Here’s the lead-in to the Dr. David Eifrig pitch some readers are asking about this week…

“If I had to Pour Every Single Penny of My Retirement into ONE STOCK… This Would Be It”

“And today, while it’s still at a good price, I’d like to share it with you, too.”

The ad is for Eifrig’s entry-level newsletter, Retirement Millionaire, which has tended to be pretty well-received when I hear from subscribers — from what I can tell he generally recommends mainstream, dividend-paying stocks, and tends not to get as hyperbolic as some of his colleagues. And, of course, he does say later on, in not so many words, that “putting every penny of your retirement into one stock” would be stupid.

But the hype is pretty over-the-top this time…

“Today, I’m going to tell you about “America’s #1 Retirement Stock”… for free.

“It has TWICE THE RETURNS OF TESLA (TSLA)… which last time I checked had handed some early investors over 18,000%.

“It’s LESS VOLATILE than Warren Buffett’s “Old Reliable” Berkshire Hathaway (BRK.B)…

“And even pays a dividend… FIVE TIMES LARGER than Apple’s (AAPL), actually…

“I’ve never, ever, encountered an investing story quite this compelling.

“It ticks every box and could potentially quadruple your investment in the coming years.”

Apple’s dividend isn’t anything to get all that excited about, but still, those are companies that catch your attention as comparisons… 18,000% is a pretty insane number… and who would say no to “quadruple your investment?”

So, what’s he talking about? Let’s check out the clues in the ad…

“This company is as intertwined in the “Story of America” as Ford (F) or Coca-Cola (KO)…

“And, to my knowledge, ties together more rich, successful Americans than any other stock I’ve ever seen during my four decades in the financial world.

“Folks as wide-ranging as Amazon founder, Jeff Bezos…

“One of the greatest (and most secretive) money makers in modern finance, Jim Simons…

“And yes…

“Even Joe Biden and Donald Trump.”

And we get some quotes that reinforce how unique this company is…

“Let’s begin by talking about this company’s insurmountable edge over all its rivals. It enjoys what Warren Buffett calls a wide economic moat… an overwhelming competitive advantage which protects its profits and market share.

“Even critics of this company have gone on record saying:

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...‘There ain’t any opposition out there. It’s sort of like holding a boxing tournament for a high school and bringing Mike Tyson in.’

“Its former CEO’s goal was to build a super-company… and he succeeded. And even its website is unapologetic regarding its desire for complete dominance, stating:

‘We want to win 100-0… not 51-49.'”

That “Mike Tyson” quote was not about the company, to be fair, it was about one of their products… more on that in a moment.

Other clues…

“‘America’s #1 Retirement Stock’ ranks better than 99.61% of the 258 other companies. It sits in rarefied air…

“And even though its net sales jumped 8% year-over-year…

“This Company Just Told Shareholders to Expect Higher Sales and Profits…”

And it had a fantastic year in 2022, we’re told — that was a lousy year for almost everything, so that means it pretty much has to be either an oil stock or a defense stock, both of which were buoyed by Russia’s invasion of Ukraine two years ago:

“… during a year so ugly it ranks with the Great Depression, the 2008 financial crisis, and the dot-com bust…

“This under-the-radar stock actually gained 37%…

“In 2022, it returned over $11 billion to investors…

“In the form of share buybacks and dividends….

“The dividend has grown annually by 10 and a half percent, on average, over the past decade.”

And although as we get to the bottom of the ad, we see that the pitch is a bit dated, (there’s a “September, 2023” under Eifrig’s signature line, though we’ve also gotten copies of the ad recently, so it’s still running)… I can also tell you, as luck would have it, that the stock is actually a wee bit cheaper today than it was when this ad was created six months ago. This is a pitch for Lockheed Martin (LMT), which is somewhat diversified as a defense contractor but is heavily reliant on selling high-end fighter planes, primarily the F-35 Joint Strike Fighter, to the US government and our allies.

