Today, we take you back to 2012… The Motley Fool is promoting it’s “$2.2 Trillion War for your Living Room” stocks again, and the ad is almost identical to the version that first started circulating in the Fall of 2012.

That’s not all that shocking, of course — once a newsletter publisher finds an ad that catches the eye of potential subscribers, they have every incentive to make sure everyone with an email address sees that same ad at least a few times a week. But this one got some folks curious because it’s being released as “A MOTLEY FOOL INVESTIGATIVE REPORT — MARCH 25, 2016”

Which it sort of is, in that there are a few comments about the fact that these picks were made a couple years ago… but they continue to keep those older picks “secret” in the ad and encourage you to sign up to get your full “Golden Age of TV” research report and a subscription to Motley Fool Stock Advisor to learn more. They also indicate that those three stocks have done spectacularly well, though they use the time period from 2012 to 2014 to illustrate that success, regardless of the fact that we’ve had another 18 months since then that could have been included, had the “Investigative report” really been done on March 25.

So… since they’re going to re-mail the same ad with minor updating, we’ll do the same thing. What follows is the identical article I published on October 15, 2012 identifying the three stocks the Fool was picking… and then stick through to the end, and we’ll see what their performance has been like and check the current valuations. I’ve also left all the original comments appended in case you want to see what other readers think.

—from 10/15/2012—

The folks at the Motley Fool have pitched a lot of “big change” stock ideas over the years, from the “end of ‘Made in China'” (3D printing) to the “Death of Microsoft” (cloud computing), and these email campaigns always get a lot of attention from Gumshoe readers … both because they’re well pitched and because the big trends they describe often do, at least in broad terms, seem well-grounded in reality.

So it caught our attention when the floodgates opened over the weekend and thousands of readers (OK, dozens — but still) wrote in asking about the latest pitch from them, called “Television 2.0”.

It’s a long ad, as they always are, and it’s signed by one of the tech folks at the Fool because he tells a personal story about taking his daughter to school and having her throw the epiphany in his face that yes, teenagers don’t need traditional cable TV anymore … but it’s really an ad for Tom and Dave Gardner’s Stock Advisor newsletter, the flagship publication of the Motley Fool, and it’s about how content creators will be the winners of the “war for your living room.”

Here are a few excerpts from the ad about the big picture — which is basically just that more people are getting their video in untraditional ways and video and cable providers are losing leverage:

“Because the percentage of households with a cable or satellite subscription is now declining for the first time in the history of television.

“3 million Americans have already cut the cord, including 425,000 in the past 3 months alone.

“And according to Credit Suisse analyst Stefan Anninger, those ‘cord-cutters’ are joined by a new group … the “cord-nevers.” A full 83.1% of new households are choosing to live without pay-TV.

“No wonder Business Insider reports that the cable/satellite industry is ‘starting to collapse’…”

And this about “how we got here,” including comparisons to old monopoly businesses like the music labels, phone company, etc….

“We started paying more and more good money to get less and less good programming.

“And we put up with it for too long.

“I mean, millions of Americans dropped newspapers, long-distance telephone service, bookstores, traditional stockbrokers, record companies, travel agents, and department stores, even though they were actually quite happy with those businesses.

“It’s just that something better came along.

“But here we are still clinging to this outmoded television delivery technology that we’re all really unhappy with.

“And now that something better has come along for this too, it’s time to act.“Not just as consumers, but also as investors.”

And then he preemptively covers that concern that’s probably popping up in your head right now: In most cases, the fastest internet service you can get is from … your cable company (or another hated monopolist with bad customer service, your local phone company), and won’t they find a way to shut down those pipes if you stop paying for the content they sell through their cable box?

“… another big problem had occurred to me.

“Even if I quit cable, won’t I still be paying those same #$!&(&*$ for my internet service?

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“You can use your imagination to figure out the actual word I said.

“But it turns out that Tom has been researching this same puzzle for months. And he’s already found the solution….

“Google Fiber. And it could be just as revolutionary as Google’s search engine was when it debuted…

“Making our internet connections 100 times faster (fast enough to watch TV and record 8 other “streaming” shows in high-definition all at once, with no herky jerky download delays). And all for the same price most of us pay our cable companies for internet right now.

“In other words, it will completely break down the wall between television and the Internet. And put the cable companies out to pasture.

“CNN Money is calling Google Fiber an ‘audacious bet.’

“But Tom says it just makes sense. (And he should know…he recommended Google in Stock Advisor on July 20 when he found out about the Fiber project, and has already made a 18% gain.)”

What is Google Fiber, as we go off on this tangent? It’s Google’s effort to push for better data service by buying up unused fiber optic cable and offering up a test bundle of tv/data/phone at a set price — it’s very much a test, here’s how the ad describes it:

“… other companies … tried to build a fiber-optic information superhighway over the years (including the cable companies) [and] left a lot of unused wiring. It’s called ‘dark fiber,’ and Google is quietly buying it for pennies on the dollar.

“Meanwhile, they’re plotting their next move — now that Google Fiber reaches more than 90% of Kansas City, they’re cutting deals with ESPN, CNN, TBS, Cartoon Network, plus (you guessed it) the NFL Network. And placing help-wanted ads for national sales representatives on their company website.

“Which is leading some technology watchers to conclude that the Google Fiber experiment in Kansas City ‘is not a test’ but rather ‘a takeover plan.'”

It’s hard for me to imagine Google pouring trillions of dollars into wiring the entire country, my assumption would be that this is all part of an attempt to push other people (the telcos and cable companies, mostly) to improve connection speeds by giving them a little frightening taste of competition, but that’s just my guess. Right now it doesn’t cost Google that much because it is literally only available in a few “fiberhoods” of two cities, and those two cities are Kansas City, Missouri and Kansas City, Kansas. Still, I must admit that if they had this service available in my town I’d be tempted to jump on it — resentment of incumbent providers runs high, though unfortunately it’s pretty much in inner cities where there’s enough population density and “dark fiber” to make new startup services feasible on the cheap.

