Time for another de-tease of an Empire Financial story… this time it’s an ad for Whitney Tilson’s Empire Stock Investor ($49/yr), their “flagship” entry-level publication. Tilson recommends a variety of stocks in this newsletter, but it’s mostly focused on large-cap stocks and aims to hold on to investments for at least 3-5 years.

The ad comes with some other “special report” ideas and recommendations, including the “Perfect Portfolio” — he doesn’t hint at what those are, but I expect they’re probably recycled from past newsletter issues and ads… he did pitch a retirement-stock-from-whitney-tilson-and-empire-financial/">“perfect portfolio” of five stocks a few years ago (BRK-B, AMZN, GOOG, FB META and MO), and in the past few months his teaser machine has been mostly pumping out ads for the “Perfect 10” Inflation stock (DNA) and the “Keystone” $4 pick for the “Energy Supercycle (TELL).

Those last two have so far been pretty disastrous this year… but still, I’m curious, what’s he pitching now?

It’s all about robotics… and about a secret robotics stock that he’ll be revealing tomorrow evening in his “special event” presentation. So let’s see if we can name that before he does, shall we?

First, a little look at the ad…

He takes that “Pearl” in the headlines from the name of a particular helper robot:

“Pearl is a robot that works at Ana Maria Oyster Bar near southwest Tampa.

“She works 7 days a week, never takes a day off, and only costs $2.50 an hour.

“Now, no one wants to see robots take over ALL the jobs that hardworking Americans need for their livelihood.

“But with rising wages and employees becoming harder to find – as you saw from the chart I showed you earlier…

“Robots have become an ideal and cost-effective alternative for business owners.

“Which explains why 50% of American restaurant operators are planning to use more robots like Pearl over the next few years.”

Restaurant robots are for the most part still pretty gimmicky, at least as I see it — I’ve had robots bring me my food on a tray before, too, and so far they sure don’t seem all that much more cost effective, but I guess they’re appealing substitutes for shuttling food and dirty dishes when the high school kids don’t want to be busboys, and progress will continue. That particular robot is enough of a novelty that it got the local TV treatment back in February, in case you’re interested… looks like it costs a few thousand dollars.

(That name “Pearl, “by the way, was given to that particular robot by the restaurant — it gets different names at other restaurants. If that intrigues you as an investment idea, there are a variety of different companies selling those robots, which for the most part look like tall Roombas with shelves and an internal map of the restaurant and the table locations that they can navigate — brands include the CLOi from LG, the Dinerbot from Keenon, and many more, there’s a lot of experimentation going on and no obvious leader that I’m aware of.)

That’s just an attention-getting story about robotics, of course, the big story in robotics and automation over the past few decades has really been on the industrial side, from the first welding robots on the shop floor in Detroit to the almost unrecognizable automatic factories and warehouses that are being built around the world right now. And that’s what Tilson hints at as his “Pearl of all investments” recommendation… in his words:

“I’m writing to you today because I’ve found the best way to play this global surge in robotics and automation…

“Not only are ALL this company’s factories fully automated…

“But with its fleet of high-precision robots that meet the needs of ALL types of industries I mentioned earlier – and its 16,289 patents – it’s set to become a global robotics leader…

“Right now, it’s flying under the radar – which is also why I love it so much…

“But when Wall Street finally wakes up to this story, I expect this company’s stock could soar at least 70%.

“And that could very well prove to be too conservative.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“Over the long term, shares could go double or even triple from here.”

Given the one specific clue, that claim about the number of patents, the Thinkolator says this must be Fanuc, the somewhat secretive Japanese company that has for many years been the global leader in robotic automation for factories — they are primarily known for making, selling and servicing industrial robots and other factory automation tools.

They’re not nearly as secretive as they used to be, about seven years ago they started to open up a little bit and allowed a little press coverage of their formerly secret factory complex in Japan, probably partly because they were criticized by activist investor Dan Loeb for their lagging shareholder returns and poor shareholder communications. Probably the best background story I’ve read on Fanuc was in Bloomberg about five years ago, if you’d like some more of the story. Around the same time, they caught the eye of a few investment newsletters, too, so we’ve covered Fanuc once or twice before. They’re still not covered very regularly in the US, so to some degree they’re “unknown,” but Fanuc is a very large company, with a market cap of just under $30 billion.