And yes, Lockheed’s previous fighter jet, the F-22, was indeed without peer… and I suppose the F-35 probably is, too. Here’s the quote from Williamson Murray, in context, this is from Andrew Feinstein’s 2011 book The Shadow War: Inside the Global Arms Trade, from a section about the stalled F-22 program (which eventually dropped from a planned 380 or so units to an eventual fleet in service of 186 when the last planes were delivered in 2011 — which is, at the very least, a reminder that plans change, and even major weapons programs need a strong political constituency to thrive, and preferably a clear “need” or opponent to counter):

“Efforts to promote the plane as a critical tool in the War on Terror floundered when [Defense Secretary] Gates said in 2008: ‘The reality is we are fighting two wars, in Iraq and Afghanistan, and the F-22 has not performed a single mission in either theater.’ In fact, it has never been used in combat. Williamson Murray of the Army War College believes that ‘The F-22 is the best fighter in the world, no doubt about it. But there ain’t any opposition out there. It’s sort of like holding a boxing tournament for a high school and bringing Mike Tyson in.'”

Not that this is a terrible thing, overwhelming dominance (and therefore deterrence) has been the mantra of the US military for decades… but sometimes the expensive weapons programs that can’t clearly justify their cost do eventually die.

This is a big company: Lockheed Martin has a market cap of about $100 billion, so it’s a hair smaller than RTX Corp. (the former Raytheon, ticker RTX) and Boeing (BA), and a bit larger than Northrop Grumman (NOC) or General Dynamics (GD). I don’t know where Eifrig gets his “better than Tesla” returns claim here, LMT has indeed been a better investment than Tesla over the past 2-3 years (TSLA is currently down about 50% from its April 2022 peak, so that’s not saying much), but has not had gains anywhere near Tesla’s 18,000% return over the past decade or so. Maybe he’s just getting crafty with words, or perhaps there’s some more extreme returns lurking in Lockheed’s history (many of the big defense contractors have consolidated over the past few decades, and Lockheed Martin used to be Lockheed Corp. and Martin Marietta, the two merged in 1995).

Here’s how those major defense contractors have performed as investments over the past 30 years… LMT (blue) is up there, though falls a little short of GD (green) and NOC (brown), even embattled Boeing (BA, pink) has almost kept up with the S&P 500. Only Raytheon/RTX (purple) has been a major disappointment among those giants.

I guess there is something to be said for those cost-plus government contracts and $500 toilet seats… and a reason why folks persist in referring to this particular industry leader as “Lockheed Margin.”

Lockheed pays a dividend of almost 3%, and has raised the dividend annually for many years (most recently by 5%, so the dividend growth has been slowing down from the average 10% or so of the past couple decades). And if we go back to just the last defining moment for the defense industry, the Russian invasion of Ukraine in early 2022, LMT has actually been among the worst performers of the defense giants — here’s that same group of companies if we start our chart on February 24, 2022, the day Putin’s invasion began:

There’s still a lot of attention on defense spending, and it seems pretty safe to assume that the world is in a period where nobody’s feeling like a “peace dividend” is around the corner — Europe is worried about Putin, Japan and the US are are worried about China (though they’re not quite as worried as Taiwan), and there seems little likelihood that the US will be relinquishing its role as the world’s policeman… or, if you prefer, the Arsenal of Democracy. The US has had dramatic defense spending for years, and it has generally been climbing steadily since the brief “peace dividend” window that came after the fall of the Berlin Wall and the first Iraq war, and there’s been no real push to reduce defense spending in any meaningful way since the 1990s — everyone’s got defense suppliers in their Congressional district, “support the troops” is a very popular saying, and both sides of the aisle seem quite convinced that preparing for the potential threat of a more ambitious China is critical (defense spending ended up dropping after the Cold War, even through the first Iraq War, and defense companies consolidated like crazy to get us down to the current “big five” prime contractors and cut the effective overhead of the defense industrial base, but spending started picking up dramatically again after 9/11/2001, and has never looked back since). Those changes don’t necessarily come quickly or dramatically, though, and the defense budget isn’t somehow being doubled next year — the big difference since the Ukraine invasion has been the changing assumptions about European defense spending, as more NATO countries seem likely to come close to meeting their defense spending commitments for the first time in decades.