More from the ad:

“I was starting to think that Google would be my big winning investment in ‘Television 2.0.’

“But David’s research has now convinced me otherwise….

“You see, Google Fiber isn’t the biggest immediate threat to the cable companies. Because it might take a few years to complete its nationwide roll-out.

“What would really make me sweat if I was the CEO of Comcast, Time Warner, or DirecTV, is a tiny detail buried on page 555 of Steve Jobs, the best-selling official biography of the Apple CEO written by Walter Isaacson.

“(David’s been watching Apple closely for years — he pointed Stock Advisor members to the company in 2008, right when the iPhone was gathering steam. And they’ve made a fantastic 336.9% return on that investment already.)

“This is the key quotation, from Steve Jobs himself:

‘I’d like to create an integrated television set that is completely easy to use. It will have the simplest user interface you could imagine. I finally cracked it.’

…

“So while some say Apple’s announcement next month will introduce a smaller version of the iPad… the truth is, Apple needs a bigger splash than that to justify the sky-high stock price that comes with being the most valuable company in the history of the world.

“That’s why Barron’s calls the announcement ‘an event well worth watching.’

“Why Computer World thinks that Apple is preparing a ‘sneak attack’ on the TV market. And why The Atlantic says ‘Apple wants to be in your living room. And it doesn’t want to settle for being the screen in your lap while you watch TV. Apple wants to be the TV.’

“It’s also why you may need to act NOW if you want to position yourself for maximum profit in the ‘holy war’ for control of television that will be waged in 2013 and 2014.”

Which, as you read through, might make you think he’s recommending Apple again — but that’s not the case either. He lays out the competitive landscape for TV viewership:

“There’s the cable and satellite companies clawing to hold onto their trillion dollar revenue stream.

“Meanwhile, there’s Google attacking through its fiber optic wires underneath the street.

“And now Apple opening a new battlefield in the living room.

“Not to mention other industry heavyweights that already offer popular ‘Television 2.0’ services with a far greater toe-hold than Google Fiber or Apple TV.

“Like Amazon, which has more than 10 million video on-demand subscribers in its Prime service.

“Or Netflix, which has more than 27 million subscribers watching movies and TV shows through its interface.”

And then gets to his “content is king” realization:

“David and Tom sorted it all out for me with something they called ‘The Cheerios Test.’

“And sent me running to my online brokerage…NOT to buy Google, or Apple, or Amazon, or Netflix…but to buy two stocks I had never heard of before, and a third one I would have never even considered…

“You see, with the brilliant strategy they gave me, it doesn’t matter which corporate giant gains a decisive advantage in this war…or when.

“Because as long as you know how to invest in these 3 stocks, you’re in good position for any outcome.”

So what the heck is the “Cheerios Test?” Here’s what he says on that:

“I love Cheerios. (Better than Raisin Bran or Froot Loops.) I eat Cheerios. (Every morning!) But I don’t really care that much about who I buy them from or what kind of package they come in; I just care about convenience and price.

“That’s when it hit me.

“They were saying that TV was basically the same.

“What we really love are TV shows. Right?

“My daughter likes Glee. My son likes Family Guy. My wife likes Top Chef. And I like football.

“It doesn’t really matter what screen we watch them on, or what time of day…or what network, cable company, satellite dish, website, app, or gadget delivers them to us.

“Our shows are our shows!

“A recent Forbes magazine article agrees. It starts with an alarming headline: ‘The Death of Television’!

“But it goes on to explain that rather than dying, TV is about to be reborn.

“And in the world of TV 2.0, we’re in control.”

So yes, it’s about who owns TV shows and can get them to you. This has been a matter for investor debate for many years, and you’ve probably heard the “content is king” argument before, though it’s held a bit stronger for video content than it has for newspapers, magazines and songs so far.

They give a rundown of some of the major content showdowns between content owners and distributors in recent years, many of which have led to better payouts for content owners:

- “Like the AMC channel (home of Breaking Bad and Mad Men) staring down the Dish satellite network.

- Fox playing chicken with Cablevision and almost blacking out a 2010 World Series game.

- Viacom (which makes The Daily Show, Jersey Shore, and Spongebob Squarepants) strong-arming DirecTV.

- The Starz movie network pulling out of Netflix.

- And the Madison Square Garden channel taking its New York Knicks games away from Time Warner cable during the height of “Linsanity” this spring.”

And there are plenty of other examples — this is a flip from where things where 10 or 20 years ago, when upstarts like ESPN or Fox News were paying cable companies or providing free or very cheap content just to get distribution. Now that content is often what drives cable and satellite subscribers to renew, so the fees content providers are charging are climbing dramatically, and cable companies are chafing… but the loss of the cable monopoly is hurting them, since so much of this content can also be accessed online and the providers of genuine hits have leverage both to get better deals for those hit shows and networks, and to force more “bundling” of their weaker offerings that are trying to gain traction.

So that’s a long bit of chatter to get through as we finally start to get some hints about which companies they’re picking:

“Why you need these 3 stocks NOW

“We’ve seen that on-demand direct distribution to the customer changes everything.

“Just like it did for online airplane and hotel bookings with Priceline.com, and online purchases of books (and just about anything else) on Amazon.com….

“Which gives content providers the upper hand — regardless of whether they’re going through traditional carriers like Cablevision or Time Warner, or new challengers like Google, Apple, and Netflix….

“Tom and David think these three winners are about to go on the kind of epic run we only see once every 10 years or so.

“And it’s hard to disagree. Because as you’ve seen in this report so far, the next revolution in television has only just begun.

“Once more people find out about Google Fiber and the new Apple TV set over the coming days and weeks…the war for the living room will be what everyone’s talking about.

“And that means even the Wall Street skeptics will finally come around…

“Which gives you a short buying window. Fortunately, there’s still time to join those Stock Advisor members and cash in — but you may need to act NOW.

