The Motley Fool’s Market Pass service offered up a teaser pitch over the weekend about a new stock that is being recommended by Rich Greifner… here’s how the email got everyone excited:

“It’s less than 24 hours until the market opens, so I’ll get straight to the most exciting story I’ve ever shared in Investor Digest

“MICROCAP STOCK TARGETS 865X POTENTIAL”

What’s with this Market Pass service, you ask? It’s sort of a “best of” service, here’s how they describe it in the promo:

“Each year, the Market Pass team reviews all the picks in Stock Advisor and Rule Breakers…

“Picks what they believe to be the very best stocks – both individually, and as part of a team…

“Sprinkles in a few ETFs as needed…

“And designs what we consider the ‘ultimate portfolio.’

“It’s meant to be THE one-stop shop for investors looking to take advantage of what Rich and the Market Pass team believe to be the VERY BEST stocks in Stock Advisor and Rule Breakers to build a potentially market-beating portfolio.”

So mostly it’s trying to winnow out some winners from among the Fool’s most popular newsletters, and throw in some other stuff — including the “best small caps for 2021” special report that they’re pitching here, including that “865X Microcap” they hint at… and, of course, it’s a pricey offering, $999 a year with no refunds (the Fool’s “entry level” letters are often sold at $49/yr and typically offer free trials and easy refunds, but, like most publishers, they design their marketing funnel primarily to feed subscribers into much more expensive services that do not offer refunds).

What hints do we get about this latest microcap? Not much, here are the clues…

“… hasn’t been recommended anywhere else at The Motley Fool…”

“This stock’s market cap is under $250 million….

“This company made $19.5 million last year…in a fast-growing online market management believes will grow to an estimated $16.9 billion by 2025. Potential 865x growth?”

And they make some claims about the very profitable business…

“800% ROI per client. That’s right – for every dollar this company spends acquiring new clients, on average they make $8. That’s a simply massive reinvestment opportunity for the company to rapidly scale up in the coming months. (And that’s with this company already being the lowest-cost competitor in its market. If they raise prices, could that ROI grow to 1,000%+ per client?)”

So which little company are we being teased with here?

No definitive answer today, but the closest match we have from the Thinkolator is IZEA (IZEA), which is a small company that has gradually rolled up a bunch of online influencer marketing agencies and providers and software tools over the past 15 years.

How do we match? Well, IZEA had total revenue 19.4 million a year as of the third quarter of 2019, so as of the last quarterly update that would have been “last year.” That was before COVID began to really depress results (though it’s down to $17.6 million as of the most recent four quarters — and, to be fair, it had been flat-to-declining for a couple years pre-COVID), and it is an online “marketplace” model company — offering both a SaaS product in its marketing software and a marketplace in which social media influencers and brands can connect.

They have been gradually trying to improve the business by making it more of a SaaS platform and bringing on new customers, and the transition to SaaS can cause a decline in top-line revenue even if you’re not in a pandemic or recession, but their revenue is still mostly really from the “agency” business where they manage influencer campaigns directly for advertisers. Maybe this is IZEA’s time to shine, perhaps they’ve finally become a real business after a “failure to launch” decade, but that’s a qualitative assessment you’ll have to make for yourself.

Certainly investors are more enthused about the stock right now than they’ve been for a few years… and the stock has gotten some attention from other newsletter pundits (Luke Lango over at Investorplace submitted it as his top pick for 2021, for example, calling their new Shake marketplace platform a “game changer”). And, of course, it’s got a good following on Twitter, and there are certainly other folks who believe that the “influencer” marketplace will be huge, and that IZEA will be a leader in the market… all of which has helped drive the stock higher, up a few hundred percent in the last several weeks (which was met by a shelf filing to raise perhaps another $35 million by selling more shares — though that’s not necessarily imminent). The fact that the shares jumped 30% this morning is perhaps some confirmation that the Motley Fool was touting this particular name, but it could also just be other folks jumping to the same guesstimate as the Thinkolator. It doesn’t take much attention to make a small cap stock go bonkers.

