Today, we take you back to 2012… The Motley Fool is promoting it’s “$2.2 Trillion War for your Living Room” stocks again, and the ad is almost identical to the version that first started circulating in the Fall of 2012.

That’s not all that shocking, of course — once a newsletter publisher finds an ad that catches the eye of potential subscribers, they have every incentive to make sure everyone with an email address sees that same ad at least a few times a week. But this one got some folks curious because it’s being released as “A MOTLEY FOOL INVESTIGATIVE REPORT — MARCH 25, 2016”

Which it sort of is, in that there are a few comments about the fact that these picks were made a couple years ago… but they continue to keep those older picks “secret” in the ad and encourage you to sign up to get your full “Golden Age of TV” research report and a subscription to Motley Fool Stock Advisor to learn more. They also indicate that those three stocks have done spectacularly well, though they use the time period from 2012 to 2014 to illustrate that success, regardless of the fact that we’ve had another 18 months since then that could have been included, had the “Investigative report” really been done on March 25.

So… since they’re going to re-mail the same ad with minor updating, we’ll do the same thing. What follows is the identical article I published on October 15, 2012 identifying the three stocks the Fool was picking… and then stick through to the end, and we’ll see what their performance has been like and check the current valuations. I’ve also left all the original comments appended in case you want to see what other readers think.

—from 10/15/2012—

The folks at the Motley Fool have pitched a lot of “big change” stock ideas over the years, from the “end of ‘Made in China'” (3D printing) to the “Death of Microsoft” (cloud computing), and these email campaigns always get a lot of attention from Gumshoe readers … both because they’re well pitched and because the big trends they describe often do, at least in broad terms, seem well-grounded in reality.

So it caught our attention when the floodgates opened over the weekend and thousands of readers (OK, dozens — but still) wrote in asking about the latest pitch from them, called “Television 2.0”.

It’s a long ad, as they always are, and it’s signed by one of the tech folks at the Fool because he tells a personal story about taking his daughter to school and having her throw the epiphany in his face that yes, teenagers don’t need traditional cable TV anymore … but it’s really an ad for Tom and Dave Gardner’s Stock Advisor newsletter, the flagship publication of the Motley Fool, and it’s about how content creators will be the winners of the “war for your living room.”

Here are a few excerpts from the ad about the big picture — which is basically just that more people are getting their video in untraditional ways and video and cable providers are losing leverage:

“Because the percentage of households with a cable or satellite subscription is now declining for the first time in the history of television.

“3 million Americans have already cut the cord, including 425,000 in the past 3 months alone.

“And according to Credit Suisse analyst Stefan Anninger, those ‘cord-cutters’ are joined by a new group … the “cord-nevers.” A full 83.1% of new households are choosing to live without pay-TV.

“No wonder Business Insider reports that the cable/satellite industry is ‘starting to collapse’…”

And this about “how we got here,” including comparisons to old monopoly businesses like the music labels, phone company, etc….

“We started paying more and more good money to get less and less good programming.

“And we put up with it for too long.

“I mean, millions of Americans dropped newspapers, long-distance telephone service, bookstores, traditional stockbrokers, record companies, travel agents, and department stores, even though they were actually quite happy with those businesses.

“It’s just that something better came along.

“But here we are still clinging to this outmoded television delivery technology that we’re all really unhappy with.

“And now that something better has come along for this too, it’s time to act.“Not just as consumers, but also as investors.”

And then he preemptively covers that concern that’s probably popping up in your head right now: In most cases, the fastest internet service you can get is from … your cable company (or another hated monopolist with bad customer service, your local phone company), and won’t they find a way to shut down those pipes if you stop paying for the content they sell through their cable box?

“… another big problem had occurred to me.

“Even if I quit cable, won’t I still be paying those same #$!&(&*$ for my internet service?

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“You can use your imagination to figure out the actual word I said.

“But it turns out that Tom has been researching this same puzzle for months. And he’s already found the solution….

“Google Fiber. And it could be just as revolutionary as Google’s search engine was when it debuted…

“Making our internet connections 100 times faster (fast enough to watch TV and record 8 other “streaming” shows in high-definition all at once, with no herky jerky download delays). And all for the same price most of us pay our cable companies for internet right now.

“In other words, it will completely break down the wall between television and the Internet. And put the cable companies out to pasture.

“CNN Money is calling Google Fiber an ‘audacious bet.’

“But Tom says it just makes sense. (And he should know…he recommended Google in Stock Advisor on July 20 when he found out about the Fiber project, and has already made a 18% gain.)”

What is Google Fiber, as we go off on this tangent? It’s Google’s effort to push for better data service by buying up unused fiber optic cable and offering up a test bundle of tv/data/phone at a set price — it’s very much a test, here’s how the ad describes it:

“… other companies … tried to build a fiber-optic information superhighway over the years (including the cable companies) [and] left a lot of unused wiring. It’s called ‘dark fiber,’ and Google is quietly buying it for pennies on the dollar.

“Meanwhile, they’re plotting their next move — now that Google Fiber reaches more than 90% of Kansas City, they’re cutting deals with ESPN, CNN, TBS, Cartoon Network, plus (you guessed it) the NFL Network. And placing help-wanted ads for national sales representatives on their company website.

“Which is leading some technology watchers to conclude that the Google Fiber experiment in Kansas City ‘is not a test’ but rather ‘a takeover plan.'”

It’s hard for me to imagine Google pouring trillions of dollars into wiring the entire country, my assumption would be that this is all part of an attempt to push other people (the telcos and cable companies, mostly) to improve connection speeds by giving them a little frightening taste of competition, but that’s just my guess. Right now it doesn’t cost Google that much because it is literally only available in a few “fiberhoods” of two cities, and those two cities are Kansas City, Missouri and Kansas City, Kansas. Still, I must admit that if they had this service available in my town I’d be tempted to jump on it — resentment of incumbent providers runs high, though unfortunately it’s pretty much in inner cities where there’s enough population density and “dark fiber” to make new startup services feasible on the cheap.

More from the ad:

“I was starting to think that Google would be my big winning investment in ‘Television 2.0.’

“But David’s research has now convinced me otherwise….

“You see, Google Fiber isn’t the biggest immediate threat to the cable companies. Because it might take a few years to complete its nationwide roll-out.

“What would really make me sweat if I was the CEO of Comcast, Time Warner, or DirecTV, is a tiny detail buried on page 555 of Steve Jobs, the best-selling official biography of the Apple CEO written by Walter Isaacson.

“(David’s been watching Apple closely for years — he pointed Stock Advisor members to the company in 2008, right when the iPhone was gathering steam. And they’ve made a fantastic 336.9% return on that investment already.)

“This is the key quotation, from Steve Jobs himself:

‘I’d like to create an integrated television set that is completely easy to use. It will have the simplest user interface you could imagine. I finally cracked it.’

…

“So while some say Apple’s announcement next month will introduce a smaller version of the iPad… the truth is, Apple needs a bigger splash than that to justify the sky-high stock price that comes with being the most valuable company in the history of the world.

“That’s why Barron’s calls the announcement ‘an event well worth watching.’

