“America’s ‘Infinite Oil Well’ — Matt Badiali teases that “Revolutionary New Technology Could Unlock a Potential $70 TRILLION Windfall”

by Travis Johnson, Stock Gumshoe | April 29, 2019 1:01 am

So... uh, what is it? We follow the clues in ads for Real Wealth Strategist to get you some answers

This teaser solution was originally published in late January, but we’re seeing the ad pushed more again now and are getting more questions so I updated this piece to provide some more information and check in on the company.

Matt Badiali[1] has been pitching an “Infinite Oil” company in recent weeks in ads for his Real Wealth Strategist[2], so I thought we’d take a moment to see if we can name that “secret” stock for you… and maybe get you started on your research.

The big picture spiel is pretty overwhelming, he shows these big pyramid charts that demonstrate the fact that the oil[3] produced in the US is but a mere 3% of the total oil in place… with the implication that this “infinite oil” technology will some how produce the rest, unleashing “a $70 trillion windfall.”

Which sounds like hokum, of course, but we’ve got to start somewhere. Here’s a little taste of the ad:

“… the vast majority of this oil has been trapped underground.

“Completely inaccessible and nearly impossible to get out of the ground.

“Until now.

“Because a cutting-edge company — based in Houston, Texas — has been working to perfect a breakthrough technology…”

He doesn’t talk much about what this “infinite oil well technology” actually is, but implies it’s something that’s been “evolving” …

“In fact, I’ve spent years watching the evolution of this infinite oil well technology. And now is the perfect time to buy in.

“You see, there is a company — employing a powerful new technology — that is among the very first to tap into the massive ‘lode’ of oil that still remains untouched.”

He draws comparisons to the huge advances that have made so much oil for pioneers in the past:

“With just three innovations: the pump jack, rotary bit and pipeline…

“Billions were made by the Trout, Hughes and Rockefeller families, not to mention enormous fortunes for shareholders.

“But all of that is nothing compared to what the infinite oil well is doing today in America’s oil fields.

“… as exciting and lucrative as fracking[4] has been for American oil…

“It’s nothing compared to the money that could be made with the infinite oil well.”

What problem does this “infinite oil” technology solve? The implication is that it’s the next wave of oil extraction, improving the production over time an dgetting rid of the well-known rapid decline of production following hydraulic fracturing (the oil gushes out to start, then quick slows). In Badiali’s words:

“When a well is fracked — it produces a gusher of oil quickly.

“However, the enormous pressure immediately begins to close the fractures again. That massive flow of oil soon begins to die down.

“In fact, production from shale wells can drop as much as 70% over the first year….

“For the past 10 years, since fracking changed American oil production as we know it…

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“We’ve still been leaving as much as 97% of the oil in the ground.

“… infinite oil well technology makes it possible to begin getting more of that remaining 97% of the oil out of the ground.

“And it does it faster and cheaper than ever before.

“When you’re talking $8 million for a conventional well, versus $2 million for an infinite oil well, the savings here are incredible.”

It sounds like what he’s really talking about might just be re-fracking — going back and re-completing or re-fracturing wells to restimulate production (or restart production from an old well)… or maybe some combination of other general improvements to well completions and restimulation.

And, of course, there’s the tease that it’s “just one company” you have to own:

“I’ve identified the No. 1 company that is leading the charge on this massive windfall.

“A company that holds the key to unlocking incredible wealth for fast-acting investors who get in now….

“It’s at the forefront of the infinite oil well revolution, and it’s in prime position to take a huge bite out of this massive new market.”

So what else do we learn about this?

“It’s at the cutting edge of advanced technology that is making the infinite oil well even more productive across all kinds of wells.

“In the industry, we call it an ‘oil field services company.’

“From well planning to horizontal drilling to completion to the infinite oil well — this company does it all.

“Their expertise in the field has made them a dominant name in the industry, with a national reputation for excellence.

“In fact, they’ve generated revenues from every major oil field across North America.”

OK, that narrows it down a bit. Any other clues?

