The first version of this article was originally published on July 16, 2018, but questions continue to pile in and new ads this week indicate that it’s still being pitched as a “one stock retirement plan” … so today it gets a full update. The ad has gone through some relatively minor changes over the past five years, changing the “catalyst” event and testing out new headlines, and the date for the latest version is now noted as January 2022, but I’ve updated this article as of August, 2023.

Alexander Green at the Oxford Club has (another) ad out for his “single stock retirement plan” that’s sending a ton of questions our way — and you can see why. He’s promoting this one stock as being able to deliver a “multimillion-dollar retirement”, and there are obviously huge numbers of us holding out hope that there’s a way to “save” the retirement we know we’re not financially prepared for.

The latest email introducing the ad is trying to catch a piece of the AI wave, even though the ad itself hasn’t been updated — this is what that email says:

“This is what is so interesting about this stock…

“The company is seeing surging sales on the technology needed to run powerful language models like ChatGPT.

“The Chairman of the company says ‘More and more people are using ChatGPT. We expect that in the second half of this year there may be a three digit increase.’

“But that is just a tiny fraction of what this secret company is doing…

“Which is why this stock picking legend went on stage to talk about it, while its still less than $5.”

And in a different email:

“We have uncovered perhaps the most unusual AI stock we’ve ever seen.

“It’s expected to see massive revenue this year – $215 billion.

“The company holds over 29,000 patents in the U.S.

“It pays an enormous dividend.

“And yet…

“It’s ultra-cheap – less than $5.”

We’ll get into that (limited) ChatGPT connection in a minute, but first let’s run through the ad — they’ve called it a “$5 stock” and a “$4 stock” pretty much interchangeably over the years, trying to roughly match reality, but the ad itself still says $4 these days.

Here’s a little taste:

“I’m going to show you how a modest investment in a single $4 stock could generate a multimillion-dollar dream retirement in the coming years.

“I call it the ‘Single-Stock Retirement Plan.’

“Some might find the idea of retiring on one stock outlandish, yet many thousands of Americans have already done it.

“In fact, as you’re about to see, the 20 wealthiest men and women in America today made their fortunes thanks largely to a single stock.”

And he says that if you’re going to retire on one stock like those wealthy men and women did (though they mostly built businesses, they didn’t invest passively in one stock), Green says it has to be “the perfect stock.”

"reveal" emails? If not,

just click here...

He’s even got a checklist for what “perfect” looks like when you’re seeking this “dream stock” for a one-stock retirement… which is when the clues start to drop in about what stock he’s pitching:

“Leader in cutting-edge technology….

“products used by billions of customers…

“profit margins protected [patents, trademarks, etc.]…

“hundreds of billions of dollars in future sales and profits… contractually guaranteed…

“pay an enormous dividend.”

And he says this “perfect” stock should have catalysts — upcoming announcements that could drive the share price — and that the “one key element” is that the stock must be “undiscovered.” And that it should “trade for a just a few dollars a share.”

The per share business is silly, of course, but investors do get hung up on the idea of paying a low per-share price as a prerequisite for huge future gains. Different countries and different eras have different expectations for “per share” pricing — some large Australian companies trade at what we would think of in the US as “penny stock” prices, for example, and it used to be that most large US companies would aggressively manage their share price, using stock splits, to keep it in the $40-100 range. The market cap and the valuation of the company are what matters most, the price per share is mostly irrelevant.

But anwyay, that’s all a lead-up to this stock that Alexander Green is teasing… what other clues do we get? From the ad:

“I only recently uncovered it.

“And if you move quickly – before an upcoming announcement set for August 20 – this $3 stock could hand you the kind of carefree retirement most people only dream about.”

And then some specifics…

“The company has inked deals with Cisco, Microsoft, Intel, Sharp, IBM, Hewlett Packard, Nintendo, Sony, Nokia and Apple…

“In total, I expect it to receive more than $35.3 BILLION from these partnerships alone….

“According to data from Intellectual Property Watchdog, the firm has quietly amassed one of the largest tech patent libraries of any company in the world.