“Why Computer World thinks that Apple is preparing a ‘sneak attack’ on the TV market. And why The Atlantic says ‘Apple wants to be in your living room. And it doesn’t want to settle for being the screen in your lap while you watch TV. Apple wants to be the TV.’

“It’s also why you may need to act NOW if you want to position yourself for maximum profit in the ‘holy war’ for control of television that will be waged in 2013 and 2014.”

Which, as you read through, might make you think he’s recommending Apple again — but that’s not the case either. He lays out the competitive landscape for TV viewership:

“There’s the cable and satellite companies clawing to hold onto their trillion dollar revenue stream.

“Meanwhile, there’s Google attacking through its fiber optic wires underneath the street.

“And now Apple opening a new battlefield in the living room.

“Not to mention other industry heavyweights that already offer popular ‘Television 2.0’ services with a far greater toe-hold than Google Fiber or Apple TV.

“Like Amazon, which has more than 10 million video on-demand subscribers in its Prime service.

“Or Netflix, which has more than 27 million subscribers watching movies and TV shows through its interface.”

And then gets to his “content is king” realization:

“David and Tom sorted it all out for me with something they called ‘The Cheerios Test.’

“And sent me running to my online brokerage…NOT to buy Google, or Apple, or Amazon, or Netflix…but to buy two stocks I had never heard of before, and a third one I would have never even considered…

“You see, with the brilliant strategy they gave me, it doesn’t matter which corporate giant gains a decisive advantage in this war…or when.

“Because as long as you know how to invest in these 3 stocks, you’re in good position for any outcome.”

So what the heck is the “Cheerios Test?” Here’s what he says on that:

“I love Cheerios. (Better than Raisin Bran or Froot Loops.) I eat Cheerios. (Every morning!) But I don’t really care that much about who I buy them from or what kind of package they come in; I just care about convenience and price.

“That’s when it hit me.

“They were saying that TV was basically the same.

“What we really love are TV shows. Right?

“My daughter likes Glee. My son likes Family Guy. My wife likes Top Chef. And I like football.

“It doesn’t really matter what screen we watch them on, or what time of day…or what network, cable company, satellite dish, website, app, or gadget delivers them to us.

“Our shows are our shows!

“A recent Forbes magazine article agrees. It starts with an alarming headline: ‘The Death of Television’!

“But it goes on to explain that rather than dying, TV is about to be reborn.

“And in the world of TV 2.0, we’re in control.”

So yes, it’s about who owns TV shows and can get them to you. This has been a matter for investor debate for many years, and you’ve probably heard the “content is king” argument before, though it’s held a bit stronger for video content than it has for newspapers, magazines and songs so far.

They give a rundown of some of the major content showdowns between content owners and distributors in recent years, many of which have led to better payouts for content owners:

- “Like the AMC channel (home of Breaking Bad and Mad Men) staring down the Dish satellite network.

- Fox playing chicken with Cablevision and almost blacking out a 2010 World Series game.

- Viacom (which makes The Daily Show, Jersey Shore, and Spongebob Squarepants) strong-arming DirecTV.

- The Starz movie network pulling out of Netflix.

- And the Madison Square Garden channel taking its New York Knicks games away from Time Warner cable during the height of “Linsanity” this spring.”

And there are plenty of other examples — this is a flip from where things where 10 or 20 years ago, when upstarts like ESPN or Fox News were paying cable companies or providing free or very cheap content just to get distribution. Now that content is often what drives cable and satellite subscribers to renew, so the fees content providers are charging are climbing dramatically, and cable companies are chafing… but the loss of the cable monopoly is hurting them, since so much of this content can also be accessed online and the providers of genuine hits have leverage both to get better deals for those hit shows and networks, and to force more “bundling” of their weaker offerings that are trying to gain traction.

So that’s a long bit of chatter to get through as we finally start to get some hints about which companies they’re picking:

“Why you need these 3 stocks NOW

“We’ve seen that on-demand direct distribution to the customer changes everything.

“Just like it did for online airplane and hotel bookings with Priceline.com, and online purchases of books (and just about anything else) on Amazon.com….

“Which gives content providers the upper hand — regardless of whether they’re going through traditional carriers like Cablevision or Time Warner, or new challengers like Google, Apple, and Netflix….

“Tom and David think these three winners are about to go on the kind of epic run we only see once every 10 years or so.

“And it’s hard to disagree. Because as you’ve seen in this report so far, the next revolution in television has only just begun.

“Once more people find out about Google Fiber and the new Apple TV set over the coming days and weeks…the war for the living room will be what everyone’s talking about.

“And that means even the Wall Street skeptics will finally come around…

“Which gives you a short buying window. Fortunately, there’s still time to join those Stock Advisor members and cash in — but you may need to act NOW.

“I wish I could tell you the name and ticker symbol of these 3 uniquely positioned stocks. And if it were up to me I’d probably just spill the beans.

“But my friends in the Motley Fool customer service department tell me I can’t, out of respect to the members who are already paying for our Stock Advisor service.”

Which is where your friendly neighborhood Stock Gumshoe jumps in, of course — I can’t give you their full report on these stocks or tell you exactly what advice they might be giving, but I can at least sniff through their clues and tell you the stocks and the tickers and give a little basic info so you can go forth and researchify on your own.

So let’s get to it, shall we? First!

“Company A is an $89 billion powerhouse that owns more than 100 global television networks, plus 7 movie studios, 4 video game companies, and hundreds of websites. Not to mention a little-known research laboratory that’s developing the next generation of TV technology. (Like a new system that lets you use any object in your house — including your couch, your coffee table, even a glass of water — as a remote control). In fact, this company’s growth potential is so strong that legendary hedge fund investor George Soros just snapped up a million shares.”

Well, probably no surprise to you there but this one is clearly Disney (DIS) — and yes, you probably also know that it’s an entertainment and content powerhouse as well as a travel and technology company, owning huge content-spewing brands like ABC and ESPN as well as the eponymous studios and cable networks and relatively recent acquisitions Marvel and Pixar, among many others. They’ve gotten so big now that it’s hard to pick just one “crown jewel” from their assets, but ESPN has probably been the single most powerful content provider in the cable/content wars, with what seems like almost unlimited power to raise per-subscriber fees — after all, ESPN gets both huge live viewership (sports is watched live, mostly) and a strong “young guys” demographic that brings in huge advertising dollars from the film studios and beer and car companies (among others).

And yes, it’s hard to argue with an investment in Disney — it’s got a fortress balance sheet, it’s a blue chip company that’s incredibly profitable, it has become a dividend growth company over the past decade, and it’s reasonably priced even after the stock has gone up about 50% in the past year. I guess the only real argument against building a position in Disney at times like these is that it’s also a tourism driven and hit-driven company, so there have tended to be opportunities to buy the stock cheaper in years when theme park visitors are down, or when they have a big flop year with their movies — though it can be hard to nimbly watch and take advantage of those things. The John Carter film was a huge flop for Disney relative to expectations over the winter, but even the announcement that they would book a $200 million loss on the film in the Spring failed to keep the stock down for very long, largely because that news came right around the time they announced that mega-hit The Avengers made over $200 million in ticket sales on its opening weekend.

