term returns have been very decent. Most of the gains come from dividends, and particularly from reinvesting those dividends and letting them compound, but over the past decade the performance has been pretty impressive — they’ve almost matched the return of the S&P 500, and have been more volatile, but that’s better than a lot of BDCs have done… and much better than the other popular “get in early on technology venture capital” funds have done.

The stock tends to ride with enthusiasm or panic about venture funding to some degree, so 2022 was a very bad year and late 2023 and early 2024 have so far been pretty good, as AI enthusiasm leads to general excitement about silicon valley startups. If you’re thinking of this as a long-term investment, with hopes that the dividend can really boost retirement income, here’s how the stock has done over time… you can see that the 2008 market crash took a big bite out of the business, as did the weak market in 2015-2016, the COVID crash in 2020, and the post-SPAC-mania tech stock decline in 2022 — compared to the S&P 500 (in orange), you really weren’t building your portfolio with those HTGC shares over the past 20 years:

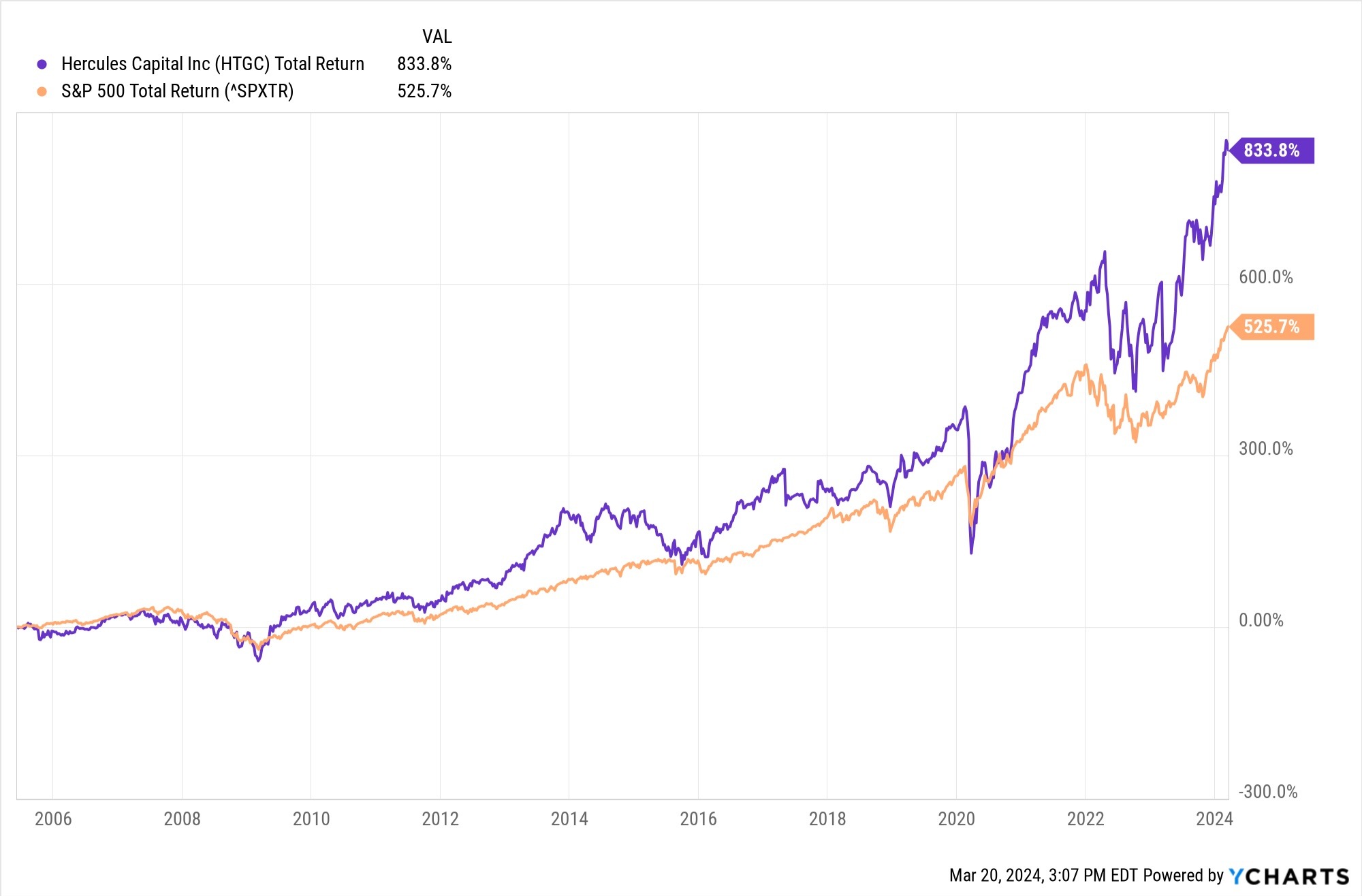

But I include that mostly just to reset your expectations — when you buy a stock like this, with a very high dividend yield, you’re not counting on capital gains from the shares going up. You have to leave that idea behind. You’re counting on the stock not losing too much or having a real existential crisis, and paying out high levels of income each year. So this is what the total return would have looked like if you had reinvested your HTGC dividends — those ~10%/year dividends added up (the amount of the dividend has varied widely, but it has always been large), and HTGC’s returns beat the S&P’s total return over those 20 years. Big and consistent dividends can be very powerful:

So how are things looking now at Hercules? They continue to grow, and they have managed to keep their net interest margin nice and high at 13.7%, so that would certainly be the envy of any bank. That’s the difference between their cost of borrowing, which they do through bond issuances that will probably gradually get more expensive, and their interest income from lending out that money, which will also rise a bit thanks to adjustable rate deals, but has always been quite high because these are generally high-risk enterprises they lend to… the idea is to have a big and diversified portfolio of lending to those companies, to make sure that your losses on the firms that fail to make it are never huge. And it seems like they’ve done well on that front, over time — often better, in fact, than their BDC peers who don’t specialize in lending to tech and biotech companies.

