“My top international junior pick has just updated their reserves and resources numbers.

“Those numbers have nearly DOUBLED.

“They’re drilling right now; production is growing. And I’m expecting a big jump in production by year-end.

“But that’s not even the best part.

“This good news is merely the precursor – a set-up – for their BIG PLAY.

“Their Big Play comes from an incredibly profitable energy breakthrough which – if it’s as successful as I think it will be – could transform this company into the # 1 junior in the world.”

So … we see plenty of teases around these parts, but that’s a Tease. The #1 junior in the world? In a sector like junior oil stocks, where the boom and bust dynamics mean there are always a few 1,000% gainers floating around to justify all the hope we throw at the 99% losers, well, “#1” sounds unusually good.

The tease, by the way, is from Keith Schaefer, who is very much a story-driven oil guy — his Oil & Gas Investments Bulletin newsletter, which is still fairly young, seems to look at least as much at growing investor interest, big land holdings, and up-and-coming areas as it does at financial statements and reserve replenishment … at least, that’s the feeling I get from his ads.

And he’s been blanketing the e-waves lately with a pitch for his new favorite international oil stock, a company that has more than a million acres of land in what he refers to as maybe the “next Bakken”, a breakthrough oil area that will make us rich.

So, well, we want to know what it is. Right?

Let’s see how he hints and teases, and get some answers. Here’s a bit more from the intro:

“I’ve followed this company non-stop for 16 months. I’ve seen it go through its learning curve.

“And now I believe the Market is about to figure out what I’ve discovered…

“A huge resource play with the very real potential to become a world-class energy play… with an experienced management team that is aggressively (yet cautiously) taking all the right steps to create a major success for everyone involved….

“I’m expecting more news inside the next 2 weeks… information that could dramatically change things for this company.”

OK — so huge potential, something happening soon, doubling reserves, drilling, producing … what’s not to like? Well, let’s not get ahead of ourselves just yet — here are some more clues about our mysterious “#1 junior”:

“The Great Energy Breakthrough that ‘Saved’ America… Is Now Going Global

“Early Investors Are About To Profit From Its First Big Overseas Success….

“… this company – one of my big portfolio trades – has acquired a full 1 million acres of kerogen-rich lands.

“That’s a million acres – that are completely untapped.

“It is already one of the most profitable junior companies – in terms of profit per barrel – on any stock exchange.

“And it has become one of the most compelling ground-floor opportunities I have ever come across in my career.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“It operates in an area of the world few oil and gas companies have ever explored – until now.”

Huh? OK, here’s more from the ad on that kerogen bit:

“Kerogen, like conventional oil and natural gas, is formed undergroundby decomposing organic matter under heat and pressure.

“But it’s not a liquid or gas. It’s a waxy solid, similar in consistency to candle wax….

“When kerogen gets heated – and the deeper in the ground it’s buried – the hotter it gets. It’s then converted to oil and natural gas.

“Of course kerogen rarely exists in free form that you can just scoop out of the ground.

“Most of the world’s kerogen is bound up in what is most commonly known as shale oil.

“This isn’t society’s first go-round with shale, though…

“Pioneers learned how to cook shale in ovens they called retorts. This produced a black oil that was used to lubricate machinery and firearms.

“Settlers in Colorado found the same strange stone, and they also built retorts to manufacture the valuable oil.

“Today, the ability to extract large volumes of oil and gas from shale makes it…

“The Biggest Game Changer in Oil Production… In the Last 150 Years”

Yeah, we don’t hear much about kerogen in these parts — at least, not since the failed oil shale efforts in the Rocky Mountains and the Green River area got a fair amount of attention in the years after the OPEC oil embargo (and again in 2006-2007, when oil was on a wild ramp ride). Kerogen is, for our purposes, oil that’s embedded in a type of immature rock and that can be released only by heating the rock, which is what Shell and other folks tried to do with some of the US’s huge oil shale resources. But it’s not worth it if you have to dig up the Rocky Mountains and put the rocks in a microwave, as experiment after experiment has found.

