An earlier version of this article was published on March 23, 2023, when the ad started circulating. The ad has been tweaked a little, and the story has changed somewhat, so we updated the story below in October, and I’ve added a March 2024 update down at the bottom as we hit the one-year anniversary.

There’s still a lot of interest in oil and gas investments, since that was the best-performing segment of the market last year, and Marc Lichtenfeld is promoting his Oxford Income Letter ($79) by promising some special reports, including “The #1 Oil and Gas Royalty for 2023″… so let’s dig in and see what he’s talking about.

The promise is for huge income plus capital gains… from the ad:

“Today, I’ll show you my #1 play to profit from the oil and gas surge in 2023.

“It’s a way to…

“Collect monthly income over and over again… for life…

“While banking huge capital gains.

“The average return on this unusual class of investments was 196% last year…

“And I believe that my pick is poised to see the same profit potential this year.”

The baseline assumption he’s working with is, “energy prices are going up” — which has been true for the past couple months (for oil, at least), though 2023 has been far less dramatic than 2022 was (oil is currently up 6% year to date, natural gas down 29%). Here’s how he puts it:

“We’re Entering Into the Greatest Energy Bull Market of This Century

“Nearly everything I’m seeing points to soaring oil prices in the coming weeks and months.

“The world’s two largest economies – the United States and China – are buying up all the oil they possibly can….

“Yet while demand for oil is expected to reach an all-time high, global supply is dropping.

“Despite Biden’s efforts to make a deal, OPEC rejected his proposal.

“And instead is reducing production to drive up prices.

“At the same time, Russia – once the world’s largest exporter of oil to global markets and the second-largest crude oil exporter behind Saudi Arabia – has been cut off from all but its closest allies.

“And here in the United States, Biden is actively squashing new oil production….

“Supply is down.

“And reserves are low.

“All while demand is surging.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“So it’s inevitable that oil prices are going to rise dramatically.”

It’s true that lots of people are still optimistic about oil companies doing very well, and it’s even true that Warren Buffet has continued to buy more of Occidental Petroleum (OXY), among many other notable investors who loaded up on oil stocks last year… but it’s also true that energy prices peaked last Summer and have been mostly falling since then. Oil today is still about 10% lower than it was before Russian tanks crossed the Ukrainian border on February 24, 2022 (and natural gas, at least in the US, is much lower (44%)).

