It’s pretty clear that every investment newsletter publisher is on the horn to all its writers and pundits, screaming “Say something about AI!!” That’s the hot trend, the next big thing… or as a friend used to say, “the text pigs sing”… and everyone wants a piece.

This is the way publishing works, of course: to get subscribers, you have to get attention… and to get attention, you have to write about things that people think are going to make them rich. Over the past several years that’s been SPACs, or meme stocks, or 5G stocks, or cryptocurrencies, or the metaverse. Today, with the national fascination over ChatGPT’s launch as a compelling AI “chatbot” and natural language generator, it’s artificial intelligence.

Today’s salesman is Whitney Tilson, who’s selling his Empire Stock Investor newsletter ($49 first year, renews at $199), and, like many pundits have done over the past few years, he is calling AI the business that could “create the world’s first trillionaires.” That quote originated with Mark Cuban, I believe, who started saying about six years ago that the world’s first trillionaire will be an AI entrepreneur, and you’ll see it in essentially every teaser ad for an AI-related stock. The actual quote, at the SXSW Festival in March of 2017, was, “I am telling you, the world’s first trillionaires are going to come from somebody who masters AI and all its derivatives and applies it in ways we never thought of.”

Cuban could well have been prescient, and he did guess at some of the future impacts — noting, for example, that he thought it would be more valuable to study philosophy than to become a CPA or a computer programmer, since AI has the potential to quickly replicate the work of those folks. Critical thinking wins, not mastery of a programming language or a specialized professional skill.

So… shall we do some critical thinking about Whitney Tilson’s latest pitch? Or should we just jump to identifying the AI stocks he thinks we should buy?

OK, fine, we’ll skip over most of the big-picture AI arguments, let me just give you a quick backdrop from Tilson’s ad (we read the whole damn thing, so you don’t have to!)

First, the greed and urgency…

“I am 100% convinced this technology has just hit a critical inflection point…

“Which, if history is any indicator, means there will be trillions of dollars flowing through one niche industry starting now.

“It also means you can be among the earliest to get in….

“From the private sector to the public sector, from the military to the U.S. government…

“Every group imaginable is spending millions, tens of millions, even billions to master this single technology.”

And while the perception of AI has leapt forward dramatically thanks to ChatGPT and it’s human-like ability to write content (including stuff that is completely made up and wrong, an essential part of being human), he does make the point that this has been a long time coming — it’s not just that Mark Cuban made this prediction in 2017, and of course did so because a lot of work was already being done in the field, it’s also that AI has been powering a lot of the stuff we do, particularly online, without really calling attention to itself. Amazon product recommendations use AI, customer service chatbots use AI, self-driving features of cars (like adaptive cruise control) use AI. In Tilson’s words:

“Most people don’t even realize they’re using AI when they do simple tasks like these. When most people think of AI, they think of robots or other highly technical innovations.

“This is why just 33% of people believe they use AI…

“In reality, 77% of us use AI every single day.”

It sure is picking up, though… Tilson says we’ve hit an inflection point with ChatGPT and the other recent advancements that have launched public demonstration projects, and that’s hard to argue with. We don’t really know what the economic impact will be, or how fast it will move, even a computer can’t tell us that, but we sure know that a lot more people are paying attention. And that means more investment will be made, whether that’s a CEO deciding to invest in AI systems to improve efficiency, or an investor speculating on stocks that have “AI” in the name in hopes of making a quick buck.

Tilson says the ChatGPT release in November is akin to the launch of the first internet browser in the 1990s, or the first iPhone in 2007, common arguments that we hear about any new technology that folks think will be a “platform” for building something huge. He said something quite similar about the metaverse in his early-2022 ads, so that provides a little context — he pitched the metaverse as “connexa terra” in January of 2022, and none of the five stocks he thought would be the foundation for this incredible new platform have given investors a positive return at this point. That’s not necessarily an argument that those were bad ideas or bad long-term investments, in many ways they’ve just gone down because everything has gone down (the S&P 500 is down about 11% since then), it’s just a reminder that you don’t have to urgently rush to “greed,” Tilson doesn’t know any better than you or I what’s going to happen to stocks in the next year. You can think it over.