Now, what has been a “game changer” and is worth it — at least economically — is shale oil. Unfortunately, the two terms are often used interchangeably and probably neither one is really accurate. The “good” shale oil is what they’re extracting from the Bakken in and around North Dakota, oil that’s light and sweet but is trapped in rock layers, and that can be released by horizontal drilling and hydraulic fracturing. That shale oil is fueling a massive surge in US oil production and increases in oil reserves, and may bring down oil prices in the future the same way that natural gas prices have been destroyed by the huge reserves of similarly trapped shale gas found in the Marcellus, Fayetteville and other shale formations.

So it seems to me that Schaefer, with this kerogen bit, is mixing the two up — which doesn’t inspire confidence, but hopefully it’s just a storytelling ploy and he’s really talking about a shale oil/horizontal drilling/fracking play overseas, not a pig-in-the-poke kerogen play that could require the kind of intensive and expensive processing (mining and heating the rock) that makes the Canadian oil sands look efficient and environmentally friendly.

But that said, we’ll move on — just note, in our parlance “oil shale” usually means the kerogen stuff that can’t really be efficiently turned into oil, “shale oil” means the good stuff that made North Dakota ranchers into millionaires.

Schaefer’s presentation seems to mix the two together, but he does at least note that the Bakken, Barnett, Marcellus, Cline, Eagle Ford etc. are the real “breakthrough” shale regions — and they have nothing to do with heating kerogen, those are all horizontal drilling/fracking plays. And he tells us, of course, that he’s found the next one. Here’s some more of the tease:

“Now a Major Shale Oil Deposit — One So Large, It Could Revolutionize the Energy Industry — Has Been Discovered Outside North America

“Most people don’t know anything about this country. It isn’t one of the top 10 oil-producing nations.

“Yet it is a politically stable nation – an ideal place for oil companies to do business and prosper.

“And I have the one company I think will prosper there the most – and be the next big yielder in my portfolio.

“As I said, this tiny energy company owns over 1 million acres of prime shale oil formations in this red-hot new play.

“For the moment, the company flies under Wall Street’s radar.

“Even better for investors, it’s a small cap company that I think is a great buy at today’s share price – in light of its leverage and growing production.”

OK, now that sounds pretty good — any guesses on the country? No? It’s OK, we’ll get there with a few more clues. We’ve seen shale pitches for “bringing Bakken technology to Country X” several times in the past, from Poland to China to Argentina, and I’m not aware of any companies actually making that breakthrough leap to be the next Continental Resources (CLR) just yet (CLR is a massive producer in the Bakken after placing a big early bet there) … but that doesn’t mean it won’t happen eventually.

So how can we identify this country and company that he’s teasing? Why, we root around in the clues for a while, of course … here’s some more:

“The company’s 1 million acres have gone largely unexplored. That’s despite great geology and numerous oil and gas seeps (springs that ooze oil and gas instead of water).

“The seeps have been traced to 2 stacked shale formations recognized as the source rocks for many of the oil and gas seeps.

“When you think of huge shale plays, keep in mind that the world’s largest, the Bakken, is only 12 to 20 meters thick.

“By comparison, just one of this company’s 2 stacked shale plays is a whopping 600 meters thick!”

I don’t know if those thickness comparisons have any point when it comes to production potential or not, but at least it’s a clue. Some more?

“It’s a unique, ground-floor opportunity to develop world-class shale oil production… in a democratic, politically stable region.

“And while this acreage is almost completely unexplored, geologists are convinced it has vast potential to produce oil and gas.

“Technical work on only 15% of the property suggests a total of 22.3 billion barrels of oil in place….

“… you normally produce 7% – 15% of the oil in a shale play.

“At just 2% (an ultra-conservative estimate) that’s 478 million barrels.

“That oil is worth at least $20 per barrel in the ground once it’s been discovered.

“That’s $9.5 billion in take-out value for the stock.

“I’ll confess—I don’t expect the company to be bought out for anything near that. Not even close. However –

“I Am Absolutely Convinced that if this Shale Play Produces Economic Oil — the Event Would Catapult the Stock Price”

OK, so some more clues — though we’ll also note that democracies and politically stable countries have not necessarily been the best oil producers, or the kindest to outside oil companies. Just saying.