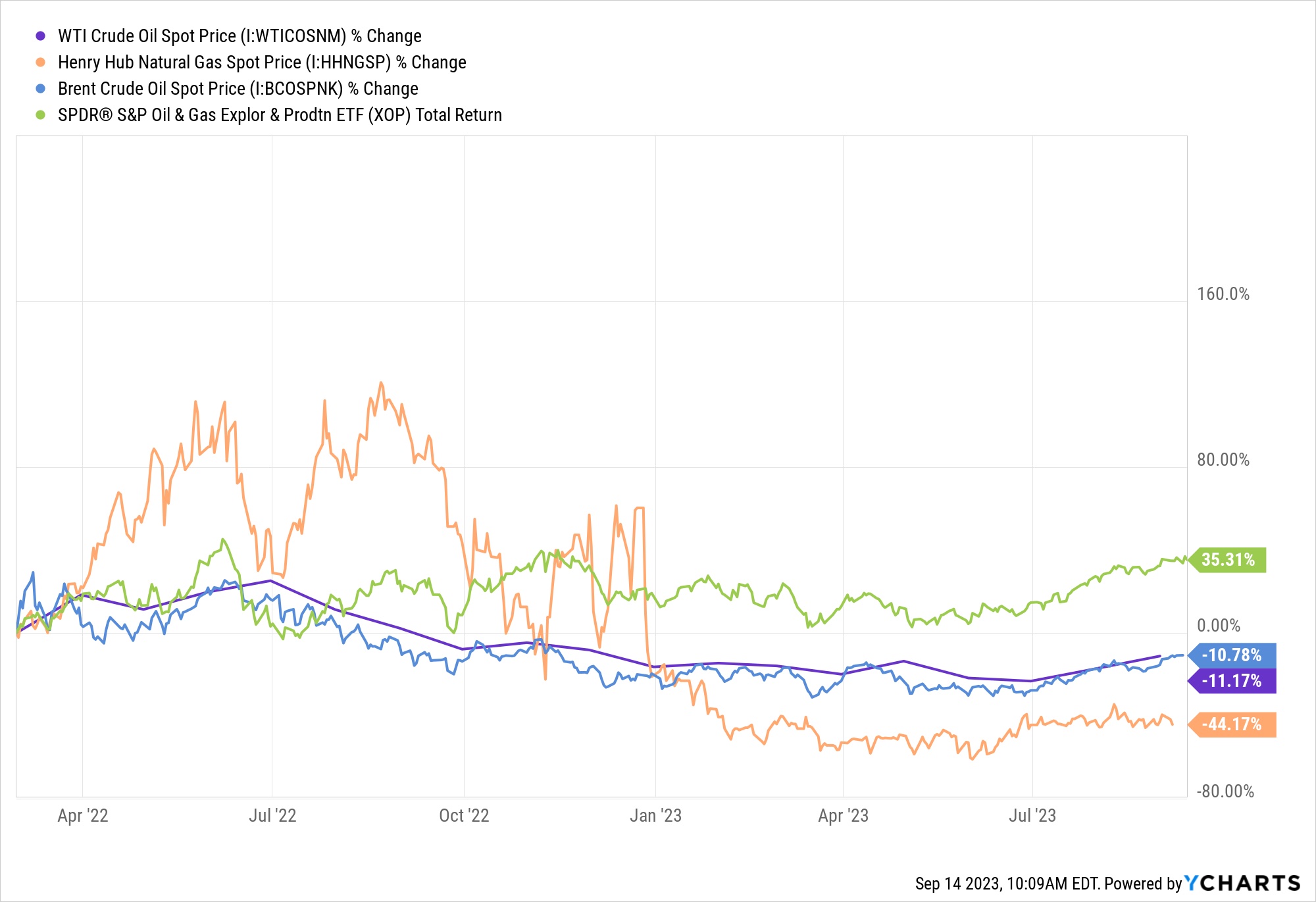

Here’s what that looks like in chart form — this chart starts on February 24 of last year, when the tanks started rolling and Putin’s energy bull market really took hold, and goes through today. The peak was very profitable for most energy companies, the decline has been more challenging… though investor interest remains robust enough that the big oil and gas companies haven’t fallen as sharply as you might imagine. The average oil & gas company is still up about 16% since the invasion of Ukraine, even with oil down 10%+ and US natural gas down 40%+.

Part of that is because oil is seen by a lot of Wall Street veterans as the cleanest “profit from inflation” trade, and presumably part of it is that the emergence of the Chinese economy from COVID restrictions, which has been happening gradually over the last year, seems likely to significantly increase oil demand. Add that to the fact that oil companies resisted the urge to over-invest this time, suspecting that the spike in oil and gas prices was probably a bit of a one-off windfall trade, and responding to investor demands for efficiency and dividends, and the profits of the big energy companies have held up well, supporting their stock prices. That green line (up 35%+) is the SPDR Oil & Gas Exploration and Production ETF (XOP), which owns companies like Chevron (CVX), ExxonMobil (XOM) and CNX Resources (CNX), green is US natural gas prices, the other two are oil prices (WTI and Brent). Even with a fair amount of natural gas exposure, producers have held up well since the windfall prices started declining last year.

But what’s Marc Lichtenfeld pitching? Something a wee bit different, it sounds like — here’s how he puts it:

“You’ll soon hear about people in your life running out to invest in oil and gas stocks.

“Many people might talk about their gains in Chevron, Shell and Exxon.

“If you choose to follow them, you may do well.

“But I wouldn’t recommend that.

“Because I’ve found an alternative investment with far more upside potential…

“And, more importantly, less risk.

“It’s – without a doubt – the most promising oil and gas opportunity I’ve ever seen.

“It’s not a stock, bond, private company or option.

“And it’s not oil futures or anything complicated.

“Rather, it’s an unusual way to directly profit from America’s energy boom…

“While collecting big monthly income.”

What else do we learn about it?

“During 2022 – the worst year for the markets since 2008 – this virtually unknown oil investment returned 149%!”

Well, sure, it was a bad year for the markets, and for the Ukrainians — but natural gas was up more than 100% for half the year, and oil was up 25%.

And while it’s not a stock or bond, apparently, anyone can buy it…

“You don’t need a special account.

“You don’t need to be accredited.

“And you don’t need a lot of money.

“You can get into this little-known oil strategy for just $25.”

This story even has a Charlie Munger connection, apparently he made this kind of investment before he joined Warren Buffett at Berkshire Hathaway, and put up $1,000 that eventually turned into annual income of $100,000 for decades.

There are a couple “regular guy” quotes in the pitch as well..

“And you don’t have to be a big investor like Munger to make big income from this secret…

“62-year-old Gerald Dowden, who owns a construction business, says he’s making even more than Munger…

“He’s banking up to $40,000 each month!

“Charlie Clark, a dairy farmer in Pennsylvania, used to scrimp and save before he found this little-known income source.

“Charlie says it felt like he ‘won the lottery.’

“He says he collects about $10,000 in income every month from it.”

Those particular examples are not from people investing in something like what Lichtenfeld is teasing, to be clear, those are from landowners earning royalties by allowing oil and gas companies to drill and produce energy on their land (those quotes are from stories like this one about landowners in the Marcellus Shale in Pennsylvania, or this one from the Haynesville Shale in Louisiana).

So presumably Lichtenfeld is pitching something similar to a royalty company, and if it’s not a stock it’s very likely to be a trust or master limited partnership (MLP), which trade just like stocks but are actually income-focused entities that usually distribute substantially all of their cash flow to partners and unitholders (and create a little bit more work at tax time, though they can also provide tax benefits to some holders).

That means the returns won’t be nearly as dramatic as those kinds of windfall returns he cites, since those were mostly earned by farmers who got big royalties because of discoveries on their land, sometimes including windfall payments for the lucky ones, but didn’t have to buy royalties (they presumably bought the land at some point, of course, often generations ago, but didn’t buy the royalties).

Here’s how Lichtenfeld puts it:

“‘Oil and gas royalties’ are a backdoor way to get paid over and over again from oil and gas properties.

