We’re starting this week a little late, dear friends — mostly because I’m coming off of an incredible high and some rough winter travel, I just got back from seeing my Detroit Lions win their first playoff game in thirty years, in person, in the loudest and happiest crowd I’ve ever celebrated with. Wow, what a weekend!

But yes, it’s back to work now… I don’t have my voice back, but I can still type, and that means we’re back to sniffing out some teased stocks.

And I’m a sucker for people who actually email me and ask personally, so it caught my eye when a reader forwarded this comment along…

“This isn’t exactly a teaser per se, but I know you love royalty (ish) businesses and Dan Ferris sort of teases on in this freebie Stansberry daily email. I think it’s fair game because it’s really just a marketing letter in reality so if you feel inclined, I’d appreciate it if you could take a peek at this one he evidently just recommended in his Extreme Value newsletter.”

And he’s right, I do love royalty businesses. And I mostly like the way Dan Ferris thinks, and we’ve had a few investments in common over the years. So let’s see what’s he’s up to now… this is from that Stansberry Digest email that was forwarded to me, which in turn is sort of a sales pitch for Ferris’ Extreme Value letter (being promoted with a 2-year subscription for $1,495):

“Once you get to my age (62), you’ve hopefully figured out that most public companies aren’t that great. Most of them aren’t worth more than a brief trade every now and then… if that. Many should simply be avoided altogether.

“Few are truly great investments that should be bought and held for the long term. It’s even more unusual to find an entire category of such stocks.

“When a stock like that is trading at a bargain price, that’s exactly what I recommend in my Extreme Value letter.”

And he waxes rhapsodically about royalty companies for a bit, using as an example Altius Minerals (ALS.TO, ATUSF), which is one of those investments that we have in common…

“Royalty companies provide funding up front to earn a share of the revenue from an asset or product later on. Doing so allows them to reap hefty rewards in the future without having to invest any new capital. It’s like a perpetual bond.

“For example, our model portfolio holding Altius Minerals (ALS.TO) owns royalties on roughly 20% of the world’s potash supply. It doesn’t invest in mining directly, which means it’s far less risky than an actual mining company.

“Altius doesn’t need to pay a single cent for exploration, production, or expansion of the mines. It’s responsible for virtually no operations except some basic accounting and administration. Instead, it just sits back and rakes in the cash from investments others are making.”

And Ferris says that much of Extreme Value’s portfolio is made of “royalty and royalty-like” businesses, and that they just recommended one of them… here’s how he teases it:

“This month, we’re recommending the biggest private royalty holder in the world. It earns an effective 13% royalty on roughly $120 billion in global revenues in an industry that’s patronized worldwide by billions of people every day.

“You know this cash gusher well. You grew up with it. Its name and logo are ubiquitous. Yet you’ve probably never thought of it as a royalty holder. And we have rarely considered it an extreme value.

“But today, this industry-dominating powerhouse is trading at an unusual discount as Wall Street ignores three significant avenues for growth in the coming years. We urge you to add it to your royalty portfolio now before the market catches on and our window of opportunity closes.”

So who’s that? Well, the only company that really matches those clues — an effective 13% royalty on $120 billion in global revenues — is good ol’ McDonald’s (MCD).

Yes, it’ a fast food restaurant chain — the biggest such global chain, by most measures, with probably ~40% market share in the United States, the largest market, and a stronger presence in most other countries than most of the other fast food chains.

Sorry, I’m showing my age — they’re called “quick service restaurants” now.

And yes, global system revenue at McDonald’s is about $120 billion these days. That’s the amount consumers spend on buying burgers and fries at all the McDonald’s locations around the world in a given year. But what makes it a “royalty like” company is that McDonald’s Corporate is really primarily a franchisor and real estate company. They own the real estate on which most of their restaurants sit, so they collect both lease payments and a gross revenue royalty from (almost) every franchise restaurant in their network, along with a bunch of other fees that franchise operators pay (for their software and support), as well as startup cost for new locations ($45,000 franchise fee, in most cases) and the cost of buying their food and supplies (burgers, fries, cups, etc.) from the parent company. There’s also a minimum 4% advertising spend for the franchisee, and some of that goes through the corporation, but that’s not really a “royalty”. I’ve seen reports that say the average rent for McDonald’s franchise operators is close to 10% of sales, so it’s perhaps fair to say that 13% is an average overall “royalty” rate for the restaurants, though that varies widely and some of the rent is really just a pass-through of real estate costs that the corporate incurs to own the restaurant.