It has 36,241 patents inside the United States and 108,749 globally.

You can see why the world’s most famed tech companies are all signing blockbuster deals with this little-known firm trading for $4.”

And it sounds like this is not a small company, despite that $3 share price…

“… revenue hit a new record last year and is expected to surge even more in the year ahead.

And I expect the company to hit at least $215 billion in annual sales this year.

“The company pays a big dividend too… 189% bigger than the S&P 500 average.”

I know, I’m still keeping that secret (don’t worry, the answer is coming in a few paragraphs), but the update is that the dividend is still above average, though not as dramatically so, as it was cut in 2019 and only recently was raised to recover to close to that level. The current trailing revenue is just a whisker under $220 billion now, so the average revenue growth rate over the past five years is now down to about 5%.

Why is this stock “unknown?” Green says it “does not trade in a normal way” and it’s not on a US exchange… and, far more mysteriously, that it “literally trades under a secret name.”

So that’s enough to get our answer, I bet, but let’s throw a couple other clues into the Thinkolator…

“”A major multibillion-dollar deal that involves both Apple and Donald Trump is about to bring this secret company into the mainstream….”

That was the spiel back in 2018. By 2020, it had morphed a bit to add some specifics about this company’s US presence, as they were building some assembly plants (though they never really followed through on the big promised factory they were promising in Wisconsin to woo President Trump, that project shrunk dramatically).

And by last year, with this new ad dated January 2022, Alex Green had shifted so that the catalyst is now the Apple Car — here’s how he puts it:

“Nothing is as long-awaited as the Apple Car, which the company has secretly been working on under the title “Project Titan” for many years now.

“But here’s what makes this a big opportunity for the $4 stock I’m telling you about.

“Apple plans to design these cars, but then work with other companies to actually produce them.

“Bloomberg has called Apple’s EV the “Ultimate Prize” for the company that partners with Apple on it… because we are talking about the potential for billions of dollars in orders.

“And it looks like the $4 stock I’m telling you about today might just be the company to do it.

“Remember, this $4 stock already does billions of dollars in business with Apple on an annual basis.

“They are big-time partners.

“There is a lot of trust there.

“And this next step in their partnership… the possibility of this company landing the contract to actually build Apple cars… is as tantalizing as any stock catalyst I’ve seen in years.”

Any other clues?

“… the $4 stock I’m talking about had very humble beginnings.

“It was started by the blue-collar son of a career police officer….

“… he scrounged together $7,500 in seed money and went to work.

“He founded a tech company, but a very different kind…

“He realized that he probably couldn’t compete directly with the Apple, Amazon, Samsung and Google of the world.

“But if he could quietly do business with these tech giants, he just might turn his own venture into a successful company.”

He started out building low-tech computer hardware — stuff like the chassis for a desktop computer — and then aggressively expanded to build and provide components for all kinds of tech products. Green cites a few recent contract examples:

“His company has signed an agreement to build hundreds of thousands of devices for Amazon’s Fire TV streaming line.

“It also recently announced that it will be manufacturing Google’s flagship Pixel 6 phone in a partnership that includes Samsung as well.

“It has a deal in place to build GameCubes and Switches for Nintendo.

“It builds PlayStation 4s for Sony.

“It has a deal with Intel to build CPUs and computer cooling systems..”

And a dozen others, components for Amazon and Nokia and Acer and Nintendo and Apple. All those clues are essentially the same as they were four years ago, with minor updates (the next Google Pixel phone will be the Pixel 8, just to note that they’re a couple years out of date on that clue now).

So who is it?

This is, as several readers have already figured out and as Alex has been teasing in very similar ads for almost five years now, the Taiwanese company Foxconn, known for playing a major role in assembling Apple’s iPhones but also a big supplier to most of the world’s gadget makers. Foxconn is the world’s largest contract manufacturer and one of the largest private employers in China (if not the largest), and is one of the largest tech companies in the world (at least on a revenue basis).