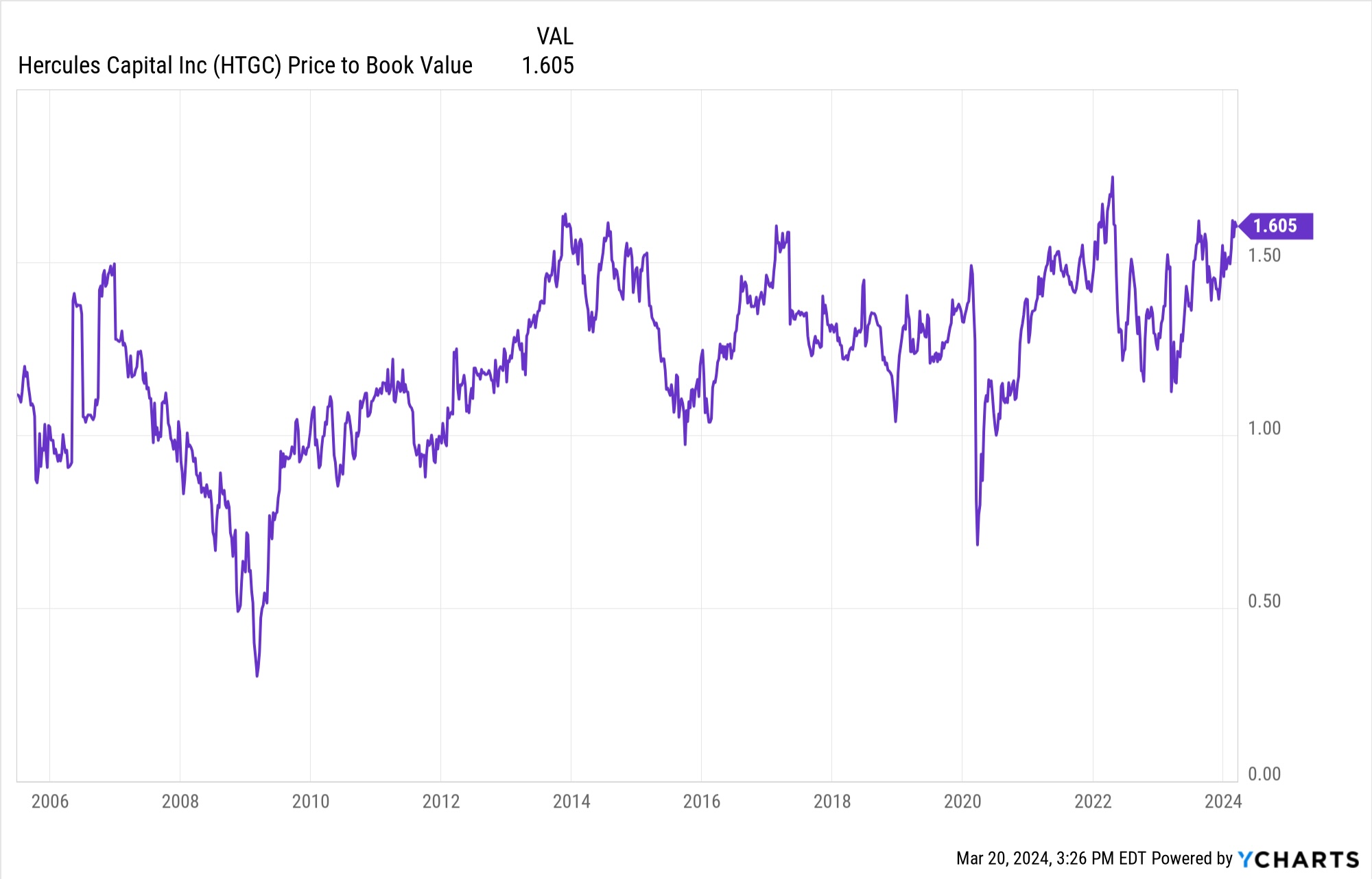

Valuation-wise, times of optimism are not necessarily the best opportunity to buy Hercules. The stock has historically bottomed out near 1X book value, and has gotten as high as 1.6X book value during more enthusiastic times, and we’re close to the top end of that valuation range these days. They use Net Asset Value (NAV) as their benchmark, which is not exactly the same as book value, but it’s pretty close most of the time… and they’ve traded in a range of about 1.1-1.7X NAV over the years — they reported $11.73 as their December 31 NAV, so at $18 today they’re trading at about 1.5X NAV. It turns out that they were pretty close to bottoming out on that valuation last time I wrote about HTGC, in October of 2022… but, well, lots of stuff was bottoming out around that time, so we should remember, when we’re daydreaming about bargain-shopping and telling ourselves that we’ll wait until it gets ugly to buy, that for most people it’s a lot harder than we imagine to buy stocks that are getting punished by the market.

Ah, to have a time machine. What matters is what we have in front of us today, and the valuation today is about the same as it was when Plaehn first started teasing this stock, back in early 2022.

The good news? They’ve raised the dividend for this year, so they’ll be paying out both a 40-cent quarterly dividend and an eight-cent supplemental dividend, for a total of $1.92 for the coming year, so the yield is still over 10% at $18 and change. And they are not in any danger of cutting that dividend, it appears — they say they already have 80 cents per share in “surplus” earnings going into 2024, so that covers a fair amount of the annual dividend even if things get a little rocky for a couple quarters.

Will they get rocky? I have no idea. The big driver is the health of the venture economy — how well technology and biotech companies are doing, whether they can keep investing in expansion and paying their bills, and that seems to be generally pretty good right now. Biotech may not be exactly booming at the moment, and alternative energy financing has been pretty soft recently as people try to adjust to higher interest rates, but there’s always hope for the next big thing in silicon valley, and anything related to data centers and artificial