“Marathon Oil, Apache, SM Energy, Encana, Energen, EOG Resources, XTO Energy, Continental Resources, EP Energy, Concho Resources…

“They ALL have relied on this company to get more oil out of their wells.

“Even big oil majors like Conoco Phillips and Chevron have been working closely with this cutting edge outfit.”

And apparently they’ve got some new technologies as part of this “infinite oil” stuff…

“This company has introduced a patent pending technology that’s making infinite oil well technology even better.

“A new technology that’s destined to open the floodgates, allowing them to extract even more oil from wells that were once thought inaccessible.

“Using the latest in advanced chemistries and leading-edge technologies, the company can customize its infinite oil well treatment for each and every well.”

How about a few more specifics?

“The men in charge have a total of over 210 years of combined oil field experience….

“Revenue grew 76% year over year for the first quarter to $553 million….

“And in 2017, they reported revenue of $1.63 billion, an increase of 69% over the previous year….

“Priced at just around $20 a share, this may be the most undervalued stock in the industry….

“Realistically, these shares could triple your money in the months to come.”

So… who is it? This is, sez the Thinkolator, the oil services[5] company C&J Energy Services (CJ)… which, in case you’re checking up on those clues, did indeed post a 76% year over year revenue growth quarter to start 2018 [6](and yes, that meant revenue of $553 million).

[7]This is a stock I had on my watchlist five or six years ago, back when oil was soaring and everyone was bidding crazy prices just to get a hydraulic fracking rig to show up on their well site (fracking usually requires a bunch of pumping trucks to line up and work one well). They were put together to quickly build up a pumping fleet to take advantage of those high rates for hydraulic fracturing equipment, and that looked really exciting for a very brief while… but then things went downhill fast as the oil market collapsed in 2014 and 2015, and the stock cratered and C&J (which used to have the ticker CJES) ended up filing for bankruptcy in mid-2016.

[7]This is a stock I had on my watchlist five or six years ago, back when oil was soaring and everyone was bidding crazy prices just to get a hydraulic fracking rig to show up on their well site (fracking usually requires a bunch of pumping trucks to line up and work one well). They were put together to quickly build up a pumping fleet to take advantage of those high rates for hydraulic fracturing equipment, and that looked really exciting for a very brief while… but then things went downhill fast as the oil market collapsed in 2014 and 2015, and the stock cratered and C&J (which used to have the ticker CJES) ended up filing for bankruptcy in mid-2016.

They emerged from bankruptcy not long after[8], and started trading again about two years ago — briefly reaching $40 as investors were enthused about their clean new balance sheet (and newly more confident in oil prices, after WTI crude had gotten above $50 following the 2016 washout into the $20s).

It has turned a bit uglier for CJ since that happy return to the markets, however — oil spiked back above $75 for a brief moment this past summer, and yet CJ shares kept slowly drifting down. They bounced off of their December 24 low, like most stocks have, but still sit at what must be a very disappointing $16 for those who were excited about the recapitalized company two years ago.

So in case you’re checking the math, yes, the stock “tripling” from here would mean that… it gets back to the price it traded at when it emerged from bankruptcy two years ago.

What, then, is the deal with CJ? Operationally, it’s more or less the same company it was five years ago, with a few acquisitions along the way. They’ve just had a little time — and bankruptcy reorganization — to help them absorb the very poorly timed expansion in 2013 and 2014, including the acquisition of much of the old Nabors (remember them? They were hot stuff in oil services 10-15 years ago).

And, to be fair, the decline in CJ shares is absolutely in line with the rest of the industry over the past two years — this isn’t just a fracking problem, or just a CJ problem… here’s the chart of CJ compared to OIH, the VanEck Oil Services ETF (and crude prices):

[9]

[9]

Though since we first looked at this pitch on January 24, things have diverged in a “not good” way — here’s what the price of oil (WTI, in blue) has done, surging higher and taking the oil services (OIH ETF in orange) with it… but little C&J Energy Services (CJ, in red), despite its better balance sheet, has fallen further still.

[10]

[10]

So rising oil prices hasn’t been enough to get folks excited about CJ this year. How about this “infinite oil” business? Does CJ have some “magic” that makes oil wells “infinite?”