I’m sure no one will get fired for recommending Disney, but this is one that, were I to buy it as a long-term hold, I’d probably nibble now but try to scale into it over a couple years and hope for a couple bad tourist seasons or a lousy Christmas movie slate to bring dips in the stock. I did own Marvel Entertainment years ago, which was a hugely successful recommendation of David Gardner’s back when they were on the verge of bankruptcy and the first Spider Man movie had yet to be released (and years before Iron Man and The Avengers made the Marvel stable of characters look like such a no-brainer goldmine), but I don’t think I’ve ever owned Disney.

Still, if you feel like there will be a full-fledged “war for your living room” with several companies vying to provide live TV, it’s hard to picture a company having more leverage in this than Disney, since they bring with them ESPN, ABC and their own Disney Studios content, and there isn’t a single cable provider in the country that could sell their service effectively if they cut ESPN. That leverage might not impact a $90 billion company that much on an earnings per share basis, particularly as this “war for your living room” will likely be waged over many years and through many test locations, but it’s still leverage.

Oh, and yes, they do have a research division that came up with a crazy cool technology that could turn your houseplant (or other stuff, I guess) into a remote control — there’s a story on that here if you’re curious. It’s not going to be financially significant in the next few years, I would bet, but it is cool.

Next?

“Company B rose from the ashes of a declining newspaper empire. Now it’s cultivating a niche TV audience that’s especially attractive to advertisers. Allowing this company to generate more than $2 billion in revenue from just 1.7 million viewers…At $1,290 ‘revenue per viewer,’ that makes its programming 76% more profitable than the average television network.

“According to Investor’s Business Daily, even though the entertainment industry is extremely lucrative, it actually has ‘a puny number of high quality stocks.’ And those are two of them.”

This one is a company I don’t know well at all, other than being quite familiar with the fact that they’re responsible for the celebrification of the interior design, real estate brokerage, and cooking industries — this is Scripps Networks Interactive (SNI), which owns the Food Network, HGTV, the Travel Channel, etc. Scripps did indeed start as a newspaper company, and was one of the dominant newspaper publishers in the world for the second half of the 20th Century (you know, back when newspapers made money), as well as a major local media company through a network of local TV stations and cable companies, but about 20 years ago they started spitting some of that prodigious newspaper cash flow into content creation, building and buying those now-well-known niche cable brands, starting with HGTV. Four years ago they split the company, so the original E.W. Scripps (SSP) still owns the 20 or so TV stations (mostly ABC affiliates, coincidentally) and 13 mid-market newspapers around the country and is a stagnant, barely profitable $600 million company, and Scripps Networks Interactive owns the five cable channels and is a rapidly growing, highly profitable $10 billion entertainment force. Or farce, if you’re feeling cynical about our desperate desire to watch other people saute onions and declutter their mud rooms.

You can certainly argue that Food Network and HGTV are strong enough, with loyal enough viewers, that they should command premium and growing fees from cable and satellite providers — if you’d asked me, I would have thought that this celebrity chef fascination was a flash in the pan when Emeril Lagasse was the standard-bearer five years ago, but even though he has moved on there are still dozens of stars being made like Guy Fieri and Paula Deen (who are, in turn, turning themselves into chain restaurant brands). So I’m the last person to suggest that I can tell where this trend goes, but these cable networks seem to have a pretty good thing going — they have low-cost content, they build celebrities who must, I presume, work cheap as they build their personal brands, and when those fizzle or the stars demand more (a la Emeril, I suspect), they move on and build the next star. It looks like it’s working pretty well — they did quickly end disputes with AT&T and Cablevision when they were briefly shut out of those networks for a few days during contract renewal talks a year or two ago, and I presume that it was pressure from subscribers that led to those resolutions, so this does seem to be a content provider that has a fair amount of leverage over the distributors — and, of course, a solid web presence.

I’ve never looked closely at SNI, but I did skim through the last quarterly report and note that while they are growing revenue pretty nicely, they’re expecting to grow expenses more quickly this year — I don’t know if that’s a sustained trend, but it’s an indication that their programming costs might rise faster than their advertising revenue and subscriber fees, which obviously would be a huge weight for the business to carry since they’re already carrying a premium valuation (about 20X trailing earnings). That could well be a temporary thing, I don’t know, but it’s something to keep an eye on — we’re certainly moving into an era of more distributed programming, with more online video … but my impression is that advertisers still tend to pay substantially more for targeted, timely mass attention through hit shows than they do for online advertisements, so that transition is closely watched by both advertisers and content owners. There’s also a competitive aspect to this space, since HGTV and Food Network have to maintain their brand positioning against plenty of other niche cable channels as well as against upstart online brands in their space, but they are clearly a leader in that competition now so they do have at least some advantage.

Next?

“Company C didn’t make IBD’s list…because it isn’t really an entertainment company. In fact, even though it operates some of the most popular channels on TV (reaching more than 1.5 billion viewers in 180 countries), its business model is completely different. Its most important customers are actually elementary and high schools. And now it’s entering another $25 billion education market with a breakthrough product that’s half of the price of the traditional choice. So you can see why this company has been able to grow its quarterly earnings per share by a fantastic 22.5% in the past year.”

Well, I don’t know if I agree with that summary of the company — but we fed it through the Thinkolator and this is pretty clearly Discovery Communications (DISCA and others, more on that in a moment), the other big cable network company that gets a fair amount of investor attention. Like SNI, they enjoy the benefits of all of the original “reality” shows — low production costs and niche marketability. They call themselves “The World’s #1 Nonfiction Media Company” and produce a bewildering array of programming for their popular channels, including Animal Planet, Discovery Channel, TLC, The Oprah Network, etc. And they are taking advantage of international distribution in a big way, partly because their documentary, reality and educational content is very easy and inexpensive (compared to fiction, at least) to translate to different languages and cultures.

But I don’t know that I agree that schools are its most important customers — or that their “breakthrough” will really turn out to be such in the “another $25 billion market.” They do have a strong educational offering, with streaming content that’s available in about half the schools in this country (replacing the beloved filmstrips of my youth on those days when the teacher has a migraine, he says cynically), and they are moving into “interactive textbooks” in an attempt to help shake up the $25 billion textbook industry, but when it comes to financial performance it’s all about subscriber fees for their networks from cable companies, and advertising revenue. In the US, they’re close to 50/50 ads and subscriber fees, and internationally subscriber fees are a stronger revenue generator at the moment — “education” is a rounding error when it comes to revenues and earnings at Discovery, though it’s certainly possible that they use that division to drive earnings or cover expenses in some other way. Their textbook initiative, called “techbook,” is yet another way for them to leverage their content into the education sphere — using the educational content they already produce to build interactive textbooks for schools, but I wouldn’t put too much weight on that. Education is a small part of Discovery’s income statement, and it’s not as though folks like McGraw-Hill or Pearson, dominant textbook publishers, have failed to notice that there are opportunities in technology-enhanced publishing for students… it may end up working well for Discovery, but I can’t see it being a major part of the business in the next five years, my guess is that in 2018 we’ll still care more about Bigfoot, River Monsters and custom choppers than we do about Discovery’s “techbook” business.