Fanuc trades primarily in Japan, where most of its facilities are located and where their own highly automated factories churn out their robots, but they export much of their production, and their biggest customer is presumably still China, and heavy manufacturers like automakers are still responsible for a lot of the end market demand. The stock trades at 6954 in Tokyo, but is also available to investors as a US depository receipt at ticker FANUY (there’s also an over-the-counter ticker, FANUF, which is likely to be the symbol you use if your broker, directly or indirectly, buys the shares for you on the Toykyo exchange).

What has it been like to be a global leader in factory automation over the past decade? Well, if you’re a Japanese company facing a tough market at home and a faltering currency, not so exciting — this chart shows the annual net income for Fanuc over the past ten years (purple), the total revenue (blue), and the total return for Fanuc investors (orange), all in US$. Not so impressive, essentially a “lost decade”:

Some context? Here’s that same chart with the average performance of Japanese large-cap companies for comparison — that’s the iShares MSCI Japan ETF in green, also in dollars. So Fanuc has been disappointing in the context of its own market.

And one more, just to belabor the point. We are hard-wired to obsess over only the recent terrible performance of the stock market in the US, but here’s that same chart with the S&P 500 added, in pink — US investors, in general, have done a lot better than Japanese investors over the past decade.

So… Fanuc is in a tough market, with some of its customers capacity constrained or still shut down temporarily (like the automakers, or like some parts of China), and with the Japanese Yen being destroyed by the US$. As an exporter to manufacturers around the world, largely in China and the US, Fanuc ought to do well, with a weaker currency that makes its exports look more affordable… and yet, it has been a moribund investment for a long time.

Why? I don’t really know. Maybe some competition, maybe just the challenges of being based in Japan right now.

Is that about to change, or might Fanuc at least have another of those “up” cycles that is has had a few times in the past decade? Maybe.

They seem to still have a strong market position, and a well-known brand name in their space, but their most frequently mentioned competitors have generally been better investments over the past eight or nine years — that’s Yaskawa Electric (YASKY) and Keyence (KYCCF) in Japan, Kuka (KUKAY) in Germany, and the Swiss-Swedish ABB (ABB). Here’s the total return for those five for as far back as we can go (Kuka trading data doesn’t go back quite ten years) — that’s Keyence and Yaskawa beating the S&P 500, and Fanuc way down there in the bottom as the worst performer for that time period:

How do things stand now? Well, Fanuc is cheaper than most of those competitors — the only one that’s less expensive, using the Price/Earnings multiple, is ABB, which is also a much more diversified company. But it’s not really cheap like some of the industrial companies these days, not at 20X earnings (a lot of automakers and big industrial companies trade at single-digit PE ratios at the moment), it’s just cheaper than the closest competition.

How about the growth prospects? It is being widely speculated that globalization is dying, and that the buildup of local manufacturing capacity is going to be a key driver of economies in the future, as we all try to rely less on each other — if that happens, I guess we’ll need more factory robots and automation tools to outfit those new factories, so that could be a driver of future earnings, though it would theoretically also cause some weakness from Fanuc’s big customers in China.

Right now, though, revenue growth estimates are not very high — analysts do think Fanuc will grow its revenue in 2023, following a strong surge in 2022, the current estimate (according to the FT) is that after 33% revenue growth in their fiscal 2022, Fanuc will have revenue growth of 14% in the current fiscal year (which is almost half over now), and be pretty flat in the year after that. The estimate for earnings growth is about the same, roughly 15% in the current year and then flattening out to almost no growth in FY 2024.

The challenge? Those estimates are all in Japanese Yen, and the Yen has lost 20% of its value against the US$ just so far this year (and 50% in the past decade), so some of these macroeconomic factors make a big difference. A collapsing currency can quickly turn that apparent growth in sales into a decline in adjusted sales, at least if you’re a US investor and are thinking in US$ — Fanuc does sell plenty of stuff in Dollars and Yuan and Euros, but it looks like it’s the “adjusting back” of those currencies to Yen when they report their results that is generating the growth, not a big increase in the real business.