And NOW, finally, we’ll get to the clues. What does Tilson think you should buy to benefit from this surging interest in AI?

“AI is rapidly becoming critical to the way that businesses around the world market their products.

“As former Magnite CTO Tom Kershaw says: ‘The entire foundation on which the internet works is going to be completely redefined.’

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“And one company is leading the way.

“It has already instituted AI tools that analyze customer behavior and create targeted marketing campaigns.

“Already, 4.5 million websites use this company to market and sell their products in 175 countries around the world.”

And it’s got some name-brand people and businesses on board…

“Massive celebrities like Kylie Jenner, David Beckham, and Adele use this company to market their own brands.

“So do huge sports brands like Gymshark, Fitbit, and even the Los Angeles Lakers basketball team.”

But then we get our light-bulb clue:

“This company was originally created to sell snowboarding equipment online.

“Sound familiar?

“It’s a very similar story to Amazon.

“The first couple of years this company was in operation, it had 28 million customers.

“This year, it’s expected to have 700 million.”

And he says that “this company is absolutely dominating the $800 billion global advertising industry.”

Hoodat? Thinkolator sez, of course, that if it’s an online company that started out selling snowboards, that’s Tobi Lütke’s Shopify (SHOP). And yes, all the other clues match… though most people don’t think of Shopify as really an advertising business, it thinks of itself as offering an operating system for retailers (e-commerce websites, selling tools, shopping carts and payments, fulfillment services and warehouses, even in-person point of sale terminals). That 700 million is not Shopify’s direct customers, to be clear it’s the customers of the merchants who use Shopify’s platform and selling tools… though more buyers of products does mean the gross merchandise volume goes up, which means SHOP generally gets a little slice of more sales (from the add-on modules that Shopify merchants use, including Shop Pay, the payment processor which exposes them directly to increasing sales). Their highest-margin business is selling the basic Shopify software subscription that lets anyone open an online store, pretty quickly and easily and without hiring a computer expert… but the fastest-growing part of the business are their add-on services for merchants, including fulfillment services (trying to compete with Amazon’s warehouse network) and stuff like payments and marketing.

Here’s part of what I said about Shopify after their last earnings report, back in mid-February:

Shopify (SHOP) is our other pandemic boom darling whose stock “busted” after the growth slowed down, and it does continue to grow as it attempts to build its global retail platform for small businesses, but it disappointed investors this quarter. And that made it seem as though it’s really the first quarter or 2023 outlook that is determining how investors feel about these stocks — ROKU and TTD had relatively optimistic outlooks, compared to analyst expectations, while Shopify’s guidance, like Toast’s, was relatively pessimistic.

The fourth quarter was quite strong for Shopify, with seven cents of earnings per share (analysts had predicted a two-cent loss), and 25.7% revenue growth over last year. Their gross merchandise volume grew only 13%, but they took more share in payments (they processed payments for 56% of sales, up from 51%), so that helped. They did raise prices, which could provide a boost in 2023, and they did some big layoffs last year, but they’re also still dealing with the costs of growing their fulfillment network. Still, they expect to improve margins a little bit in 2023, so that’s good — the guidance for the first quarter was for revenue growth in the “high teens,” and that seems to be the challenge at the moment, that’s a hair below what analysts were forecasting (the analyst estimate was $1.45 billion in first quarter revenue, which would be 20% growth). I don’t know why that would be so critical, as with essentially all retailers the first quarter is the least meaningful one for Shopify… but, well, investors get some new data and they feel the need to react to each incremental bit of information, that’s the way the Wall Street Overreaction Machine works.

This is another challenging growth company that is not currently profitable enough to reasonably come up with a valuation based on profits or cash flow. For a long time I watched the basic level of 15X revenues as a buying zone, since that had worked as a floor in the years before the pandemic (during the pandemic, of course, it soared to ridiculous levels, more than 50X revenues), but that certainly didn’t hold as a “floor” last year, the stock dipped to about 7X revenues when investors were panicking about all growth stocks during the worst part of the inflation spike. Any real valuation work with Shopify would require extrapolating their growth out five years and arbitrarily deciding what their margins will be like at that time… we can bang our heads against that math problem, I guess, but it won’t do us much good, the inputs are too mushy….