“You get to bypass all the normal costs of doing business, like exploration, hiring rig workers, buying machinery, and bringing your oil and gas to market.

“Instead, you simply collect incredible royalty streams for owning a very valuable asset… the oil or gas field.

“It’s the ultimate passive income investment.

“And you don’t need much to get started.

“As I’ll show you in a minute, you can get a share of many of the most profitable and valuable oil and gas royalties for a few bucks.”

And, yes, he’s got “one favorite investment” in this space:

“In a moment, I’m going to share with you details on my #1 royalty stake that you can take advantage of today for just $25.

“You can simply make a single investment…

“And collect MONTHLY royalties.”

Sounds appealing, right? Here Lichtenfeld explains the appeal of top-line royalties:

“The point is, the entire process for exploring, extracting and refining can cost hundreds of millions, if not billions, of dollars.

“But oil and gas royalty interests are a different story.

“Royalties spend very little money to make money.

“It’s a perfect investment during times of high inflation, like right now….

“Because royalties get all the growth of the oil and gas industry… but don’t have to pay high interest, like companies such as Chevron or Exxon Mobil.

“AND you don’t take on all their risks.

“You’re simply acquiring a right to a portion of the income from some of America’s biggest and richest producing oil and gas fields….

“All the hard work is done by a big oil and gas company… and they bear all the risk.”

I am a sucker for top-line royalties, or really for any kind of business that works in a similar way, giving shareholders exposure to the cash flow of an industry without requiring big capital investments… Warren Buffett likes to talk about these capital-efficient businesses, too, and has shared thoughts over the years about how even companies that aren’t specifically royalty owners can have similar business models.

Somebody on Twitter found this old 1979 article on Buffett, for example, that I really liked, he talked up the idea of a “gross revenues royalty” at that time, and though he was talking about different businesses, newspapers and iron ore, the basic idea is the same…

Here’s an old Warren Buffett profile:

[TLDR: When there’s inflation, look for businesses that are (a) royalty-like and (b) asset-light.] pic.twitter.com/cSx2kc8bk6

— Turtle Bay (@72types) January 6, 2023

So which one does Lichtenfeld like? Let’s check out the clues…

“It’s a royalty stream from the most productive oil reserve in the world…

“The Permian Basin….

“Surging Permian production has made the U.S. the top oil producer in the world.

“Already, it’s producing 5 million barrels of oil per day.

“That’s almost half the U.S. supply.

“And over 20% of the world’s drilling rigs are operating in the Permian… more than all other countries, including Saudi Arabia.

“But this is just the beginning.

“Only 37% of its wells have been tapped.”

OK, there are a few companies who own royalty interests in the Permian Basin… any other hints for us, Marc?

“This single royalty lets you profit from over 380,000 acres in prime oil and gas fields.

“Revenue is at its highest level in three years, as are earnings.

“It has no debt, has $11 million in cash and pays out its earnings back to shareholders, hence the sky-high yield.

“Quarterly revenue growth is up a staggering 717%…

“Over the last year, it’s brought in $42 million.”

So hoodat? Well, this is the aptly named Permian Basin Royalty Trust (PBT), and Lichtenfeld’s pitch, even with a few updates, is still dated “February 2023”, so the numbers are a bit out of date — and sadly, things are not going quite as fantastically for PBT now that we have a few more quarters of numbers.

As of September, PBT revenue was up 717% on a year-over-year basis, but as of December that number came down to 354%, and now we’ve lapped those boom-year numbers in 2022 and the past two quarters have shown growth of 28% and, last quarter, a 20% reduction in revenue.

2022 was the best year for Permian Basin Trust, in terms of top-line numbers, since 2012, they ended up with $54.5 million in revenue and distributed most of that to shareholders (sorry, “unitholders”), so the total dividends for 2022 came in at $1.15 per unit, and on that basis the trailing dividend today would be a hair over 5%. Not exactly a “sky-high yield,” though I guess if you bought a year ago, at about $13/share, you would have enjoyed a 9% yield during the boom times.

The bad thing about being a passive royalty owner, however, is that there is a down side to “passive,” too — you don’t get to tell the companies who are operating on your royalty lands how much to produce… and they’re producing a commodity, so you can’t set the price for your own oil or gas, you have to take what the market is offering. With oil and gas prices falling pretty dramatically from the peak, production flattened out for a while and even come down a bit this Spring, and the revenue from selling that oil and gas has come down pretty substantially.

PBT does pay cash distributions to unitholders on a monthly basis, but those payments are FAR lower now than they were last year — the distributions in September and October of last year were 22 cents and 21 cents… but then November dropped to eight cents, December to four cents, and the distribution has stayed low all year, ranging from two to five cents. The past two months have both been a hair above two cents, so if that kept up it would annualize out to 25-30 cents per share for the year, a yield of 1-1.5.

Not so sexy.

So the reason to buy shares of PBT, essentially, is that you are pretty sure oil and gas prices will go much higher again. Nobody’s buying for a 1-2% dividend, they’re buying for the hope that the drilling on PBT’s royalty lands, which is still ongoing, will ramp up and produce more oil and gas for years to come, and that prices for those commodities will rise again. And as long as you don’t mind waiting, it’s OK if it takes a while — the operating costs for the Trust itself are small, so they should be able to survive and eventually be ready for the next bull market, even if the energy market dries up for a while and production and prices collapse.

