Both versions of Motley Fool Stock Advisor, the US flagship and Motley Fool Stock Advisor Canada, have been out with teaser pitches about their “A.I. Disruption Playbook” investment ideas, and readers have some questions… so let’s see what we can tell you.

First, the US version…

“5 years from now, you’ll probably wish you’d grabbed these 3 A.I. stocks.

“Here’s a little preview:

“The Sleeping Giant with the Potential to be the #1 A.I. Company in the World: This tech titan has been working on AI for over 20 years, but it seems like many investors haven’t fully realized the edge this company has when it comes to A.I. yet. We think it’s only a matter of time before this sleeping giant wakes up.

“Whispers from the E-Commerce Shadows: Behind its vast online marketplace, this company’s leaps in artificial intelligence promise unmatched logistical advancements and a voice system poised to rule our homes. Its unique, vast datasets are the secret sauce, ensuring it stays an AI frontrunner.

“The Social Butterfly with Grand AI Ambition: While connecting millions daily, this company is diving deep into AI, aiming for computer systems that outperform human perception in seeing, hearing, and language within the next decade. Current efforts personalize user feeds, but upcoming projects hint at hardware innovations from voice-commanded building to universal language translation.”

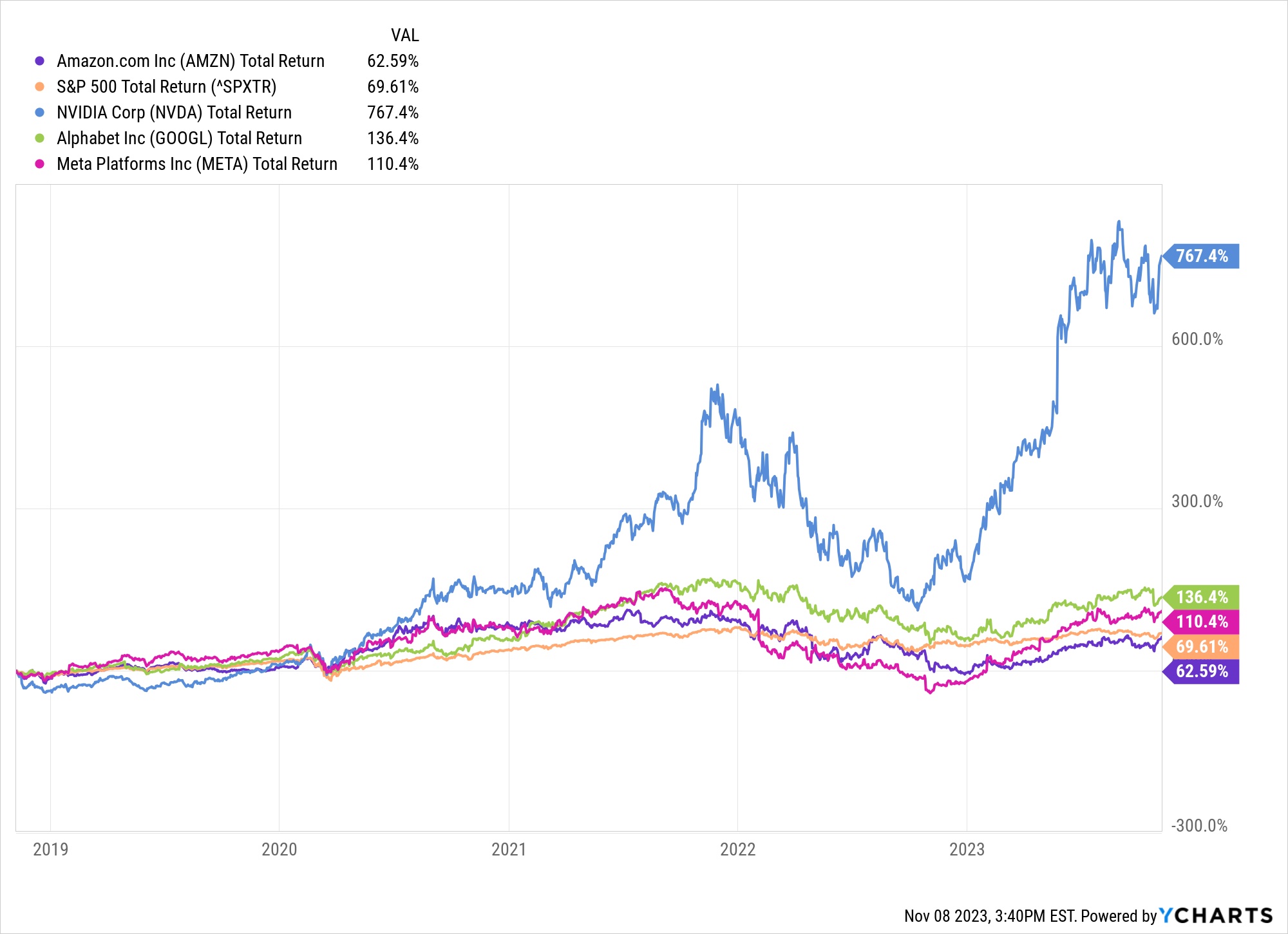

OK, so those sound a little mysterious… but there’s really no change, the Motley Fool has been pitching most of these stocks in their “A.I. Disruption Playbook” ideas for at least five years, and from the evidence we have it looks like two of the three companies teased have been the same since at least 2018, though I don’t know whether they’ve consistently updated the “A.I. Disruption Playbook” special report as time has passed or not. The three “A.I. Disruption” stocks were NVIDIA (NVDA), Alphabet (GOOG, GOOGL) and Meta Platforms (META) for years, but now they’re often “giving away” the ongoing NVIDIA recommendation (perhaps because it’s now the obvious poster child for AI, after a booming year), and the three stocks are…

“Sleeping Giant” = Alphabet (GOOGL, GOOG)

“Whispers from the E-Commerce Shadows” = Amazon (AMZN)

“The Social Butterfly” = Meta Platforms (META)

So no big shock there. Yes, all three of these are big investors in A.I. projects of various sorts, and have been implementing them as part of their core product portfolio for a long time… and in the case of GOOG and AMZN, they’re also big beneficiaries of other companies investing in AI training capacity on their cloud platforms. And credit to the Fool for picking these and sticking with them, I’m sure those have all been active recommendations in Stock Advisor for many years, since they almost never sell stocks, and it’s no secret that those tech giants have been driving the performance of the U.S. stock market for a very long time, with in some cases some meaningful whipsawing during the COVID pandemic and its aftermath. With the exception of Amazon, they’ve all beaten the S&P 500 pretty handily over the past five years (though none as dramatically as NVIDIA, of course)…