If you want to make some long-duration bets on growing platforms that can become the tech giants of tomorrow, I think Shopify, Roku, and Toast are all rational speculations along those lines… but they are still in “growth over profits” mode, and that’s inherently dangerous and means there is no real floor for the share price if things get ugly. They are well-financed, and have sustainable businesses, so they should survive whatever tough times the market throws at them… but they haven’t gotten over the hump yet to being self-sustaining and profitable. The potential is that they can become so large that they can’t help but gush enough free cash flow to be profitable… though they’ve also been quite profligate in their spending in the past, including on stock-based compensation, so they have to keep proving that they can grow with some discipline after their adjustments to an inflationary and lower-growth world over the past year.

These stocks have different drivers to a large degree, of course, but they also rise and fall as a group when big-picture inflation and growth worries rise and fall, so if you’re at all worried about volatility, it’s important to limit the overall allocation to these kinds of ‘stories.’

What’s the AI connection? All indirect, if you ask me. Yes, Shopify and its software-development partners (people who sell plug-ins and tools to Shopify users) do offer some “AI” features, like Shopify Magic’s AI-generated product descriptions, and they’re pretty cool and may work great, but I don’t imagine they’ll dramatically move the needle for Shopify’s revenue anytime soon. I’m sure they use a lot of machine learning in optimizing their products and code, and in marketing, but those are really table stakes for a company that’s effectively competing with Amazon.

I really like Tobi Lütke and the company he has built, but Shopify is above my “max buy” price right now, if only by a hair, we’ll see if that valuation judgement changes when they report next, in about two weeks. Today Shopify is valued at about 11X sales and at about 200X 2024’s forecasted adjusted earnings (it was just barely profitable last year, and about the same is expected this year, though that’s on an adjusted basis — they use a lot of stock-based compensation, so on a GAAP basis they likely won’t be profitable even if they double their sales in the next two years. Like Amazon in the early days, they remain fully committed to growth over profitability — sometimes investors buy into that story, sometimes they don’t.

That’s a pretty tangential play on artificial intelligence, though, so what else is Tilson pitching? He points us to several “platform” companies in AI that should also do very well, with another chunk of bait on the hook being a special report called “Buy the Platforms: Your Best Shot at a 500% Winner”

So, um… what’s a platform? From the ad:

“One of the best ways to profit from any new technology is to ‘own the platforms.’

“Platforms are businesses that create systems so that other companies can develop their own projects.

“Google is one of the most famous platform businesses – it makes money connecting millions of businesses around the world with customers…

“And the company returned up to 5,000% gains over the long run.

“eBay is another great platform business. Since the early days, its stock has gone up more than 11,400%.

“First-mover advantage here is huge, and that’s why I want to show you how to invest today in three AI platform companies I believe will dominate this space and potentially make early investors many, many times their money in the years to come…”

So… what are those stocks? The clues are a little thinner here, let’s see what the Thinkolator can come up with…

“The first of these companies is THE dominant player in this space – it provides AI platforms for 100,000 clients…

“One of these clients is entertainment titan Disney, which is using this company’s AI to build tools that let it tag nearly a century’s worth of content.

“Other multibillion-dollar firms also use this company’s AI platforms, including Intuit, 3M, and T-Mobile.”

And growing by buying up startup competitors has been a big part of “platform” companies for a long time, so we also have this:

“This company has just made seven huge acquisitions in the AI space.

“I recommend you buy this business’s stock immediately and hold for the long term. I think it’s going to be a huge winner in the AI race.”

Depending on what you mean by “just made,” that could apply to almost anbody… hell, SurveyMonkey has made “seven AI acquisitions” (it also changed its name, to Momentive (MNTV), and sometimes refers to itself as “Momentive.ai” — lots of folks signing up for “.ai” URL’s these days. That’s not the secret stock here, though, of course — the company Whitney Tilson is almost certainly teasing here is… good ol’ Amazon (AMZN). Sometimes the big keep getting bigger.