And the “secret name?” Foxconn is the more widely-known name of the company, adopted when they were trying to get more international sales around 1980, and its the name you’ll see most articles use (as when they discuss the massive “Foxconn City” in Shenzhen, which has more than 200,000 workers), but the actual name under which it was founded (in 1974) is Hon Hai Precision Industry, and it’s still listed under that name in Taiwan. You can see the company’s own description of itself on their website here.

So yes, I suppose it’s kinda “secret” that Foxconn, the contract manufacturer that most tech investors have heard of, is actually Hon Hai — though certainly all of the institutional investors who own the lion’s share of this large cap stock are obviously aware.

And yes, it’s technically a $3-4ish stock, though that requires some currency translation — it trades in Taiwan at ticker 2317, and was recently priced at T$110 in New Taiwan Dollars (it was T$82.80 when we first covered the stock in 2018), which in US$ would be $3.65 today (the exchange rate has fluctuated over the years, but hasn’t changed all that dramatically).

It’s not particularly difficult to trade the stock in the US — there is an ADR representing the Taiwanese shares for US investors, it trades OTC at HNHPF (sometimes has been HNHPD, when it’s trading ex dividend), with each US OTC share equaling two shares in Taiwan. There are similar depository receipts trading in London at HHPD, also representing two Taiwanese shares each. The overwhelming majority of trading volume is usually in Taiwan, as you might imagine, so that’s where the “fair” price is set, but the London and NY trading tends to be very close to that price most of the time, despite the lower volume.

So if you want to buy in the US, technically you’re paying $7 or so per ADR today (or ~$6 back in 2018)… but each ADR represents two shares, so I suppose you can say it’s “secretly” a $3 or $4 stock.

All that mystery and intrigue is beside the point, though — the question is, do you want to own a piece of this gigantic electronics manufacturing company? Here’s what I can tell you about it:

It’s a big company, the market cap is just under US$50 billion… so it’s not likely to rise 1,000% over the next decade, and it’s not a small cap rising star, even though the share price looks fairly low to those of us who are accustomed to US tech companies who let their per-share prices rise into the thousands sometimes. Hon Hai is the second largest stock in Taiwan, trailing only the massive Taiwan Semiconductor (TSM).

Hon Hai/Foxconn has usually been priced at a steep discount to the broader market, and has underperformed the broader market for a very long time. The shares trade at about 12X trailing earnings and 1X book value right now, with a price/sales of only 0.25, and the dividend is very high — it’s 5% on a trailing basis now, though the payout varies pretty widely (they pay out only once per year, in August).