Discovery is also one of those multiple-class stocks — DISCA is the A shares, which get one vote per share, DISCB, B shares, gets 10 votes per share, and DISCK, C shares, gets no voting power. DISCK trades at a bit of a discount since it doesn’t get the voting power, which might be interesting for small investors who understand that they don’t get any corporate voting power anyway, though you can imagine a proxy fight or activist investor situation when voting shares should trade at a substantial premium, too, so those things are always a tough call — and really, though I hold shares in companies that have “lower class” non-voting or fewer-votes shares (like Berkshire Hathaway and Google), I don’t like to encourage that activity. The B shares are very illiquid, but currently priced about the same as the A shares.

Discovery is extremely profitable and growing nicely — their growth in the last quarter was not as strong as SNI’s, but they’re more than twice as big and have profit margins that are a bit stronger, and they are really the leaders when it comes to leveraging content internationally and across platforms, which helps to significantly increase profitability when they get their content right. I have more confidence in Discovery than I do in Scripps, though that may just be because they have a broader array of channels and hits and niches they can play to beyond Scripps’ core niches of travel, cooking, and home improvement… or it could just be a reflexive response to the fact that Vanilla Ice hosts a real estate show for Scripps on their DIY network, and I have a hard time believing in a world where that’s possible.

This is clearly an interesting time of transition for television and video entertainment — I don’t know if we’ll end up “giving up” on cable TV en masse in a surprisingly fast transition as happened with CD players and is happening a bit more slowly with printed newspapers, but there is a move to more online and streaming content and there are plenty of companies who are working to further that transition with hardware, software, and streaming libraries, including Netflix and Google and Apple and Amazon and hundreds of smaller players, but it’s also quite possible that the transition will be a lot slower, and there’s still a lot of power in the hands of the TV networks and the cable and satellite distributors … even if it’s not as much power as they had ten years ago. There are, for example, plenty of places to watch shows online — and even lots of increased investment in professionally produced “channels” online through Amazon, Google, Netflix and the like, all of whom are funding content development as well as trying to expand their distribution businesses … but traditional TV still has a very strong position with the people who care the most: advertisers. Online video ads are a very fast-growing market, but reports I’ve seen indicate that they’re only about 5% of the size of the traditional television ad market, and the strength of television has always been it’s power to create a mass market and homogenize society, urging essentially every single American, over the space of two or three days, to see the same movie or visit the same store at the mall that coming weekend.

It’ll be an interesting thing to watch, seeing if the increasing niche-ification of media and the distributed content continues to erode that mass market, but I have my doubts that it will happen all that quickly — car dealers and movie producers really want to be able to reach everyone, all at once, and they’ll pay a premium for it … with some exceptions it strikes me that it’s been the advertisers, not the viewers, who are willing to consistently pay for hit content.

But that’s just my squishy impression of the speed of the big picture transition, and it probably doesn’t mean anything. What we get from this teaser are three strong content-dominated companies, each of whom is very profitable and trading at a premium to the market, and each of which has shown enough growth and stability to (arguably, depending on what you think the future holds) deserve such a premium. Think Scripps Networks, Discovery Communications or Disney are right for your portfolio, or the best play on the revolution in video delivery? Let us know with a comment below.

—–and back to 2016—–

Well, the story today is pretty similar to 2012 in some ways, at least as long as you’re using a broad brush to paint the disputes between content owners and content distributors… though Facebook, Google’s YouTube and others have dramatically increased the power and profitability of video advertising on the internet in the last few years.

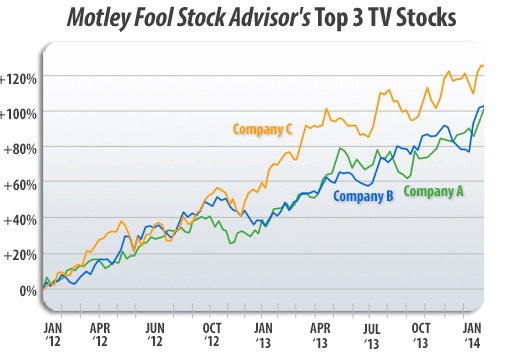

The latest version of this ad includes a chart of the performance of those three stocks from 2012 until the last time they probably really updated the ad, in early 2014. Here’s a screen grab of that:

And here’s my version of the same chart, all I really did was add in the S&P 500 as a comparison (that’s the green line on the bottom) — this is a ‘total return’ chart, so it includes dividends:

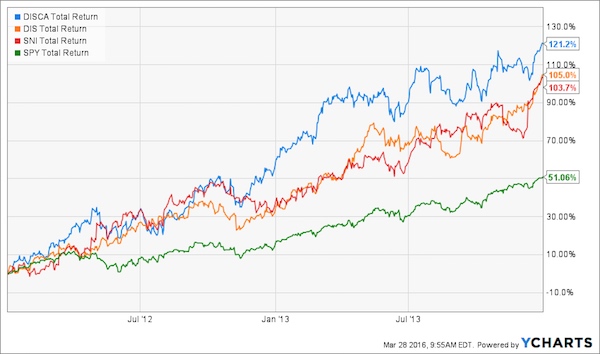

You can see that the ad isn’t lying about that 2012-2014 performance — all the picks did essentially twice as well as the market. But why are they re-promoting this idea now, more than two years after the end of the chart? Are the stocks still outperforming the market, or are they appealing bargains now? Here’s what the chart looks like if you bring it up to the present:

The S&P 500 is still that green line, now with a total return since 2012 of about 74%… but now that’s a lot better than the total return of Scripps Interactive and Discovery Communications, each of which lost roughly half its value over the last two years. Disney is the only one that has continued to beat the market, despite the fact that it’s by far the largest of the bunch (and despite the fact that it took two serious tumbles over the past year).

I never ended up owning Discovery or Scripps, but I do own Disney now — I bought when it collapsed this year, a dip in the shares that I felt like I had been waiting years to see. What do the valuations look like for these stocks now?

Discovery (DISCA/DISCB/DISCK) is expected to grow earnings at about a 10% rate over the next few years, and is trading at 18X trailing earnings. The stock has collapsed because growth dramatically disappointed over the past few years — you’ll note that the old clue above was that “you can see why this company has been able to grow its quarterly earnings per share by a fantastic 22.5% in the past year”… in the new version they did update the clues a little bit, and Discovery is hinted at with the sentence “So you can see why this company has been able to grow its earnings per share by an annualized 5.2% during the past five years.”

Growing earnings per share at 5% over the past five years is not impressive. Not for a stock that has always been talked about as a “growth” stock, paid its CEO $150 million a year or so ago, and had an average PE ratio in the low-20s for much of that time. To make matters worse, for most of 2013 the stock traded at 40X earnings. A lot of that investor disappointment has come because costs have risen for the content developer, for some of the same reasons that folks have worried about Disney (like the sports rights fees issues — Discovery bought EuroSport a while back and spent heavily on getting the Olympics rights in Europe), and because they depend very heavily on overseas growth and the strong US$ has really weakened those international results. They still have a lot of hits in the “unscripted” TV arena that they helped to popularize, and their partnership with Oprah appears to maybe not be as much of a disaster as it looked like a few years ago, so who knows, maybe they will return to growth, especially if the dollar weakens a bit against other major currencies.