Amazon, like Alphabet and Microsoft and other tech titans, has been investing in AI for decades — AI is what powers the increasing efficiency of its delivery and fulfillment networks, and its product recommendation engines, and, yes, there are lots of AI products within Amazon Web Services that are used by other companies. Including their big effort to add metadata to old Disney filmed content. And their press release about new AWS tools for using Generative AI even highlighted 3M and Intuit as customers. And yes, they do claim to have played a major role in democratizing machine learning, and that they’ve made it accessible to “more than 100,000 customers” in the press releases about their new Bedrock platform. Microsoft Azure and Google Cloud are real competitors now, AWS is no longer the only real choice for companies trying to build new technology platforms in the cloud… but AWS is still the biggest, and they’re clearly not standing still.

Can’t argue with buying Amazon here, I just updated my thoughts on Amazon and added to my position last week… and I don’t know if they’ll continue to be an AI leader as this technological revolution continues to build steam, but it seems a pretty high-probability bet.

Next?

“The second platform company I recommend that you invest in today has perhaps the most advanced AI platforms in the world right now.

“Already this company has developed platforms to:

- Generate computer code from high-level mathematical operations

- Accelerate the process of deep learning

- Generate visualizations for scientific experiments

- Help researchers better understand epidemics

- Create 3D maps of the human body

“And that’s just for starters.”

And this one’s been making acquisitions, too…

“This company has also recently made 18 top-line acquisitions in the AI space, ranging from language processors to chatbots to automated mapping.

“And right now, the company is trading at a huge discount thanks to the recent stock market volatility that hit tech stocks.”

They’re apparently working on other important stuff, too…

“Not only that, but this company is addressing some of the biggest problems we face in the world… gender bias, medical care, and renewable energy, to name a few.

“And now that we’ve hit the inflection point for AI, this company’s share price could blow well past record highs.”

That could also really be any of the large tech companies, and I would hesitate to be at all certain about this answer… but the Thinkolator sez our most likely pick here is Google parent Alphabet (GOOG, GOOGL), which has has the broadest portfolio of “outside the core” R&D projects of any big tech company over the past 20 years, and is involved in all those things hinted at (though none of them come close to “moving the needle” for Alphabet’s earnings, of course).

In recent times, particularly because of their high dependence on advertising revenue, Alhabet has generally been the second “cheapest” of the big tech firms, behind only hated Meta Platforms (META)… but they are probably also the single company that has spent the most on AI research, and relied the most on AI in its core products (particularly Google Search). And thanks to Microsoft’s splash with Bing and it’s integration of OpenAI’s ChatGPT “conversational search,” there has been a recent narrative that Google is behind in AI, which arguably took about 10% out of the stock price recently. (In gossipy Silicon Valley, there also seems to be a lot of delight about how OpenAI was founded in part by Google engineers who couldn’t do what they wanted within Google, and that DeepMind, the AI company Google bought a decade ago, has been hamstrung by its corporate parent, or that Google held off on AI chatbots because of their ethical worries… but also that Alphabet has invested in yet another startup, Anthropic, that was built by former OpenAI engineers and has yet another potential rival AI Chatbot in development. Beyond the headlines about “winners” that move stock prices, there’s a soap opera in full swing.)

I’m not at all certain that this is Tilson’s second “platform” pick, but it’s the best match we’ve got. And it’s one of my largest and longest-held positions, so I can’t say I disagree with him on this one, either, even if I don’t see any high probability that GOOG shares will “blow past record highs” in the near future. Here’s part of what I wrote about GOOG when I was doing a bit of ranting about the new speculative mania in AI back in February.

“I am pretty confident that Alphabet has invested more into artificial intelligence R&D over the past decade than Microsoft has, much of what they offer is powered by advances in AI behind the scenes, and I suspect that their capabilities, including the tools that Deepmind has built since Google bought them almost a decade ago, are not markedly inferior to ChatGPT… but that “Google failed, ChatGPT and Microsoft won” narrative is exactly what twitchy stock traders and content-starved pundits love to focus on: A great story….