And while there’s a lot of selling back and forth among the US and its allies, that has led to much bigger moves for the European defense contractors like Leonardo (FINMF), Rheinmetall (RNMBF), BAE Systems (BAESY) and Thales (THLLY), here’s what that chart looks like if we add those four (which have Italian, German, British and French origins, respectively), those four lines at the top dwarf the recent returns of the US defense leaders:

euro-defense-leaders.jpg">

So Lockheed Martin is an interesting idea, it’s trading at the low end of its historic valuation range, at about 15X earnings, and that’s probably mostly because analysts expect earnings to be pretty flat over the next few years — the current forecast is that revenue will grow from last year’s $67.5 billion to about $74.3 billion in 2026, which would be average revenue growth of about 3%… but that their earnings per share will grow by an average of only 1% per year over those three years (falling this year, then rebounding a bit). That’s also roughly what Lockheed Martin did from 2020 through 2023, so I guess it’s a reasonable assumption, though it could be that their larger buyback authorization will help to boost per-share growth above those analyst estimates (they approved a $6 billion buyback last Fall, and have been doing a lot of buybacks in general — they have reduced the share count by 25% over the past ten years, partly funded by debt, so that’s been a major part of the shareholder return).

And yes, Lockheed has been a big US company, and a big part of American industrial production, for a very long time — with some interesting anecdotes from its history, including the one that Eifrig uses to lure subscribers into the ad, the story of how they camouflaged their Burbank, California factory after the Japanese attack on Pearl Harbor. Here’s hoping they won’t have to do that again.

Anything else stand out from the teaser pitch? If you go by five-year beta, then yes, Lockheed Martin is less volatile than Berkshire Hathaway (BRK-B) — that really just measures how correlated the stock is to the market, so LMT has a beta of only about 50%, while Berkshire Hathaway is close to 90%. No surprise there, Berkshire pretty closely tracks the S&P 500 on any given day, but I was surprised that LMT was only 50% correlated to the market over that time period. That’s fairly low for a very large company, though the beta is in the same ballpark as General Dynamics and Northrop Grumman… doesn’t necessarily mean anything if you’re a long-term fundamental investor, but it’s interesting.

And yes, he does eventually get to the “better than Tesla” return — that means you have to go back to the 1970s, before it was Lockheed Martin, Eifrig notes that the company has gone up 46,763% in ~50 years. I haven’t checked that data, and don’t know whether that’s based on buying Lockheed Corp. or Martin Marietta just after the Vietnam war, but I imagine it’s accurate. The total return for shareholders who bought immediately after the Lockheed Margin merger in 1995 would be about 3,250%, so that would be a return of about 12% per year. Better than average, the S&P 500 total return for those 30 years is almost exactly 10% per year — though the outperformance really came from 2014-2020, which I guess was probably the prime spending rampup period for the F-35.

Eifrig’s general theme here is summed up pretty nicely here:

“What If Our Government’s Reckless Spending Could Make You Richer? …

“I’m appalled by how debt-ridden our country has gotten on their watch. Of course I am.

“That said…

“As an experienced investor… all I see is opportunity.

“And, right now, one corner of the stock market stands head and shoulders above all others….

“Nobody is rooting for war.

“I far prefer the idea of living in a peaceful future where our common humanity and right to privacy is respected. But that doesn’t seem like the way things are going.

“So let us be clear-eyed individuals for our families… and put our money to work where capital is flowing, right now… particularly billions of dollars worth of government-promised capital.

“Clearly, it’s flowing into the defense sector… and a select few companies which I’ll tell you about in a moment.”

And beyond Lockheed Martin as that “#1 Retirement Stock,” he does hint at a few other defense industry stocks he thinks you should buy, so let’s see if we can ID those for you, too… here’s the tease:

“After exhaustive research, I’ve identified a shortlist of companies which look set to grow even more in the very near future… and their stock prices are a fraction of “America’s #1 Retirement Stock”.

“…One company is a virtual “monopoly” and is the US Navy’s key supplier.

“Another one – an under-the-radar company operating out of Rhode Island – is carving out a hyper-profitable niche in the aviation business… and might just have built the world’s next great war machine…

“And a third company is one of the biggest beneficiaries of a secretive Pentagon meeting of the defense industry’s most important figures… now known as the ‘Last Supper.'”

That “virtual monopoly” is very likely to be Huntington Ingalls Industries (HII), which has a monopoly over the construction of and refueling/refurbishing of the Navy’s fleet of aircraft carriers. They do other things as well, including hulls for submarines and destroyers, and have been coming out of a balance sheet restructuring and trying to restart growth a bit, with the likelihood of improving cash flow over the next few years. I started buying the stock a little over a year ago, largely because it was trading at a pretty meaningful discount to its larger defense industry peers but had a more defensible and longer-term guaranteed revenue stream because of the 50-year life of aircraft carriers and the need to essentially be building one new carrier and refurbishing another at all times in order to maintain the fleet. Politicians love aircraft carriers, and they are the primary usable extension of US power globally, so the future seems pretty predictable… and investors like predictable.