I don’t know how it works out in the end for them, but I own all of those stocks other than META, which is probably still the most undervalued of the bunch (even if it’s not as undervalued as it was a year ago) — I just don’t like the company, so I avoid them, despite the obvious power of all the personal information they can mine to train their own A.I. systems. All four of those, along with Microsoft, are among the most likely leaders of A.I. for the foreseeable future — they have vast swathes of data and huge customer/user bases to market to, they have ample capital to invest heavily in A.I. projects of all kinds in these days before there’s a real “business plan” for A.I. in many cases, and they can afford to fail a lot, be patient with A.I, and still be profitable and extremely powerful.

That’s arguably “in the price” for a lot of these stocks, at least to some degree, since they’ve been some of the biggest beneficiaries of the AI enthusiasm of the past year. NVIDIA is still at an almost unprecedented valuation for a tech hardware company (and more worrisome, the only real potential precedent is “Cisco in 2000”), but this isn’t the Court of Appeals, precedent doesn’t necessarily mean anything IF NVIDIA keeps posting shockingly excellent revenue growth and saying optimistic things about the future because of the still-surging demand for their H100 GPUs. That’s a meaningful IF, of course — they report next during Thanksgiving week, so all eyes will be on Jensen Huang as we shop for our turkey and stuffing on November 21.

The others are not growing anywhere near as fast as NVIDIA right now, but they’re much easier for me to stomach on the valuation front, even if they’re not particularly “cheap” after a year of AI-fueled multiple expansion and pretty solid operating results. Amazon and Alphabet are both still below my “max buy” levels, though well above my “preferred buy” price (I bought more Amazon in January and April, but haven’t nibbled since then… I haven’t really bought more GOOGL since mid-2022, other than a little arbitrage as I shifted from GOOG to GOOGL to boost my position by 1% or so, but it’s been one of my core positions since 2005). I wouldn’t argue with either of those — if you’re looking to own a position for 5-10 years or more, it’s hard to come up with many companies who are better positioned to handle whatever the world throws at them.