Well, I’m not a geologist or an oil expert, but I think the only rational answer to that question is “no.” They do have some patented technologies, like pretty much all makers of oil services equipment, but they do not have the capability to instantly make oil wells that extract 3% of the potential oil in place suddenly capable of extracting 97%.

I can only assume that’s a hyped-up reference to just “technology keeps getting better” and the work that CJ and lots of other providers do does continue to improve oil extraction — better casing, better coiling, better fracking, more efficient targeting and computer control, better chemistry and techniques for re-fracking and stimulating wells… everything keeps getting better and more efficient, but there isn’t one “breakthrough” that someone owns that would suddenly make old wells new again, or create a new revolution in hydraulic fracturing that’s dramatically better than what anyone else is doing. My impression is that it all gets better over time, and no one owns the future — if they did, someone would buy them out (CJ is only a $1 billion company at this point, and they don’t have any debt).

Even insiders don’t see a revolution coming, it appears — from the data I skimmed it looks like they have been steady sellers of the stock they get granted each year, but no insider has bought shares since they emerged from bankruptcy two years ago (and that points to some wisdom on their part, all those sales were at prices far above the $15-16 range the stock is in right now). And yes, in case you’re wondering, the key executives have shuffled around some but have largely been with the firm through the bankruptcy and rebuilding, and mostly have 30+ years of experience in the industry… I didn’t do the math, but you can easily get “210 years of experience” out of their resumes.

So what’s going to happen from here? I don’t know, of course, just like I don’t know whether higher oil prices will eventually soak up the excess capacity created in 2014 and spur another surge in drilling and completing activity, or if oil prices will dip further on global growth[11] fears.

On the positive side, CJ has quite a bit of flexibility because they discharged that debt in bankruptcy and haven’t done any real borrowing since… they can let their fracking fleet sit idle when prices are too low for them to operate profitably, as they appear to be doing to some degree (fracturing is still almost half of their revenue — the huge truck-borne pumps and associated equipment that get moved around to frack wells… it’s an expensive service when the available equipment is all in use, but gets cheaper when trucks are idle, and oil companies are also likely to invest more in more aggressive fracturing services when oil prices are higher).

And they also won’t be paying taxes for quite some time, thanks to their historical operating losses that they can harvest… and they say they’re buying back stock, too, a luxury they didn’t have when they were buried under $1.4 billion in debt. It’s still not helping the stock, but perhaps it will in the future… particularly if oil prices go up. You can get a decent view of how the company is currently operating (and how they see themselves) from their February investor presentation here[12].

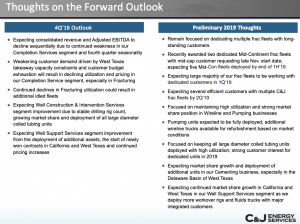

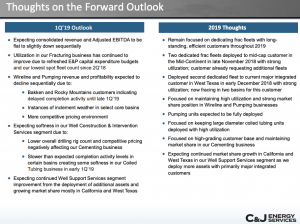

My take from their previous presentation (November)[13] was that the fourth quarter would probably show continued decline, but that 2019 might start looking a little better as they anticipate improving their market share and getting a more stable fleet under contract, including some fracking trucks that they’re going to upgrade, partly by putting more of their fleet under exclusive contract with specific oil producers (instead of just doing one job at a time), but the guidance didn’t really improve when they updated investors in February.

Here’s that forward-looking assessment from the November presentation, just FYI, followed by the assessment published with their last quarterly presentation in February:

[14]

[14]

[15]

[15]

Analysts (other than Matt Badiali, perhaps) are more pessimistic — they predict some continued ugliness, going from 81 cents in earnings per share in 2018 (that’s adjusted earnings, ignoring the big writedowns they took on goodwill in the fourth quarter, and on retiring some equipment) to a loss of 97 cents in 2019 (2019 estimates have been coming down, too, back in January analysts were expecting only a loss of 79 cents), on falling margins and revenue that will fall by almost 10%… though they think we’ll be back to 2018 sales levels plus a little bit in 2020, and will return to profitability. I would assume that future optimism is at least partly based on new pipeline capacity in the Permian coming online late this year and in 2020, which might help spur demand for completions (Permian shale producers are offtake-constrained right now — there isn’t enough pipeline capacity to get their oil and gas to market hubs or the Gulf Coast for export, but new pipes are under construction now) … and, of course, no one knows what the oil price will be in six months, and that should be a driver for all the oil services companies as well.