And this is, we’re told, also one of those “secret” assets — where the company is fairly valued based on the other stuff that they own, stuff that everyone knows about, and you get the shale oil prospects “for free.” Here’s a bit on that:

“… there are an estimated 126 million barrels more recoverable oil in targets directly above the shale—based on a 9% recovery rate.

“You know what my favourite part of this shale play is, though?

“It’s FREE. That’s right – investors are getting it for free.

“That’s because, at year-end 2012, the company will be producing more than 2,000 barrels a day of very profitable oil.

“Only this oil is coming not from the shale play, but from a different play altogether.

“The company has a second big basin – a bonus to the huge shale play I’ve just told you about.

“This second play – far away from the first – has more than 150,000 net acres of highly profitable oil.

“And, like I said, they should finish the year delivering the market more than 2,000 barrels a day.

“The stock is fully valued just on that. That’s why I say the monster shale play is free.”

And the clues keep piling up, just in case you were getting bored:

“In play # 2, they’re now producing from 4 wells—and on a major growth curve.

“They have barely scratched the surface over here, and they already have more than 30 prospects or leads.

“The company is drilling quickly now to complete a total of 12 exploration wells in this basin this year.

“They plan to drill at least one a month through 2013, to grow production, cash flow, and reserves.

“And — this is a company that has the geology figured out — There are dozens, possibly hundreds, of potential drill locations here.

“The company’s wells initially flowed 600 to 1,100 barrels of oil a day.

“They’re hitting 80% of the time.”

Schaefer must have been paying attention in copywriting class — he almost never writes a two-sentence paragraph that might slow people down, they’re all quick-hits with no adjectives … it’s like reading a John Grisham novel. That’s a lesson I can’t seem to remember, I usually squeeze at least a couple sentences into each, well, sentence.

He then goes into lots of other clues about other picks he likes, which leads me to think that he’s still holding and touting DeeThree Exploration and Poseidon Concepts, both of which have done extremely well (though I don’t know what price he paid) … but for our international shale play that’s pretty much it — though he does add on that management owns 30% of the company, and that they’ve got positive cash flow and no debt, both of which are checkmarks in the “plus” column.

So who is he teasing?

Toss it all into the Mighty, Mighty Thinkolator and we learn that this is … New Zealand Energy (NZ in Canada, NZERF on the OTCQX in the US)

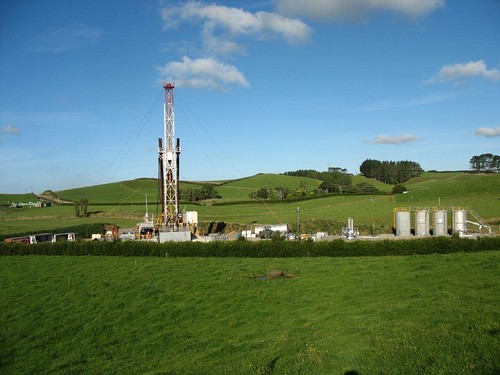

Which kind of spoils the second surprise, that this is a little exploration and production company operating in … New Zealand. They are indeed currently producing oil from several wells in the Taranaki Basin on the West Coast of the North Island, with a goal of getting that production up to 3,000 bopd of very light, sweet crude in the near future. They are also banking a fair amount of their future on their much larger exploration areas on the East Coast of that same island, which is where the shale idea comes into play.

Need to make sure? Well, the numbers match quite perfectly — including the 22.3 billion barrels of original oil in place (OOIP) for those shale territories, though even that 2% extraction number (478 million barrels, also a match) needs a fair amount of exploration before it could potentially becomes “discovered” and the potential becomes anything close to a reality.

Need to make sure? Well, the numbers match quite perfectly — including the 22.3 billion barrels of original oil in place (OOIP) for those shale territories, though even that 2% extraction number (478 million barrels, also a match) needs a fair amount of exploration before it could potentially becomes “discovered” and the potential becomes anything close to a reality.

And they are producing from four wells and did recently almost double reserves, though that news and the relatively less impressive fourth well haven’t given investors a lot of love for the stock in recent weeks — it’s a decent sized company still, with a market cap around $200 million, but the stock has fallen a good 20% as the last few announcements have come out this month (and is down even more harshly since the early drilling success inspired a huge ramp up in the share price early in the year, when it got over $3.50 a share after tripling in the first quarter). Right now it’s around $1.60.

