Today we’re releasing an old Friday File for all of our free readers (and as a reminder for any Irregulars who missed it the first time around) — this ad has been running off and on for a long time, but we covered it on July 10 and the article below is not updated. The story is still essentially the same, and the versions of the ad that I’ve seen are the same — the company has reported one additional quarter now, with continued progress more or less on the same pace they were showing in the prior quarter (ie, continued unit growth, sales growth, and expense growth, no huge boom in installed base yet, and nowhere near sales that are large enough to absorb their selling expenses, overhead or R&D costs).

So… it’s still a story, still interesting, still all about the future and how you see it… with that, I’ll leave you to it.

—from 7/10/15—

Today, for your Friday File pleasure, I don’t have any portfolio updates or changes to talk to you about so I thought I’d take a quick look at a tiny little robotics company that’s being teased (again). I’ve never written about this one before, but it has come up in reader discussions from time to time — probably, in large part, because the technology is “cool” and has gotten a lot of attention in the press, and because Keith Fitz-Gerald over at Money Morning has been an ardent fan since at least last Fall.

This pitch isn’t from Fitz-Gerald, though, it’s from Jim Pearce over at Investing Daily, in an ad for his Smart Tech Investor newsletter. This is a $49 newsletter, so it’s one of those “entry level” inexpensive letters that the publishers use to generate a pool of potential customers for their more profitable $200-$5,000 letters… and that means they’re taking some chances here, because they’re talking up a microcap stock (market cap around $100 million) for what is intended to be (though I don’t know what their circulation is) a mass-market newsletter, which sometimes results in a stock that reacts much more to the newsletter’s attention than to the actual fundamentals of the company.

Maybe that’s for the best, though, as the “fundamentals” for this one are, though enticing and promising, quite future-oriented. That’s a nice way of saying that the current valuation is ridiculous based on their achieved results, so current investors are clearly anticipating something much better in the future.

So what’s the stock? The one being touted here by Pearce is Ekso Bionics (EKSO), which is one of a handful of companies trying to develop powered exoskeletons. These are primarily in demand right now in the health care and rehabilitation sectors, where $100,000 robotic legs can help people walk (or, at least, start to learn to walk) after injury or paralysis, but a fair amount of the R&D funding is also coming from the military, which in addition to being interested in rehab is interested in the future “iron man” potential war-fighting capacity of exoskeleton robotics (and, before that, in the ability of powered suits like these to help a solder hump 200 pounds of gear across hostile terrain after getting dropped out of a helicopter).