Scripps Network Interactive (SNI), the owner of HGTV and Food Network, is much cheaper than Discovery these days and trades at what appears to be a more reasonable forward PE of 12… though the stock has been in the doldrums because earnings aren’t really growing. Earnings per share are expected to grow only 2% this year and slightly more in 2017, but analyst somehow expect them to reignite to average 10% earnings growth out into the future after that. I don’t understand why, and I’m always suspicious when big earnings growth numbers are based on huge numbers three or four years out instead of growth in the current year (just because the current year growth might be forecastable within some degree of error, but the other stuff is extremely unlikely to be accurate)… so it’s not too expensive to consider, but neither do I find it terribly appealing. But then again, I don’t like the Food Network or HGTV or understand the obsession with watching cooking competitions (though presumably it’s a problem for Scripps that the biggest cooking star around, Gordon Ramsay, doesn’t work for the Food Network). This still seems a thin bet for me on a few channels that I don’t think are likely to be as valuable or as high-growing as the analysts expect — but they do know a lot more than me, that’s just my opinion.

Interestingly, the old “moribund” parent, EW Scripps (SSP), has done much better than the spun-out Scripps Networks since 2012 — the old newspaper and TV station owner has doubled, while SNI is only up about 50%.

And Disney (DIS), which I do own now, is in a different league — it’s ten times larger than either Scripps or Discovery (yes, the clues above said “$89 billion powerhouse” in 2012 and that’s been updated to “$194 billion powerhouse”) and obviously has huge businesses outside of television content. And though I didn’t own it back in 2012, and thought it might be worth scaling into over time, it took me a long time — I bought into the stock last year because the stock got too cheap in the panic over ESPN’s possible problems from the “cord cutter” generation, and it’s still a pretty small personal position. ESPN is by far the most valuable cable television franchise, with dramatically higher fees than any other network and a huge advertising business, and it’s more than 40% of Disney’s earnings, so their future is obviously a big deal for Disney. I personally think the impact of cord cutting is overstated, partly because the trend is gradual and partly because I think ESPN is far likelier to be viable as either a standalone “over the top” channel sold without a cable subscription than most cable channels…. or a core part of new “skinny bundles” that are being talked about as a compromise for folks who want to get rid of $100 cable bills.

But I do acknowledge that DIS may face headwinds at ESPN, partly because of astronomical content costs (buying sports rights), and I don’t count on ESPN being the primary driver for Disney earnings in the future — I just think the market is failing to appreciate the fact that Disney is the world’s best marketer and brand expander, and it so happens that Star Wars and Pixar and Marvel and Frozen and now Zootopia are continuing to bolster the argument that Disney has again institutionalized, after a weak period a decade or so ago, their ability to create hugely valuable content that continually generates blockbuster results. Disney is huge and pretty expensive at about 16X next year’s earnings and will also probably grow earnings in the 10% neighborhood, analysts say, but it’s also, I think, the one real “blue chip” in entertainment, and the one that can work those brands across different businesses better than others (theme parks, cruises, movies, TV shows, merchandise, etc.).

You can see my bias there, of course — I own Disney and like it, and I’m a bit more skeptical of the growth of the other two… but Discovery and Scripps are certainly smaller and less tightly scrutinized than Disney, so there’s a better chance that some “hidden” value could emerge from those smaller shares that, unlike Disney, are still small enough that a big new hit show, or at least a new hit network, would have a meaningful impact on their shares.

That’s all for our trip down memory lane to 2012, and our current look at the same stocks that the Motley Fool continues to tease for potential Stock Advisor subscribers… have a thought about cord cutting, or these kinds of content companies? Other winners or losers in the shifting sands of entertainment? Let us know with a comment below.

Disclosure: I own shares of Google, Apple, Facebook and Disney among the companies featured above, and call options on DIS. I do not own stock in the other firms mentioned, and will not trade in any stock covered for at least three days.

I have an educational question on the Symbol for Discovery Communications , “DISCA”. What is the meaning of ‘A’ at the end for Nasdaq four letter symbol? I know that if it is ‘D’ or ‘C’, don’t touch it because the stock is in some kind of trouble.

Oh! I just checked on Yahoo it is not DISCA’, it is now ‘K’. So that’s going to be my second question.

Would appreciate answers from anybody…………

DISCA, DISCB and DISCK are all just different share classes with different voting power. I think I included details above somewhere.

NanoTech Entertainment is into IPTV and 4k streaming into a 4D Seiki TV. interesting new company, ntek. IPTV seems to be growing stronger with younger generation

Thank you so much for cutting through all that BS!!

by 10 min in i was screaming GET TO THE POINT ALREADY!! And eventually just gave up and closed the link!

You can cut this time greatly by skimming through the article and

reading primarily just our Gumshoe’s summaries.

What makes more sense about the pump up is the bet with Aereo and it’s ability to win the streaming rights (which they just ended up losing in the Supreme Court Ruling) Had Aereo won this ruling imagine who the losers would have been? To me the pump was about building investors, only to swipe their cash on the quick dip had Aereo won the spot that could have changed it all!

Yeah, but do you like GMO’s in your cheerios?

Soros also owns a to of Monsanto!

Thank you so much for writing this article in the way that you did. I got about 8 minutes into the spiel and couldn’t take it anymore.

Why hijack my screen and time when I have this crazy ability to read and just get to the dang point already?!

Seriously, what’s in it for you to force us to listen to the whole thing?

Last I checked “Ain’t nobody got time fer dat!” and it’s just dang annoying.

This article here did a wonderful job by stating the script as well as interpretation and allowed us to read and digest at our own speed.

TV viewing hours are declining, but the transition to fully interactive TV will take at least a decade. So I don’t know if the 3 content companies will take off like a rocket. The prize in this space remains an integrated, broadband, interactive, user-initiated delivery network, and Google will have the technology when a provider springs up. So I would buy Google.

The variety of web-connected tablets and smartphones continues to grow, as well as the range of mutually incompatible standards available for viewing streaming media. For content providers, this means that they have to serve more platforms than ever before.

You suggest Google, but are there other companies addressing/solving this problem?

Litterally laughing out loud.

Just a hint of advice: before asking a dumb question, and getting these kind of Dum Dum answers, MAYBE YOU SHOULD READ THE ARTICLE ABOUT THE QUESTION YOU ARE ASKING.

I feel for your soul if you’re trying to invest…

This reply meant for the comment below, honest mistake. Sorry!

So you make mistakes, too? Who would have guessed? Perhaps you should not comment on the “dumb” questions of others. It never hurts to be polite, even online with strangers.

Do you know what the 3 content companies are ?

Did you read the article?

I despair for the future.

Moron.

Calm down, Rambo. Bill Legate covered the reply nicely.

I know what happened. You saw the video on Motley Fool then tried looking up the article to find out the 3 companies. You found this and thought it was just a reprint verbatim of the video. It is not. Someone actually comments on it and gives you all the answers you need. It;s actually very interesting.

you are correct sir!