The East Coast basins where they have almost two million acres (including both the permits they hold and those they’ve applied for) are long-known petroleum areas — oil seeps have kept people looking for oil there for over 100 years. The punchline is, dozens of wells have been drilled in this area (which isn’t that many, considering the vast size), but although some oil and gas have been found no one has ever found a commercial discovery (ie, big enough to invest in). They do compare the characteristics of these shale basins to the Bakken, but I certainly don’t have the expertise to tell you whether or not they’re just blowing smoke — I do know that it’s early days and they’ve done very little exploration or driling so far, and have not done any horizontal drilling or fracturing of the shale so I have no idea whether they’ll be able to produce oil from the East Coast shale areas.

They do seem to be doing well on the Taranaki stuff on the West Coast — they’ve acquired more permits and are drilling more aggressively now that they’ve found oil in four wells (they are producing from three of them, the other one had heavier oil and they had to decide whether to invest in lifting equipment to produce on that well), so they are indeed cash flow positive (in the last quarter, at least) and they could be profitable just on those conventional production permits if they keep finding more oil, as seems likely. Maybe not a good value, that depends on a lot of factors, but profitable is definitively good. And they recently bought a midstream production site and they’ve invested in pipelines, so they are looking at this (still the producing stuff in Taranaki that we’re talking about) as a sustainable project that they’re going to keep expanding. They do not have a huge number for reserves just yet, about 450 thousand barrels in the “proved and probable” category that would keep them going for only about six months at that hoped for 3,000 boe/day production rate if I’ve done my math correctly (I may not have, so do check) … so it’s not the reserves we’d be buying, it’s the anticipation that they will dramatically increase their reserves as they continue drilling these conventional wells — including eight wells being drilled between now and February.

If those wells are encouraging and both production and reserves go up, then the exploration project on the shale/kerogen area can be a bit more of a sideshow, waiting to see if they learn anything exciting next year but not counting on huge returns. I have no idea how the shale exploration might go. You can see how they line it up in their latest investor presentation here, and it certainly looks nice and shiny … but of course, it would. They’ve got a lot of cash on hand, they raised money earlier this year so they should be able to do their drilling and do at least some exploration even if their production doesn’t ramp up as dramatically as they hope.

And yes, New Zealand is a democratic society, with a government that is apparently at least somewhat amenable to oil and gas producers and interested in achieving energy independence — if the shale turns out to be an area that is amenable to fracking like the Bakken (they say they see good indications, but there’s been just very limited testing so far), I have no idea whether more wide-scale hydrofracking will be allowed. Oil companies in New Zealand have been using hydraulic fracturing for something like 30 years in the more established Taranaki region and other areas to boost production and, as in the US, it has picked up in the last decade … but it is apparently a continuing issue of political and environmental debate, particularly when it comes to groundwater contamination and earthquake risk. You can get a small taste of that from this student newspaper article, and by major newspaper opinions for and against fracking, just to get the flavor of the situation, but I have no idea what’s likely to happen in the future.

So there you have it — New Zealand Energy may well have stock price catalysts as their drilling results roll in, including possibly news within a few weeks as Schaefer teases either from the well that’s completing right now or from their seismic data interpretation, and they did just substantially increase their reserves numbers. It looks to me like you do need some more good drilling results and/or something positive to come out of the shale exploration next year to justify the stock climbing substantially from this point, but I might just be overly cautious since I haven’t spent much time exploring their reports. There are massive claims for the potential oil in place in their permit areas, both conventional and unconventional, but as far as I can tell it’s still a gamble as to whether or how that theoretical oil gets turned into reserves and extracted.

I’m sure Keith Schaefer knows far more about the company than I do, and I expect there are also plenty of Gumshoe readers who can better explain their exploration potential (please do, use the friendly little comment box below) … but I can at least tell you that I’m quite sure this is the pick he’s teasing. As to whether it’s a great idea for your portfolio … well, that’s your call. I do not own any of the stocks mentioned above, and won’t trade in any of them for at least three days.

Schaefer only disclosed a small part of the picture. Has he embellished?- No! Acvtivity will really start to accelerate after 1st of year. Other participants involved.

