Another year, another junior gold miner teased by Nick Hodge. It has a Groundhog Day kind of feel to it, since so many of these early-stage gold explorer stories sound the same, but this time he’s actually pitching a stock that I haven’t written much about.

Ready to dig in? Let’s go.

Hodge’s ad is for his Hodge Family Office newsletter (“on sale” for $999 for the first year, renews at ?, 60-day refund period), which is his “upgrade” service at Digest Publishing.

And he’s got a looooooong spiel, including some video of his site visit in Idaho and lots of talk about how gold is “rising” (which is not true, not at the moment, so perhaps he put that language together earlier in the year — though the ad is otherwise pretty up to date). But the easiest summary comes from the order form… here’s a little snippet:

“Drilling Into A 20-Bagger: Exposing the Potential of America’s Next Biggest Gold Discovery

“Once details of this historic gold discovery go public… this sub-$1.00 miner will begin a breathtaking ride.

“The kind not seen since Diamond Fields surged for 200,000% gains on its nickel discovery.

“And you have the unprecedented opportunity to buy in ahead of the crowd.

“Remember, I’m only privy to this mine’s real wealth because of my insider contacts…

“And my boots-on-the-ground visit to the mining site in Idaho…

“Few outside of a very well-connected group have even heard of this company.”

What else do we learn about this little gold miner? Well, it’s trading under a dollar… it’s trying to build a mine on the site of a past-producing mine in Idaho (at one time the largest gold mine in Idaho, no less), and he says the project has approval from the locals.

And when he gets into more detail, we learn that the property has about 16,000 acres, and that it might become one of the largest gold mines that’s not owned by the majors (Newmont and Barrick).

He also makes the odd point that he thinks this gold miner has “kept its real wealth a secret” and hasn’t reported all of its gold — he says that they talk about having four million ounces of gold in their project, but that “In reality — and you could only know this by visiting the site — it holds no less than 10 million gold ounces by my calculations.”

The site consists of five different deposits, identified over a span of 3.5 miles and to a depth of 2,000 feet, but Hodge also thinks more gold could be discovered along the strike, or beneath it.

There are also some big-money folks lining up for this project, apparently…

“billion-dollar hedge funds are betting big on this play!

“One made a $10 million bet in early 2022 — enough to own over 8% of the company.”

And much of Hodge’s argument rests on the possibility that once the mine is ready for construction, and they’ve identified more reserves, it could get bought out at a fat premium price… so he compares it to another buyout:

“Earlier this year, large gold miner B2Gold took out Oklo Resources for $62 million. Oklo had gold resources of just 669,000 ounces. So B2Gold paid just over $92 per ounce.

“At that rate, the ten million ounces I think this project has would be worth $926 million, making every share worth $10.65.

“That would make this a 2,030% winner.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“Other takeouts have come at an even higher premium. When Barrick bought out Randgold a few years ago it paid $240 per ounce.

“That would make this ground worth $2.4 billion, and shares of the company that own it worth over $27.50 — some 5,423% higher than they currently trade.”

So what’s the stock? This is, sez the Thinkolator, the junior mining explorer Revival Gold (RGV.V in Toronto, RVLGF OTC in the US), which is trying to develop a mine at the Beartrack-Arnett project, in northern Idaho, a site that was previously mined in the 1990s.

There are two considerations for this mining project, it appears… the near-term potential, which is that they might be able to start with a small mine that can pay for itself, and the long-term potential, which is that the small operating mine they’re trying to plan could help to finance the much larger mine that the big (though as yet unproven) potential deposit could support.

They shifted to this “phase one plan” to talk about a smaller-scale project a couple years ago, basically building a small mine to use the existing infrastructure and produce some of the more accessible ore, generating cash flow that might let them get through to the next phase of possibly building a larger mining operation.

They issued a preliminary economic assessment for this plan back in November of 2020, and it concluded that they could restart the mine with only $100 million in startup capital and then produce 72,000 ounces of gold a year for seven years… and that the net present value of that project, using a $1,550 gold price (we’re at $1,650 and falling now), should be $88 million.

That might seem somewhat appealing to investors today, if there’s any potential beyond that small mine, because the current market cap is just under $40 million… but do note that they use a laughably low 5% discount rate to get at that present value. If you used a 15% discount rate, for example, to take into account the risk of a mining project and the much higher inflation and interest rates we have now, the same numbers would probably put the net present value of that project at about $40 million, right where the company sits today. (If you’re not familiar with the calculation of net present value, which basically incorporates the cost of money or the opportunity cost for the time you’re waiting for that value to be realized, there’s a good primer on the concept here.)