"reveal" emails? If not,

just click here...

Will influencer marketing be with us forever? Kinda seems that way, regardless of how silly it seems to so many of us. And IZEA has consolidated a fair amount of that business, particularly among the “regular” consumer brands (they’re not a fashion/luxury group, think more “hiring some TikTok stars to do a dance about Campbell’s Soup”), with a good roster of clients and a solid-sounding business model (SaaS subscription fees for the platform, plus add-on service sales and a piece of all deals made in their marketplace).

My other hesitancy about calling this out as a match is that I don’t know if they are really generating an 800% ROI for their new customer acquisition, I haven’t seen that claim anywhere and it’s certainly not reflected in their financials (their “sales and marketing expense” has pretty consistently been in the range of 30-40% of revenues — meaning that each dollar of marketing spending, which presumably is largely customer acquisition, brings in about $3 in revenue, not $8 — and selling and marketing expenses have risen more than revenues every quarter for more than a year). I also have not seen a specific claim that they believe their “online market” will reach $16.9 billion by 2025, though that forecast is in the ballpark with what I’ve seen some other folks estimate for “influencer marketing” in general.

Here’s how IZEA describes their “core revenue streams”…

“Managed Services” is a project management business, they actually manage a campaign and pay the creators.

“Software licensing” is a high-margin SaaS business, licensing the use of their platforms (mostly IZEAx for self-managed programs and BrandGraph for data and reporting)

And “Marketplace fees”, which is probably self-explanatory — they host a marketplace for “influencers” and service providers (photographers, etc.), and collect 12-15% of any transaction that takes place on that platform. The latest version of this platform is called “Shake” and is available for everyone as a self-serve platform, which might finally help the business to get some scale, though listings are curated to some degree and they also have a legacy enterprise platform (IZEAx) that’s more closed, and it is indeed lower-cost than Fiverr (FVRR) in terms of marketplace transaction fees… whether it’s the “lowest cost” platform, I don’t know.

They have reported some customer wins recently, from the government (both military advertising and COVID “wear a mask” marketing) to some large consumer brands, and said that their managed service bookings, which tend to gradually hit actual revenues over 3-6 months, have surged in recent months (up 48% in the fourth quarter, helping 2020 to recover to 12% growth on the year after a terrible period during the pandemic shutdowns)… so that’s a sign of some hope for the next few quarters… but this is a wildly volatile one, the shares surged as much as 30% this morning, perhaps from that Motley Fool attention if this is indeed the stock being teased, and it’s well over $5…. pretty impressive, given that just a few months ago the company was worried about maintaining its Nasdaq compliance as the shares dipped below a dollar (and after there was a teensy bit of insider buying at 75 cents in November).

As a business, it sounds attractive in the abstract, particularly because of the large store of data they have about influencers and celebrities and social media campaigns and the possibility that they can turn that into a larger platform with their self-serve Shake business. Beyond that, well, you’ll have to make your own call — the numbers are not there yet, their SaaS revenue is less than $2 million a year as of last quarter and their managed services revenue is by far the biggest part of their business, so there’s no really obvious reason for it to trade at a “SaaS multiple” since it has none of that subscription stability, and they’re not currently growing so you have to have a little faith about growth resuming before committing to buy the shares at a “growth multiple.” Of course, everything that has a more obvious SaaS connection is already trading at 30X revenue, it seems, so perhaps you have to stretch a little to find such names in this market.

They do have a decent amount of cash, and after their shelf registration they’ll presumably be selling a bit more now that the stock is at multi-year highs, but the story is entirely about their optimism about their new products and recovery in enterprise influencer spending that could spur growth as those products gain traction or as the economy recovers — as of last quarter, they were getting some recovery in bookings but the actual financials showed decline, not growth, with marketing spending from their clients lower and their fees pressured, presumably due to competition.