So that’s the Thinkolator’s answer for you: McDonald’s is, if you look at it that way, the world’s largest royalty company. About 60% of McDonald’s revenue comes from franchise restaurants, which means it’s almost entirely royalties and lease payments, and that portion which comes from the franchisees does total up to almost exactly 13% of the total systemwide sales right now, so I imagine that’s where Dan Ferris is getting his “13% royalty” number from. (The other 40% is from the relatively small number of stores that McDonald’s owns and operates itself — about 5% of locations, but 40% of revenue and probably 10-15% of operating income, since running the restaurants comes at a much higher cost than just collecting royalty fees or owning real estate.)

Is it appealing as a stock? Well, maybe. McDonald’s is one of the all-time great businesses, and there are a few things working in their favor, but the stock does not necessarily look objectively cheap right now. At $290 it’s valued at about 25X trailing earnings, with a dividend of a little over 2% and earnings that have grown, over the past five years, at only about 5-6% per year. They are profitable and have a good return on assets, and a good balance sheet, and obviously have one of the world’s most valuable brands… but to see an “extreme value” here, you probably need to look at the future, not the past.

"reveal" emails? If not,

just click here...

What’s coming up that could make McDonald’s more valuable? The catalysts that I see are their increase in the royalty rate, their rollout of the new smaller-format freestanding beverage chain, CosMcs, and, perhaps, their changes to the franchise agreement that give them more control over legacy locations (ie, not making it “automatic” that franchise owners can pass the restaurant down to their heirs… which presumably means they could take the location back and sell it again, and there is a huge cohort of baby boomer franchise owners who might turn over in the foreseeable future).

The franchise royalty rate is already going up, from the base 4% to 5%, but only for new North American partners… this seems likely to eventually filter through the whole system, perhaps along with less-publicized rent increases (they’re usually on 10-year contracts), so McDonald’s share of the total revenue pie could gradually increase a bit, maybe to ~15% from the effective 12.5-13% now.

And I have no idea how the new CosMcs concept will do, they’re rolling out their dozen or so test locations in the first half of this year and say that “specialty beverages and coffee” is “a space we believe we have the right to win”… but it is true that McDonald’s has tested lots of specialty offshoots and ideas over the years and they don’t always work. It could be a meaningful boost in a couple years, particularly since the gross margins on beverages should be better than for fast food, or it could quietly disappear.

The gradual changes to the franchise agreement and any rent or royalty increases could backfire, I suppose, since McDonald’s also wants to keep its franchisees happy, but it seems as though those franchise operators have gradually been getting squeezed by the company for decades, and they’re still mostly very profitable family businesses, so maybe they can keep squeezing without major complaints. There’s a reason why McDonald’s franchises are more expensive to open than almost any other franchise business, with the exception of some big hotels (you’ve got to have at least a few hundred thousand dollars in cash to get started, and most operators will already be at least “millionaires” to qualify, it’s not easy to get accepted by McDonald’s as a new franchise owner). This one of the most sustainable and predictable restaurant businesses, there’s a very low failure rate, and McDonald’s probably has the best portfolio of quick service restaurant real estate locations in the world, so they keep attracting people… and they can probably afford to squeeze those operators a little more.

So that’s what I see — a great business, which might have better growth in the next five years than it did in the last five years, because of those new CosMcs locations and, more importantly, the gradual increase in rents and royalties. It’s not obviously cheap right now, at about 25X earnings and 30X free cash flow, but it is true that it’s trading at a smaller premium to the market multiple than was the case for most of the past year — the S&P 500 has a trailing PE of about 23 right now, and McDonald’s is at 25, so that’s pretty close — a year ago, MCD was at 35X earnings and the S&P was at 22, so it’s now being priced more like an “average” company, and there’s at least an argument to be had that McDonald’s will have above-average performance in the future. It is, at the very least, an above-average company, with a well-managed and beloved brand and a fantastic operating model, and it’s also got very steady profitability thanks to the royalty/lease payments from the 95% of McDonald’s restaurants that are run by franchisee partners.

McDonald’s shares do get cheap sometimes, like during the COVID crash, or when there’s a sudden backlash against their food that turns investors off for a little while, but it’s fairly rare, and those are also the times, of course, when most of us would be too afraid of the world to buy shares. Six years ago, in early 2018, McDonald’s had about the same relative valuation to the S&P 500 that it carries today, both were trading at roughly 22-24X earnings… and whaddya know, the returns, to date, are also quite similar right now. You didn’t have to buy the hot AI stock or hit the lottery by buying at the absolute lows, you could have bought McDonald’s, a relatively slow-growth company, and had a market-matching return, with a bit less volatility than you would have gotten from the overall market.