That may well also be true of LMT and the F-35 and whatever major weapons programs follow that, or, for that matter, Northrop Grumman and its B-21 bomber program, or General Dynamics and its Abrams tank… but there’s a lot more uncertainty when you’re dealing with those shorter-term programs, if only because competing designs and similar products are often feasible, and Boeing or someone else might get a bigger slice the next time the program is revamped. We might cycle through several refreshes of fighter aircraft over the next 30 years, but we can be pretty certain that the aircraft carrier HII is starting to build right now will be back for its expensive mid-life retrofit and refueling 30 years from now, and nobody is building a new shipyard in the US that can do this work (that could change too, I assume, but it would probably take a war — the US has almost no shipbuilding capacity beyond the current naval shipyards, period, and there is only one shipyard in North America that can work on aircraft carriers).

HII is the only defense stock I own right now, and it’s been on a tear of late so it’s at a price above what I’d prefer to pay, though it’s still pretty easily justifiable (I’d hesitate to pay more than $260-270, and the stock is around $290 at this point, but if we’re willing to believe that their turnaround is going to really accelerate earnings over the next few years, as company management says, you can probably get away with paying up to 20X earnings, which would be around $340). I think they’re likely to have a steady future, with the long backlog of their aircraft carrier and submarine contracts, and will probably outgrow most of the large defense companies over the next few years (HII itself is not very large, with a market cap of only about $11 billion, so growth is a little easier to come by, and they have been making inroads into non-shipbuilding work, too — it was actually created as a spinoff from Northrop Grumman a little over a decade ago, just FYI).

And our “under the radar” company in Rhode Island is presumably Textron (TXT), the only defense contractor based in that tiny state. Textron is still primarily a commercial aviation company, they sell the Cessna and Beechcraft planes and Bell helicopters — though they do get 25% or so of their revenue from the government, and they’ve got some large contracts — including, a little over a year ago, winning the lead contract to replace the Blackhawk helicopter with the Bell V-280 Tiltrotor. They have a variety of businesses, and they’re much smaller than most of the defense industry leaders (market cap around $17 billion), but the valuation looks pretty reasonable — as long as their commercial/private aviation business doesn’t collapse for some unforeseen reason, the ramp-up of growth from that new Bell defense contract should goose returns over time.

Analysts expect Textron to have $6.30 in earnings per share and to grow those earnings by about 10% a year for the next couple years, and the commercial business, particularly supply and service of the existing fleet, may give them the opportunity to gradually improve their margins… and their debt is much lower than I would have guessed, given the capital intensive nature of aerospace manufacturing, so that’s a good sign, as is their history of buying back stock over the past decade (they’ve burned more of the share count than LMT or HII, less than Northrop Grumman). The stock has jumped this month, thanks to a good earnings report in January, but the current valuation of about 14X expected 2024 adjusted earnings seems quite reasonable. TXT will probably be more volatile than the big boys, but it should also have substantially more potential to “surprise” with stronger growth.

That catches my eye a bit, though it’s a complicated enough company that I’ll have to spend some more time on this one — for now, it goes on my watchlist.

And as for the third one, the beneficiary of the ‘Last Supper’, we’d need more clues to really hazard a good guess for that one. The “Last Supper” he’s talking about was a meeting at the Pentagon in 1993, in which the Secretary of Defense essentially called in all the big defense contractors, warned them of major cuts to the defense budget for the foreseeable future (the Soviet Union was collapsing, and there were no real threats to justify major procurement programs), and they essentially were told to consolidate to survive. That led to a ton of M&A activity in the defense business, including the creation of Lockheed Martin and the acquisition of dozens of smaller contractors by the big four or five leaders.