“The biggest risk to Google’s share price, in the near term, is probably the fun “someone is finally beating Google” story, and the fact that Microsoft CEO Satya Nadella is talking about taking on Google on its home turf. Just like Google can afford to take on Amazon and Microsoft Azure in cloud, so Microsoft can afford to take on Google in search. Don’t know how it will work out, or if they’ll win, but they can definitely afford to try….

“It is, at least, fun to hear companies competing for attention and trying to build cooler products in the big tech sector, which had drifted to become a land of natural-seeming and almost unassailable monopolies — that’s good for everybody. Alphabet has arguably gotten lazy about improving some of their core products, but the AI excitement of the past couple months has already given them the kick in the pants that they need. The ChatGPT/Bing challenge was enough to bring Google cofounders Sergey Brin and Larry Page back to work on the core of Alphabet’s business for the first time since at least 2019, so it should be an interesting year.”

I’ve owned Google and then Alphabet shares for 18 years now, so I’ve held through some very rough times for the company — that will probably be the case a decade from now, too, though I’ll reserve the right to change my mind someday. Right now, the share price is perfectly reasonable, I could justify buying GOOG up into the $130s, and I added a bit last Fall, but I did bump down my valuation earlier this year so it’s currently a bit above my “preferred buy” level ($94).

What else?

“… there’s one more platform company that I recommend you buy shares of right away…

“It looks to take AI to a new level, and over the next few years, I expect it to become one of the biggest AI companies in the world.

“Right now, this company isn’t associated with the tech elite, but it could soon be placed right up there with the FAANG stocks (Meta Platforms’ Facebook, Apple, Amazon, Netflix, and Alphabet’s Google)….

“Its AI chips are lightyears ahead of the competition. Its newest system has been described as an “AI supercomputer in a box.” And it has built the most powerful chip system ever created.

“In other words, just as millions of companies seek out Amazon’s AWS to power their websites…

“Millions of companies could come knocking on this company’s door as they strive to power their own AI efforts.”

And we’re told that Forbes has called this “America’s most important company.”

So what’s the story, and what’s the stock?

Well, whenever you see “Forbes called this…” or “The Wall Street Journal says company X is…”, remember that those are publications that publish a lot of opinion pieces, in addition to news. And Forbes, in particular, has been quite open as almost a free-for-all blogging platform for the past decade or so. If you felt that the old paper Forbes magazine from the 1980s had any gravitas, it’s worth being mindful of letting that gravitas seep over into today’s Forbes.com. That article they quote here, actually, was from another financial newsletter guy, it’s from an article Stephen McBride of RiskHedge posted on Forbes.com a couple years ago. It’s a fine article, and the title will tell you our answer today: “Nvidia’s Chips Have Powered Nearly Every Major AI Breakthrough”