And yes, Meta (META) makes my skin crawl a little, and it has rebounded strongly from the “way too cheap” levels a year ago, but it’s still at least rationally priced — their ad revenue growth has been better than Google’s during this year’s recovery, and they’ll probably continue to be more volatile as Mark Zuckerberg shifts the company’s priorities and (I think) wastes money on stuff like the metaverse and Oculus virtual reality hardware, but I could be wrong about that… and they can afford to waste a lot of money. META is valued at about 22X forward earnings, and will probably continue to grow its earnings at an average clip of near 20% in future years, so that’s a pretty easy valuation to accept.

But what might the Motley Fool Canada be selling? Their special report has the same name, it’s still the “A.I. Disruption Handbook”… but two of their stocks are different… here’s their tease:

“The Sleeping Giant with the Potential to be the #1 A.I. Company in the World: This tech titan has been working on AI for over 20 years, but it seems like many investors haven’t fully realized the edge this company has when it comes to A.I. yet. We think it’s only a matter of time before this sleeping giant wakes up.

“The Dark Horse Putting the “Intelligence” in A.I.: Founder-led, 600x smaller than A.I. giants like Nvidia, and utilizing A.I. in a meaningful way, this dark horse is helping some of the biggest corporations in the world like Starbucks, Walmart, and Zoom enhance their workforces using cutting edge A.I.

“The ‘Microcap Moonshot’ with a Powerful A.I. Algorithm: This tiny Toronto-based microcap only went public in 2021, but it’s more than DOUBLED its revenue in that time and is highly profitable… and it’s all thanks to the powerful A.I. algorithm under the hood.”

OK, so the “Sleeping Giant” is still Alphabet (GOOGL, GOOG), we can check one of the list. A great company whether you buy it with bucks or Loonies. The others?

The “Dark Horse” stock is very likely Docebo (DCBO), which the Fool Canada teased with somewhat similar language back in late August — they are roughly 1/600th the size of NVIDIA, depending on what day you check, with a market cap now of about $1.4 billion. And they’re reporting this morning, after I finish this article, so we’ll have to see if the story changes… but this is what I said about them on August 29, the last time I looked at them:

Docebo is involved with AI but in a fairly limited way thus far, developing AI systems to help them create better learning and training programs for their corporate customers (Docebo sells a cloud-based learning management system for education and development of employees). I don’t know if they’ll be an A.I. barnburner, but they do have solid longer-term contracts for their SaaS platform, with growing revenue and good customer retention, so it’s quite possible that they’ll be able to grow into their fairly rich valuation, especially as a small company — market cap is below $2 billion, they’re valued at about 60X next year’s estimated adjusted earnings, and earnings growth could be in the 50%/yr range for a few years if they stay on trend (they really have just started to be profitable, and growth from zero often looks very fast). Still speculative, but not a ridiculous idea at a valuation of about 8X their annualized recurring revenue, the current revenue growth of 25% or so should be enough to turn that into solid results over a few years if they can keep it up and keep their customer retention numbers high. Don’t understand the sector well enough to have bought into this one myself, but perhaps worthy of more research.

"reveal" emails? If not,

just click here...

Q3 numbers will be out by the time you read this, so maybe that sounds foolish now, we’ll see. The stock price has jumped around a bit, but as of Wednesday’s close it’s right about where it was when I wrote about this stock a couple months ago.

And how about the “Microcap Moonshot?” The Thinkolator’s best answer there is Propel Holdings (PRL.TO, PRLPF OTC in the US), which is a “fintech” company that’s trying to improve the lending business, working with their AI platform and banking/lending partners to provide loans and lines of credit to consumers in the US and Canada. This can be a scary sector, as we’ve seen with other “different way of managing credit” companies in the past, like Upstart, LendingClub or SoFi, most of which have meaningfully changed their business model along the way (or failed completely), but so far Propel’s performance looks pretty exceptional.

They just reported their third quarter numbers (presentation here), and they keep adding new customers, earning a good yield from their customers and, they say, getting more selective with their credit risk exposure… so their revenue and income still look very impressive, despite the fact that they assume (and see) a very high volume of “charge-offs” (12% of loan balances) and maintain high provisions for loan losses and liabilities (more than 50% of revenue).

It would take quite a bit more research to get me comfortable with this company, I imagine, but on the surface it looks pretty impressive and very cheap — $300 million market cap, valued at about 10X earnings and only about 4X forecasted 2024 earnings, with a dividend yield of about 5% (and they’re increasing the dividend by 5% next quarter). At that very low valuation, I would assume that investors are worried about the creditworthiness of their customers, who are mostly lower income folks who live paycheck to paycheck and have been clobbered by inflation (sorry, paycheque to paycheque… this is Canada), and perhaps are concerned about any squeeze in Propel’s net interest margin — they don’t carry all the loans they facilitate on their books, but they do have some of their own debt, and the cost of that debt (13% or so) is rising.