I don’t know if I would invest in these three content providers, or whether I would drop money on companies like Comcast. ( CMCSA & CMCSK ) Comcast has a good track record of a continually rising pps, as well as a majority share of a television network, and movie catalog with NBC and Universal.

Good point — and if you prefer oddities, there’s always John Malone’s Liberty Media –cable systems, content, and a baseball team.

Sure, buy Comcast if you have no problem aligning yourself with pure evil. I, myself, would never buy stock in companies that seem to be ethically challenged – like Comcast or Wal-Mart – even if it means missing out. Humanity trumps money for me everytime.

Good for you, we need about 300 million more people in this country to get on board with the belief that people matter more than money and that preserving and building community is an American value that deserves a front row seat in the national cultural, social and economic dialogue – even though it can hardly be measured in terms of “economic” value.

SOMETHING TO THINK ABOUT… COMCAST MAYBE LOOKED AS A MONOPOLY WITH ALL IT’S MERGING AND TAKING OVER THE CABLE COMPANY PIE ! TIME WERNER MERGING WITH COMCAST AND TAKING CONTROL OF THAT MARKET.

There’s another reason people are dumping cable. Because you can download the movie/show/game or quite literally whatever and play it through your DVD from a USB stick. As soon as someone produces a creature that can stream content while seamlessly downloading 8 other shows I choose, I will be having one. I’ll even start paying for content again. And I bet half the planet will get one too . So the company that makes this creature is the one I want a piece of.

Isnt the Tivo Roamio basically just that! it was just announced! And it does like the xbox one and combines all your apps into one channel guide! And you can stream to any device you have also…. My sister got in with Tivo when they had the lifetime memberships! That is looking like an amazing center piece for any theater room!

I always find this content argument difficult to swallow. I admit that this is totally based on my own experience. If there is anything that I find less than boring on a regular channel, I may well watch it. There’s usually something that falls in that category every day. If however I’m offered a DVD or a download then I’ll only buy it if it’s something I find really, really interesting/amusing. This means I buy “content” about once a month at the most. Perhaps less. And even then it might be some time before I actually get around to watching it. After all, I can watch it when I want to. From an advertisers point of view isn’t it better to have the audience that’s held captive by the limitations of time/availability? Someone who may not see your message for months isn’t interesting. Or am I atypical?

You’re not atypical, you’ve just been brainwashed into thinking that you don’t pay for your content. What you’re essentially saying is that at least some (most?) of the content you consume on a daily basis is not “something you find really, really interesting/amusing”. Why would you pay the cable company (way too much money) to watch something that is merely “less than boring” to you? How has the cable company managed to lower your expectations to the point that you’re willing to plop yourself down in front of a TV and watch something that you don’t really like? And to make it worse, not only are you paying to watch something that you don’t really care for, but you’re also being forced to watch the advertisements that come along for the ride. It’s a dying business model that no longer makes sense and change is coming…

Also, you assume just because you don’t directly pay for content

that you aren’t “buying” it. This is a falsehood, the cable companies,

Netflix and other providers are paying for it on your behalf and when

you pay them, you indirectly buy the content….only you aren’t the

one choosing what content gets purchased. Therefore, the content

providers are the ultimate winners if they provide a product that

sells.

I think the funny thing is, he never said “buying”, he said ” content “. I’m pretty sure he knows he’s paying for cable content, but as far as the new trend of only buying content you really want to watch, he doesn’t do that very often. He was asking is that atypical or the norm these days. I don’t know if its the norm, but I don’t pay for cable or satellite, I will however buy a season of a show I like off of Amazon and watch it when I have time. You can watch current season shows the same way. You just have to wait about 6 hours for it to hit your library, but at least you’re paying for EXACTLY what you want and its ad free.

everyone here keeps talking bout paying for your shows and t.v. I downloaded a v20 downloader and then go to onllinemoviespro.com and download the shows i want or movies. I even you tribler. so how come you guys are paying for your tv. just been reading alll this stuff because i still haven’t figured out the three stocks in that stupid video and i’m curious does any of this stuff concern me no my job is childcare i don’t care about stocks just that i hate watching some stupid internet movie that motley ‘FOOL” made literally to make you sit there for ever as he keeps babbeling and not making sense or leading to a point. until he started talking at the end about ordering something. kind felt like i sat here waisting my time when i could have been on youtube downloading stuff onto my compter. thanks piracy rules

Google and some of the other companies mentioned in your excellent report are good; however, if you want more bang for your buck , and a company that could double , check out GILT

GILT is involved with Radio and Television Broadcasting and Communications equipment……WATCH THIS ONE!

I feel that since Gilt is an Israeli company and things are currently so difficult vis a vis Israel and the Palestinians and that all sorts of conflicts have been developing in the middle east that investments there can be seriously affected by local happenings. As a result I tend to presently avoid the middle eastern countries.

You are dead wrong. The best minds i the world for computer software technology are in Israel. Go visit the county. It is fantastic and you feel very safe there. Th smartest people in the world are there in medicine, engineering and computer are there. Their defense technology is better that the US.

“.. and you feel very safe there ..”

Unless you are Palestinian.

” .. Their defense technology is better that the US .. ”

who they stole much of it from.

They didn’t need to steal our technology, as we gave it to them in the interests of national security.

Israel and US are partners in everything. There is no difference in buying stock in a company from either country. Likely bad Karma either way

Israelis are famous for improving our best weapons. Who else has the wherewithal to put a rear-view mirror in a fighter jet? Think about it.

I wonder if Motley Fool is still holding Netflix? What does anybody else think about their short/long-term prospects?

Travis, have you held GOOG and AAPL for years? I see from the stockcharts weekly chart that Google has had several stomach-wrenching dives in this time. I don’t think that you could call them dips. I am not anti-Google, though I did just read a story of them disappearing in five years! (CNBC via Yahoo). Did you buy and hold and hedge?

I’ve been in and out of Apple a bit over the years, but have bought and held Google since picking up shares in 2005, I think

This has to be one of the most fun and entertaining news letters out there, you do not have that Joe B smile of Smiling Faces Tel Lies, it is your presentation that is a blast to read and by the way I know it was not the hospital Meds because they go to your pain and you have to come down when you get out, must be Obama’s new 15 person panel who knows your body better than you do, I hope it went well because it sounds like you are up to speed and I really mean that, I can not wait that when they just shoot a laser a you from the door and it tells your blood pressure unless you just like to be woken up every hour or so. But off of the smart tv multi screen and screens I bought all of those domain names for the write off ,especially after the San Fran, Calif convention next month ,I already had calls to sell them but as I said I might need the write off they where so impolite I would not sell the name that they said they would out advertise me by getting .net,.org .tv etc. I think they thought I just got .com and they called back again, this should be good for a few dollars on domain names greed is every where all the sites are under const. but they got my name somehow and they are big boys with there own they just do not want any competition, I told them go to my spacecloudboy.com and make an appt. there when Idecide what to do with them, I always did like the song SPACECOWBOY BUT NOW IT IS SPACECLOUDBOY.COM,etc any thoughts let me know because if we can not smile we should not be here. Back to business when Romney got on the coal miners against Obama I thought who ever wins will get some coal moving again dirty but cheep and it just blows across the Atlantic Ocean not like we where attacking China they use the heck out of it with SOLYNDRIA JUST A TAX PAYER JOKE , BUT REALLY iPICKED UP SOME COAL AFTER THAT SMART TV REMARK AT THE DEBATE TICKER (ARLP) any thoughts on that market or other plays on that energy that you think are in the money, I live in Oklahoma and Obama won’t even let the clean NAT/GAS go without the EPA and China’s approval. Really hope you feel good from hosp. and it is a blast reading your article’s , kind of like watching Johnny Carson and Ed in the old days and then making a buck off of your views which is a show I do not watch (VIEW) Obama goes on there and it is all women and talks about some video why does he not let his mother in law go instead at least she could tell us the colors the curtains are that Oprah wanted and now they don,t even talk. All in good fun what about coal and keep up the great work I should have to pay for this,good job!!!!!!