No Teasers can withstand the Power of the Mighty “Thinkolator” ..Salute

I can add that nze’s sister company, tag oil har manager to get Apache Corp to invest 100 musd on the East coast to get 50% of the land tag holds. So, apparantly, some bit oil company has som interests in this play. Nze can både it’s time and Wait for tag oils results. If they are good they Will probably get an even beter deal than tag oil.

Hello Travis & fellow GumShoe Readers:

Would you please recommend your favorite Oil/Gas focused newsletter? I have read the reviews on the site, but still lost. No clear favorite. I’m looking for something understandable to the average intellect, not too costly (Up to $200 year) and someone you respect for timely advice. I am an active investor, not a day trader. I really want to focus my learning curve on Energy, primarily Oil / N Gas. I love your newsletter, Thank-you!

Be blessed.

SW

Hi SW,

I suggest you check out Frank Curzio’s Small Cap Specialist and Porter Stansberry’s Investment Advisory. Both have suggested numerous oil and gas companies and have some great special reports.

Check them out!

PC

To:SW

Don’t believe in just taking and not giving back have found alot of good information here. Through my research Ive uncover the following, u can research there worth for yourself (RCON), Longreach Oil & Gas Limited (LOI.V), APIC Petroleum Corporation (MKVDF), APIC PETROLEUM CORPORATION (API.V).

Travis Johnson,

As I read the article above, I was absolutely positive you were talking about New Zealand, North Island.. I kept thinking the thinkolator was going to spit out Tag Oil, a Canadian Corporation, who controls several million acres there. They have been there for several years and most successful. Go to http://www.tagoil.com and view their website and historical success.. I was fortunate enough to get in on the ground floor of their venture and have enjoyed a profitable ride. Stock closed today at $7.27 Taoif. Pink Sheets. NZE is a neighbor to Tag Oil, there and most certainly, they share their geological info.. Tag Oil is debt free, with cash galore onhand.. Problem is, there is no dividends, only stock growth to generate profits.

“owns 7 million miles?” Big mistake.

What’d I miss? Who said who “owns 7 million miles”?

My thinking is shifting toward altenative energy, with the idea that petro will not be sustainable; I believe that petro significantly impacts global warming. Thus, am I right to see this investment as short term, appropriately? How would others want to play this? Is it a growth stock?

MAybe you better ask Obama LOL he can tell you just how unprofitable Aternative energy companies are. Enjoy the Petrol ride and forget green until private non gevernment backed companies can be profitable on their own.

The author is too casually dismissive of oil shale as a resource, and makes several mistakes in describing it and its relationship to the oil-bearing shale of formations like the Bakken. First, all oil source rocks contain kerogen, even the overcooked gas shales still have small amounts of kerogen left in them. Second, the terms “oil shale” and “shale oil” have been applied to the rock and the product of retorting that rock for more than 100 years. The Bakken and other oil-bearing shales need a different term, as well as one for the product (shale-hosted oil). Industry has begun to recognize this, and is calling it tight oil, but I have never seen oil that looked tight. They mean “tight-rock oil,” because the rock is not always shale, but this leaves a problem with the proper name for the rock formations. The efforts to produce oil from oil shale in this country are continuing, and did not end after the runup in oil price in 2008. Production is likely to start in 2013 or 2014 i Utah. Commercial technology exists, and is in operation in three countries with a slow steady ramp-up occurring over the last decade, and substantial increases likely through projects in the design and permitting stage in the U. S., Jordan, Estonia, China, and possibly soon several others. Oil shale will not ramp up any more rapidly that shale gas did in the 1990s, when virtually no one had ever heard of it. But it does not deserve the arrogant dismissal that reflects the author’s lack of knowledge more than actual facts.

Arrogant? Gumshoe? Surely you must be joking. Suggest you re-read his review above, then re-read your own overblown response, then look in the mirror to see what arrogant looks like.

OK I Say we all gang up on this obvious Troll and protect our beloved Travis Anyone with me ?

You clearly know your rocks, Dr. Boak, but you are a lousy interpreter of tone. “Arrogant dismissal”? Travis?