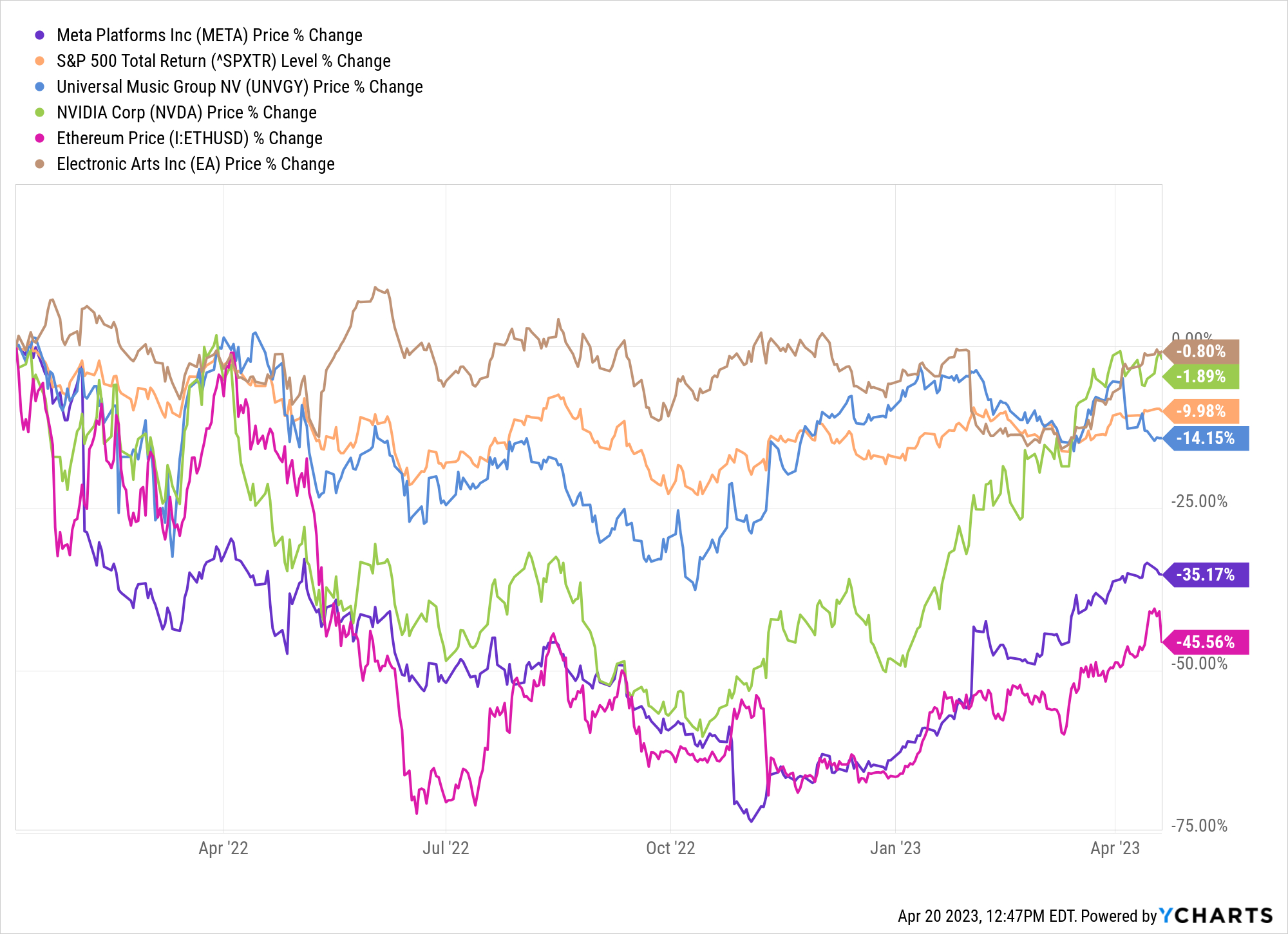

So, yes, this is a pitch to buy NVIDIA (NVDA) as an “AI Platform” company. And that’s certainly a consensus move, and it is the reason why NVDA shares have doubled in the past few months… they’re one of the few growth companies that is now back near its late-2021 highs again. Just for some context, NVDA shares were below my “max buy” price in mid-January… and now they’re $100 over that price. It’s crazy, to be sure.

But yes, if you want to buy the company that is most directly exposed to the “picks and shovels” of AI, NVDA is probably still the surest bet on that front. I can’t tell you that it’s a sure enough bet to pay a whopping 150X earnings for the shares… or, if you want to be more charitable, 60X the forecast for next year’s adjusted earnings… but NVDA is still really at the center of AI hardware. At least for now. Their high-end GPU chips and accelerator chipsets for data centers are doing a ton of the heavy lifting for AI — those complex questions that you ask of ChatGPT have to go back to the data center, where (probably) NVDA chips that have been “learning” patterns of speech and language are fed the new prompts, and work like mad to build a natural language response. That’s why ChatGPT answers take a few moments to be formulated — there’s a lot of computing going on in the cloud to build those answers, and was a ton of computing going on before that to build models and learn to get ChatGPT to the point where it could build answers to questions.