There’s no fancy financial engineering or compounding value here — the Trust generates cash flow from the royalties they own, and they pass that cash flow to you. They don’t invest anything in buying new royalties, and they don’t do anything like buy back shares, and outside of some strict limitations they can’t even borrow money, a trust is a pretty simple structure — they have their operating costs to keep all the legal reporting and accounting accurate and cover whatever other costs are necessary as a public trust, which generally tallies up at about a million dollars a year for PBT, and the revenue that’s left over is distributed to the 46.6 million shares of PBT — if that top line is $53.5 million, like it was last year, then that ends up being a distribution for the year of $1.15 per share… if it’s $21 million, like it was in 2016, for example, that’s 42 cents per share. So far, the best year for PBT was 2008, with $2.39 per share in distributions, and the worst year was 2021, at 23 cents (a hair lower than the 23.5 cents in 2020, when oil demand collapsed).

There is an important distinction here, though. This is not really a “gross revenues royalty.” There are costs that go into turning the production on their royalty lands, which are primarily in a parcel called the Waddell Ranch, into their royalty revenue — the words they used in the March quarterly update were, “the the oil and gas sales attributable to the Royalties are based on an allocation formula that is dependent on such factors as price and cost (including capital expenditures),” but you can spend some time with the 10-K if you want to really get a handle on what the impact is.

Basically, the royalty on their biggest property ends up being 75% of the profits from the oil and gas production on their lands, so despite what Lichtenfeld says about this, they do effectively get hit with their share of the capital expenditures, operating expenses, and other costs. These are not clean “top line” royalties like we might be used to some from other royalty businesses, the Waddell Ranch Properties (which is the biggest royalty asset PBT owns) generated $243 million in sales in 2022, but only $47 million in net profits, and Permian Basin Trust owns 75% of that, so their “royalty income for distribution” from Waddell Ranch last year was $35 million. Most folks refer to this as a “Net Profit Interest (NPI).” Which can be an effective investment, particularly when you have a good operator and costs are low (and oil prices are going higher, of course), but it’s not a royalty. A share of profit is very different than a share of revenue.

So that helps to explain some of the very dramatic shifts in distributable income — when the operator spends more heavily to drill or when operating expenses are high, as is the case this year, that eats into the royalty owners share… and if that happens when oil and gas prices are falling pretty sharply, it can quickly erode that distribution. The hope, I guess, is that the spending on well completions and the investment in increasing production will pay off, ideally with higher production over the next few months that happens to coincide with higher oil prices, but we’ll see how it works.

This has happened before, so even in a good year there might be quite a bit of seasonality, depending on how they allocate the capital spending budget. Waddell Ranch didn’t contribute anything to the “Total Royalty Income” in 2021, and, in fact, they were effectively in deficit on that property for a few months as production paid off the capex budget, which meant that PBT didn’t catch up and start receiving 2022 payments from Waddell Ranch until May of 2022… which I guess makes it more remarkable that they had such a strong year of royalty revenue after energy prices soared through the middle of last year, since that larger property only generated royalties for PBT for seven months of 2022. That’s an indication of just how levered a royalty company can be to higher commodity prices, even if it’s not so clean in their case because they’ve really got a “net profits” royalty, not a “gross revenues” royalty.

The plan earlier this year was that Blackbeard, the operator of their Waddell Ranch property, would invest $122 million (net to PBT) on CapEx, for 49 wells, which is similar to what they spent last year ($124 million), and part of the reason that the cash distribution was so low to begin the year was that they were eating that CapEx budget (you drill before you get paid)… the Trust’s proceeds out of Waddell Ranch’s $17 million in revenue in January (which is what goes into the March royalty payment) was negative $411,000, mostly because the CapEx budget was over $14 million… so if Blackbeard keeps spending at their intended pace, that would be roughly $10 million a month in CapEx for the rest of the year, which would probably mean that they either need these new wells to be very productive or they need higher energy prices, or else royalty income is going to be meaningfully lower for the balance of the year.

Now that we’re a little further along, Blackbeard has reduced its CapEx plans for the year, which also reduces the number of wells they’re likely to complete. The projection for PBT’s share of CapEx in 2023 is still $97 million, same as it was a month ago, and as of the September update from PBT they said “approximately 58%” of that budget has been incurred (it was 42% a month ago). Which means that again, in September, the Waddell Ranch NPI deal, by far their largest asset, did not contribute to the monthly distribution.

That led to this change to the language in the March monthly distribution announcement, the emphasis was added by me “…if current oil and gas pricing continues, Waddell Ranch may or may not be able to continue to contribute to the distribution in the foreseeable future, to cover the ongoing CAPEX budget.” That’s still the language they use as of September (the previous assessment, way back in February was that, ” if current oil and gas pricing continues, Waddell Ranch should continue to contribute to the distribution in the foreseeable future.”)

That change in language happened from February 20 to March 20, during which oil prices dropped about 10% and natural gas prices dropped about 5%. Gas prices remain low, but oil has started bouncing back… and the language has not gotten more optimistic. The foreseeable future, lest we remind you, is not really as foreseeable as we think it is.