Other big players have been warning of tough times ahead in US shale oil, and that’s certainly been increasing the pessimism level (Shlumberger’s CEO, for example, said in January[16] that “I think it’s going to be a fairly tough year in North America” and indicated that growth in US shale oil is likely to slow down a lot).

I have no idea how it will work out, of course. Leading up to the original publication of this teaser pitch (and our solution) in January, CJ had traded almost perfectly in line with oil prices for six months, with no real sign that investors were choosing one drilling/completing/fracking company over another even if CJ might look slightly better than other small players and have a better balance sheet than most… so I guessed that CJ would go wherever oil prices told it to.

That didn’t turn out to be true — the shares of CJ diverged from the bullish move in oil prices in late February, right around the same time that they reported their 2018 earnings and caused analysts to downgrade the 2019 forecasts (oil services in general also failed to participate in the WTI oil price rally over the past two months, so it’s not just CJ).

Apparently a rising oil price isn’t enough, I guess we’ll also have to see some fundamental improvement in terms of orders and utilization and prices — and we’ll hear next from CJ in a week, on Tuesday morning, May 7, before the market opens.

Given the fact that the larger Halliburton (HAL)[17], which is also focused on the US shale business, was pretty pessimistic about 2019 when they reported last week (and saw its shares drop as a result), and even-larger Shlumberger (SLB) noted that their only real near-term optimism was overseas (where CJ has no presence), I wouldn’t expect miracles from this next quarter for CJ… but you never know, the Permian is the big driver of activity and things could pick up there later in the year and in 2020 when more pipeline capacity for actually bringing oil to market comes online, and the oil services business goes through savage boom and bust cycles and pricing can shift very quickly when demand for equipment surges.

So what do you think? See oil surging again, improving profitability for oil services companies and helping CJ stand out again? Think growth fears will keep all the oil services stocks looking ugly? Let us know with a comment below. (We’ve left the comments from the first version of this article attached, so you can see if any of your fellow readers could predict the future back in January.)

- Matt Badiali: https://www.stockgumshoe.com/tag/matt-badiali/

- Real Wealth Strategist: https://www.stockgumshoe.com/tag/real-wealth-strategist/

- oil: https://www.stockgumshoe.com/tag/oil/

- fracking: https://www.stockgumshoe.com/tag/fracking/

- oil services: https://www.stockgumshoe.com/tag/oil-services/

- to start 2018 : https://investors.cjenergy.com/2018-05-03-C-J-Energy-Services-Announces-First-Quarter-2018-Results

- [Image]: https://www.stockgumshoe.com/wp-content/uploads/2019/01/fracking.jpg

- emerged from bankruptcy not long after: https://investors.cjenergy.com/2017-01-06-C-J-Energy-Services-Successfully-Completes-Financial-Restructuring-Emerges-From-Chapter-11-Bankruptcy-And-Adopts-Stockholder-Rights-Plan

- [Image]: http://ycharts.com/companies/CJ/chart/#/?maxPoints=850&legendOnChart=true&securityGroup=&useHttps=false&securitylistName=&splitType=single¬e=&annualizedReturns=false"es=true&useEstimates=false&correlations=&format=indexed&units=false&securities=id:CJ,include:true,,id:I:WTICOSNK,include:true,,id:OIH,include:true,,&title="eLegend=true&annotations=&partner=&endDate=&zoom=custom&scaleType=linear&source=false&recessions=false&displayTicker=false&startDate=01/13/2017&securitylistSecurityId=&calcs=id:price,include:true,,