The business did falter during COVID with all the factory shutdowns, and has bounced back some after that, but the revenue per share, in US$, has been essentially unchanged in a decade, and during that time most of the key operating numbers have also gotten worse (gross margin and operating margin have both generally been trending down, meaning their profit from each of those dollars of revenue is also falling). If there’s a burgeoning giant within Fanuc — and there may well be, it is a sector leader and a well-respected brand — then it’s still fairly well hidden when you look at their financial results. You’d need a qualitative reason to be excited, there isn’t much of a quantitative one.

Maybe that reason will be some resurgent strength in the Yen? Predicting that is way outside my circle of competence, but I guess anything is possible. The US Dollar is beating all the other major global currencies this year, but it’s especially beating the Yen. This is not a precise measure, but here’s the performance of a few of those currencies in US$ ETF form over the past decade, using the Invesco CurrencyShares ETFs:

The situation is very similar for Yaskawa Electric and Keyence and many of the other players who I haven’t mentioned, though Keyence has generally been more profitable and carries higher margins because they’ve outsourced more of their own manufacturing (and, to be fair, they make tools for automated factories, not so much the big automation systems or the actual robotic arms, they’re more likely to build the barcode readers and the measuring systems). In general, for the Japanese factory automation leaders like Fanuc, Yaskawa, Daifuku and others, things look decent when it comes to the current growth and performance in Yen terms… but not so impressive in Dollar terms.

For comparison, ABB also does a lot of their work in non-US currencies, especially the Euro, and sells a lot into the US. It’s also US-listed, so we have some forecasts and projections in US$ to work with — analysts think ABB will grow by a 2-3% or so on the top line, and that their EBITDA will pick up again after a very bad 2022, but will still be below 2021 levels for several more years. So… not so sexy there, either.

But really, none of these companies are doing particularly great — with the possible exception of Keyence, a company that has focused more on some higher-margin parts of the factory automation business (to be fair, I should probably compare Keyence to Cognex (CGNX) or Faro Technologies (FAR) or Zebra Technologies (ZBRA), not Fanuc… but, well, this article is almost over). Factory automation is indeed a growing trend, we all see more and more robotic factories, and more fully-automated factories and distribution centers, but the biggest companies who have largely been responsible for automating those factories and selling those robots over the past ten or twenty years have not been particularly great investments.

Is that going to change? Is Fanuc, arguably still the leader, now cheap enough to be worth a gamble, as factories around the world look to automation to solve the current labor shortage? That seems to be the argument from Whitney Tilson, if we read between the lines of his teaser pitch. I don’t own any of these stocks, and don’t feel an immediate compulsion to change that.

So go forth, dear friends, researchify to your heart’s content, and decide whether you want to jump aboard the Fanuc bandwagon. It’s hard to argue that there’s a good reason to rush this research, so don’t let the FOMO bug get into your Fanuc thinking… but please do share with your favorite Gumshoe readers. Ready to buy Fanuc? Think it will remain “dead money?” Have other favorites in the robotics and automation space? Let us know with a comment below.