While 2020 was a rough year, they did say the right things back in the summer about investing to try to lead in their sector, this is from the Q2 conference call:

“While others in our category might be struggling to survive for various reasons, we believe it’s the ideal time to focus on segment domination and scale. To that end, with the capital we’ve recently raised, we plan on deliberately increasing our cost basis and net loss over the coming quarters to promote investments in key areas around our business that we believe are long-term game changers, from hiring and launching our first ever wholly virtual professional selling program this fall to develop up and coming in-house sales talent to adopting a virtual first human capital stance across all company departments.”

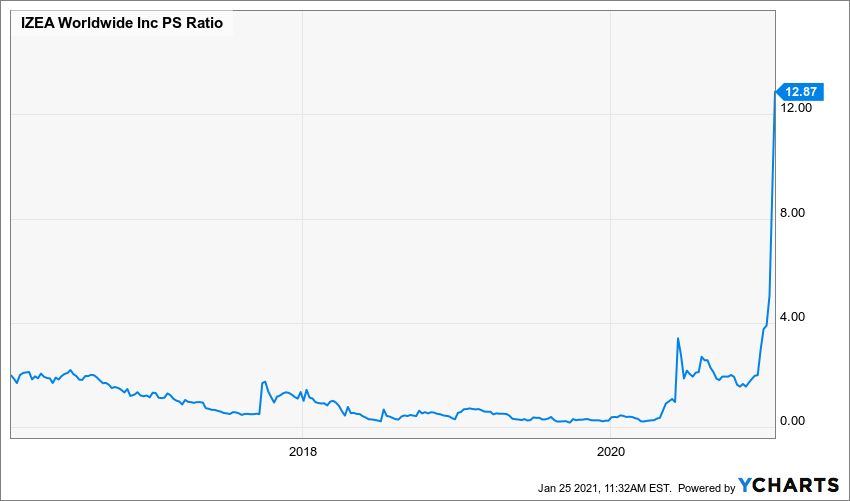

So I can see why you’d look at this one and find it interesting, but do note that the valuation is at a historic extreme — maybe it’s justified because of the improved product suite and the rollout of Shake, or just because the overall market is trading at such high multiples and people do love a SaaS/marketplace story, but the company has been around for quite some time and, as an investment, has generally been a disappointment so far (unless you bought in the past couple months), so part of your assessment, if buying shares, would have to be “ah, NOW things are finally lined up, and they’re about to get it right.” Here’s what revenue and the stock price have looked like over the past five years:

And here’s what the price/sales ratio has done over that time period, the amount investors have been willing to pay for each dollar of IZEA revenue:

So it’s certainly more popular, investors are optimistic, and the company thinks it is well positioned. Whether or not you agree, well, that will have to be your call — so read your tea leaves, dear readers, and tell us what you think the future holds for IZEA.

And, of course, feel free to chime in if you think there’s a better answer to that Motley Fool microcap tease… just use our happy little comment box below. Don’t worry, we don’t bite.

Investor news here is some of the most informative realistic I have found yet. Many recommendations here could save most investors thousands from gurus with bad investment advise. My research starts here and I have not been disappointed yet.

Agreed. Getting in with IIPR early on was worth the price of admission alone. I would not have heard about that one that soon were it not for Travis. Thank you!

YYYUUUPPP!!! VERY happy with my small IIPR stake!

this joint was at .80 not that long ago, so already 8x for some!! wow

Hi. I just read this in one of those free analyses from Motkey Fool where they try to sell you a subscription. By the way I subscribe to their basic service.

“Investing legends and Motley Fool Co-founders David and Tom Gardner just revealed what they believe are the 10 best stocks for investors to buy right now… and IZEA Worldwide, Inc. wasn’t one of them.”

What do you make of that? I’m not being contrary. I really want to know what you think.

Thanks

They publish a 10 stocks list each year, and every month in their intro newsletter they pick the 10 “Best Buy” picks for that month out of the hundreds in their model portfolio. That language at the bottom of the article will appear at the bottom of the majority of their articles as a marketing pitch.