And we need also to keep in mind that the net present value of the project, whatever it is, probably won’t be shared among the 87 million shares that currently exist… that share count is very likely to climb meaningfully, since It looks to me as though they’re close to running out of money and they still have years of drilling and prep work and permitting to do before they even consider trying to borrow construction capital. Which very likely means they’ll be selling more shares, starting very soon.

As of the last press release I saw from Revival Gold, the one saying their deal to sell a side project (the Diamond Mountain phosphate claims) fell through, presumably because their buyer didn’t get financing, they said that their cash balance was at C$3.3 million as of September 30. That’s down from the C$7.1 million on June 30 that they last disclosed, in their previous press release (about some more strong drilling results last month), and they are still drilling, or at least still planning on releasing more drilling results later this year, so they must still be spending money. That means they’re probably going to need to raise some cash very soon to keep the lights on and the drills spinning, presumably before the end of the year.

And this is not the greatest environment for raising money. Even with good drilling results, the fact that gold prices are falling probably means it will be tough for a junior miner to raise more cash if they have to go to the equity markets.

Who knows, maybe another institutional partner will step in, like the Donald Smith Value Fund did early this year (that’s the hedge fund which invested $10 million early this year, as Hodge teased, and that cash is likely to be gone by December… the fund bought about 8% of the company, but also got warrants (at 90 cents) to boost that ownership to about 12%… and the share price is currently below where it was when that deal was done in January).

Or maybe they’ve got phone calls out to all their investment newsletter and mining-media friends, perhaps including Nick Hodge (who I assume probably participated in their private placements a few years ago), offering them tours of the mine site and trying to get them to gin up interest in the company and give them a chance to raise money at better prices.

It’s a tough tightrope these junior miners have to walk, constantly raising money for the expensive and time-consuming work of exploration and permitting, making the right decisions about drilling and financing and longer-term plans, but also trying to keep their investors excited about projects that always take far, far longer and cost far more than anyone ever anticipated.

It’s really the potential large future mine and the possibility that the deposit has millions of ounces of gold that has Nick Hodge excited — though a bigger project would obviously cost a lot more to build, and probably take a lot longer to get permitted, and they haven’t even gotten to a pre-feasibility study for a smaller project, or booked any measured resources, let alone real reserves. That might change in the reasonably near future, they recently said that they’ve retained a new mining consultant to work on their pre-feasibility study, and that the technical work is underway… but also that it won’t be released until sometime in the middle of 2023. So for now, it’s just that preliminary economic analysis for the smaller “phase one” project that we have to rely on, plus a raft of press releases reassuring investors that their drilling continues to find high-grade seams of gold.

What about the comparables that Nick Hodge cites? That takeover of Randgold is not at all comparable — that was an acquisition of a pretty large and operating miner, with cash flow and multiple producing mines and lots of reserves.

But B2Gold’s acquisition of Oklo could be somewhat similar to a potential acquisition of Revival Gold, I suppose — Oklo had a large property in Mali, including a flagship property which had reported its mineral resources just a year earlier (Dandoko) as well as plenty of exploration potential both at that site and at other deposits. Their total mineral resource estimate was 528,000 ounces of measured and indicated gold, and 141,000 ounces of inferred gold, and there was also some synergy because B2Gold has operations nearby, and could use its existing mills for some of the production at Dandoko.

Sadly, however, Oklo didn’t quite get US$62 million — the acquisition was about 2/3 in shares, and B2Gold has lost about a third of its value since the announcement back in May, and it was done in Australian dollars, which have lost considerable value this year… but yes, the consideration ended up being somewhere close to that — I’d say more like $50 million at this point. Which is about $75 per ounce of resources.

Revival is not quite as far along in drilling and reporting resources as Oklo was, but they’re pretty close — as of early 2020 they reported a total of about 3 million ounces of indicated and inferred resources, and in May of this year they updated that to 4.05 million ounces, about half indicated and half inferred. None of their resources reach the level of being “measured” yet, so this is very early stage stuff.