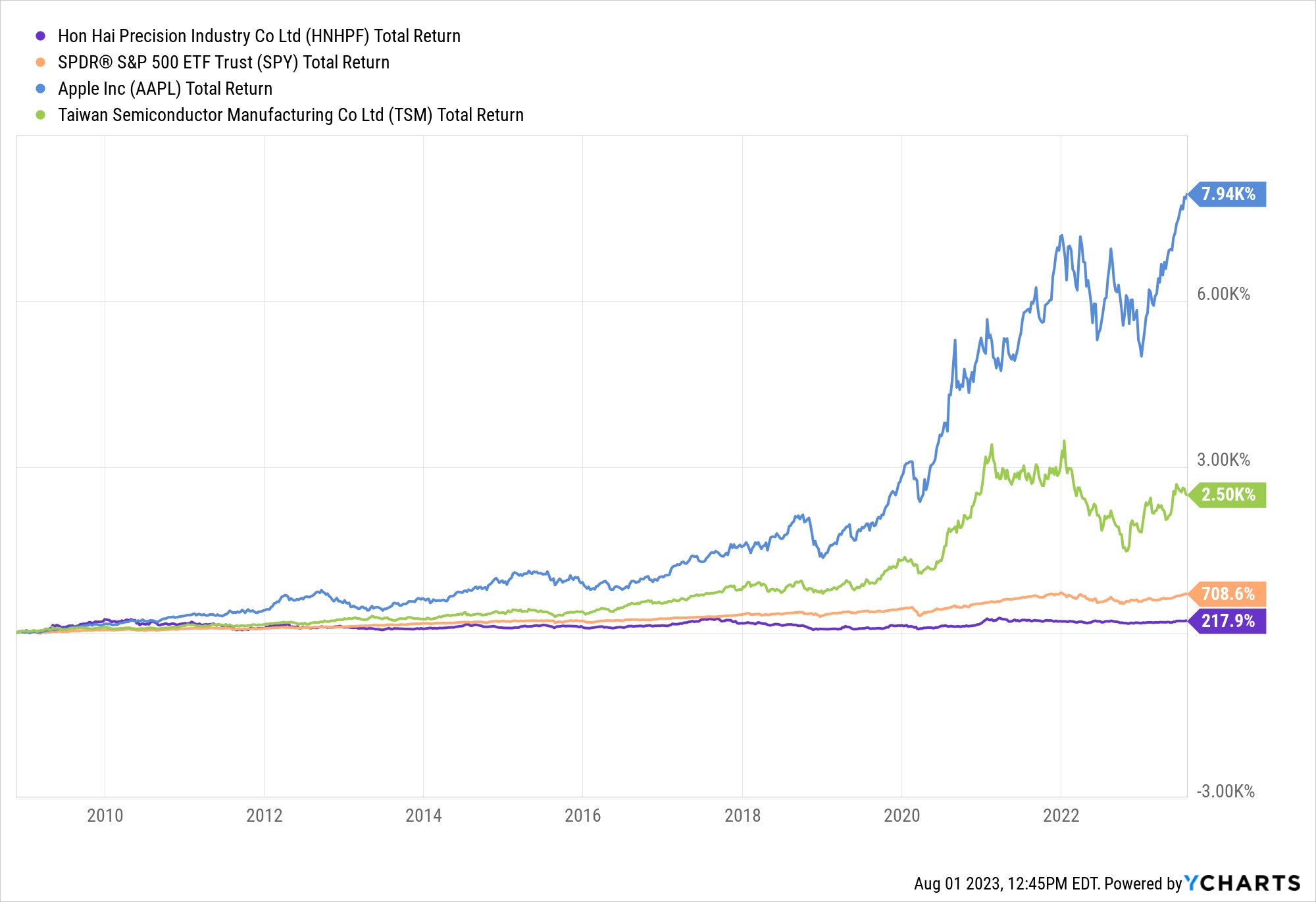

That relatively high dividend hasn’t helped the stock much, I’m afraid, it has almost always traded at pretty close to that valuation (the PE has ranged from 8-12 over the past decade), and has not been able to generate any meaningful share price growth for a long time. Even if you bought at close to the bottom of the market (for Hon Hai, at least) in November of 2008, you would have gains of only 200% over 15 years, including dividends… far short of the 700%+ return of the S&P 500 over that time. And almost 8,000% for Apple, Foxconn’s most important customer, or 2,500% for Taiwan Semiconductor (TSM). Here’s what that looks like on a chart, for the visual learners among you — that’s Hon Hai in purple at the bottom, and the S&P 500 in orange:

In case you’re curious, here’s that same chart for just the five years or so since the Oxford Club folks started pitching this as a “single stock retirement plan” — Hon Hai (in purple) is now trailing the broader market’s returns (orange) by “only” about 45 percentage points at the moment, with still big gaps to the performance of TSM and AAPL:

Which does serve, at least, as a helpful start to a thought exercise about who profits from hit products — is it the designers, the developers, or the companies who sell them parts and assemble the actual gadgets? Lots of things go into that, and there are plenty of growing and profitable component makers, and Foxconn has certainly made a profit most of the time over the years, but the two things that seem to me have the most impact on compounding long-term growth in the sector are sustainable brands and some measure of uniqueness.

Suppliers can do very well when their product or chip or whatever is better than the competition, but they also have to keep that edge… or make the component an in-demand brand or a near monopoly, as Intel did 40 years ago with their “Intel Inside” branding campaigns for chips and their tight partnership with Microsoft.