So we might end up seeing their “lesser” asset, the portfolio they call “Texas Royalty Properties,” which is a collection of royalty properties spread around (mostly) West Texas, again become a much larger percentage of their revenue?

That portfolio looks more like a real royalty, it does not include adjustments for CapEx, and operating costs are much lower, and they have a 95% share instead of 75%, but the top line is almost always a lot smaller ($22 million in production in 2022, versus $243 million for Waddell Ranch). That portfolio of royalties is what is keeping the distribution above zero right now (In September of 2022, for example, Waddell Ranch generated $8.5 million in “royalty” revenue for PBT, and Texas Royalty Properties $1.9 million… in July of 2023, the most recent month (reported in September), with production higher for both of those assets than it was a year ago, but prices far lower, especially for gas, Waddell Ranch was still in deficit (their NPI for June would have been about $1.5 million, but they owe for past months CapEx still, so they just lowered the cumulative deficit to about $200,000), and Texas Royalty Properties generated $1.1 million in royalty revenue, a number that has been relatively steady this year. Deduct the modest operating costs for the Trust, and that $1.1 million divided among 46 million shares is a little over two cents, thus the 2.24 cent dividend for that month (down from 2.45 cents last month).

What the dividend happens to be next month depends partly on what prices were in August (since production takes about two months to get moved and sold and trickle through to royalties), but perhaps more dramatically on what the capital spending is for Waddell Ranch in August. The top-line difference doesn’t seem so big, Waddell Ranch had revenues of $23.5 million going into the September payment a year ago, and a still-pretty-high $17 million going into the March payment, but the huge CapEx spending really makes a difference (CapEx and OpEx that reduce the NPI totaled $12 million last September, $17.8 million in March). That’s what turned slightly positive in June and July, but not enough to make up past deficits yet (July revenue was $19 million, minus OpEx of $4.9m & CapEx of $12.8 million, led to $1.5 million, which could have doubled the dividend to almost five cents… but they still have to pay down accumulated CapEx from earlier in the year, so they get nothing — since the accumulated CapEx deficit is almost repaid now, if that dynamic stays the same for August, with similar pricing, then the dividend could double in October). The last time the Waddell Ranch NPI contributed to the dividend was in June, when the April production netted PBT enough to do just that, pay roughly twice as large a dividend (roughly five cents), and it contributed a little bit in several of the earlier months of the year, too.

You do need the magic of rising prices if you’re going to have anything left over after that kind of increase in capital spending we’ve seen from Blackbeard at Waddell Ranch this year, even with the reduction in the CapEx budget through the year (it was $122 million earlier this year, now down to $97 million), and since these horizontal fractured wells require constant working and probably have a rapid production decline in general, the CapEx likely never goes away — if you want production growth (which the operator surely does), there has to be at least a steady, if not growing, amount of drilling. That’s a known challenge for any oil producer, but it’s pretty irritating for someone who might have been mistakenly thinking they’d be getting a passive top-line royalty.

Still, the Trust persists for a long time, maybe forever if they keep finding new formations to drill (the beauty of the Permian, and the reason this royalty interest didn’t play out decades ago, is that it’s stacked, with a dozen layers of producing rock in a lot of areas, and they keep finding more layers to exploit under the same plot of land). The Trust does try to calculate the future value of their share of reserves, though that is mostly an exercise in math for math’s sake — nobody knows what production or pricing will look like in the future, or what new oil they might find, but as of this year they say their discounted future net cash inflows (at a 10% discount rate) are worth $686 million. To give you an idea of how sensitive this is to current prices and production levels, the same properties had a calculated value of $80 million in 2020, 87% lower than the current reserve estimate. I guess they have to give us those numbers, but we should probably ignore them. (The market cap of PBT right now is just about $1 billion, so it’s way over the discounted cash flow value value… and the market cap did fall to about $100 million at the 2020 lows.)

The good news? It’s a grantor trust, not a master limited partnership, so you don’t have to deal with K-1 forms, they report their distributions to you, and your share of the earnings, on a regular ol’ 1099-MISC form through your broker (though they do also send out a tax package to help you report your share of the Trust’s business, including credit for depletion, so it might not be all that much simpler — haven’t gotten one of those, so I don’t know whether or not it’s annoying).

Bad news? The distributions are not “qualified” dividends, they are considered pass-through royalty income, so you’d pay regular income tax, not the lower dividend tax rate. I haven’t seen their tax package, to be fair, and it’s pretty likely that depletion allowances would mean that most of the distribution is return of capital, like a MLP, which would mean it reduces your cost basis rather than generating taxable income.

What’s going to happen in the future for PBT? That’s a good question. Royalty and NPI payments are tallied up and distributed about two months after the oil is produced, and they post a monthly announcement here for investors (those are the source of most of the details I’ve shared today), so the September distribution of $0.022414 per share is based on the production from their royalty and net profit interest (NPI) projects in July.

The company won’t be issuing lots of other press releases or presenting at conferences, so there’s no flashy powerpoint deck that predicts the future (remember, their overhead costs are only about a million bucks a year, mostly for legal and accounting/auditing, they don’t really do much of anything directly, including sell themselves to investors)… their projections essentially consist of this sentence in the monthly reports:

“The worldwide market conditions continue to affect the pricing for domestic production. It is difficult to predict what effect these conditions will have on future distributions.”