Cathy, the death panel is a fairy tale, sell your coal stocks (nat gas is a better way to go at least in the short run) and get some sleep tonight.

Jimmy L thanks for the death panel fairy tail . you know sell your coal stocks and get some sleep and that nat gas is better in the short run , your advice is impressive because I did short the coal stock you are a mind reader, and as far as the short term nat gas you might want to reconsider that or say who this short term wonder nat gas is , I kind of been doing okay on HFC AND THAT EXTRA DIVY and CVI AND JUST PICKED UP SDRL WHO HAS A NICE TWO DIVY MONTH IN DEC FOR 1.70 WHICH COMES IN HANDY ON DEC 21ST ,YOU MIGHT LOOK INTO THAT BECAUSE I have NOT FOUND A NAT GAS SHORT TERM LIKE YOU SUGGESTED MAY BE YOU WANT TO PUT A NAME WITH YOUR COMMENT as far as sleep that comes with Cancer and a broken neck but if you are such a good person as your comments seem you can go to my website usabaygreen.com and get something from amazon or one of the other affiliates on there. I do not keep 1 cent of that money it all generates and goes to the childrens cancer and leukemia via the BANK OF OKLAHOMA WHO DID NOT TAKE YOUR TAX DOLLARS FROM THE MAN WITH OUT A BUDGET CALLED OBAMA you seem like a person who would help a child in there last days , sleeping might be easy for a hard worker who stands in line to get his Obama check cashed MAYBE THEY WILL GET SOME COTS AND A NATURAL GAS HEATER WHILE THEY WAIT BUT IF THE KEYSTONE OPENED THERE MIGHT EVEN BE A JOB and the Navy would not be forced to buy there fuel from DYNAMIC FUELS AT 6 TIMES THE PRICE OF A GALLON AND WHO OWNS DYNAMIC FUELS THE BILLION DOLLAR CHICKEN MAN TYSON FOODS WHY WOULD THEY HIDE THAT AND THEN RIP OFF THE COUNTRY TO GET THE CHICKEN BUTCHERS UNION VOTE AND CUT THE NAVY who happens to let you vote and keep this country safe on 6 times the price of fuel from TYSON FOODS better yet go fill up at 6 times what a gallon cost the Navy, go ahead and look up the modern day SOLYNDRA RIP OFF MAYBE THEY COULD GET ON YOUR SHORT NAT GAS RUN , Do you think the DRONES OBAMA JUST BOUGHT FROM CHINA AVIATION RUN ON NATURAL GAS look on that Web Site how patriotic for Obama to buy Drones from China and bring them here, they are on there way some to the ports in CALIF. SOME TO TX, AND THE REST TO NEW YORK so the union guys can unload them, go ahead and pull the China aviation web site up Obama forgot to tell the voters he likes watching those Drone Movies FROM THE WHITE HOUSE now that is the USA embassy death panel FAIRY TALE and don’t you worry they will be watching you so maybe you can get some sleep. Well have a good rest

Man that sounds like the whole of America is being run by Obama! or it is just paranoia rapped in that nice rant wrap!

Yes He is in fact the great dictator…or at least he thinks he is. BTW the death panels are a myth in NAME only. Read that part of the bill. When a third party decides on your treatment based on predetermined factors(which we are not privy to) what would you call it. I really wish Obama’s minions would read his books. Why would they; the bandwagon is still rolling!

You are crazy. The third party you are talking about NOW are the insurance companies accountable to no one. Under so called Obama care the panels, which are not death panels BTW, are accountable to US. They simply choose the most efficacious treatment based on best practices, not deny coverage like insurance companies simply based on cost! And the panels don’t prevent you from paying out of pocket for whatever treatment you want!!!!

seems like LOTSA paranoia……………..

Cathy sounds like one of the flag-waving Right Wingnuts who has gone off her meds big time–either that or she’s a Teabagger suffering from paranoid delusions. She probably needs Obamacare, so she can get access to some psychiatric help. LoL.

She has more of a lefty-loony Obama supporter tinge to her ramblings if you substitute “Bush” for every “Obama” she typed. Sort of like the progressive wackos in the Occupy movement shouting their drivel in front of the bull. Different team, same playbook, as perfected by the Leftist morons from 2000-2008.

I love how the right-wing nut balls refer to end of life planning/help as “Death Panels”. No one is telling anyone what to do or controlling their lives! Conservatives are afraid of all change, that’s the definition of a conservative. They are also generally older, generally more religion dependent and generally less educated. Just look at FOX News – High on scare tactics, short on facts with lots of editorializing and comments like “what If…”, You never Know”, “Pretty soon…” and “mark my words…” Not a truly fact-based presentation like all the respectable networks. It’s really too bad that so many people are afraid to embrace change. Which has gotten America to where it is today. The world leader in just about everything!

what do we know about Ice Web

I believe that content is king and that it is becoming very more hard to monetize. The internet and TV will be eventually be one. Many kids today download their TV programs commercial free from torrent sites or stream them on the internet and view them on their laptop, tablet or their TV screen. I like the content provided by owners DIS, TWX, NWSA and SNI but think that their current stock valuations are too rich.

I can come to terms that content is king but haven’t we seen content companies loose their way and become shadows of the their former glory. So I would probably buy some shares in any of these companies but I’d keep an eye on them for management changes that would affect the future earnings. Look at MGM, Marvel or how Rupert Murdoch built his media empire.

Ok I’m willing to admit that content is king but… this is a multilayered issue.

You have content then distribution but finally you have personal delivery; ie your player. This is the bottleneck. Tv gets a finished product, video and audio fully rendered. All other systems get data and that requires a player such as adobe, the dominant player in this space. The player is required because of the excessive volume of data. This leads to the current problem of too much bandwidth.

These content providers may well be good long term plays but short term capital gains will almost certainly be in tech companies dealing with the bandwidth issues such as Destiny Media Technologies (DSY on the TSX). They have created a new player that plays through your computers browser instantly and reduces bandwidth by 95%.

Thank you for all your hard work Travis and well done with the charitable work.

So, what are the three stocks ?

Did you ever dind out what the three stocks are?