I have the stock. It is not IZEA

They seem to do that to say that they have better picks. I have SA and RB with them and I have been pretty much ahead on most of the ones I was attracted to. But it seems like a waste of money to renew. I won’t be doing it next time my subscription is up

is IIPR a stock? or what is IIPR that you speak of.

Is a stock omega345, Right now is selling at $186.40 per share. Up to date(01/29/2021) the growth is +$170.00 (1002.30%) from $16.40 in 12/12/2016.

Sharpspring (SHSP). Thank me later.

Thank you, Professor! Ditto for me with Travis’s service. I ALWAYS check here to get an honest observation and recommendations. IIPR was a great pick. Good luck to everyone this coming week, I think it’s going to be a wild ride!

Do we KNOW that this is SHSP, or just suspect it..?

I bought the service. The stock is SHSP. It is alot like Hubspot, which is another MF favorite. It is much smaller though. Other stocks in the MF 2021 small cap report from are as follows: API, BOMN, CWH, FLGT (which already doubled my money), INSP, MGNI, NCNO, and PAR. They are winners and will provide big returns over the next few years.

Thanks Professor Code for being so generous. Really appreciate everythign you guys do

Professor. Which motley fool service are you referring? Thanks.

I think it is Market Pass

Market Pass

Thanks Professor and ddeids.

I have the stock advisor and not sure if I want to keep it after 1 year. I find each time when a recommendation comes out, price already shot up. A few times I hurry up and buy the recommendation, only to have the stocks come way down later on. Not very good luck for me.

Do you both like Market Pass?

Hi Eleanor the trick is to wait for a few days to buy. I geneally wait for a week and then slowly build up positions. I have been buying since march on SA and it has done well. Anyway these are long term plays so a few dollars here or there may not make a difference 2 years from now. Especially if they go up 10x. Beyond that even I would like to know how different is Market Pass from SAand RB; since it seems to be a mix of the two

Hi John. That makes sense. I checked on the Fool website, it doesn’t look like they offer Market Pass anymore. I suppose one can pay for both SA and Rule Breaker to get all the recommendation.

Yes I like it. I usually wait a few hours to buy after recommendation to see if price run up comes back down. If you hold the stock for a few months, it often goes up even more. You just need patience!

Much appreciated professor.

Echoing what others have said, thanks so much!

Nikondancer, can you help us with the Round 4 recommendations from Motley Fool 10x?? Thanks!!

Travis has requested that I not post these. I don’t think it was necessarily his choice but it was a directive from the MF.

Bummer, I understand though. Thank you!

Reddit seems as nice community with private messages possibility. Are you there to discuss unrelated topics?

Motley Fool seems pretty active monitoring this forum that makes me wonder if they turn up here to look at ideas and recommendations of other newsletters and use it as a screener for their future services.

On reddit I go by john_wick_finance incase we can catch up for a chat

hey nikondancer, are you on reddit/fb?

Hi nikondancer, thanks very much for your generosity so far along with propmate and some others related to this particular service. Is there any option to reach you privately at all?

Yes, I have a gmail address. User name is the same.

The surge is hard to accept, and some will calm down but others just go straight up. Overall I was a skeptic at first, join MF Stock Advisor a few years back and did nothing with it, then cancelled. But then in April 2019 I started following in earnest, roughly followed 8 out of 10 recommendations; slowly built up a portfolio well into Q3 of 2020. My 2020 calendar year return was 80%, needless to say I am very happy. I know 2020 was not typical, and be foolish to expect the same for 2021, but hoping to beat the mkt again, whatever the market might be.

The Motley Fool products have been very good to me. Their recommendations are intended to be held for at least 3 years, if not 5 years or more. In the grand scheme of things, the immediate run-off is quite insignificant. If you are concerned, don’t buy on the day when the recommendation comes out but wait a day or two. But seriously, even if you are buying at all-time-high, if the share price still goes up, it’s really not a problem in a long-hold situation. I bought TDD when it was recommended for the second or third time and by then it has gone up over 200%. Bought it, and already a multi-bagger in two years.