- [Image]: http://ycharts.com/indicators/crude_oil_spot_price/chart/#/?legendOnChart=false&annotations="es=false&useHttps=false"eLegend=true&splitType=single&endDate=&startDate=01/24/2019&correlations=&format=indexed&zoom=custom¬e=&securityGroup=&maxPoints=850&calcs=id:price,include:true,,&securitylistSecurityId=&units=false&partner=basic_850&source=false&dateSelection=range&annualizedReturns=false&displayTicker=false&useEstimates=false&scaleType=linear&title=&securitylistName=&chartType=interactive&recessions=false&securities=id:I:WTICOSNK,include:true,,id:OIH,include:true,,id:CJ,include:true,,

- global growth: https://www.stockgumshoe.com/tag/global-growth/

- their February investor presentation here: https://investors.cjenergy.com/download/2019.02.25_Management_Presentation_%28Post_4Q18%29_vF.pdf

- their previous presentation (November): https://investors.cjenergy.com/download/2018.11.26_Management_Presentation_vFINAL.pdf

- [Image]: https://www.stockgumshoe.com/wp-content/uploads/2019/01/CJNov18outlook.png

- [Image]: https://www.stockgumshoe.com/wp-content/uploads/2019/01/CJFeb19outlook.png

- said in January: https://www.wsj.com/articles/shale-growth-slowing-oil-field-services-giant-says-11547832801

- Halliburton (HAL): https://www.stockgumshoe.com/tag/hal/

Source URL: https://www.stockgumshoe.com/reviews/real-wealth-strategist/americas-infinite-oil-well-matt-badiali-teases-that-revolutionary-new-technology-could-unlock-a-potential-70-trillion-windfall/

Travis, you nailed this one. C&J will continue to trade in line with WTI. Watch to see if they bring back up any of their sideline frack fleets. I think activity for Frackers will be flat to down Q4 to Q1.

I’m doubtful of C&J doing anything other than tracking the index, as it has done in the past. If it had showed an ability to outpace the index, over ANY time period, I might be more open. If I am going to bet on an oil company, I would choose the “endless oil well” of Pioneer ( PXD). They have unlimited reserives in the Permian Basis- the biggest field in the US.

Thanks for your assessment on CJ Travis. I researched this area for opportunities a while back and found what may be a good sleeper here, symbol XCOOQ, an old company soon to be coming out of bankruptcy and they are currently making good profits and they own tons of acres of land leases in the Primerian basin. You may want to look into it.

I made a big mistake subscribing to Matt Badialis Front Line Profits.

I down 10K following his stock picks, he rename it to Side Line Losses.

No more Matt Badiali for me, he may be a great geologist but he sucks at

picking stocks to buy!

not really

From what I read, electric vehicles are selling better (yes, I read the one where you can’t give a gasoline car away in 10 years). But for now, I see a down hill trend.

Don’t hold your breath—the Chi-Coms own all the operable rare earth mines including brokering child labor in the Congo for Cobalt. Between personal electronics and EV projected supplies will soon be come very scarce. Did you watch the Indy 500, the Monaco Grand Prix and the Coca-Cola 600 over the past week? AIN”T GONNA HAPPEN in this Century.

An EV Uber-type car service in Montreal just went belly up—you see EV don’t run well or at all in the coming ICE AGE!!

CJ might be a good company, but Argus Research and Ford Equity have sell ratings on the stock.

It appears that Travis did not uncover evidence that this company has an industry note worthy tech advancement to support the claims. BS.

CJ may clearly have a preferred status with its customers so I would put it on a watch list if oil prices move the services industry as Travis stated. Even a 25% growth rate

would move this stock.

Travis, I suspect we will see breakthroughs in recovering currently unrecoverable oils. My guess is that it will come in the form of controlled chemical burns which generate steam to power small turbines for long periods of time….not better fracking capacity.

$70 trillion is kind of a big number. Just how they will come upon that revenue isn’t explained very well. I don’t buy the 97% of oil left in the well either. It may take 10-20 years or longer, but many of these oil fields see 30-40% of reserves extracted. Sure, there is much room for further extracting methods to be invented, but there is no company that will magically reap $70 trillion in any of our lifetimes. And if liberals get their way, we will be walking or riding bicycles, not driving gas consuming cars.