Couldn’t have said it better myself. If oil and gas prices go up sharply, PBT will probably do pretty well, though it looks to me like the share price is already effectively “pricing in” some much higher distributions kicking in at some point in 2023, presumably in the hope that the CapEx spending was being front-loaded and will drop, and also that the big CapEx investments last year and this year will turn into production growth, which it has in the past, and that this will increase the cash flows from new wells at some point in the future.

If energy prices don’t go up, PBT won’t do so well. The CapEx costs, which the new operator at Waddell Ranch have been kicking up in recent years as they’ve increased production, could be beneficial over time, we don’t really know what the plan is because Blackbeard is private, so all we know is that the CapEx is now estimated to be $97 million for the year, they’ve spent 58% of that as of July, which is, to save you the math, 58% of the way through the year, and at current oil prices that continuing CapEx on their Waddell Ranch NPI is still eating most of the distributions right now.

Over the past few decades, it has worked out that rising oil and gas prices do generate higher revenue for PBT. And since they have no debt, their own operating costs don’t change much, and they never issue new shares, so that means higher energy prices have historically led to higher dividends.

Here’s a 20-year chart that shows the PBT price (purple), their trailing annual dividend per share (orange) and the WTI crude oil spot price (blue) — only about 20% of revenue is natural gas, on average, so I left that out to simplify things:

What does that tell us? To me, it says there’s a LOT riding on those little blips on the far right of the chart, with the trailing dividend dropping as they pay far less than they did a year ago, but with oil turning up in recent months.

Back in March I wrote that the surge in the PBT share price didn’t look sustainable to me, and I bet against it with some put options — the shares did drop, but not enough for me to make any money from that bet.

Things will look up if oil and gas prices surge higher, but if they just stay near this level the huge CapEx spending at Waddell Ranch could continue to eat up a lot of the potential returns before they become royalties — that would be OK if investors were expecting to end up with a 25-50 cent dividend for the year, but I don’t think they are, not at $20 a share (down from $23 when Lichtenfeld started pushing this, but not down that much). Nobody buys an oil royalty trust for a 1-2% yield unless they are really optimistic about future production growth. There seems to be more oil-price optimism in PBT shares than in anything else I’ve looked at.

That annual dividend bottomed out at 30 cents after the last oil crash, in 2014 and 2015, when oil was in the process of falling from $100 to $30, but back then the higher-margin Texas Royalties were producing 50% more than they do now, and Waddell Ranch was producing much less but also had dramatically lower CapEx spending. My guess is that because of much higher CapEx and operating costs, they need substantially higher oil prices today to generate a 30-50 cent annual dividend than they did in 2015, when the oil price ranged from $35-60… though that depends on how much Blackbeard wants to keep pushing into CapEx for more drilling if oil prices stay at these levels or fall.

During the brief period when oil was trundling around at $60-70 in the second half of 2018, PBT generated monthly dividends of about five cents, though that was with a different operator… and at the time they were spending almost nothing on CapEx at Waddell Ranch. Maybe they’ll hit a “sweet spot” for pricing and CapEx that lets them maximize their NPI revenue and grow from here, but PBT is not the operator — we don’t know what the best strategy is for Blackbeard, the company making the decisions, but it’s not necessarily “maximize current royalty revenue,” there’s always the risk that the operator might prioritize production growth or asset utilization over net profit, especially in the short term. The good news is that Blackbeard has roughly doubled production from Waddell Ranch since taking over in 2019… the bad news is that they have spent heavily to get there, and PBT has to eat its portion of that spending before they can make their net profit.

My guess back in March was that PBT’s distributions would recover a little late in the year, but probably max out at something like 50-60 cents for 2023, roughly half of the $1.15 they paid in 2022 — at $20, that would be a 2.8% yield, less than you can get from ExxonMobil (XOM, current yield 3.1%), and about half of what you can get from a bank savings account. Even if the dividend recovers to last year’s windfall levels, with oil and gas both going up 30-50% from current levels, that would still be only a 5.5% yield, much less than most oil royalty trusts and similar companies are paying. Given that we have only three months left in 2023, and the dividends tally up at about 30 cents so far in the first nine months, I might have been a little too optimistic with that 50-60 cent guess.

To be more optimistic than that, to bet that things will be better in 2023 or 2024 than they were in the boom year of 2022, I think you’d have to really love what Blackbeard is doing as the operator at Waddell Ranch, and see some kind of pathway for higher production and lower CapEx spending — again, possible, but I don’t know why you’d bet on it when other royalty trusts have current production and yields that are much stronger and would be similarly levered to higher oil prices if they occur (unless, I suppose, you have some insight into Blackbeard or Waddell Ranch and know there’s something surprisingly amazing coming).

Summing up? All royalty trusts and similar net profits interest plays in oil and gas benefit from and are levered to higher energy prices… but PBT seems to need higher energy prices, since its operator is spending heavily on CapEx, and PBT’s price seems to build in a lot more optimism about the energy market in 2023 than others.

Think I’m too pessimistic on this one? Think the CapEx spending they’re doing right now to generate dramatic revenue increases in the coming months? Have I missed something in my analysis that justifies the soaring share price, despite the low current distribution? Do let us know with a comment below.