What I see is Travis saying “I might just be overly cautious since I haven’t spent much time exploring their reports” and “I’m sure Keith Schaefer knows far more about the company than I do, and I expect there are also plenty of Gumshoe readers who can better explain their exploration potential.” Hardly arrogant. You may want to pay a little closer attention to what someone is actually saying before you shoot out flames.

I’m glad you mentioned Dee three and Poseidon concepts. I just started to follow Kieth back in may of this year. when he 1st talked of dee three it was @ $ 4.23. I did my own research and liked what they were up to. Luckly I did not act on it right away , then in June it dropped down to $2.20, I got in @ $2.65, today it’s around $6.57, ya I’m happy with that , I’m even happier as RBC announced there target of it going to $8.50. Long story short on Poseiden, they pay a great divident .09 per share per month. bought them in June as well @ $12.21. today , they are near $15.75. So far with Kieth , I’ve done alright. I don’t know much about his last teezer, but as I always do , do my own research and make a decision, thx

Gumshoe’s aim is to come up with the name of stocks teased in newsletters. As a bonus he provides an informative and appreciated summary of the industry the stock is in. While I find your comments also informatiive, you have missed the point on what Gumshoe’s objective is. I also agree with others that the term “arrogant” is misplaced. Gumshoe is a jack of all trades, whose readers find a valuable source of information when researching stocks. He is not an expert in oil and gas as apparently you are. Who knows, if you follow his free articles, maybe you will also financially benefit from his depth of knowledge in numerous industries.

While I definitely failed to acknowledge that Gumshoe’s analysis of the problem he intended to solve was cautious and well documented, I stand by my criticism of his comments on oil shale, where he clearly has little more competence than the author he takes to task for mistaking the nature of the play he is selling, specifically, the following statements:

“Yeah, we don’t hear much about kerogen in these parts — at least, not since the failed oil shale efforts in the Rocky Mountains and the Green River area got a fair amount of attention in the years after the OPEC oil embargo (and again in 2006-2007, when oil was on a wild ramp ride).”

These efforts didn’t fail – they are still going on, and the author can’t have looked too hard at this issue if he doesn’t know this.

“But it’s not worth it if you have to dig up the Rocky Mountains and put the rocks in a microwave, as experiment after experiment has found.”

Once again, a distorted and ignorant picture of a resource and technology that he clearly does not understand.

“he’s really talking about a shale oil/horizontal drilling/fracking play overseas, not a pig-in-the-poke kerogen play that could require the kind of intensive and expensive processing (mining and heating the rock) that makes the Canadian oil sands look efficient and environmentally friendly.”

The author appears to have picked up the pseudoenvironmental opposition’s stock line about oil shale, again reflecting ignorance of the nature of oil shale production, and the science and technology behind it.

My objection is to launching into a series of gratuitously negative assertions about a resource the writer knows little nothing about, rather than simply making the distinction between oil shale on the one hand and oil-bearing shale formations like the Bakken on the other, and leaving it at that. Then his article would have consisted only of useful deductions and not claims made with no factual basis.

Arrogant is defined as, “Having or revealing an exaggerated sense of one’s own importance or abilities.” I did not engage is such exaggeration, as I made no comments on the main portion of his article. It is clear I should have emphasized that I was only commenting on one part of the article, so that the readers who replied would have understood that. Were it not for the fact that the rest of the article is fairly straightforward and simple logic, I would be led to have concerns about the quality of the analysis of a writer who was so willing to engage in these unsupported assertions.

DR. JEREMY (JERRY) BOAK

Contact Information

Associate Research Professor

Department of Geology and Geological Engineering

Colorado School of Mines

1516 Illinois Street

Golden, CO 80401

USA

Thanks for your insight, Dr. Boak. But, what you refer to as “arrogance” can just as easily be a far different writing style to a completely different audience, than yours. Travis seeks to keep a light, humorous and informative writing style to oftentimes boring, mundane subjects. Much different than academia’s dry, informative style. Most of us Gumshoe readers would get much more information out of Travis’ explanation of a “kerogan play” than an academic rendition of what constitutes the proper geological makeup of kerogan. Actually, you are both right on the oil shale industry in Western Colorado. Sure, it’s holding on by the skin of it’s teeth, but for all practical purposes, until oil gets to $150 plus per barrel, it’ll just be a speculative operation.