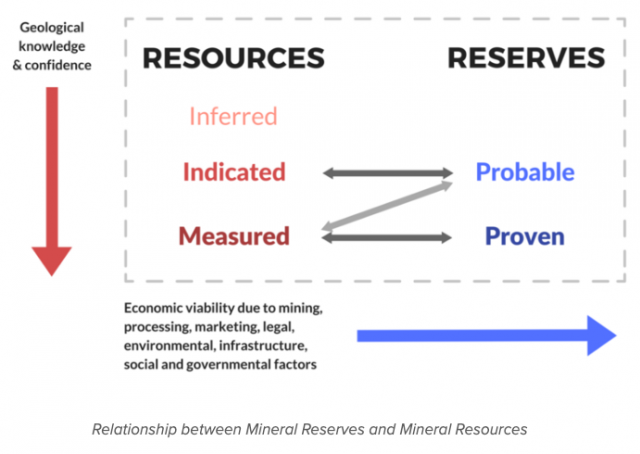

It’s very important to keep in mind that indicated and inferred resources are not at all the same as proven reserves. There’s a continuum of “quality” for minerals in the earth, based on how much drilling and analysis has been done — so an inferred resource is something that you think is probably there in something like a commercially viable quantity, based on initial drilling and some geological understanding of the area. Proven reserves, at the other end, are the result of a lot more drilling to more specifically define what’s underground, with something closer to certainty (though still a ways off — it’s still under ground, after all, and drilling can only show you so much), and proven reserves also come with an economic assessment — not just that the mineral is there, and you’re pretty sure how much is there, but that there’s also reason to believe that you can produce that mineral using defined mining methods and within economic parameters that make real world sense.

It takes time and a lot of drilling and geological analysis work to move from “we found gold” to “I think it’s this much gold” to “we’re really sure there’s at least this much gold” to, finally, “I can promise the bank that we’ll be able to produce this much gold at a profit and repay our construction loans.”

Here’s a useful chart that I lifted from New Pacific Metals that might help the visual learners…

So are those ounces in Idaho, along with the potential of Revival’s remaining property and the likelihood that they’ll find more gold as they continue drilling, worth more per ounce than the Oklo property in Mali? Less? That’s entirely a judgement call, and would include a lot of factors, including location and the exploration potential beyond those initial resource claims, as well as on the acquirer’s inside knowledge about what construction and operating costs might be if the mine ever gets built. But if Revival’s indicated and inferred mineral resource is worth as much to a buyer as Oklo’s measured and indicated and inferred resource, roughly $75/ounce of gold, then that would be about $300 million…. which is, obviously, vastly larger than the current market cap of Revival Gold, which is valued in the stock market at about $40 million.

Which is how you can fuel some excitement about a junior miner, even if you know that it’s probably many years from even deciding to build a mine, let alone actually getting it permitted and built. IF it works out well, there’s a path to creating a lot of value… but this is mining we’re talking about, so don’t get too far ahead of your skis. If you want to start to dig in on Revival Gold and the project it is trying to develop, their latest investor presentation is here.

The most comparable project in the neighborhood is probably the Stibnite project being developed by Perpetua Resources (PPTA), which used to be called Midas Gold, and which Nick Hodge has also pitched pretty aggressively over the past five years or so. Perpetual also sells itself on the notion that it is reviving an old mine in Idaho, will clean up the site of a past mine in the process, and could have a very high grade and large mine once it’s built.

Perpetua’s project is already much larger than the potential size Hodge sees at Revival, the Stibnite project has reported proven and probable mineral reserves of 4.8 million ounces of gold, and another 6.0 million ounces of measured and indicated resources, and they’re involved in back-and-forth with permitting and responding to local feedback about their mine plan right now, so they’re partway through the environmental reviews and the federal and state decisions they need to go in their favor. They still have many years to go, but Revival is years away from even beginning that process. Right now, Perpetua is valued at $114 million, so, for comparison’s sake, that’s about $25 per ounce of reserves, or $10 per ounce of total reserves and resources.

Is one of these projects more likely to be approved than the other? Maybe, I’m certainly no expert on the challenges of dealing with mine permitting in Idaho, and of the different parts of the state, but the two projects seem fairly similar to me… and Perpetua is dramatically further along. Partly thats because Perpetua’s Stibnite project often sat on mothballs for years at a time when gold prices were stagnant, but part of it is just the complexity and cost of exploration drilling and mine planning and federal and state permitting.