3/19/24 update: I check in on this one from time to time, mostly because the ads keep circulating and that leads to more questions from Gumshoe readers. We’re now about a year into Lichtenfeld teasing this as a “Huge Monthly Income” oil & gas play, and as a “10,000% Dividend”. The main bit of news since October is that the dividend did finally pop up to the “expected” level of 10-15 cents per share, and become meaningful for a couple months… but after those good dividends in November and December it has now come back down, paying out something more like the average of 4-5 cents per month. The other point of interest is that in December PBT sued the operator of their key Waddell Ranch property, Blackbeard, and essentially seems to be claiming that the “royalty” is being underpaid because Blackbeard claimed some operating expenses (which the Trust doesn’t have to pay) as capital expenses (which are deducted from the Trust’s net royalty income).

No idea when or if that gets resolved in court or somehow leads to a higher future dividend. Assuming no change, Blackbeard said that they ended up spending about 90% of the reduced $97 million (net to PBT) CapEx budget in 2023, and are planning to spend $90 million in 2024… so the best guess is probably that 2024’s dividends will be somewhat similar to 2023 IF the oil and gas prices are also similar (so far, gas is way down, and oil is slightly below the 2023 average price but trending upward for the moment).

During the 12 months that Lichtenfeld has been touting this “huge monthly income” play it has paid out about 60 cents in dividends total, and that’s roughly what we thought investors should expect when we covered this ad a year ago… which at the current price would be a 4% yield, and if you bought when Lichtenfeld started pitching it, at about $23 in March of 2023, your “income” would have been around 2.5% of that purchase price, and your total return, with the stock currently at about $14, would be a negative 35-40%.

Disclosure: Of the companies mentioned above, I own shares of Black Stone Minerals. I also own shares of Berkshire Hathaway.

At $95 p/b, the entire world economy begins to shutter, while oil production has already drilled the low hanging fruit, and it going farther and farther to his risk areas, offshore in the Arctic, deep waters in the Atlantic, while Alalska and the North Sea are petering out. Oil prices are cyclical, i.e., when prices rise, demand falls, when prices fall, demand rises. Oil cannot possibly stay at these prices without governments raising rates, that always leads to price collapse. You don’t buy oil at the peak. It’s time to go short, not long.

Less exploration, continued high usage… I’ll stay LONG, especially on the “little” companies

Cliff

Marc Lichtenfeld Bio: Marc Lichtenfeld – Mick Jagger

Marc Lichtenfeld (lead vocals) is thrilled to be playing Mick Jagger in Start Me Up!.

He formerly played Mick in Sticky Fingers in the northeast and in Tumblin’ Dice in San Francisco. He also sang in San Francisco’s ‘80s tribute Like, Totally! and with Grammy nominated guitarist Gil Parris.

A former actor, Marc appeared on stage in New York and San Francisco in shows including: Slasher, the Splatter Rock Musical and the stage premier of Last Exit to Brooklyn.

When not performing as the world’s greatest rock singer, Marc is a two time best selling author and the only Mick Jagger impersonator to ring announce world championship boxing and MMA matches on ESPN, HBO and Showtime.

Excellent! I knew about the ring announcing, didn’t realize he was also a Mick Jagger impersonator.

Travis, if you want a good laugh Youtube “Marc Lichtenfeld in Start Me Up!” and watch the videos. He’s a hoot!

So many ads that I never get to read the articles, currently looking for a similar website that doesn’t have so much clutter.

Sorry about that, Google handles the ad load automatically and some days it feels much worse than others… we do now offer an ad-free version for folks who are interested in “buying out” the ads.

I hold & like PRT and NRT royalties better, they have a better dividend yield, and a better P/E ratio.

Cliff

PBT’s been good to me.

Because I bot 100 in April 2020 for $337.

Even with “COVID FOREVER” priced in,

that seemed really cheap!

I see no reason to buy more at its current $22.

OR, sell it.

Its also NOT an MLP, for which tax prep expenses can exceed profits.

That’s a nice cost basis! If only we could all go back in time to April 2020 and put all our capital to work at those prices 🙂

PUMP it UP, Marc!

ALL TOO COMPLEX for me! Just sold AAPL for a healthy profit and put the $ into a bank CD paying 5.25% which will be untaxed since our income falls below taxable level for a retired married couple!!!

Selling AAPL might have been OK, but taking your money and putting ANYTHING in a bank investment right now is probably less than smart. You would be better out checking (where most people don’t even know the opportunity exists) putting it in your insurance account where many pay 3-4-5% interest!

Owned PBT and several other oil-gas royalty companies for many years. Found tax reporting of these companies is worse than the K-1 forms. Even with the expanded tax reporting that most companies do including PBT, (some do not and that is much worse), I found their reporting “clear as mud”. Fortunately my tax returns for the period of my holdings did not raise an issue with the IRS . Finally gave up totally and sold out of all of mine oil & gas royalty holdings

Again, you gotta know the territory. Most royalties generating a few thousand a month are purchased at auction . They are small interests, either royalties or overriding royalties. The buyer usually is usually paying 2 to 10 years income. As you said, the royalty interests have no say in the operations, but there is still risk. What if the operator decides to plug the well(s) because of low margins? Bye bye income. What if the operator is no count? He won’t be producing over the long term. The safest royalties are on properties that have little or no decline in production. On horizontal wells the royalties may be high at first, but the decline rate is steep, so the royalties will also decline steeply. The worst part of any resource investment is that the producer doesn’t set the prices. Right now the futures markets set the prices, and those are manipulated.