So, to set the record straight, neither one of you are wrong or arrogant. Just different and writing to a different audience. Which explains the different perspectives.

Available published estimates are that oil shale could produce an economic return at $50-60/barrel, given technical success. Others at the technical meeting I chair annually give estimates in the range $40-80. So you are also wrong about Western oil shale. And the Estonians are already producing from a twin of the retort they plan to build in Utah. I did not go into the details of the definition of kerogen, although I think most readers of this column could probably understand the difference between chemical reactions and melting. His comments may have been light-hearted, but they were still wrong, and disparaging of an active industry, and yet asserted as fact. Not only that, they were not really useful with respect to the item being discussed. They therefore certainly could not be considered as informative. I actually don’t typically write in academic style, although I can. I just try to get facts right.

OK I have a response for you. YOUR arrogant self serving personal appreciation of yourself is not shared by me. I didn’t get therough the first paragraph of you ever so pompous toned response. Perhaps if we are all too mundane for you perhaps there is another venue where you will be more comfortable chatting with your ever so educated peers. Right now you have just pissed a lot of us off. We happen to adore Travis and I for one am not in the least impressed with you Deborah

So what do you have to add re: prospects for New Zealand Oil?

As far as I can tell, the writer gets it right as long as he doesn’t stray from his limited technical knowledge. He highlights the parts of the prospect where there is risk – small number of tests, potential for environmental opposition, etc. These do require careful consideration before investing, and it doesn’t sound like the article he reviews provides that level of detail. So, while there is every reason to believe that a shale play could develop in New Zealand, it is seriously speculative at this time.

As I pointed out in one of my replies, most of the column appeared to be very reasonable. It was only when he indulged in remarkably strong negative comments beyond his knowledge of the subject, that I found him to be overconfident. However, I did wonder, if he is willing to stray so far beyond what he knows, are there other conclusions of his that are equally suspect?

Can you please just simply go away? We are ordinary folks here who like our homey down to earth friend.

Dr. Boak:

The Estonians may be producing oil from oil shale via retorting, but they are also producing a environmental nightmare with retorted tailings covering large areas and the retorted tailings are difficult to reclaim. Retorted oil shale produces an expanded shale product tha occupies 50% more volume than the mined shale. In addition, the spent, expanded oil shale is easily leached of all sorts of toxic metals including As. Some of the metals may be worth recovering such as Mo, u, V, Ni, and Zn.

I am a CSM MS graduate in Economic Geology, 1984, and in 1984 my project under Dr. Stermol (Mineral Economics professor) was to do a DCFROR analysis of an oil shale project on the West Slope of Colorado using the retort process. My conclusion at the time was that it would take $40-45/barrel oil to make the project economic. Since that time, general inflation is about 260% and inflation in mining costs has been at least in the 300-400% range if not more. Maybe the costs are lower for “in-place” retorting but there are still the problems with regard to the eaching heavy metals. However, cost estimates in the mining industry in recent years, at least for hard rock mines, have been notoriously unreiable as for example, ABX’s Pacua Lama project in Chile (capital costs have nearly doubled from original costs estimates), the Galore Creek project (Teck-Nova Gold)- shelved fo the time being), and the proposed super pit at Olympic Dam (shelfed for the time being due to rapidly rising capital costs). Cost estimate from a bunch of promoters and pumpers are not to be trusted.

The volume myth has long been put forward. The volume increase is simply the volume change between solid and crushed rock. The Estonians are trying to clean up the mess left by the Russians, who did not much care what they did to the environment. Estonia, as a member of the European Union meets standards as rigorous as ours. Leaching experiments by the USGS show that spent shale is not hazardous. Cost estimates were conducted by DOE, not by “promoters,” and for a variety of production processes. If the estimates were mistaken, only the investors will lose, as the project will not be subsidized. If other alternative energy sources were judged by the data of 1984, they too would suffer from the same negative comparisons. Perhaps the commenter would like to come back to campus for the next Oil Shale Symposium and find out what is new in oil shale development.