“I wish I could tell you the name and ticker symbol of these 3 uniquely positioned stocks. And if it were up to me I’d probably just spill the beans.

“But my friends in the Motley Fool customer service department tell me I can’t, out of respect to the members who are already paying for our Stock Advisor service.”

Which is where your friendly neighborhood Stock Gumshoe jumps in, of course — I can’t give you their full report on these stocks or tell you exactly what advice they might be giving, but I can at least sniff through their clues and tell you the stocks and the tickers and give a little basic info so you can go forth and researchify on your own.

So let’s get to it, shall we? First!

“Company A is an $89 billion powerhouse that owns more than 100 global television networks, plus 7 movie studios, 4 video game companies, and hundreds of websites. Not to mention a little-known research laboratory that’s developing the next generation of TV technology. (Like a new system that lets you use any object in your house — including your couch, your coffee table, even a glass of water — as a remote control). In fact, this company’s growth potential is so strong that legendary hedge fund investor George Soros just snapped up a million shares.”

Well, probably no surprise to you there but this one is clearly Disney (DIS) — and yes, you probably also know that it’s an entertainment and content powerhouse as well as a travel and technology company, owning huge content-spewing brands like ABC and ESPN as well as the eponymous studios and cable networks and relatively recent acquisitions Marvel and Pixar, among many others. They’ve gotten so big now that it’s hard to pick just one “crown jewel” from their assets, but ESPN has probably been the single most powerful content provider in the cable/content wars, with what seems like almost unlimited power to raise per-subscriber fees — after all, ESPN gets both huge live viewership (sports is watched live, mostly) and a strong “young guys” demographic that brings in huge advertising dollars from the film studios and beer and car companies (among others).

And yes, it’s hard to argue with an investment in Disney — it’s got a fortress balance sheet, it’s a blue chip company that’s incredibly profitable, it has become a dividend growth company over the past decade, and it’s reasonably priced even after the stock has gone up about 50% in the past year. I guess the only real argument against building a position in Disney at times like these is that it’s also a tourism driven and hit-driven company, so there have tended to be opportunities to buy the stock cheaper in years when theme park visitors are down, or when they have a big flop year with their movies — though it can be hard to nimbly watch and take advantage of those things. The John Carter film was a huge flop for Disney relative to expectations over the winter, but even the announcement that they would book a $200 million loss on the film in the Spring failed to keep the stock down for very long, largely because that news came right around the time they announced that mega-hit The Avengers made over $200 million in ticket sales on its opening weekend.

I’m sure no one will get fired for recommending Disney, but this is one that, were I to buy it as a long-term hold, I’d probably nibble now but try to scale into it over a couple years and hope for a couple bad tourist seasons or a lousy Christmas movie slate to bring dips in the stock. I did own Marvel Entertainment years ago, which was a hugely successful recommendation of David Gardner’s back when they were on the verge of bankruptcy and the first Spider Man movie had yet to be released (and years before Iron Man and The Avengers made the Marvel stable of characters look like such a no-brainer goldmine), but I don’t think I’ve ever owned Disney.

Still, if you feel like there will be a full-fledged “war for your living room” with several companies vying to provide live TV, it’s hard to picture a company having more leverage in this than Disney, since they bring with them ESPN, ABC and their own Disney Studios content, and there isn’t a single cable provider in the country that could sell their service effectively if they cut ESPN. That leverage might not impact a $90 billion company that much on an earnings per share basis, particularly as this “war for your living room” will likely be waged over many years and through many test locations, but it’s still leverage.

Oh, and yes, they do have a research division that came up with a crazy cool technology that could turn your houseplant (or other stuff, I guess) into a remote control — there’s a story on that here if you’re curious. It’s not going to be financially significant in the next few years, I would bet, but it is cool.

Next?

“Company B rose from the ashes of a declining newspaper empire. Now it’s cultivating a niche TV audience that’s especially attractive to advertisers. Allowing this company to generate more than $2 billion in revenue from just 1.7 million viewers…At $1,290 ‘revenue per viewer,’ that makes its programming 76% more profitable than the average television network.

“According to Investor’s Business Daily, even though the entertainment industry is extremely lucrative, it actually has ‘a puny number of high quality stocks.’ And those are two of them.”

This one is a company I don’t know well at all, other than being quite familiar with the fact that they’re responsible for the celebrification of the interior design, real estate brokerage, and cooking industries — this is Scripps Networks Interactive (SNI), which owns the Food Network, HGTV, the Travel Channel, etc. Scripps did indeed start as a newspaper company, and was one of the dominant newspaper publishers in the world for the second half of the 20th Century (you know, back when newspapers made money), as well as a major local media company through a network of local TV stations and cable companies, but about 20 years ago they started spitting some of that prodigious newspaper cash flow into content creation, building and buying those now-well-known niche cable brands, starting with HGTV. Four years ago they split the company, so the original E.W. Scripps (SSP) still owns the 20 or so TV stations (mostly ABC affiliates, coincidentally) and 13 mid-market newspapers around the country and is a stagnant, barely profitable $600 million company, and Scripps Networks Interactive owns the five cable channels and is a rapidly growing, highly profitable $10 billion entertainment force. Or farce, if you’re feeling cynical about our desperate desire to watch other people saute onions and declutter their mud rooms.

You can certainly argue that Food Network and HGTV are strong enough, with loyal enough viewers, that they should command premium and growing fees from cable and satellite providers — if you’d asked me, I would have thought that this celebrity chef fascination was a flash in the pan when Emeril Lagasse was the standard-bearer five years ago, but even though he has moved on there are still dozens of stars being made like Guy Fieri and Paula Deen (who are, in turn, turning themselves into chain restaurant brands). So I’m the last person to suggest that I can tell where this trend goes, but these cable networks seem to have a pretty good thing going — they have low-cost content, they build celebrities who must, I presume, work cheap as they build their personal brands, and when those fizzle or the stars demand more (a la Emeril, I suspect), they move on and build the next star. It looks like it’s working pretty well — they did quickly end disputes with AT&T and Cablevision when they were briefly shut out of those networks for a few days during contract renewal talks a year or two ago, and I presume that it was pressure from subscribers that led to those resolutions, so this does seem to be a content provider that has a fair amount of leverage over the distributors — and, of course, a solid web presence.