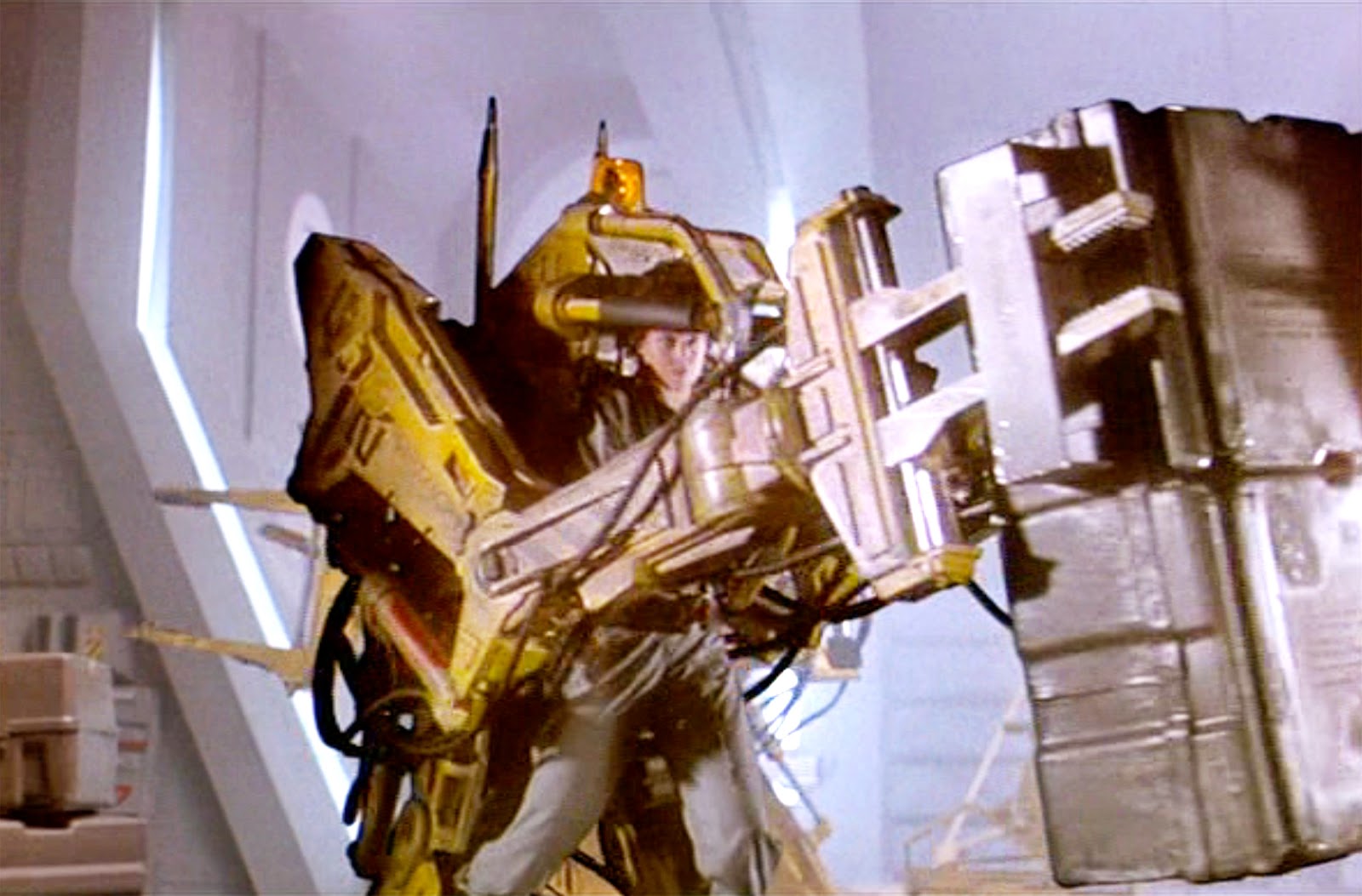

There are also industrial applications possible for this and similar products, with designs that increase efficiency and improve worker health and longevity for high-impact manual work in shipbuilding, on assembly lines, and elsewhere, including real-life versions of the robotic “loader” suit used by Sigourney Weaver in Aliens… but it appears that the healthcare and military sectors are the first big customers for exoskeletons (and sponsors of exoskeleton robotics research) at the moment.

There are also industrial applications possible for this and similar products, with designs that increase efficiency and improve worker health and longevity for high-impact manual work in shipbuilding, on assembly lines, and elsewhere, including real-life versions of the robotic “loader” suit used by Sigourney Weaver in Aliens… but it appears that the healthcare and military sectors are the first big customers for exoskeletons (and sponsors of exoskeleton robotics research) at the moment.

So what’s our pitch for Ekso? Let’s share some of the ad with you…

“The Pentagon has recruited a tiny company for a top-secret mission vital to our national security…

“A new line of contracts is projected to ignite this $2 stock… sending it soaring to $10… then to $20, all before 2015 closes out…”

And now it’s a $1.20 stock, not a $2 one, so those imagined possible returns are even more enticing… if they have any chance of coming to pass, that is. $1.20 to $20 in about six months (it’s July now, you know — 2015 is more than half over) would be returns of better than 1,500%.

Which you are almost certainly not going to get, to be clear. At least, I can see no potential for that kind of return — this is a product that has been developed over decades of iterative advancements in robotics, batteries, microcontrols and other areas, it’s not going to suddenly become mainstream overnight and generate ridiculous returns in six months. My lustful lizard brain wishes for huge gains like that, of course, but the rest of my noggin tells me to be much more cautious — maybe five years, if their development goes well. This strikes me as a 2020 story, or 2030… not 2015.

And there’s no guarantee that Ekso is going to end up being the strongest story in the space — the similarly sized ReWalk Robotics (RWLK), which went public recently, is working on very similar products for “mobility enhancement”, and both of those $100 million companies — who may have a small lead, since their products are already FDA approved for clinical use — are no doubt keeping a close eye on Activelink, which has the backing of leviathan Panasonic and is pushing the development of much cheaper lower-end exoskeleton/strength enhancement wearables, and on Parker Hannifin’s Indego, which is aiming to get FDA approval soon and claims some advantages over Ekso and ReWalk (including substantially lower weight and cost, if the published reports are true). And there may well be others which which I’m unfamiliar.

Here’s some more from the ad, which focuses a lot on the military applications:

“Thirty-three miles from Silicon Valley…

“In the same warehouse that once rolled out cutting-edge tanks, cars and planes for World War II…

“And where Ford once built the ‘Arsenal of Democracy’ that saved the free world…

“Now sits a critically important research lab… the epicenter of the next big military revolution.

“It’s here where the Pentagon is bankrolling a top-secret program, one the Wall Street Journal claims ‘could change the way the U.S. military fights wars.'”