But which one was a primary beneficiary? Well, it’s hard to say that it was Raytheon, since that’s been such a relative disaster for so long (including after buying the aerospace business from United Technologies and beccoming RTX a few years ago), but it could easily be either Northrop Grumman (NOC) or General Dynamics (GD), both of which are large and in good shape and pay rising dividends and have benefitted from consolidation — probably NOC more than GD, though Northrop is also arguably the most richly valued, at least by a hair, of the major defense contractors (and GD, like Textron, also has a commercial business with its Gulfstream jets). It could be someone smaller, too, of course — L3Harris (LHX) or Curtiss Wright (CW), aviation parts companies TransDigm (TDG) or HEICO (HEI), or dronemakers Kratos (KTOS) or Aerovironment (AVAV).

So we’ll leave that last one unanswered… If you want to peruse some other ideas in the defense industry, it might be worth skimming through the article I wrote about a year ago, when Eifrig’s colleague Dave Lashmet was teasing defense stocks for his Stansberry newsletter.

And finally, Eifrig throws in another “special report” tease, called “How to Hire a Lobbyist for your Portfolio” — again, this is a “I hate wasteful government spending, but we might as well profit from it” argument… here’s what he says…

“‘Portfolios of firms with the highest lobbying intensities significantly outperform their benchmarks…’

“You Can Either Invest Alongside These Insiders… Or Go Against Them

“Again, we need to deal with the world as it is, not as it should be.

“And this model portfolio features four of the most lobbied stocks in the world. They have returned as much as 79%…184%… 225%… and 1,196% since I added them to our portfolio.”

I have no idea when he picked those stocks, so it’s hard to gauge whether those are great returns, but there is certainly an argument to be made that the firms which spend the most on lobbying — including lots of healthcare, technology, and, yes, defense companies — do indeed get a good “return” on that investment. If you want to buy into that idea, you can either consider some of the other very large government contractors, like Booz Allen Hamilton (BAH), Leidos (LDOS) or CACI International (CACI), or big health insurers like UnitedHealth (UNH) and their ilk… or you could go the easy route.

Yes, there’s a “who’s the biggest lobbyist” ETF, the Strategas Global Policy Opportunities ETF (SAGP), which says it “uses publicly available lobbying data to consider investments in both domestic and international companies set to benefit from periods of intense lobbying of the U.S. federal government.”