I’ve never looked closely at SNI, but I did skim through the last quarterly report and note that while they are growing revenue pretty nicely, they’re expecting to grow expenses more quickly this year — I don’t know if that’s a sustained trend, but it’s an indication that their programming costs might rise faster than their advertising revenue and subscriber fees, which obviously would be a huge weight for the business to carry since they’re already carrying a premium valuation (about 20X trailing earnings). That could well be a temporary thing, I don’t know, but it’s something to keep an eye on — we’re certainly moving into an era of more distributed programming, with more online video … but my impression is that advertisers still tend to pay substantially more for targeted, timely mass attention through hit shows than they do for online advertisements, so that transition is closely watched by both advertisers and content owners. There’s also a competitive aspect to this space, since HGTV and Food Network have to maintain their brand positioning against plenty of other niche cable channels as well as against upstart online brands in their space, but they are clearly a leader in that competition now so they do have at least some advantage.

Next?

“Company C didn’t make IBD’s list…because it isn’t really an entertainment company. In fact, even though it operates some of the most popular channels on TV (reaching more than 1.5 billion viewers in 180 countries), its business model is completely different. Its most important customers are actually elementary and high schools. And now it’s entering another $25 billion education market with a breakthrough product that’s half of the price of the traditional choice. So you can see why this company has been able to grow its quarterly earnings per share by a fantastic 22.5% in the past year.”

Well, I don’t know if I agree with that summary of the company — but we fed it through the Thinkolator and this is pretty clearly Discovery Communications (DISCA and others, more on that in a moment), the other big cable network company that gets a fair amount of investor attention. Like SNI, they enjoy the benefits of all of the original “reality” shows — low production costs and niche marketability. They call themselves “The World’s #1 Nonfiction Media Company” and produce a bewildering array of programming for their popular channels, including Animal Planet, Discovery Channel, TLC, The Oprah Network, etc. And they are taking advantage of international distribution in a big way, partly because their documentary, reality and educational content is very easy and inexpensive (compared to fiction, at least) to translate to different languages and cultures.

But I don’t know that I agree that schools are its most important customers — or that their “breakthrough” will really turn out to be such in the “another $25 billion market.” They do have a strong educational offering, with streaming content that’s available in about half the schools in this country (replacing the beloved filmstrips of my youth on those days when the teacher has a migraine, he says cynically), and they are moving into “interactive textbooks” in an attempt to help shake up the $25 billion textbook industry, but when it comes to financial performance it’s all about subscriber fees for their networks from cable companies, and advertising revenue. In the US, they’re close to 50/50 ads and subscriber fees, and internationally subscriber fees are a stronger revenue generator at the moment — “education” is a rounding error when it comes to revenues and earnings at Discovery, though it’s certainly possible that they use that division to drive earnings or cover expenses in some other way. Their textbook initiative, called “techbook,” is yet another way for them to leverage their content into the education sphere — using the educational content they already produce to build interactive textbooks for schools, but I wouldn’t put too much weight on that. Education is a small part of Discovery’s income statement, and it’s not as though folks like McGraw-Hill or Pearson, dominant textbook publishers, have failed to notice that there are opportunities in technology-enhanced publishing for students… it may end up working well for Discovery, but I can’t see it being a major part of the business in the next five years, my guess is that in 2018 we’ll still care more about Bigfoot, River Monsters and custom choppers than we do about Discovery’s “techbook” business.

Discovery is also one of those multiple-class stocks — DISCA is the A shares, which get one vote per share, DISCB, B shares, gets 10 votes per share, and DISCK, C shares, gets no voting power. DISCK trades at a bit of a discount since it doesn’t get the voting power, which might be interesting for small investors who understand that they don’t get any corporate voting power anyway, though you can imagine a proxy fight or activist investor situation when voting shares should trade at a substantial premium, too, so those things are always a tough call — and really, though I hold shares in companies that have “lower class” non-voting or fewer-votes shares (like Berkshire Hathaway and Google), I don’t like to encourage that activity. The B shares are very illiquid, but currently priced about the same as the A shares.

Discovery is extremely profitable and growing nicely — their growth in the last quarter was not as strong as SNI’s, but they’re more than twice as big and have profit margins that are a bit stronger, and they are really the leaders when it comes to leveraging content internationally and across platforms, which helps to significantly increase profitability when they get their content right. I have more confidence in Discovery than I do in Scripps, though that may just be because they have a broader array of channels and hits and niches they can play to beyond Scripps’ core niches of travel, cooking, and home improvement… or it could just be a reflexive response to the fact that Vanilla Ice hosts a real estate show for Scripps on their DIY network, and I have a hard time believing in a world where that’s possible.

This is clearly an interesting time of transition for television and video entertainment — I don’t know if we’ll end up “giving up” on cable TV en masse in a surprisingly fast transition as happened with CD players and is happening a bit more slowly with printed newspapers, but there is a move to more online and streaming content and there are plenty of companies who are working to further that transition with hardware, software, and streaming libraries, including Netflix and Google and Apple and Amazon and hundreds of smaller players, but it’s also quite possible that the transition will be a lot slower, and there’s still a lot of power in the hands of the TV networks and the cable and satellite distributors … even if it’s not as much power as they had ten years ago. There are, for example, plenty of places to watch shows online — and even lots of increased investment in professionally produced “channels” online through Amazon, Google, Netflix and the like, all of whom are funding content development as well as trying to expand their distribution businesses … but traditional TV still has a very strong position with the people who care the most: advertisers. Online video ads are a very fast-growing market, but reports I’ve seen indicate that they’re only about 5% of the size of the traditional television ad market, and the strength of television has always been it’s power to create a mass market and homogenize society, urging essentially every single American, over the space of two or three days, to see the same movie or visit the same store at the mall that coming weekend.