The Pentagon has indeed been bankrolling research on exoskeleton robotics, including the HULC program being run by Lockheed Martin with contributions by Ekso, and the collaborative (including Ekso) TALOS (the TActical Light Operator Suit) program that’s described in this article.

And yes, Ekso’s headquarters are in the old Ford Assembly Plant in Richmond CA, just across the San Francisco Bay from San Quentin Prison — that plant is now partly a national historical park, part of the “Rosie the Riveter” story for its wartime use, but also hosts some private businesses, including Ekso and SunPower, among others.

"reveal" emails? If not,

just click here...

The military funding is real, and Ekso does get meaningful cash from it — but it’s really only meaningful because Ekso is so small and their other revenue so low. Their work on the military exoskeletons recently mostly consists of a $1 million grant in 2013 and a $2 million grant this year, along with some subcontracted and licensed work with Lockheed Martin (which has paid Ekso some small amount in royalties for sales of their unpowered Fortis exoskeleton to navy shipyards). This is really very early stage work, still. Ekso delivered 64 of their flagship Ekso exoskeletons to healthcare facilities last year (nine were leased, 55 sold), bringing their total installed base to 110 as of January — and they’ve hired a pretty large sales force, so they’re certainly hoping to increase those numbers… but it’s not happening overnight.

Their total revenue for 2014 was just over $5 million, and so far in the first quarter they’ve increased sales a bit, by about 50% over the same quarter last year… but they also increased their share count by about 50%, so the price/sales number is about the same. This is not a financial story, and not a company you can get excited about based on their proven ability to sell the Ekso suit into the healthcare business — to buy it, you really have to believe that their intellectual property is core to exoskeleton development overall (which is probably a hard case to make, given the many different companies working on designs that use slightly different technology, though I certainly don’t know the patent universe in this area), or that their medical/rehab sales will rise dramatically from here or that, at some point over the next several years, they will get substantially larger grants or project development contracts from the Defense Department. All are probably possible, I have a hard time seeing them as likely — just my opinion.

If you’re curious about the bull case, you can also see most of Keith Fitz-Gerald’s commentary on Ekso here — including his piece responding to the recent short attack on EKSO here.

Short attack, you say? Yep, as is probably not shocking for a $100 million company that came public in a reverse merger, with very little revenue, and with shares that trade over the counter, you can make a pretty good short argument about EKSO (short meaning, “you think the stock will go down”) — and if you use the short-seller’s tricks and exaggerate the negatives and distribute your negative opinion widely, you’ve got a decent chance of being able to scare enough folks out of a stock that the shares fall, a self-fulfilling prophecy. It works on the long side, too, of course — that would be a “pump and dump” … on the short side, it’s often called a “short and distort.”

The short attack/analysis itself was made largely by a short seller who calls himself “Pump Stopper” and is posted here on Seeking Alpha, the very brief response by Ekso Bionics is here. Ekso Bionics has been, at least, somewhat ham-fisted in their self-promotion — they’ve apparently hired stock promotion firms to spread the word in the past, so perhaps getting hit with a “short and distort” attack is some kind of logical payback for that, but I wouldn’t assume that the fact that they used self-promotion and used a somewhat shady investment banker for their reverse merger (which is a big part of the short thesis) means the company is necessarily fraudulent.

I’d say they’re wildly overvalued unless you see a very rosy future for their Ekso rehab products, and they will probably raise cash in the next six months or so, but my browsing of their materials didn’t scream “fraud.” The way to profitability for them is getting these into every rehab hospital and big physical therapy operation and becoming the standard of care, and if you’ve spent a lot of time in those kinds of places you probably have noticed that there aren’t many $100,000 machines in use — probably in large part because insurance companies are not climbing all over themselves to pay extra for rehab. This is probably a tough slog for their sales force, but if it’s effective enough to really accelerate a return to walking for patients, and the technology continues to improve and the price continues to come down, there’s a future possibility of meaningful revenue.

The company is going to need to raise more money to continue to fund their R&D work, particularly since their very expensive exoskeletons are not going to immediately become large-volume sellers. This is very early days, as I noted above, and they are still on pace to sell fewer than 100 a year of these machines. They filed a shelf registration to raise up to another $75 million or so, but I would assume that they’d prefer to raise that money at higher prices if they can — the stock is down about 30% or so since the short attack (though, to be fair, it was going down before that as well).