That’s what I’d look for when researching Foxconn… where do they have the opportunity to become more than an anonymous assembler? What’s keeping them from having to compete on price? Perhaps the relatively low valuation is a buying opportunity — but the valuation has always been relatively low, and is actually on the high side right now, historically speaking… and Foxconn shareholders have failed to really benefit from sales growth or new businesses or booming iPhone sales for a very long time, trade war or no trade war, COVID or no COVID.

That leads me to think there are some structural problems behind their relatively weak performance. Is that going to change if they get the contract to assemble an Apple Car? The closest thing we have to an “outsourcing manufacturer” for automobiles in the public markets right now is Magna International (MGA), and that stock also trades at about 12X forward earnings, so it’s not like investors are habitually lusting after these kinds of opportunities.

The stock does also carry some political and regulatory risk, or at least “headline risk” because of the frequent complaints and lawsuits about worker treatment at its many gigantic factories around the world. We all remember the stories about suicides by Apple iPhone workers several years ago, and those were mostly Foxconn stories about the pressure, secrecy, long working hours and employee stress in Shenzhen, but similar smaller-scale stories seem to pop up with some frequency.

Foxconn gets lumped in as the “iPhone maker” by most investors, so the share price tends to react to the iPhone cycle as predictions of huge sales volume send the stock climbing and slower sales, like we’ve seen recently, help to pressure the stock… the company is obviously far more than “just” Apple’s main manufacturing partner, though I don’t know if that will help to smooth things or create a real growth trend for the stock.

They’ve been aggressively expanding into new businesses and buying up brands and technologies for a long time… and yet, adding more second-tier brands and low-margin businesses in very competitive sectors hasn’t really given them better profitability. My impression is that the pressure of the low-margin contract manufacturing business, where companies like Apple push them to get costs lower and lower each year, seems to have kept them from showing any real sustainable earnings growth on the back of the growth in the business… so if Alexander Green ends up being right about this being a “one stock retirement” idea, it will likely be because Foxconn starts to get a little more leverage over the actual brands whose products they make, giving them a chance to increase margins… or because they finally move up the “value added” chain a bit, as they’ve been trying to do with their push into the automotive business. I see no sign of that happening in any real way over the five years that Green has been pitching this as the “one stock retirement” idea — their gross margins are still about 6% and their net profit margin about 2%, pretty much the same as they were in 2018.

And that massive US investment? It hasn’t really panned out. The centerpiece of that plan was a big display factory in Wisconsin that Foxconn agreed to build, in high-profile handshake ceremonies with then-President Trump, with promises of 13,000 new jobs and a renaissance in US high-tech manufacturing, and that plan seemed pretty snakebitten from the beginning. There is still a Wisconsin project for Foxconn underway, but it’s much smaller now, with hopes for maybe 1,500 jobs (there’s an interesting story here about how it all went wrong, if you’re curious). Maybe the latest push to “onshore” more technology manufacturing will mean yet more incentives to lure Foxconn to build facilities elsewhere in the US, we’ll see, but so far it’s not a meaningful factor for Foxconn’s earnings. What was touted as a $10 billion investment in factories by Foxconn was downgraded to an investment commitment of about $672 million in 2021.

More recently, Foxconn has signaled that they plan to enter the electric vehicle business, competing with longtime auto industry outsourcers like Magna International (MGA). The highest-profile part of that was purchasing the former GM plant in Lordstown, Ohio that Lordstown Motors had previously bought for its electric pickup truck project — it’s essentially an outsourcing deal, Foxconn is buying the factory and will be contract-manufacturing the pickup truck for Lordstown Motors, and hoping to also manufacture electric vehicles for other companies who don’t have the manufacturing expertise. It sounded like a desperate ploy from an EV maker who had gotten in over its head, and Foxconn, unlike Lordstown, does have the resources to invest in building up the plant. Who knows, maybe they’ll be able to translate their skills to this new industry and get a new avenue for growth.