intelligence is finding it pretty easy to raise capital right now. I don’t see any particular sign that Hercules is in trouble… just that they’re not trading at a real discount to their historic valuation range. This is their price to book value chart going back 20 years… no surprise, they’re probably a more appealing buy at times when nobody wants to buy them, but that’s true of just about any relatively steady company:

So what’s the potential if you buy when it’s relatively expensive, like it seems to be today? If you bought HTGC back in the summer of 2014, when it was also trading at about this same valuation (1.6X book value), you would have generally trailed the S&P 500 most of the time for the past decade, sometimes by a wide margin, until just catching up recently, so that’s probably as close as we can come to a reasonable guess about what happens to them in the future.

And yes, as you might expect, that return was essentially all from the accumulated dividends — that’s the S&P 500 total return since August of 2014, in blue, compared to the HTGC total return including dividends in orange, and the actual share price of HTGC in purple.

Sentiment is often expressed in the dividend yield, since most people (rightly) own stocks like this for the income, and HTGC is sort of in the middle of the range on that front with the current 10%+ yield — the dividend yield has mostly been in the range of 8-12% over the past decade. On that front, we’d neither be getting a bargain nor whistling past the graveyard today, though we should perhaps note that for big chunks of that time the “risk free” return from government bonds was 1-2%, and now it’s well over 4%, so the competition has been getting stronger:

The math can work out, as Plaehn says, a high current yield that goes up even a little bit, particularly if you reinvest it for 3-5 years to grow the base, can really goose your income… high yields are powerful things. Just keep in mind that this is still a stock, and it’s still essentially a specialty lending company that depends on a very volatile part of the economy, making 3-5 year loans at high rates to lots of fast-growing but often unprofitable young companies, so there can be downturns when bad news hits, or even just when sentiment shifts and people lose confidence in tech and biotech.