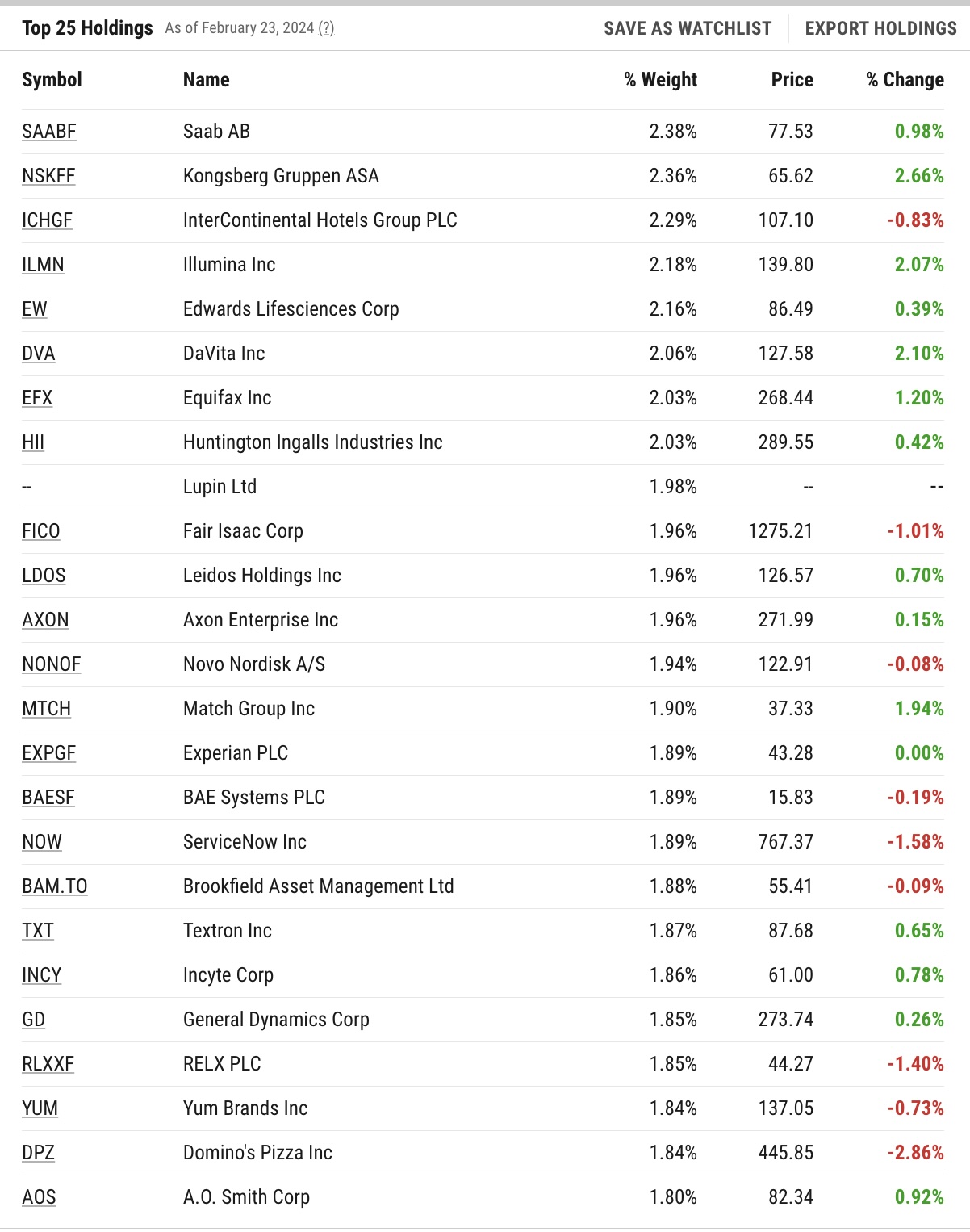

The top stocks in that portfolio aren’t the ones I would have guessed, frankly, and the ETF has been around for less than two years so there’s not much indication of what the performance will be like (it has mostly tracked pretty close to the S&P 500, though hasn’t kept up with the latest surge of tech-stock excitement so is currently trailing by a bit). Here are the current holdings of this actively traded ETF, in case you want to go fishing in this pool… gotta say, I didn’t expect to find Brookfield or Domino’s on this list, but I guess they’re as interested in “massaging” government regulations as anyone else:

So… any of these beneficiaries of government spending float your boat, from Lockheed on down? Have a favorite way to invest in the current interest in defense spending? Let us know with a comment below.

Disclosure: Of the companied mentioned above, I own shares of Huntington Ingalls Industries, Domino’s Pizza, Brookfield Asset Management and Berkshire Hathaway. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Strategas Global Policy Opportunities ETF (SAGP)

Holy Smokes!

That’s just like the super right-wing State of Alaska –

living off the federal tit!

(plus some oil money)

I wonder what MTCH is lobying for.

Less regulation of internet lying, maybe?

Could have been looking for regulatory leverage over the app stores, their fees to Apple and Google were massive before the cracks in the App Store payments oligopoly started to appear.

That makes sense.

What’s the Alaska connection? Not obvious to me from that list.

Money spent on lobbying, being seen as more important than doing useful work.

I had not thought about an ETF for lobbyists who squeeze the government for our money. Considering all the money grabbing that goes on I thought there were be more than 5 companies in this ETF: https://www.strategasetfs.com/sagp

Is there a search engine for ETFs?

Those are just the top five holdings, in case you’re curious, you can click through and download the whole portfolio on that page if you’d like to — the ETF holds about 100 stocks.

There are a bunch of ETF search systems — including Morningstar, ETF Database (etfdb.com) and ETF.com

I confirm LMT is Doc’s #1 stock to buy. Special report to Retirement Millionaire subscribers last November 2023

Thanks Clay. Do you like it yourself?

I just stumbled across another ETF that might go well with SAGP.

The Unusual Whales Subversive Democratic Trading ETF (NANC) is an exchange-traded fund (ETF) that tracks the performance of influential members of the Democratic Party in the United States. These individuals are often referred to as the “unusual whales” of the party.

It has only been around for a year but has gone from around $24 to $33 in that time.

LOL, wonder how they track that. I’m under the impression that disclosures of politicians’ investments aren’t very good or consistent. They have versions of the ETF strategy for each party, looks like NANC is doing better than KRUZ so far 🙂

That’s awesome! And here I am following Quiver Quant (for entertainment purposes only 🙂 )

Checkout

https://www.dubapp.com/

They appear to match portfolios