DIS

SNI

DISCA

If one had shorted apple when the price slipped below the 50day moving average, one would be looking at a tidy sum

I just watched the Motley Fool video today and then read the analysis above.

I must say that I’m not convinced that they’re right on this one. To use their Cheerios example, granted, it doesn’t make sense for me to go across town to buy a box of cereal if the store across the street from me sells the same box for the same (or lower) price. But, what they’re trying to say is that I should go out and buy General Mills stock just because a new store opened up across the street, which will take business away from the store across town. In the end, I don’t think General Mills’ profit is going to change if I buy the cereal from one store or the other.

Likewise, I don’t see how a content provider’s profit necessarily increases just because their TV shows are distributed via the internet instead of television. If anything, I could see this hurting some of them, because with the internet, the array of available content is much larger, meaning competition is much higher. For traditional TV, the production companies’ competition was each other. On the internet, their competition is each other, PLUS all of the other stuff you can find on the internet (no, not just THAT stuff, get your mind out of the gutter). You can kill an hour just browsing through Youtube videos that people took with their own cell phones (hell, you probably killed a half hour just watching that long-winded Motley Fool commercial).

I wouldn’t be surprised if low-cost TV productions, using nothing more than a couple of high-end digital cameras and some good editing software, become hits with their own followings on Youtube and similar online content distributors. In the past, it took a lot of expensive equipment to create a good video, and there were very few opportunities to get that video broadcast since the only real way to do so was through a TV station. Now, anybody can make a video and the whole world can see it within a few minutes.

To look at it another way, who really profited from the downfall of the record industry (weren’t they also “content providers”?)? It was Apple, through iTunes. Who profited from the downfall of the book publishing industry? It was Amazon, through the Kindle. (Those are just examples. I’m aware that there are others who have also been able to similarly profit through digital content delivery.) Who has really profited from the death of newspapers? Has anyone? I can’t tell you the last time I actually paid for news content (I just get it all online, for free), so if anybody, it’s the internet service providers who were already getting money. Otherwise, you just have the news companies selling ads, just like they’ve always done, so there’s really no new revenue/profitability there.

So, if the Amazons and the Apples (and the Googles) of the world have been the ones to have profited off of all of the other phases of the internet revolution, why should it be any different for television?

Yes, the content providers will always be there, and it is the demand of the content that drives everything, but I just don’t see how getting rid of cable and replacing it with internet distribution suddenly makes Disney more profitable. You’re just replacing one revenue stream (TV advertising and cable carriers paying to broadcast their shows) with another one (online advertising and digital content licenses). But, as I noted earlier, the internet brings much more competition to the table, and a lot of that competition is free to the end viewer.

When the cable companies go down, it will be whoever controls the new distribution channels that will profit.

Absolutely agree with your comment. I don’t see the leverage tilting in favor of the content providers. If any, whoever has the best delivery mechanism will hold the edge over the content providers. You are right, it doesn’t affect GM at all if I buy my box of cereal from Walmart of CVS Pharmacy! I can’t see Google laying fiber optic cables throughout the country and the world. Apple could revolutionize “how” you consume your content, just like how they revolutionized how you talked on your phone. Unless Google has something up their sleeve on this front, in the next 5 years, Apple (and perhaps Samsung?) has the edge…and all of the smaller companies that make Apple technologies work.

Exactly! You guys are right where I was after listening to the MF video. In addition to what you have shared about consumption devices/services, I also believe backend streaming technologies companies like AKAM will prove huge players. AKAM is cheaper now that most Fools have dumped in fear of further drops, but their fundamentals are solid and growth prospects on a global basis outstanding.

I have researched Disney and Scripps and Discovery and what I find is interesting. See http://www.secform4.com/

All three show massive insider sales, no purchases. Some insiders have even sold out their entire positions!

Why would I want to buy a company whose insides are bailing out?

Many saw accelerating income/cap gains into 2012 to avoid the higher taxes they all knew were coming after the election. This is/was true for all taxpayers.

In this space (content providers and distributors) there are so many different scenarios that might emerge – all of them just about equally plausible – that I think any investment is purely speculative.

A backlash building. As content providers raise their rates cable bills getting out of control. Also cable sells ads also and much programming is decimated to make room for it.

You and Motley Fool both mentioned the new rabbit eared digital set top antennas that will pick up a great number of these channels without paying for cable. I suppose a great number of people could benefit from them, and even some poorer customers could dump their cable if they had them. Couldn’t the producers of these devices be a good investment?

Probably not — I presume any Chinese manufacturer can churn out digital

Antennae for a couple bucks a pop. At most. There’s nothing particularly proprietary in over the air TV signals, as far as I know.

Not only are they “not” right…they are dead wrong…

i am retired from the programming industry

Its a fundamental misunderstanding about cable and programming…

cable makes a good margin on television…their broadband margins are in excess of 90%

none of what he talks about can be watched without the broadband connection except through expensive wireless data plans…so the supposed antiquated networks are in total control…”Clawing to hold on”??? ‘attacking with fiber?? its laughable..

i have been long comcast, aapl, goog, and disney for a while..im quite pleased and i expect both to thrive in the future …if google invests $100 billion in networks i’m selling GOOG…

google fiber is a test…verizon spent 10 years building out FIOS in only a part of the country.. it will take 20 years or more for google to build out..and the costs would be literally $100 billion’s

and in the meantime the cable companies will simply put the same tech in their networks…it makes absolutely no sense at all…and it highlights the vacuous nature

of the “analysis”…he neglected to mention that comcast owns more dark fiber than google…its laughable..they bought it over 10 years ago!! they have been preparing for this since they bought ATT cable in 2001…

my own sense is that folks at comcast are actually happy with this trend…it will take 20 years for this all to happen..and during that time, cable will ramp up data plans and we will paying the same $150-$200 bucks, maybe more….. without the margin hit from programming..

also people do not understand that when disney loses their monthly sub fees, and advertisers can’t create value and subsidize programming and cable…the programs we think we get for free will be much more expensive…look at what wrestling and boxing can charge for niche programming unavailable anywhere else…and that will give you an idea of what it will cost to watch tv…

i watched the video and i actually have motley fool newsletter…this video made me wonder if i should drop it..

Cable companies are virtual monopolies within thgeir service areas. At some point this will change. Most people hate their providers. They don’t hate their content. Much of the existing fiber was government subsidized either directly or , in most states, where customers funded the networks via costs still included in local service charges. In other words a de-facto broadband tax. Read you provider bills and look at every line item. Somewhere there is tax meant for companies to use for broadband initiatives. They owe us.

This is as hilarious as it is uninformed.

There is no doubt that cable companies benefit from rights of way and access to public works..they pay for those rights, and pass those costs on to consumers.

However, since the mid 90’s Comcast has spent over $100 billion building out their network….this is why Google Fiber is nothing but a test..they will never spend that kind of $$

Cable companies “owe” us nothing except their fiduciary obligation to maximize the value of their company on behalf of shareholders, and i’d say they are doing a pretty good job.

I subscribe to Motley Fool. However, this particular article is so idiotic that it makes me wonder about what they say regarding industries where I am less informed.