Try telling all the diseased/dying people in PA Shale areas it’s not dangerous. I probably know less than anyone commenting here on Shale economics: All I DO know, is oil companies do not pick up the tab for the damage they cause-now they’re branching out into Water Plays-since their poisoning off billions of acre feet increases the values exponentially. I live in NM-we depend on oil as >1/3 of our revenues come from our fields my family works in-all dangerous to their health-but they do it for the dollar. We had leaking tanks-Texaco, Shell, and many others-here in NM. We paid with our diminished lives for these Arrogant, above-the-law Companies’ crimes with our pocketbooks to clean up their “Superfund” sites, and we continue to pay for it decades later with poisoned water-you name the poison, it’s in our once pristine aquifers-while these companies bank billions each, year in, year out. Are you seriously going to claim they couldn’t make sickening profits if they ran cleaner operations? I refuse to invest in our killers…their time is over-Tesla/Keshe/HHO tech is available RIGHT NOW-but inventors are literally in the cross hairs of these wicked companies who don’t give two *hits about our world, our water, our soil, our people, since they think, following the Georgia Guidestones, they’ll be part of the 500,000 people left after their “culling” of all of us undesirables. We, The People, and our Revolution have a huge surprise for all of them.

Even the EPA concluded the perceived problems in Dimmock PA were not caused by hydraulic fracturing. But this comment refers to development of shale gas. Oil shale development does not necessarily even require hydraulic fracturing (although ExxomMobil’s approach will involve some fracturing), and Shell has already performed experiments indicating that they can clean up their underground retort after completion of production. I agree that practices decades ago were not the best, and that there continue to be environmental issues that must be raised and dealt with. I have never endorsed unregulated development, having spent a number of years trying to clean up the residue of past mistakes.

Man this guy loves to hear hin=mself speak guess his wife [I doubt he has one} keeps his mouth shut at home.

My wife appreciates factual information, by which you are not impressed. Evidently, it is more important to put people down than to engage in legitimate argumentation. I just put out factual responses to the misrepresentations I found here, not because I like to hear myself talk (or write), but because I think trashing things to make yourself sound knowledgeable is not cool. I liked most of what Travis wrote about things he knew about, but it bugs me to hear a subject I actually work on so stupidly misrepresented for no real purpose. It is not so much about thinking highly of myself, but of being really annoyed by self-righteous junk. And one of the commenters on this article actually asked me for more information. A lot of folks from all walks of like appreciate the information I present in a lot of different forums.

How can I find the schedule for the next Oil Shale Symposium?

Generally, if you Google Oil Shale Symposium you will find us. However, there will be an oil shale symposium in June in Tallinn, Estonia, so that is what you will likely find along with our website for the one that just finished in October. The next Symposium in Golden will be next October 14-16, with a field trip the 17-18th. I would be happy to add you to our email distribution if you send me contact information at jboak@mines.edu.

Jeremy Boak, Director

Center for Oil Shale Technology and Research

Colorado School of Mines

Golden CO 80401

The East coast doesn’t have a history of drilling – the major problem will be getting the drilling permits approved by all the different parties involved – my understanding from a local source is each permit will take ages and for fracking hundreds of permits are required. This will take years before any progress will be seen.

Or until they vote the Obama progressive Socialist liberals crew out

Alas, Deborah, you lost the election!

Right on, Deborah! On all counts above!

Well just to follow up on the original tout, looks like NZ is in trouble. They can’t hit their production targets due to steep decline rates and are low on cash. Stock has dipped below $1 in recent days after being in the $3’s earlier in 2012. Talk is Tag Oil might buy them out cheap.

This has been one of the most interesting (and entertaining) discussions I seen for quite awhile. The last comment from Bill, brings it full circle.

I applaud Travis for not responding to the bickering and negative comments. Please keep on doing the great job you are doing and continue to allow the free flow of comments from professionals and non-professionals. Makes for an interesting forum. We all have to sort out the facts from the fiction. I think they call it “due diligence”. 🙂

@RAN

Do you have current ticker please for : Longreach Oil & Gas Limited (LOI.V), APIC Petroleum Corporation (MKVDF), APIC PETROLEUM CORPORATION (API.V).

LGO- http://www.longreachoil.com/

http://www.fasken.com/longreach-oil–gas-limited-completes-arrangement-with-apic-petroleum-corporation/