Part of this is technological leadership, part of it is superior hardware, and part of it is habit — because NVIDIA focused on AI processing early on as one of the prime uses of its GPU chipsets, and also built software for AI projects, most of the AI engineers who have been coming up with stuff over the past decade have probably used NVDA chips and systems. Most other specialized kinds of chips have become commoditized over time, but NVDA has been able to keep innovating and stay in the lead, which is why they’re trading at valuations which would be patently ridiculous for any other semiconductor company. It may well work out great for NVDA still, even if you buy at inflated prices today… but when you buy a stock at a high valuation, you have to accept a wider range of outcomes (and you probably have to be more patient).

Here’s a brief and slightly updated rehash of what I said about NVDA after their February earnings update:

NVIDIA is still projected to get back to about $4.50 in earnings per share in 2023 and grow from there… but the sentiment has clearly shifted up and down and back up several times over the past six months — mostly because people can again see the future potential dominance of NVDA in AI processing, and because now that Microsoft is putting its heft behind a consumer-facing AI project (ChatGPT), AI feels more real to individual investors. It’s not just the amorphous and rapidly growing technology theme that has been building for a decade under the surface, which was and has been true, AI is a huge part of what has made autonomous driving and Google search and Amazon’s recommendations and so many other things work better over time, but now AI has a focal point in ChatGPT, and I guess that makes it easier for investors to take it seriously.

I did sell some call options on part of my NVDA position, I think we’re in a valuation range that’s tough to justify these days so I’d be willing to sell down my holdings a little, but I expect to remain an NVDA shareholder for a long time, and would happily buy some more if we drift into my buy range (which is currently unchanged, I still think $173 is the most I’d want to pay) — nobody else seems as capable of being a pivotal hardware player in so many important technology trends, all while their longtime foundation, high-end PC video gaming, continues to be much stronger than analysts expect. Great company, and momentum traders are happy to see it back in the market’s good graces, but as a long-term investors this is not a stock I want to buy when investors are most excited about it.

I’ve been selling calls against my NVDA position all year, and they haven’t been exercised yet, but my current crop expires tomorrow, so I might end up selling some of my NVDA at $290 if we get that far. I’d be OK with that, even though I might have to wait a long time to buy those shares back at a reasonable price.

And that’s it for secret teaser picks… I should note that these are all stocks that Whitney Tilson has teased and recommended before, for a variety of different reasons — Amazon, Shopify and NVIDIA were all in his “EOD Will Mint Millionaires” Pitch a few months ago about the “Everything on Demand” trend, Alphabet’s Waymo and NVIDIA were both in his “Transportation as a Service (TaaS)” pitch about three years ago for their autonomous driving connections, and Amazon and Alphabet were both in the “Perfect Portfolio” he pitched when he was launching Empire Financial back in 2019.

So… have any favorites of your own in this space? Think the more direct AI pitch by Tilson’s colleague Enrique Abeyta is more compelling (that was C3.AI, which he’s been pitching for a couple months — “My #1 ChatGPT Stock for 2023”), or prefer other hopefuls or startups, or, like Tilson, do you like some of these larger players who have been working on AI for years? Do let us know with a comment below… thanks for reading!

P.S. Tilson also throws in a pitch for what he calls “The 20X AI Moonshot,” a company that “just entered into a nearly $10 million deal with the U.S. Department of Defense” and is working on next-gen vaccines, living medicines, enzyme discovery and synthetic biology, and he says it’s less than $5. I haven’t dug deeper into that one of late, but I suspect he’s re-teasing Gingko Bioworks (DNA) here, a stock he has been pitching as the “next great monopoly” and then the “$4 inflation stock” and, later “$2 inflation stock” that he would buy for his wife’s retirement account (I suspect he actually likes his wife, but also that she doesn’t need to be cautious with her retirement account). I last covered that pitch of his here, if you’d like to dig into it yourself…. Lately, Tilson has been saying that he thinks it “just bottomed,” the stock has been bumping along in the $1.25-1.35 range for a month or so.