Those downturns don’t always look dramatic in the rearview mirror, but if you bought in the Spring of 2022, the prior peak for HTGC as it touched $19 per share, then I’m sure it would have been plenty painful to watch the shares lose 40% of their value in a couple months during that ugly year.

And I don’t know what AI is going to do to the venture capital world and to startups in general over the next few years, but there will probably continue to be volatility… so with companies like this, taking the path of sanity often means watching the dividend, monitoring the financial health of the company to remain confident that they can keep paying the dividend, and trying to ignore the share price. Things definitely got a little worrisome in 2022, but they’ve survived that mini-shock and are back to reducing their leverage and earning a higher return on shareholder equity these days, with plenty of capital available to keep making loans. You can check out their latest investor presentation to get the basic overview, but after my quick check-in today I’d say they’re doing just fine right now… and are priced like they’re doing just fine. Their next quarterly dividend payment is a couple months away, it will probably be declared around May 1 and paid out a few weeks later, so you’ve probably got some time to think it over.

Sound like your kind of dividend investment? Have other high-yield plays or BDCs that you prefer? Let us know with a comment below… thanks for reading!

Thanks!

Great timing on this thread! Tim Plaehn also mentions high-yield ETFs like JEPQ and AMZA in Dividend Hunter. What are your thoughts on them?

Have not looked in great detail at either — there are a bunch of covered call ETFs like JEPQ which seem reasonable, give up some upside for income (though the downside risk is not usually reduced). I invest in AMLP over AMZA, but they’re very similar pipeline ETFs, and they’re not exactly cheap right now but they are usually quite steady — great time

To buy those is when there’s a panic about oil prices and they overreact to the downside, their cash flow doesn’t usually suffer much from lower energy prices, but the share prices often do.

RWAY is another great one. They currently trade at a price to book discount and I’ve been following them for quite some time. They remind me of a publicly traded Metropolitan Fund, and after the recent earnings there seems to be a good opportunity here.

HTGC – I have owned shares for several years and when the price drops I buy more. Consistent dividend payer along with several other recommendations from Tim Plaehn’s Dividend Hunter service. This is one of the few services that I tried and have had good success with and signed up for a lifetime subscription. Tim seems to be very selective on the Dividend Hunter portfolio and does not switch comanies in and out willy nilly 🙂 I am waiting for HTGC price to drop and then I will pick up more. I do reinvest dividends to compound the returns

I have also been a subscriber since the Covid lockdown and have done very well with his picks.

I’ve owned HTGC in the past, but lately have turned to the BDC ETF BIZD, now paying more than 10%, when I want to dabble in that kind of investment, even though it doesn’t seem to mitigate any risk. Their largest holdings at the moment are, in order, ARCC, OBDC, FSK, and HTGC. The next div date is coming up 4/1, I believe. I won’t trade it in the next three days. All of these companies mentioned obviously know what they are doing, based on their track records, but I have a problem with the fact that I DON’T. That runs contrary to Peter Lynch’s golden rule No.1, which is to know what you own and why you own it.

The less comfortable you are with the merits of the specific companies, the more sense an ETF makes. Hard to argue with ETFs in general.

BIZD expense ratio @ 11.17 % is larger than their dividend.

That’s mostly a quirk of the tax law, not a real management fee — because of the way BDCs are taxed, the ETF, which the SEC considers to be a “fund of funds”, has to report the passed-through “acquired expense ratio” of all of the BDCs it owns. You “pay” those if you own the BDC individually, too, you just don’t get slapped in the face with it, in effect the BDC really reports it as part of their operating expenses. The actual management fee charged by the ETF manager is 0.42%, so that’s the only additional fee you’d take on for buying BIZD instead of buying the various BDCs individually. The manager explains it here.

I’ve owned HTGC since Oct. ’21 and while it did tread water for awhile it has picked up nicely. I won’t buy any more at its current levels but will on a decent pullback

Bought FSK a year ago. Shares are only up 4%, but adding the divs has brought the total return to 17.1%. Some divs were reinvested at a higher price than now so the divs haven’t compounded. Not bad, but it’s significantly lagged HTGC with shares up 52% in a year, not including divs. I’m still hanging on to FSK waiting for the market to recognize its low 0.77 P/B and 13.7% yield.