It’ll be an interesting thing to watch, seeing if the increasing niche-ification of media and the distributed content continues to erode that mass market, but I have my doubts that it will happen all that quickly — car dealers and movie producers really want to be able to reach everyone, all at once, and they’ll pay a premium for it … with some exceptions it strikes me that it’s been the advertisers, not the viewers, who are willing to consistently pay for hit content.

But that’s just my squishy impression of the speed of the big picture transition, and it probably doesn’t mean anything. What we get from this teaser are three strong content-dominated companies, each of whom is very profitable and trading at a premium to the market, and each of which has shown enough growth and stability to (arguably, depending on what you think the future holds) deserve such a premium. Think Scripps Networks, Discovery Communications or Disney are right for your portfolio, or the best play on the revolution in video delivery? Let us know with a comment below.

—–and back to 2016—–

Well, the story today is pretty similar to 2012 in some ways, at least as long as you’re using a broad brush to paint the disputes between content owners and content distributors… though Facebook, Google’s YouTube and others have dramatically increased the power and profitability of video advertising on the internet in the last few years.

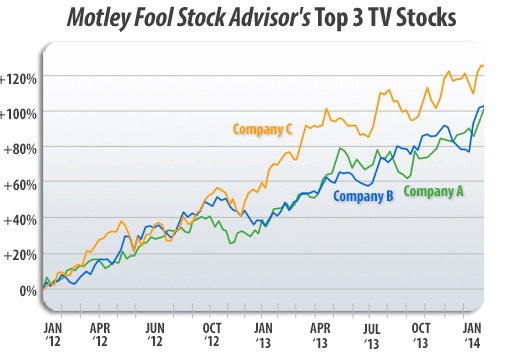

The latest version of this ad includes a chart of the performance of those three stocks from 2012 until the last time they probably really updated the ad, in early 2014. Here’s a screen grab of that:

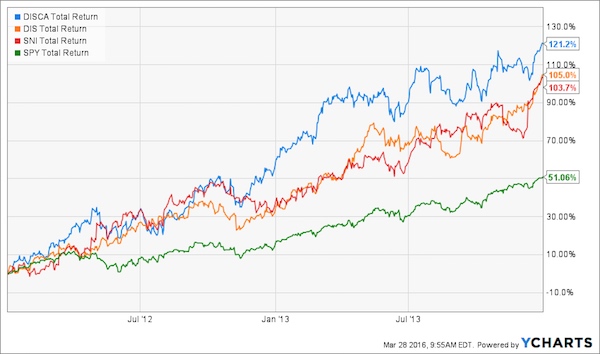

And here’s my version of the same chart, all I really did was add in the S&P 500 as a comparison (that’s the green line on the bottom) — this is a ‘total return’ chart, so it includes dividends:

You can see that the ad isn’t lying about that 2012-2014 performance — all the picks did essentially twice as well as the market. But why are they re-promoting this idea now, more than two years after the end of the chart? Are the stocks still outperforming the market, or are they appealing bargains now? Here’s what the chart looks like if you bring it up to the present:

The S&P 500 is still that green line, now with a total return since 2012 of about 74%… but now that’s a lot better than the total return of Scripps Interactive and Discovery Communications, each of which lost roughly half its value over the last two years. Disney is the only one that has continued to beat the market, despite the fact that it’s by far the largest of the bunch (and despite the fact that it took two serious tumbles over the past year).

I never ended up owning Discovery or Scripps, but I do own Disney now — I bought when it collapsed this year, a dip in the shares that I felt like I had been waiting years to see. What do the valuations look like for these stocks now?

Discovery (DISCA/DISCB/DISCK) is expected to grow earnings at about a 10% rate over the next few years, and is trading at 18X trailing earnings. The stock has collapsed because growth dramatically disappointed over the past few years — you’ll note that the old clue above was that “you can see why this company has been able to grow its quarterly earnings per share by a fantastic 22.5% in the past year”… in the new version they did update the clues a little bit, and Discovery is hinted at with the sentence “So you can see why this company has been able to grow its earnings per share by an annualized 5.2% during the past five years.”

Growing earnings per share at 5% over the past five years is not impressive. Not for a stock that has always been talked about as a “growth” stock, paid its CEO $150 million a year or so ago, and had an average PE ratio in the low-20s for much of that time. To make matters worse, for most of 2013 the stock traded at 40X earnings. A lot of that investor disappointment has come because costs have risen for the content developer, for some of the same reasons that folks have worried about Disney (like the sports rights fees issues — Discovery bought EuroSport a while back and spent heavily on getting the Olympics rights in Europe), and because they depend very heavily on overseas growth and the strong US$ has really weakened those international results. They still have a lot of hits in the “unscripted” TV arena that they helped to popularize, and their partnership with Oprah appears to maybe not be as much of a disaster as it looked like a few years ago, so who knows, maybe they will return to growth, especially if the dollar weakens a bit against other major currencies.

Scripps Network Interactive (SNI), the owner of HGTV and Food Network, is much cheaper than Discovery these days and trades at what appears to be a more reasonable forward PE of 12… though the stock has been in the doldrums because earnings aren’t really growing. Earnings per share are expected to grow only 2% this year and slightly more in 2017, but analyst somehow expect them to reignite to average 10% earnings growth out into the future after that. I don’t understand why, and I’m always suspicious when big earnings growth numbers are based on huge numbers three or four years out instead of growth in the current year (just because the current year growth might be forecastable within some degree of error, but the other stuff is extremely unlikely to be accurate)… so it’s not too expensive to consider, but neither do I find it terribly appealing. But then again, I don’t like the Food Network or HGTV or understand the obsession with watching cooking competitions (though presumably it’s a problem for Scripps that the biggest cooking star around, Gordon Ramsay, doesn’t work for the Food Network). This still seems a thin bet for me on a few channels that I don’t think are likely to be as valuable or as high-growing as the analysts expect — but they do know a lot more than me, that’s just my opinion.