Perpetua’s Stibnite project released its pre-feasibility study in 2014, and its feasibility study in 2020 (the feasibility study is the stage where you try to become “bankable,” that’s generally the study the bankers will use to decide whether to finance the mine’s construction), and even the company’s own timeline indicates that they don’t expect final permitting approval for at least another year, with construction perhaps beginning by sometime in 2024, and commercial operations getting underway in 2027. And yes, if you’re thinking about that “have to sell more shares” bit, Perpetua has done a lot of that through the years — since they released their pre-feasibility study, in 2014, their share count has more than quadrupled.

And that’s for a deposit that has a large and economically viable reserve base, with pretty low expected operating costs, and includes a bonus in the form of a big antimony deposit. And has a strategic relationship with a huge hedge fund, as John Paulson’s Paulson & Co. have been major lenders to and investors in Perpetua Gold for at least six years (they are by far the largest shareholder now, they own about 40% of the company).

Though it’s also a different kind of narrative, because Perpetua is a lot closer to maybe making a construction decision, which means it’s “real” — and once something becomes a real potential business, not just an exciting gold discovery, investors often begin to fret more about the financing and the economics of the mine, getting less lusty about the leverage to gold and beginning to think about stuff like cash flow and earnings and construction overruns. One of the major challenges at Perpetua is that they’ve estimated it will cost about a billion dollars to build the Stibnite mine. Raising that kind of money right now sounds very daunting, with interest rates way up and gold prices way down, so sometimes a daydream of a small company doing exploratory drilling on a big discovery is more exciting. Revival won’t be digging a big pit before 2030, I would guess, so the hard stuff like financing and reserves is way off in the future, it will be years before they even begin to estimate how much the project will cost… but who knows, maybe they’ll move a little faster on their “phase one” project or otherwise get investors enthused (I may be too skeptical, but skepticism is a key survival trait of junior mining investors).

Perhaps Nick Hodge is correct in saying that a smaller deposit is easier to permit and move forward quietly, perhaps Revival’s Beartrack-Arnett project will represent less of an environmental or permitting challenge than Perpetua’s Stibnite project has… but a smaller deposit is also much harder to finance. A larger potential mine is always easier to justify to investors and financiers, so I don’t see any reason why Revival would “downplay” the size of their deposit… particularly because they need to raise money, like now, and reporting good drill results has often been the way that explorers get their share price up so they can sell more shares. They haven’t been at all shy about announcing their drilling results this year, or their larger estimated mineral resource.

I think the simple answer is probably the correct one here: at Revival Gold they just haven’t proved out the resources or the reserves yet, they’re still doing pretty early-stage drilling to turn inferred resources into measured resources, and they’ve hardly even begun the conversations about permitting and environmental impact, so developing Revival’s project, even if they begin small, is going to take lots of time and lots of money. That Phase One project could be justifiable, it’s got a short payback period and sounds like it should be profitable, at least based on the preliminary economic analysis of a couple years ago (maybe it will change with the pre-feasibility study next year), but it’s also not exactly a barnburner — even if it pays back the investment in three years, and generates a nice levered return for investors, it’s still quite small, and it still depends on someone ponying up $100 million for construction (sometimes that’s easy, sometimes it’s hard — a lot depends on what the markets and the gold price are doing at the moment when they need the money).

Maybe Revival Gold will get lucky, time it well, and be a popular gold explorer whenever gold prices jump higher again, providing an exciting surge for investors. The best results tend to come when a tiny junior miner reports great drilling results at just the time that people get lusty about gold again… but unless you know when we’ll see the next bull market for gold, that’s a bit of a crapshoot.

Given the very long time it will take to explore this property and move forward with development, even on a smaller scale, I’d guess that speculators are looking for either a rabid bull market in gold, or a takeover by a larger miner… and any longer-term investors, like John Paulson over at Perpetua Resources, who’s pushed for change but still probably hasn’t really made any money on that investment in the past six years, are just betting on the potential leverage of a gold miner, socking away a little exposure to the shiny stuff for a rainy day. Can’t say I blame them, there seem to be plenty of clouds in the sky, but long-term investing in junior mining stocks is tough to justify for most people.

You can get windfall returns from speculating on mining projects, for sure, and plenty of fortunes have been built on the dream of turning hills of rock into bars of gold, but it’s not usually fast or easy, and mining is generally a terrible and expensive business. Permitting is hard, financing is hard, operating mines is hard, even if you avoid the flooding problems or cost overruns or labor challenges that plague many projects, or the political unrest of so many mining jurisdictions (Idaho is pretty easy, relatively speaking, but permitting in the US is very slow), and once you battle your way through that… surprise! You don’t get to decide what the price of gold will be at the time you’re ready to sell it.