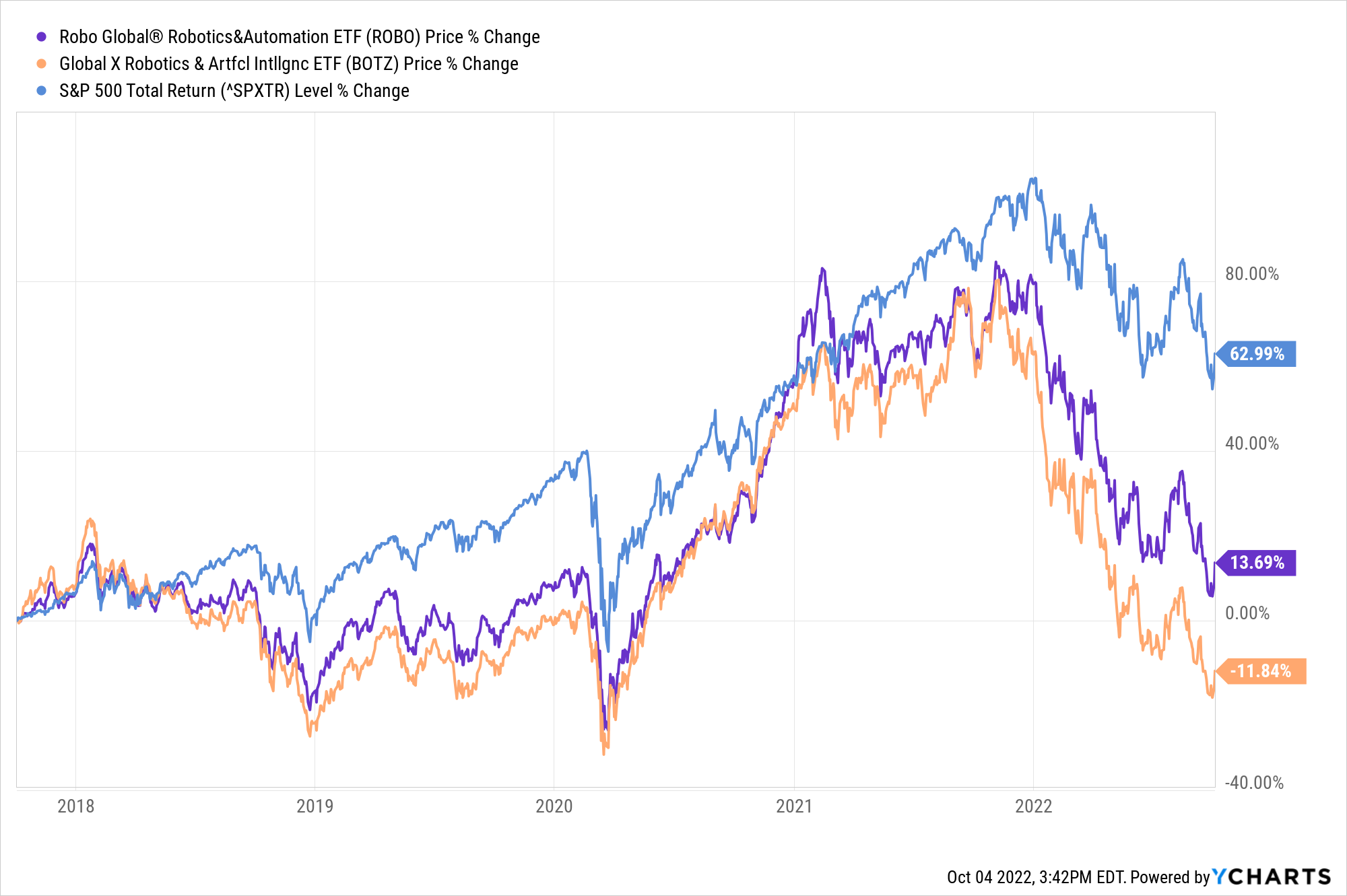

P.S. And yes, as you might have guessed, there’s an ETF for that — if you want to bet on robotics and automation as a growing trend, there are actually two decent ETFs to choose from. Robo Global (ROBO) is a little more expensive and much more diversified, Global X Robotics and AI (BOTZ) is more concentrated and has a much larger allocation to Fanuc, ABB, Keyence and Yaskawa, along with some others. They’ve mostly traded together, as you’d expect, and both have trailed the S&P 500 pretty dramatically… though as with so many other “story” stocks and tech stocks, that’s mostly because they crashed a lot harder this year than the broader market did.

Disclosure: Of the companies mentioned above, I own shares of and/or call options on Amazon, Alphabet, Berkshire Hathaway and Ginkgo Bioworks. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Can you pay Pearl? Does this reduce the tip? C’mon man! Give me a reason to go to a restaurant that has these. If it had a slot to put coins in and pick a song, maybe.

My “Pearl” faithfully cooked and served me and the rest of the family dinner for my first 18 years. No tip was asked for, just a “thank you” and occasional help with the dish washing. She was, of course, my dear mother who, sadly, is unable to serve anyone any more. No robot could have ever replaced her.