Interestingly, the old “moribund” parent, EW Scripps (SSP), has done much better than the spun-out Scripps Networks since 2012 — the old newspaper and TV station owner has doubled, while SNI is only up about 50%.

And Disney (DIS), which I do own now, is in a different league — it’s ten times larger than either Scripps or Discovery (yes, the clues above said “$89 billion powerhouse” in 2012 and that’s been updated to “$194 billion powerhouse”) and obviously has huge businesses outside of television content. And though I didn’t own it back in 2012, and thought it might be worth scaling into over time, it took me a long time — I bought into the stock last year because the stock got too cheap in the panic over ESPN’s possible problems from the “cord cutter” generation, and it’s still a pretty small personal position. ESPN is by far the most valuable cable television franchise, with dramatically higher fees than any other network and a huge advertising business, and it’s more than 40% of Disney’s earnings, so their future is obviously a big deal for Disney. I personally think the impact of cord cutting is overstated, partly because the trend is gradual and partly because I think ESPN is far likelier to be viable as either a standalone “over the top” channel sold without a cable subscription than most cable channels…. or a core part of new “skinny bundles” that are being talked about as a compromise for folks who want to get rid of $100 cable bills.

But I do acknowledge that DIS may face headwinds at ESPN, partly because of astronomical content costs (buying sports rights), and I don’t count on ESPN being the primary driver for Disney earnings in the future — I just think the market is failing to appreciate the fact that Disney is the world’s best marketer and brand expander, and it so happens that Star Wars and Pixar and Marvel and Frozen and now Zootopia are continuing to bolster the argument that Disney has again institutionalized, after a weak period a decade or so ago, their ability to create hugely valuable content that continually generates blockbuster results. Disney is huge and pretty expensive at about 16X next year’s earnings and will also probably grow earnings in the 10% neighborhood, analysts say, but it’s also, I think, the one real “blue chip” in entertainment, and the one that can work those brands across different businesses better than others (theme parks, cruises, movies, TV shows, merchandise, etc.).

You can see my bias there, of course — I own Disney and like it, and I’m a bit more skeptical of the growth of the other two… but Discovery and Scripps are certainly smaller and less tightly scrutinized than Disney, so there’s a better chance that some “hidden” value could emerge from those smaller shares that, unlike Disney, are still small enough that a big new hit show, or at least a new hit network, would have a meaningful impact on their shares.

That’s all for our trip down memory lane to 2012, and our current look at the same stocks that the Motley Fool continues to tease for potential Stock Advisor subscribers… have a thought about cord cutting, or these kinds of content companies? Other winners or losers in the shifting sands of entertainment? Let us know with a comment below.

Disclosure: I own shares of Google, Apple, Facebook and Disney among the companies featured above, and call options on DIS. I do not own stock in the other firms mentioned, and will not trade in any stock covered for at least three days.

Consider broadband over power lines . Using power facilities or fiber as back haul to Wifi access points (cell masts???). The investment issue is not the backbone of a network or even the local network distribution points….it has always been the “last mile”….the cost of getting the service into your home. Coax cable has been a huge investment but if you use this aren’t you still paying the cable company? Who is the player for the local wifi technology that can provide fiber optic speed media and support many users within a geographical area….or would it be the company deploying all of these last mile solution devices?

very informative.

Hi guys thanks you for the cool site , tips and all the good info I did get rid of my telephone land line since 1999 and got rid of cable since 2005 replaced by cell phone and INTERNET I just got me a smart tv at target on black friday and a roku 3 for Christmas and have been watching Internet tv programs and as you know most of students cannot afford to pay for cable so they will go for the least expensive method and that is my amigos streamed tv via smart tvs and or with roku 3, soon to be a roku tv this fall, so I will buy me some companies that have lots of CONTENT and I see a lot of more MILLIONS cutting off the pain in the a cable companies since you know when need them they you will be at your place between 8 am and 6pm and then just waste your time so this is the FUTURE of streamed tv is just starting buy your good stocks for the long haul and Happy new year 2014

I didn’t read through all your readers’ comments and someone may point this out to you already but they were not talking about Discovery. I too research the company and discover does not fit the profile. You should do more thorough research. They were talking about News Corp. the 180 territories and 1.5 billion viewers was alluded to Starsports news corp and espn collaboration for the ICC championship that hit 180 countries. The school books is Harper Collins who is as big as mcgrawhill that you mentioned.

Company A are you sure they were not talking about TWC and not Disney worth more than 89 billion? I’m unsure and still doing research but TWC makes more sense and may be they were talking about the now somewhat contentious and may not go through deal with Charter. Regardless it was definitely News Corp and not discovery they are talking about. Check out the facts .

No, I’m afraid you’re wrong. A is absolutely Disney, C is certainly Discover. The facts in the ad match Discover exactly, and I don’t believe News Corp has had a quarter of 22.5 percent earnings growth in the past couple years, aside from the fact that it doesn’t fit the theme very well, — but more importantly, the teaser pitch from the Fool also included a comparison chart of their three “secret” TV companies. The chart shapes exactly match the charts of Scripps, Discover, and Disney. News Corp isn’t close.

That’s not to say News Corp mightn’t be a better investment, that all depends on what you think of them. And they may have been featured in subsequent ads from the Fool — but as of a year and a half ago when this ad was sent around, and as of the version of the ad that you can still see here if you like, it was Disney, Scripps Interactive, and Discovery Communications.