The investors who are attracted to small mining discoveries are often the same ones who are attracted to early-stage biotech projects — it’s fascinating stuff, you can quickly learn more than most people about these esoteric properties or projects and make yourself feel like a smart insider, but still, most biotech R&D projects fail at some point on the long timeline to approval and commercial sales… and most mineral discoveries are never mined. You have to either enjoy riding the speculative roller coaster, with a mind to jumping off at some point, or you have to have incredible patience and above-average skill at analyzing these individual projects and separating the winners from the losers. I’m lacking there, and in these sectors I know I’m likely to be buying shares from someone who knows the geology or the biology a lot better than I do… so I don’t tend to invest much in biotech or mining.

And I’ll continue to pass on this one, though, like Perpetua, there’s certainly a case to be made for optimism in valuing the potential of the property at Revival Gold. If you’d like to make the case or try to talk me into it, or have other junior miners you think are better situated, I’m sure we’d all be delighted to hear your take — the happy little comment box below awaits your contribution.

P.S. Does the name Revival Gold sound familiar? It has gotten the attention of newsletters a couple times in recent years — Frank Curzio touted it for one of his letters about three years ago, though I didn’t cover that one, and the only time I’ve written about it before was when Nick Hodge’s colleague Gerardo Del Real teased it as a big winner just as COVID was hitting, in March of 2020. The share price is still pretty close to where it was when those prior ads were running, at least in US$ terms — the stock had a little surge with gold prices rising, but gold has come back down and the stock has followed. Perpetua Resources, in case you’re curious, has been teased many times over the past half-dozen years and has generally been a worse performer than Revival — though it has also been more volatile, so it had both higher highs and, recently, lower lows as it reacted to spurts of investor attention and to shifting gold prices.

Let’s say you spend ten dollars a week on the lottery. This might be the same so long as you stop playing the lottery.

That is probably the sane way to think about these kinds of speculations — though in truth, of course, the lottery has much worse odds and much higher payouts for “winning”.

Travis, you help keep me sane. Thanks for all you do. Nice to know the facts instead of just the hype.

I agree with JustJohn, when he says “Travis, you help keep me sane. Thanks for all you do. Nice to know the facts instead of just the hype.”

Since we’re talking about GOLD: MAMA MIA, since my mother died about 10 years ago and left me a couple of ounces in bars, GOLD HAS GONE NOWHERE, OMG. — What happened to all the people telling dentists to save all their patients’ gold? — Would I carry my couple of oz gold bars for cashing out? — Maybe, to pay off a loan … — So, guys/gals, seeing how COIN got crushed in EVERY major market swoon, WHAT IS THE FUTURE FOR GOLD? — T.I.A. for your take 😉 — Have a good day, friends.

Yes, I have heard several times in my long lifetime that gold was going to be valued at the equivalent of $50,000 an ounce. Still waiting.

Travis, can you look into the stock that supposedly controls an ocean of oil in Texas. StreetAuthority is pushing it.

Will see what ads I have from them in the hopper — it could easily be a repeat, they had a similar pitch for “Rockefeller Riches” earlier this year that I covered here: https://www.stockgumshoe.com/reviews/takeover-trader/de-teased-street-authoritys-the-mother-of-all-oil-booms-and-1-sure-shot-play-for-rockefeller-riches/

Disclosures – I own shares of RVLGF and I’m a geologist. Their gold property is a pretty good one, but I’ve learned over the years that the only reserves are what you’ve already produced, no matter what the mineral commodity. They probably should have done a JV on the phosphate property with a fertilizer producing company. Until their approach changes RVLGF is just a speculation, a fairly good one among many. I think the return of gold loans would be good for the gold mining industry. The royalty companies are doing a variety of this, but financing though bank loans is a dead end. A couple of other items. Perpetua is a joke. I’ve seen their presentation. The project is a reclamation project. No real possibility of a payoff. Valuing gold in dollars is another joke. You can’t get the real thing for the spot price and you can’t get any gold from GLD.

mining in that part of idaho goes way back. It’s a very friendly mining state, the shares are cheap and i don’t mind throwing a few bucks at it. At least it’ll keep me abreast of idaho mining !