PBT As a Dividend play? I get the pass through 97% net profit margin but less than a dollar annual dividend with a share premium of 21.50.. Nope , I ll buy Dorchester minerals with a slightly higher premium but a dividend output of 3.90 annually.

The dividend has been higher in the past, perhaps it will be again. I assume that’s the hope.

I have a small profit in BSM and also a 100+ % profit in PR which I believe you previously covered around. December 2021. PBT has never been added to the Oxford portfolios

Must just be one of his “special report” stocks, I guess — Oxford sometimes does that with other names (Alex Green has been calling Hon Hai/Foxconn his “one stock retirement” idea since 2017, but I’m told he has never actually recommended it in the portfolios… so presumably it just works well at recruiting subscribers when it’s used in a “special report”)

Yes, Now there is a special invitation to join Lichtenfeld in his penny options service! He is pushing an Energy stock that is under $10. Any guesses as to what he is pushing?

YES! I Want Immediate Access to Marc’s Penny Options Trader…

Including a Free Copy of His Newest Investment Research Guide: “Double Your Money: The Sub-$10 Energy Stock Poised for Explosive Profits”

Bundle of reports, videos, and subscription perks that you’ll get when you sign up. Learn more below!

Travis – this is the teaser ad he is sending out. There are so many stocks under $10 now in the energy space, we can only guess what he is spinning?

Sounds like it’s probably a repeat of a similar teaser pitch he made a few months ago — haven’t looked to see if the company might be different, but it appears the same at first glance I covered that here.

If the company he was teasing was RES as you concluded, then they reported today and at the open the price fell @9%. Since then, it has recovered to just above flat, which suggests that buyers saw an opportunity. The main business of RES was down, creating a loss of revenue. Here is the news report{

RPC Shares Fall 9% as Pressure-Pumping Weakness Drags 3Q Results

October 25, 2023

09:07 AM ETPublished October 25, 2023 09:07 AM Eastern TimeDow Jones Newswires

Shares of RPC fell 9% after the oilfield services company cited a drop in demand for pressure pumping, the company’s main service line.

The stock fell 9% to $7.90 in the premarket session. So far this year, shares were down 2% through Tuesday’s close.

The Atlanta-based company reported third-quarter sales of $330.4 million, down about 28% from last year and below analysts’ expectations for sales of $376.7 million.

RPC’s earnings of 8 cents a share missed analysts’ expectations of 24 cents a share.

Chief Executive Ben Palmer said business across the company’s service lines was stable, except for in pressure pumping, where demand didn’t recover as the company expected.

Pressure pumping generated most of RPC’s revenue in 2022, and the company said growing shale-related production activity has boosted demand for pressure-pumping services in recent years.

Write to Will Feuer at Will.Feuer@wsj.com

(END) Dow Jones Newswires

October 25, 202309:07 ET (13:07 GMT)

Copyright (c) 2023 Dow Jones & Company, Inc.

Related Investments

RPC Inc

Last 3 Months

Back to News

What do we want to do with our options, Travis?

I’ve already lost my speculative money on that one, my options expired worthless a month or two ago 🙂

The ‘smart money’ bought puts! At least we were not sucked into buying LICHTENFELD’S newsletter1

Yep, capex has been falling more than most folks expected — don’t know whether it’s the low gas prices or the high interest costs, or something else.

Just saw Marc’s pitch about his one look chart, with just one line, and his team’s $50,000 AI computer that signals buy/sell proving 5X your money. After 5 minutes I fast forwarded to the end…. I did not bite the big cost ($1995) I wish it was legit but I am so skeptical of every “sure thing” these days. Thanks for doing a lot of Oxford Club write ups here.

About 2% of broadcast emails look interesting, and I wish they were legit. However…..

Weren’t there some huge discoveries of new oil offshore of Guyana and offshore of Africa this year? I think Mobil has the franchise for the Guyana field if it is developed. One play on the African discovery is Reconaissance Energy Africa, a penny stock with lots of downside I suspect. I haven’t seen much discussion of these discoveries. Any comments?

ust checked today after closing and PBT is at the lowest price in over 18 months at $13.35. That would make the divicend of slightl more than 4 cents a share monthly, to an annual rate of around 3.5% or so. PLUS as a Canadian , I would have to pay a 15% non-resident tax on that, and everyone who is not a resident of the U.S. or Canada would have to pay a 30% penalty tax. Why would anyone won’t this ??

Sorry about the typing errors, fat fingers

I used to own Energy Transfer LP but sold it for a profit because my accountant kept griping about the tax complications. Are all these these royalty trusts the same when comes to income tax reporting?

Most of them are publicly traded partnerships or trusts, I don’t know if there are any exceptions among the royalty companies but there might be (there are exceptions in pipeline world, I think Kinder Morgan and OneOK are both corporations now… and the ETFs generally absorb the K-1 filing impact and turn it into something easier (I use AMLP, but there are others)).