Travis,

How about you fellers subscribe to all of the other investment letters, or have a friend or relative do so, and then you will definitely have all of the answers. You can then pretend to reverse engineer or claim that you have developed the “Stock Investment Enigma Machine!!! It may seem somewhat unethical but heck, the other stock adviser services are generally manipulating us with half truths and etc. anyway. Your analysis of those suggestions is what we value from you the most. That is your forte, so to speak.

Thanks Philip — I’d rather keep having fun with them and exercising the ol’ Thinkolator, but a few folks have suggested the same.

It seems to me that what is certain is that demand for ever faster broadband will soar and Verizon (VZ) is briliantly placed with their entire coverage of the USA with fast broadband. They have invested very heavily to be in position and has taken on considerable debt to buy Vodaphones 45% stake in its company. Watch them fly in 2014 and 2015 whilst their competitors scramble to catch up with the vast lead Verizon has. It seems as though they were very wise to do so.

Is that not an even better bet then the content providers, since it is their customers who have more reason to switch from cable to fast wireless broadband and save a fortune to receive such content.

Interesting/disgusting that they have been recycling this article for at least 16 months (I just got the email/ad for it today). A is definitely Disney, as the market caps match exactly in Oct 12 and Feb 14 ($139B)

I don’t know if it is the quirky way my browser is set up, but when I closed the tab which was playing the Motley Fool video, a dialog asked me if I really want to leave the page, and the video was replaced with the entire (text) transcript of the presentation. Coulda saved 45 minutes if I knew that in advance….

RE.47 I think you will find most such videos do that now. change happens.

The only thing I am sure of when reading the article and all the above is that Internet TV is the future way content will be delivered to our TV’s cheaply. No one loves their cable companies and their charges,

The cheapest and most effective way to deliver and receive content throughout the USA and internationally is through the internet when received by clients subscribed to a 4G LTE service. Thus the demand for high speed 4GLTE service will sky rocket. Verizon has by far the largest 4G LTE coverage reaching 97% of the population of the USA with AT&T in second place lagging considerably behind. I favour horizon at current depressed prices only because of the large amount of Verizon shares that shareholders in Vodaphone chose not to take up. The demand for 4G LTE will sky rocket in next to no time and Verizon is better placed to reap the benefits. Indeed it is not at all far fetched to expect US media companies to be interrested in buying Verizon so as to offer delivery of their content bundled with a 4G LTE full internet / TV / music/ film/ home shopping / phone service bundled.

I see no surer way currently to profit from the delivery of TV content over the internet that is about to revolutionise our lives. The content kings that we will all scramble for, may well turn out to be a consortium of content media companies that will be able to provide us all with the best and most diverse content as well as the fast 4G LTE service that covers 97% of the USA population (Verizon) bundled. That would make perfect sense for all.

The only worry with Horizon I have heard expressed is its debt level, following the vodaphone deal. Going into debt to be in prime position with your network to take full advantage of the demand that will explode for fast 4G LTE is of course a wonderful place to be. Having in effect borrowed to achieve a vast market lead for fast 4G LTE ensures you reap the benefits more than anyone else. Frankly it is dumb of Vodaphone and vodaphone shareholders to sell their horizon shares at a time when it would seem a certainty that TV via the internet will explode. Perhaps Vodaphone and AT&T wish to exploit the cost savings and wonderful fit globally that could be reaped when taken over by AT&T for the benefit of Vodaphone shareholders as well as AT&T shareholders. Owning 45% of Verizon may well have posed a problem for such a deal when even greater benefits are to be reaped globally under AT&T. I suspect we will see an agreed deal within six months in which AT&T buys Vodaphone at a price that is bound to be attractive for Vodaphone share-holders. This certainly makes sense as to why they chose to sell the wonderful investment they had made owning 45% of Verizon at a time when they were fully aware of the vast leap in demand for 4G LTE services that delivering TV over the internet would bring.

I remember when a 12 baud modem was hot stuff & www stood for world wide wait. I believe that for some time yet backbone won’t catch up to demand for content streaming of all kinds,TV, Netflix, communications,data in general & is going to demand huge increase in electric generating capacity. To fill that need I think either uranium or thorium reactors are an absolute must. The drawbacks can & will be solved. If the USA alone got serious about electric autos that would demand doubling our power grid. We will run out of sites for wind & solar long before they supply 5% of market demand. IMHO

Here are some links in support; There is much more if you look for it….web.mit.edu/course/3/3s32/…/jamieson.html en.wikipedia.org/wiki/Electric_vehicle

This article is nearly 2 years old. What say you now about Google’s “trillion” dollar effort to bring fiber to the masses?http://googlefiberblog.blogspot.com/2014/02/exploring-new-cities-for-google-fiber.html?m=1

Thanks for the insight. Yes the Motley Fool video was entirely too long. What was this about needing things faster? Would love to get an update as reader above stated. 🙂

Really interesting reading the comments from about 2 years ago. All of the 3 stocks mentioned in this article are up approx. 75%,75%, and 90% when checking charts at a 2 year setting. Not to say they will stay this high for ever, but it is at least interesting to the nay-sayers.

Not very attractive now.

I just received this Motley Fool vid today. I enjoyed reading everyone’s insight on WHAT ARE THE 3?! Sad news for me was that I owned Discovery when it came out as an IPO. Since it dragged. I got rid of it a few months later. OUCH! Maybe I can get my In-laws will invest in these 3. Or maybe they already have. I believe it’s time for a fresh new 3 stocks!

this is old. I am sorry Travis……

uh no actually even older now its year 2015. i’ve now spent like two hours reading all this whatever it is and seeing the dates no ones really posted anyting since jan. 2015 so… I’m bored tired of reading about people owning stocks i don’t even understand stocks but now i know you people are hellla boring. well good lucks on your stocks hahahaha

Stocks are basically just part ownership of a company. You buy shares of the company (very very small percentage of the company) and as the company’s value goes up, so too does your stock’s value, and as it goes down the same is true.