Disclosure: Of the companies mentioned above, I own shares of Amazon, Alphabet, Shopify, Toast, Roku, The Trade Desk and NVIDIA. I have sold covered calls on NVDA at $290, so those could be exercised and result in a sale, but other than that I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules (and I will not trade or otherwise close those NVDA option positions before they expire tomorrow — if the stock is above $290, they’ll be exercised, if not, they’ll expire worthless).

By VRSSF and put it away!

Lots of talk there, eager to see revenues.

Does anyone know about Dragaanfly (DPRO )? The company builds drones and I think one of them is in use in Ukraine.

Be careful. See today’s or yesterday’s press release

NVDA is the play for AI

Hey – no fair countering hucksterism with reality!

Or maybe we should be lauding Tilson, not the Stock Gumshoe, for his ethics.

Tilson has been hyping (maybe) Ginko Bioworks relentlessly while its stock tanks – halves, then halves again! But if the stock was a “20X AI Moonshot” at $4, then surely it’s twice as good – a 40x moonshot! – at $2, & nearly twice as good AGAIN at under $1.3o today.

Far from castigating Tilson, we should admire his honesty & tenacity. It would be disingenuous to stop touting it every time it plummets: that just makes a sure thing more affordable.

If it crosses the $1 threshold into penny stock status I expect Tilson to massively increase his promotion of it. It’s the honest thing to do? Certainly the sane thing to do if he (or his firm) has any money riding on it.

If Tilson’s wife ever looked at her portfolio, she’d probably file for divorce, in which case that portfolio might get a huge boost. It looks like the conclusion here is to just buy the tech giants of the NASDAQ, who have been using AI for years and that is what has helped them to be so successful. Why all the buzz?

Interesting idea. Compliment the guy for continuing to recommend a stock every time its down another 50%. Theoretically at least, since it can never go to zero, I plan to buy when Saint Whitney recommends it at $.0000000001.

These giants have spires. As tall on this earth outlooking, as those of government, those of churches, …

…I can tease, too. Please deposit 15 million for me to continue.

50% of AI researchers predict that there is a 10% or greater chance that humans go extinct from our inability to control AI. Can’t wait for that!!

ive been around a while and remember hearing that in leonardo da vinci’s time when there was a technological revolution:)

I think of ChatGPT as an app, not a platform, that combines limited internet supplied data with a database of 100 years of Chinese fortune cookie slogans to fulfill requests with interesting but unreliable answers. The app has surely pushed AI to the top of the wiz bang list of the next greatest things since the sliced bread idea, or even the invention of TP!

Worth a Sherlock Holmes look would be the stock being pushed by Tobin Smith and his Transformity Wealth Management company, which now seems to have joined forces with Chris Rowe, founder of TMI. As one of their subscribers I won’t give away the secret stock, but I have found the lengthy sales pitch selling their new service to be full of clues, and available on YouTube (this is not the equally lengthy report on the stock, which is included in Transformity membership as a freebie report):

https://www.youtube.com/watch?v=S1HOAOB_Plw

I’d be interested in a second opinion by our resident guru, Travis, on the vast amount of info Tobin has put together on this supposed AI platform stock. Is the company alone in all the AI goodness they are about to release, which is centered around their open source AI operating system, or maybe they have competition unforeseen by Tobin? It would be nice to know before renting a bigger truck to back up to the loading dock whether this stock could end up in the graveyard next to Betamax recorders and Blackberry phones, or could it really be that promising?

Note that the link in my previous post is not the one I intended, and I can no longer find the right one. In the meantime I’ve found that Mr. Smith has publicly released the stock symbol on his Twitter site – #TRANSFORMITYRESEARCH: Tobin Smith’s Official Feed, and coolsoupy has mentioned it in the first post here.

The full write-up can be found on the stock’s Yahoo Finance page under “View all posts” in the Conversations section. Look for a 15 April post by Jed.Clampett which contains only the Mailchimp link to the report.

Is this the Lumber Liquidators guy? No thanks. Anyone can recommend a stock when its at the bottom of its cycle, of course its going to make money going back up. Ill stick with Nvidia.