There is some potential for slightly better margins in the auto assembly business, Magna often has a 4-5% profit margin, versus 2-3% for Foxconn, but I wouldn’t count on Foxconn being great at this new business out of the gate. As they announced when they unveiled some prototype designs in 2021 (assembled by someone else), “Our biggest challenge is we don’t know how to make cars.”

I’m sure they can learn, but I’d hesitate to bet a lot on them being really good at it anytime soon. Still, if they get a high-profile deal with Apple, it might easily bump up Hon Hai’s share price — people love an exciting story, and the Apple Car would be a big deal. I’m a little skeptical about ever seeing an Apple Car, having been promised one for more than a decade now, but perhaps it will eventually lead to something.

And as to the “ChatGPT” connection? That’s pretty tenuous — basically, the argument is that because the growth of AI will lead to more demand for servers and more equipment in data centers, that FoxConn will be assembling a lot of those boxes and will therefore have big growth in that area.

Well, maybe. They are seeing rising demand for servers, so that’s true… but that’s a bright spot in a fairly tepid business right now. According to Reuters, back in May…

“Foxconn Chairman Liu Young-way told the company’s annual shareholders meeting the firm remained cautious about this year due to monetary policy tightening, geopolitical tensions and uncertainty over inflation, but servers were a bright spot due to surging interest in AI.

‘More and more people are using ChatGPT,’ he said. ‘You can see the market for AI servers will rise much faster than expected. We expect that in the second half of this year there may be a three digit increase.’

“The Taiwanese company has a 40% global market share for servers and aims to further increase that, Liu added.”

According to that same Reuters update, Foxconn’s “cloud and network” segment, which includes their server assembly business, was 22% of revenue in their first quarter, and though that was a bright spot it was also likely to remain flat in the second quarter (they should report second quarter earnings next week, that report was on August 10 last year). At the time of their first quarter update they were still expecting “flat” full year earnings, due to continuing soft demand for consumer electronics relative to the pandemic peak (and inventory gluts that remain in some of those products). They’re still optimistic that more car companies, particularly new EV companies, will come to Foxconn for contract manufacturing and help them build up that business, and they’re also expanding their production capacity for batteries and electric vehicles in China, but the startup at Lordstown has been slow (they’re making some autonomous tractors right now, but plan to launch their “Model C” EV platform late this year). They’re doing a lot of cool things, including investing in satellite development, metaverse applications in their factories, and partnerships for automotove software and semiconductors, but none of it is currently creating any margin improvement or meaningful revenue growth.

Things may pick up with server demand, we could get a surprise 10% revenue boost this year if server demand really continues to go ballistic because of AI and they get a 100% increase in that business… but since they’re also saying that they expect 2023 to be a pretty flat year, I assume that assembling servers is not a particularly high-margin business. Which means their earnings, for the foreseeable future, will probably continue to be determined by how many iPhones and similar consumer electronics are sold.

I have a hard time predicting huge success for Foxconn in general, particularly because they’ve been in this rut of relatively slow growth and low (often declining) margins for a long time, but it’s certainly possible, and they are trying to expand into more businesses, particularly EV assembly. You may well take my skepticism with, well, a bit of skepticism… maybe the “one stock retirement” hype from the Oxford Club and my skepticism can balance out a bit, and then you can go into your analysis fresh and unbiased and make your own call.

It’s definitely a cheap stock, so you’ve at least got that going for you… But there’s no rush, it’s been a cheap stock almost all the time for close to 15 years now, so the odds are pretty good that you’ve got time to think it over.

So please do go forth, researchify for yourself, and let us know what you think about Hon Hai and its prospects for the next few decades. Just use the friendly little comment box below… and thanks for reading! I’ve left all the old comments attached below from our past updates to this story since 2018, to provide some perspective.

Disclosure: Of the companies mentioned above, I own shares of Amazon and Google parent Alphabet, as covered in my Real Money Portfolio. I will not trade in any covered stock for at least three days, per Stock Gumshoe’s trading rules.

Does anyone know the new AI coin for 2023 that Teeka is offering for free?

An interesting review by a star reviewer. Thank You

Thank you for exposing this slick con artist