Have you heard that Venezuela heavy oil shipped to US gulf refineries is down to 300,000 barrels/day from 500,000 and may get cut much, much more due to the Communist leader. US refiners say they need the heavy oil to produce diesel fuel. What idiots, Canada has billions of barrels of heavy oil and shipping is shorter. Oopps, Socialism is the secret word for Communism from todays journalists.

I think a lot of the U.S. decisions have to do with not only logistics and economics, but also political decisions as well. For instance, a complete collapse of Venezuela would possible mean more refugees trying to gain access to the U.S. which would only increase the cost burdens placed on our welfare system. So, while the U.S. would like to see new leadership in Venezuela they probably don’t want to see a total collapse

When the speculative hype is driven out of a market, investors and traders focus on facts as prices decline. In the oil patch the big ones are interest rates (discount rates in re: inflation risk, economic growth) , Big Oil Co E&P budgets, and the price of WTI and Brent (stored supplies, anticipated demand). The innovative fracking E&P companies haven’t really proven they can get great FCF returns, to pay back their Private Equity Investors, while they have engaged in this huge experimental production model to frack the source rock of known petroleum basins in mid continent. The success of the fracking model has diminished some of the hype boosting oil prices, by taking away the fear of scarcity of oil As a commodityand the unknown future about where the next barrel is going to come from- as long as the capital is there to do the horizontal drilling and hydraulic fracking. It’s only as infinite as the cheap money.

Kind of disappointed that in the course of covering this stock no mention of the many dangers of fracking oil, and the trail of dirty waterways left in its wake. (sigh) it’s always about the money, I see. Still, I do like this newsletter very much, Travis.

Fracking causes earthquakes and home damage, https://en.wikipedia.org/wiki/2009%E2%80%9319_Oklahoma_earthquake_swarms. That shouldn’t be a problem as long as Trump remains in office and dismantles environment regulations and monitoring. But in the future, these Fracking companies may face huge class actions lawsuits. I don’t want to own any home wrecking stocks, let alone one with the potential to get sued out of business. There is always another stock to invest in, so I don’t need to think anymore about this one. Great work GumShoe.

Read Peter Zeihan, ……get educated, gotta know both sides before one states ’causes earthquakes and home damage’. Really come on.

Trump ???….. in 2013 , Obama gave a speech praising fracking , and our new energy independence………. and INCREASED new drilling permits

Back in April of last year it was at around $30 and a steady down turn to $14.90 today says it all…

Anyone think now might be a good time to buy?

Well done Gumshoe! Claims like these (can get 97% of trapped oil out) should generally be dismissed out of hand. As you correctly point out, if it were true and only one company could do it, the stock would not be at $16, but $160+. My experience with subscriptions is that they never are decent substitutes for doing your own work and applying essential critical thinking.

Thanks again!

Buck

EV stocks before Oil for me at the moment.

What about Buffetts 230 Million bet on BYD in 2008, he got 10 % ,at the time they were mainly making batteries and contract manufacturing of low end mobiles, now they are the biggest EV manufacturer in China, they just reported a 632% increase in Q1 profit YoY. https://chinadeep.info/top-10-automotive-stocks-by-dividend-yield/

Your own research is no substitute for subscriptions. Once in a while, you may subscribe an investment letter if a third party vouch its integrity and efficacy of its recommendations.

For Oil and Gas stocks, I have narrowed to OXY, COG, ENB, OKE, VLO, EPD, APC, RDS-B.

Price of Oil and circumstances change rapidly and so the list of select stocks.. Short term these stocks are expected to yield positive hits. Except ENB and EPD, I have remaining stocks in my portfolio largely for capital appreciation.

I AGREE NO SENSE WASTING TIME AND MONEY WITH A LOSER. THERE ARE BETTER FISH IN THE OCEAN LIKE 5 G….

I AM INTERESTED IN ANY INFORMATION RELATING TO COMPANIES AT THE FOREFRONT OF THE 5 G GENERATION.

YOUR OPINION IS APPRECIATED.

I REMAIN