I have two simple rules: 1) NEVER buy on news of the recommendation, and 2) NEVER buy an IPO. As John Wick says, wait a few days or weeks … keep an eye on the charts to see what the momentum is doing, and you can usually buy at a better price. If I am really excited about a stock, I’ll often put in a 60-day limit order at the price I want to pay. If the stock runs away, so be it, but most of the time, I get it on a dip … remember why you are buying the stock … it is because YOU think it is a good investment, not because the MF, or anyone else recommended it to you. Once you buy it, there will be times, sometimes at the beginning, that you simply have to close your eyes to a slide. I had one of those no too long ago, down nearly 30%. I gutted it out, and within the next month, I was up 15%, and it hasn’t looked back … I never did find a reason for the slide. Look at CCIV this week … there was no reason for it to have gone up to $60+, and certainly, no reason for it to have fallen back to $36 in the past two days … it’s all emotional trading. It should grow to $70, probably over the course of the next 12-18 months based on the company’s proper valuation…I’m not worried.

Same with IPOs … if you look these, I’d say 90% of the time, the stock spikes in the first few days, then over the next 2-3 months it will drop like a rock, hit a “normal” trading range, and then if the company really does have legs, it will climb back up in a more usual and orderly fashion. So unless you can buy the IPO, pre-market, don’t. I’m a long-term guy, so I generally don’t get too fussed about market swings. As I’m getting older (61 now), that is changing simply because I don’t have a 10-year runway to recover from a bad slump. Now I really am starting to pay attention to charts, and I read everything I can.

I use the exact same strategy. Patience, DD and Gumshoe is key!

I’m 68 and retired. The term “long-term” is rather frightening now, and I’ve allowed the stock service to handle half and I handle the other half of my portfolio. I don’t think I’ve owned a stock for more than 1 year. MF turned me on to some very good stocks that I sold way too early like Shop and Trade Desk. The perils of being an old investor or trader.

I first subscribed to Motley Fool Stock Advisor in 2016. All the stocks which they recommended and which I bought and have held for a long time, have gone up over 100%, for example Shopify (up about 34x), Nvidia (up about 5x), Alphabet, Facebook, Match, Illumina, Twilio, Zoom, etc. In short, I trust MF SA. In my experience, they don’t recommend duds, and they’re more reliable than any other stock advisory service.

Thanks a ton for your generosity

Thank you enormously for your kindness, Professor. We all owe you one.

Wow!

Thank you Professor Cole

Is there a chance this stock is PUMB? Thank you for all the insights on the discussion thread.

Too large a company to really be called a microcap, in my book, but it certainly had a good day today. I’m assuming you mean PubMatic (PUBM) — they went public late last year and seem to be going up against The Trade Desk, among others, programmatic advertising management/software and other tech-driven ad services for publishers and advertisers. It’s a big and fast-growing business, though I don’t know much about the company at this point.

Sorry for the typo. Yes, I meant to say PUBM. Indeed the market capitalization for PUBM doesn’t meet the the definition of microcap. Do you have any idea at this point which one is better buy among PUBM, MGNI, ACUIF and CRTO? They are all in the advertising sector. Thank you in advance.

The only answer I can give is that I haven’t bought any of them, and nothing in a quick glance at their financials makes me feel compelled to chase after them at the moment..

Thank you, Travis.

MF is recommending CRTO, I own ACUIF and it has been a phenomenal investment for me, but I got into it at around $6. PUBM is interesting, but going up against TTD is tough. I also own TTD and was fortunate to have bought it at $53. I don’t know anything about MGNI. I think any company in this space will grow, so you really have to look at management and any new innovation. One thing for sure, all of these stocks are wildly volatile. TTD trades in a $150/share price window, so if you own say $200 shares, you could be down $30,000, and the next month back up that much. Two days in the past 10, the stock has made a $60 swing…one up and one down … that can be hard to stomach.