The shares are now pretty close to where they went public, which was done through reverse merger back in January 2014 (they raised about $20 million then, and got another $20 million from exercised warrants late last year — after they agreed to revise the warrants, which came from their private placement, pre-IPO deals in early 2014, from a $2 strike price down to $1, likely because they wanted to force a quick exercise and raise more cash). They’ve been spending $3-4 million per quarter in cash, so they could probably squeak things out for another year at the current cash burn pace, but they’ll probably sell more equity to raise cash before that. Technically, that’s dilutive — but, of course, there’s precious little by way of fundamental economic results to be diluted, so you’re just seeing your equity interest in an intangible future possibility of growth and income diluted. Hard to quantify that.

So… excited by the possibility of powered exoskeletons helping people to walk again, and creating a new army of Iron Men someday? Think Ekso is the big winner? Let us know with a comment below.

P.S. Back to September now 21 again… Ekso reported their most recent quarter in August, you can see the press release here… they have now apparently sold or otherwise placed 147 machines in total, and the financials continue to show progress in sales but also an acceleration of “cash burn” as they went through almost $5 million (they have $16 million of cash left). The stock was around $1.10 when we uncovered it in July, and remained at that level after earnings but jumped up about 25% a week or two later to the current $1.40 range — not sure the reason for the surge, whether it was more newsletter attention or a move by one of their competitors or something else, but I haven’t seen any substantive news since earnings.

We’ve left the original comments from July appended below, feel free to add to the discussion if you’ve something to say about bionics, Ekso, or anything else of relevance. Thanks for reading!

Fantastic analysis. I learn more from you every week about the market than I do from any other source.

I feel like a kid strolling down the street with a helium balloon on a string and then you come along and pop it. There goes turning my 10,000 into 66,500. Thanks Travis.

also hospitals are just bursting at the seams with cash for products like this.

The edge of Tomorrow has used these prototypes in their fiction pictures. So it’s coming it’s time we give more to our soldiers. Maybe 5-10 yr’s. The gov. needs to start on this is they haven’t right now.

I have bought and sold this a few times before, as I am subscriber to Total Wealth , a free newsletter by Keith-Fitz Gerald. He claims that EKSO will be a stock $20 in 2020. You can read that analysis too in moneymorning.com

One can wait, but after that bad news in recent past on their CEO (or board member) on alleged fraudulent practices, (what Keith named as “short and dump”), I lost my confidence on this company. I still keep checking its price but thanks to Stockgumshoe.com now that I know what I will do instead.

Thanks for your insight Travis, I was getting all kinds of buggy thinking about a Robo-Cop type army. But I don’t forsee a bonanza here. I they make a move to capture health care then they may have something. Bigger companies will grab the Pentagon’s money

It won’t go from $1.20 to $20 in about six months; but I believe it will go to $20 by 2020. There is nothing wrong to buy 500 shares at $1.20 costing $600.00 and forget it for next five years. Or follow up the system “Buy Low and Sell High”, Over and over like I am going to do.

Good Luck

Roboots on the ground ?

The guy at Money Morning put the price at $20-$21 by 2020.

Thanks, Travis. I have lost tons in the past on these “We will be some day since we have the best story company” and am all most completely out. MEI did well until their last miss Q and may return to a high growth revenue company, though I cannot call the quarter.

Currently, I am long on NAT that has shown signs of high storage and daily rates for Suez max tankers. Their $0.40 dividend for a $ 16.00 stock bodes well only if the tanker daily rates stay the same or continue to go higher. It has gone from $8.00 to 16.00 and likely will go higher before the dividend is paid in August. I am looking for other companies that have been out of favor but have increasing revenue rates if any are known on this site.

Thanks, Travis for you persistent fundamental research. I have found no other even close to equal to what you provide.

Speaking of old news, what’s the latest on TPLM. I still see price targets of $6-$7. It was suppose to be a “Buy” at $5, then it became a “Buy” at $4, then $3 and now it just closed at $1.77. Will it still be a “Buy” when it gets to $.59?

As a paraplegic I have been tracking the evolving development of exoskeletons with great interest for a couple of years now. For the civilian rather than military applications. As a customer I want one now. As an investor I would steer well clear of any of these companies for the time being. The technology is a long way off, and by the time it does get ready for showtime it is anybody’s guess who the significant players will be. EKSO and it’s ilk will survive on military contracts and low volume production – but there’s no huge, quick returns to be had here. The only rationale for investing in them is as a way of “donating” to a good cause. I wish them luck, but will keep my wallet in my pocket.

Governments, including our own here in Canada have been highly criticized for failing to properly support injured veterans because of the high costs. What it says to me is the people who run wars from the safety of their own protected bunkers care little about those that risk “life and limb” to fight wars that make no sense to begin with, but generate big profits for the owners of companies supplying the hardware to blow people up. What fools we mortals be, at least turning wars over to robots might save human lives and needless suffering,