Well jimbo, you are just a bit off base about stocks. You are correct that when you buy a stock (at least most stocks) you are becoming a voting shareholder of a company. But the price of your stock is not based on company value, it is based SOLELY on what other potential investors think it’s worth at any given moment. In other words, a stock is a derivative, just like a mutual fund, an ETF, a REIT, a bond, or any other financial vehicle. Except in an IPO you don’t buy stock shares from the company, you buy them from some other investors who want to sell them. Those sellers have their reasons for selling, just as you have your reasons for buying. Psychology is perhaps the most important tool in investing. Knowing the market means knowing the investors. The best way to make money on stocks to buy the ones where the demand for them increases over time. You have to make an educated guess as to which ones people will actually want in the future. If you mis-guess the investor psychology, you lose. In the case of the Motley Fool recommendations, these three stocks will only increase in value if the demand for them increases. Hmmm…. all this marketing buzz that has been generated – will it succeed in increasing demand for them? Congratulations, we are all part of the marketing effort!

uh no actually even older now its year 2015. i’ve now spent like two hours reading all this whatever it is and seeing the dates no ones really posted anyting since jan. 2015 so… I’m bored tired of reading about people owning stocks i don’t even understand stocks but now i know you people are hellla boring. well good lucks on your stocks hahahaha. that video was a joke this site is a joke you all just wasted your own time i know because i just waisted mine reading everyones garbage post dumb dumb dumb. go to work do your job being on this blog is pointless who really cares what happens to t.v . everyone seems to want to pay for it so let them pay for it. i’ll just go out side and use mcdonalds or starbucks wifi. stream some movies while using a v2o downloader and not only will i wathch the move i’ll also now own it for free no internet bill no tv bill no 4g bill no buying a dvd and recorder. nope just plain and simple piracy. buy that stock

Oh yes, you are “smarterthanmeduh” when you don’t understand what investing has to offer. You may be able to pirate, watch, and own any movies, shows, music, and games… and that is great. but investing has the potential to cause you to earn MONEY, not free junk. So if you invest wisely, even a 100$ starting account could become a fortune compared to your sorryA$$ sitting outside trying to get a free wifi signal. Then you could pay for it and actually contribute to the American market system instead of trying to sabotage it. People who pirate only make me slightly angry… people who are stupid AND are pirating make me furious. eff. yew.

Haha, talk about someone who completely missed the point!

Sitting outside Starbucks, leaching the free Wi-Fi and waiting for the Bernie Rally to start?

I came across this MF ad just today – I want my 15 minutes back! But I can see that this has been around for close to two years now. Did a quick check on DIS, SNI, andDISCA and more or less have doubled since first came out. Maybe I need to be on THIS website more often!!! I do love this site!

Well, Discovery is 50% down since beginning of August and hasn’t gained anything after this report was created!

Wow….I was bored to tears! He seems like a nice guy but when the timer went away on the video I should have known it was a bait and switch. Hey I don’t mind commercials but keep them short and to the point. This was just painful!

If you’d rather not watch the video and would just like to read the content when you follow one of these links to such a video, click Ctrl & W together (as if to close the window) (or apple W on a mac) and a screen will pop up and ask you if your want to leave or want to stay. Then choose to stay (click what ever button that defines that choice) and the video will be replaced with text of the video’s content instead of the video player. As fast as I read, these videos are like watching (and waiting for) a constipated dog taking a dump – it never seems to end. It’s why I only have a cat now – I never have to take a dog for a walk.

Motley Fool investment analyses are IMO above average. Motley Fool pitches are beyond agonizing. If there was ever a more productive way to drive potential investors AWAY from their product, Motley Fool hasn’t found it yet.

This idiot, actually expects us to believe , that in a few years there will be no more tv and that we will like it ? Seriously?! Give me an effing break , if tv were really going out the door people wouldn’t be spending so much money on making high tech movies and dvds etc. The next time this monkey wants to get people stirred up and believing something as stupid as this , he better target people who are severely challenged who have no ability to call BS when they see it . Sorry mister not everybody is as gullible and stupid as you would like them to be. Try again . NEXT !!!

I know a bit about this industry… I worked in it for many years..

Like I said, the video is so ridiculous I’ve followed it for years as people continue to watch it…

I get a motley fool newsletter… if they can be this idiotic and uninformed about something I know about, it makes me wonder if I should take anything they say seriously??

Ah, but it got your attention, no? That’s all they wanted. “The PC is dead!!” is another silly attention-getter that has been around for at least 15 years. PCs have had to give up market share to other devices, and that’s prob. the worst we can expect for TVs.

Look at the stock prices since this video was released in 2012.

Winterfawn you should change your name to Jane (Gratuitous SNL reference). He is talking about television as a platform, not the physical device.

So let have everyone list their Top 2 Choices and see what come out on TOP

Mesh networking is coming. These are the steps

Step 1) In your spare time develop and release open source free cell phone operating system and give it away. (Android)

Step 2) Map out and build database of nationwide wifi hotspots ( get sued for this one )

Step 3) Purchase core wifi/cellular systems manufacturer to own significant patents to modify wifi chips to broadcast a 10 watts. Also put USB port on most popular cable modem in America so it accept an external wifi device. (Motorola, get some heat from the Feds on this)

Step 4) Force Cisco to rerelease an open source model of their most popular wifi router by secretly funding BuffaloTech DD-WRT release.

Step 5) Develop and provide encrypted mesh protocols to be used in DD-WRT.

Step 6) put big shiny red button in Android app that is appealing to push.

Step 7) Discourage 100 million users from pushing that red button because the FCC has made large scale public Wifi networks illegal to operate because of pressure from the telecom lobby and Verizon. Also mention that as good citizens we should allow the NSA to skim and retain all our electronic communications as it should legal pas through AT&T and Verizon’s POP’s.

Step 8) Accidentally built the worlds largest fastest most secure redundant CPU sharing Data and storage sharing network.

Step 9) Compare Verizon network and it’s stock value to that of the pony express soon after the continental long line telegraph system was built.