Thank you for your information. I’m a member of rule breaker and MF didn’t suggest CRTO in that service. Exactly, for good stocks like TTD and shop, we need to hold tight and don’t sold too early. I owned TTD before and sold too early.

I bought the service. The stock is SHSP. It is alot like Hubspot, which is another MF favorite. It is much smaller though. Other stocks in the MF 2021 small cap report from are as follows: API, BOMN, CWH, FLGT (which already doubled my money), INSP, MGNI, NCNO, and PAR. They are winners and will provide big returns over the next few years.

Thanks @Prefessor Code for being so generous. Appreciate it

Thank you so much for your generosity. I really appreciate it.

Thanks, Professor. Appreciate the great info.

Hello Professor. I have been reviewing this thread again and SHSP is not disclosed as being recommended or owned by MF as of May 14, 2021. So I can’t believe it is the correct pick.

Travis this is an incredible resource! Thank you. I am new to the game here overall, and wanted to ask you and everyone. Any opinions – Are TTD and SHOP too late to get in on?

Too pricey for me to buy, but sometimes with great companies it’s still worth overpaying if you have the stomach to hold for a decade.

If I did not own them, I’d think about buying a tiny stake and waiting for the next terrible month to nibble a little more, but they’re really hard to buy at this valuation so that’s a very personal call. They’d be at almost

historically uniquely rich valuations even if they fell by 50%, so it’s a tough call.

SHOP is still a current recommendation of Motley Fool. As I mentioned earlier, if it is a good company, even buying at all-time-high is not a problem because it will go up. I bought SHOP 4 months ago and it’s gone up 40% already.

I stated a couple of comments back that I had owned both and sold them way too early. If I were 20 years younger I would nibble at both and if Shopify for some reason fell 50% I would buy all that I could. The company and the young CEO are incredible.

Can confirm it is IZEA

Also take a look at Voxtur Analytics Corp (VXTR). It is already a solid business in providing analysis and automation for property appraisals, but the real opportunity is if they can connect all the dots and automate the entire real estate transaction process. It is still a penny stock, but there is a possibility for being a 50-bagger.

It looks like it was halted from November to January. Know what the story is on it? https://stockcharts.com/h-sc/ui?s=vxtr.v

Not the original poster, but trading was halted because of an acquisition. There’s a great one-hour interview of the CEO, that explains the investment case really well. For me, the bottom line is that it’s a solid business already (i.e. not just a start-up with future potential) with huge growth prospects in automating things around real estate transactions. https://www.youtube.com/watch?v=X95QB_Hf9ec&t=10s

win both ways option trades

Can anyone share the stocks part of newsletter – SPACS with 10X by Tom Gardner- sent out Feb 13th?

Todays recommendation at 2PM EST. MF SA – IDXX – Idex Laboratories

I would be interested to know if anyone has any information on BOTS (BTZI) I have several thousand shares, it’s been in the red for some time but recently it’s starting to rise and I doing very well. I don’t know if I should hold it or sell it. Anyone have any information on this, it would be much appreciated .

The american crash

Does anyone know the 10 stocks recommended today on the 4th round of the Motley Fool 10x?

Any news on Jeff Brown’s early-stage company that’s set to profit from America’s last digital leap? Supposedly small biotech, public for year or so. I haven’t made any headways on it.

Learn how to trade options and buy puts to bet on the downside of an underlying stock as a hedge, Then you don’t have to worry about trailing stops or stop lossess.

Does anyone want to share in the price of the subscription with me? I really would like to know what the 6 cryptos are that he is recommending. If a few of us got together we could get the subscription for a reasonable price. Anyone interested?

Good move on being 50% in cash now. In addition to cash, I’m allocating as a hedge a greater % of portfolio into value stocks. You can read more details in my last comment to Travis. Thanks for commenting:)