Of course, a single stock will always be “riskier” than the S&P 500, you can’t entirely do away with the risk that any one company could face a surprise catastrophe or make a huge mistake… but if things get ugly and there’s some kind of AI-fueled bubble and crash in our near future, then McDonald’s will probably be a lot steadier than the hot stocks of the day. And sometimes that works out fantastically if you’re patient enough… the company seems to keep chugging along, so in the short term we are probably at risk of worrying too much about whether it’s “cheap enough” and not really consdering how nicely a steady company like this can compound. Here’s what McDonald’s looks like compared to the S&P 500 if you bought it 20 years ago, when it also traded at about the same earnings multiple as the S&P 500:

Should you buy McDonald’s today? That’s your call. Great company, global leader, and a business that’s probably going to improve under the surface as their “take” from their restaurant fleet improves a little over time, and it’s trading at probably a reasonable valuation. You could do worse, but I’d hesitate to say it’s an “extreme” value right now. As always seems to be the case, the more you pay, the more patient you have to be — but this is, at the very least, a high-quality company that has always been worth the patience in the past.

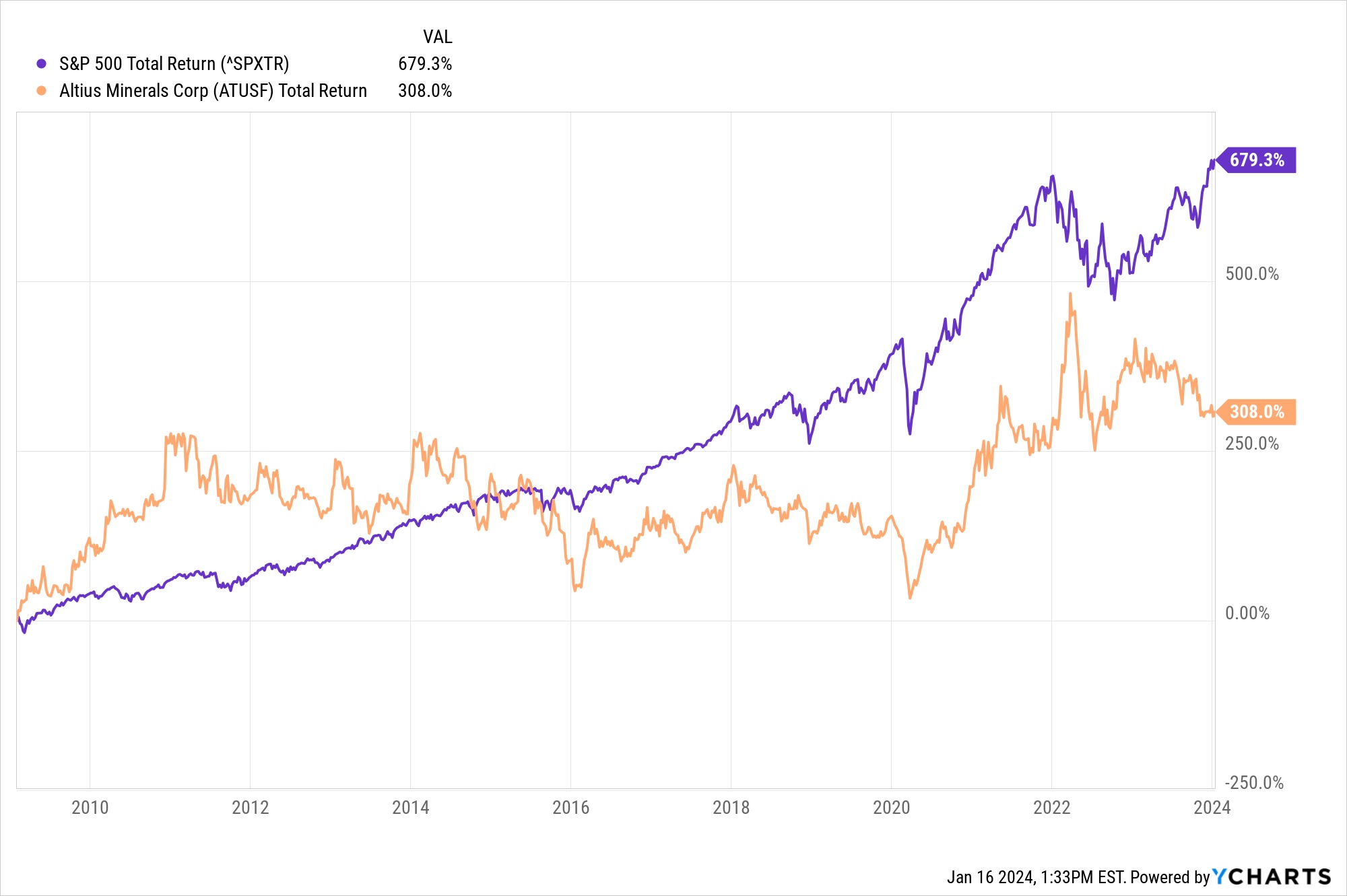

For what it’s worth, those royalty plays in the commodity space that Dan Ferris mentioned in his spiel are also my favorite way to get exposure to that space… but it’s worth noting that unless you run into a real commodity bull market, they’re not terribly likely to be strong outperformers. I think they still play a valuable role in a portfolio, but Ferris notes that his has gains of 189% on Altius Minerals, which was a recommendation he made almost 15 years ago, and 90% on his current secret “No. 1 Recommendation,” which is almost certainly Sprott (SII), a company he started recommending about six years ago. That means Sprott has probably lagged slightly behind the S&P 500 since he recommended it, and Altius has been a severe laggard. Yes, those are positive returns, and even pretty good positive returns, but even with the bear market in 2022 they have failed to keep up with the much steadier performance of a basic index fund. Sprott did spike higher several times over the years, perhaps in part because of Ferris’ teasing of the stock or because of movements in the price of gold, but as of now it’s roughly a match for the S&P 500. Which is fine, but not all that exciting for an almost six-year hold.

Altius has been significantly worse, just because that 189% return is spread out over a dramatically longer time period. I dont’ know the date when he first bought the stock, but he started using it as a teaser pitch for his newsletter in February of 2009, and this is what the return has looked like — that’s Altius in orange, the S&P 500 in purple:

That’s not to say that these are bad companies, there are reasons to like both Sprott and Altius, particularly for their royalty-like business models (Sprott is mostly a manager of commodity ETFs, so it’s a more indirect “royalty” in the form of a management fee), but these kinds of companies do not tend to be world-beaters unless their particular commodity market takes off. Altius took some big hits with the effective writedown of their excellent Alberta coal royalties when that industry was shut down several years ago, and has been hurting this year with the falling price of potash, so it will probably take a real boom in either copper or potash prices to make the stock soar again. You (and I) would have definitely been better off with a royalty on a steady operating business, like McDonald’s, than a royalty on volatile commodities.

What happens next? That’s anyone’s guess, but I’d be delighted to hear your thoughts — just use the friendly little comment box below. Think McDonald’s will continue to be one of the great royalty businesses in the world? See better performance from their competitors, or from some other kind of “gross royalty” or similar business? Expect the commodity royalties to take over as leaders? Let us know….

P.S. Gumshoe readers always want to hear how actual subscribers feel about the newsletters they pay for, so if you’ve ever tried out Ferris’ Extreme Value, please click here to visit our Reviews page and share your experience with your fellow investors. Thanks!

Disclosure: of the companies mentioned above, I own shares of Altius Minerals. And I ate a McDonald’s burger in the airport yesterday. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

How can you NOT be pulling for Detroit now? Congrats Lions fans!

travis are you from michigan if you are where from ps thanks for all your hard work

No, but my Mom is from Traverse City and I have a bunch of MI relatives. Caught the bug from a distance 🙂

So now we know how you got the name Travis!

Sometimes I like to think I was named after Alamo martyr Colonel Travis, but I think my Mom just liked the sound of it… subliminal from growing up in Traverse, I guess.

Hey, Tampa, come on up to Ford Field. We got a stomping waiting for you. GO LIONS.

Yes, three cheers for the Lions, the Ford family and Coach Campbell, who often looks like he could shred a referee! We in Houston are also ecstatic about our worst-to-first Texans. Perhaps we meet in the Super Bowl?

Hope so! Though that one I’ll be watching from home, sadly, I can swing a splurge for playoff tickets but $10K for Super Bowl tickets is a little tough to justify 🙂

Yep, as a subscriber I can confirm that Mcdonalds was what Ferrris was recommending.

Thanks James, always nice to get a confirmation.