The Canadian Fools also included Propel in their “top Canadian fintech stocks” last year, and had started to recommend it (and own it) by May.

So… I guess we’ve got a solid five “A.I. Disruption Playbook” stocks for you to chew on, not including NVIDIA… including a couple smaller stocks that haven’t gotten the A.I. “tease” treatment very often. Any of those sound appealing to you? Have other favorites you think we should consider? Let us know with a comment below.

Disclosure: Of the companies mentioned above, I own shares of and/or options on Alphabet, Amazon and NVIDIA. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Thanks for the Motley Fool teasers as always, Travis.

About Nvidia being expensive, Yahoo has:

Trailing P/E 112.50

Forward P/E 28.01

PEG Ratio (5 yr expected) 0.94

IMO, they aren’t necessarily expensive, but they are risky. I’m long NVDA, but I’m not depending on just one stock to benefit from AI. To me, NVDA is complicated, and I’d write too much if I tried to explain the risk & reward I see.

If this isn’t peak earnings, they aren’t necessarily expensive. It essentially all depends on whether this surge in demand and dramatic profit margin improvement as a result of AI investment is sustainable for a few years, or is peaking right now. And that depends on a lot of things — competitive products and whether they make a dent in market share, exactly how much they need to sell into China to sustain their revenue growth, and what Taiwan Semiconductor can build for them, and at what cost.

It can work out, which is why I’ve kept part of my position. But it could also implode very dramatically with one or two bad quarters. There has never been a large semiconductor company or tech hardware company that trades at ~40X sales for any period of time… but there maybe has never been a company as well positioned as NVIDIA for so many different technology trends over the past decade. I don’t know how anyone can have a great degree of certainty about which way this story goes over the next year — I’m sure NVIDIA will be an important and successful company a decade from now, but the current valuation means it has to become a much stronger company over time, it can’t weaken, and a lot of that is out of their control. The biggest risk is probably a pullback in orders from the big tech titans at some point, whether that’s because they have their own chips that they’re happy with or just because they over-ordered during this frenzy and they have enough to sustain their AI investments for a while… it doesn’t seem like we’re likely hitting that point now, just going by the anecdotal commentary from some of their big customers, but we might not know in advance, particularly with the monkey wrench of China sanctions flying around in the middle of the machine right now.

NVIDIA AI chips the H100 are in acute short supply and even hyper-scalers like Azure, Google are placing companies on a Q. Hardly anyone can get a cluster of any reasonable size for a day while weeks are needed for serious work.

Even AI cloud providers like Coreweave etc are placing folks on wait-list. Many countries and large cloud providers outside USA are waiting to mid 2024 for expected deliveries ( after full payment up front…) and despite the ban to China users do not expect the situation to improve much.

Usual panic FOMO bulk orders. Azure has a estimated 40K H100 order and UAE cloud providers have a 25K H100 order also pending.

NVIDIA has upped its production towards 2 Million + .The gap in demand and supply may not be visible till end 2024 if not later. There is a great deal of momentum on the Factories of Intelligence build up all across the world and alternatives like AMD, Intel really are very poor.

The margin are good. Nvidia is now providing super-

computing servers as DGX pod retailing from 2.5 Mill to 100 Mill + for those giant farms and also leasing the AI servers to some cloud providers. It also is giving priority to smaller AI specific cloud providers and taking equity shares in many start-ups.

Think it as an Apple for AI. A very different beast

I took a small bit when it skidded towards 400.

lets see

I like Palantir. I suspect the sales effort used to be the CEO trying to explain ontology to puzzled executives, but now they’re doing AI bootcamps where developers bring their own data and see meaningful results very quickly. It’s in the earnings call. Bootcamp-led growth isn’t a sure thing because my info about it is all from the company, but if the goodness isn’t massively exaggerated, I think it could work out very well. (Their stock-based-comp is another subject.)

symbol for Docebo is dcbo

Oops, thanks for catching my typo in the Quick Take.

Motley Fool tease- the rocket fuel of AI play worth 11 Amazons- any connection?

Yes, that language was used in this same ad. Likely the same “buy microcaps for AI” pitch that the Fool Canada has been sending out for a month or two, though I haven’t seen a new version recently.