Today I’m taking a look at a Kyle Dennis ad for his Sniper Report ($97/yr), which is published by RagingBull. Haven’t looked at his stuff before, but it seemed to get some reader attention, so… digging right in.

This is what I imagine got most of the dreams of greed ignited:

“I sincerely believe it will be the easiest quadruple of my money in my entire career.

“It all centers around this cube and its connection to this metal pole.”

I didn’t copy over the image for you, but it’s basically a photo of a cellular antenna tower (the “metal pole”) and some kind of packaged microchip (the “cube”).

More from the ad:

“About 75 BILLION devices will center around these two objects. And this technology isn’t something ‘nice to have’. This isn’t a new Facebook, or, some Uber or AirBnb. This is a technology that already exists in a much smaller way—100X smaller—but it’s reached its life cycle.”

And he pitches his stock as a “picks and shovels” idea — though he uses a different metaphor:

“Instead of investing in a horse, you invested in the track and the betting circles.

“Meaning…

“No matter which horse wins the race…

“No matter which jockey holds up the trophy…

“No matter what… YOU WIN. You win a cut of the profits not just during the race, but from every race after.”

And apparently this particular cube is essential…

“If you don’t have this cube, your device will not work with the new technology. Without it, you won’t be able to interact with these metal pole-things I showed you before….

“In every single device that runs 5G… and all 5 tech giants are working on adapting products or their platform to the technology… will require this cube to communicate with these metal poles.”

So yes, he’s pitching some kind of chip or part supplier that produces something essential for 5G. More clues?

“Why this cube instead of the pole?

“With an estimated 75 billion devices about to be unleashed on 5G—that’s more than 10 per person on the planet—that’s 75 billion chips needing to communicate. If it costs a company $40 to manufacture a chip—that’s over $3 trillion dollars. If they sell it for a 400% markup or $150 which is relatively standard…that’s $12 trillion dollars in revenues.

“And that’s just for this one small cube. Entire devices need to be re-made. New products in virtual reality and IOT need to be revamped.

“Not to mention, these stinkin’ metal poles I keep showing you. Compared to the 75 billion chips we need, we will an estimated 300,000 of 5G antennas according to CBS News.”

And a few more tidbits…

“… this company isn’t a startup. They’re a $10+ billion dollar company. They’ve seen double-digit topline growth the past few years. That already signals a strong buy….

“Their profits hover under 45%. Their cash flow increased 5X in a mere four years.

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“On top of that, they’ve been buying back shares five years in a row. They were even doing that before Trump’s tax cuts.”

And he says that buyback is pretty huge…

“Companies only buyback shares when they are fully confident their stock price is about to explode.”

Uh, that’s not true. That’s what they’re supposed to do, buy back shares when they’re undervalued, but history tells us that companies are no better at telling when their stock is undervalued than anyone else…probably worse, in fact. In practice they generally buy back shares when the price is high and they’re trying to juice per-share earnings growth to keep investors happy…. or when they’re issuing tons of employee stock options and want to buy some of them back to cut the dilution so their earnings per share numbers don’t drop.

More hints?

“Forbes calls this stock a ‘good value’. And I agree. Within the next year, I expect it’ll quadruple and hand early investors a tidy fortune.”

Next time someone cites Forbes as if it’s still a reliable and edited business magazine, remind yourself that it’s now mostly a blogging and paid promotion network… good piece on that trend from Epsilon Theory here. I have no idea which Forbes article cited this “secret” stock as “good value,” or when, but, of course, you can always find a citation for someone saying that they think pretty much any stock imaginable is a “good value.”

So… what’s the stock? This is our old friend Skyworks Solutions (SWKS), which has indeed spend the past year or so positioning itself more vigorously as a “5G company.”

I stopped out of Skyworks a while back because their revenue and earnings took a hit from the fact that they were (and are) still mostly an iPhone chip supplier, and falling iPhone volumes really hurt them, but they have been clawing back this year.

The big benefit for Skyworks a few years ago, that they had a great product that got included in the iPhone, a huge win for a small company finally making the big time… has become also the biggest risk for the stock more recently. Skyworks gets roughly half of its revenue from Apple these days, and almost all of that is from the iPhone… and as a chip supplier, they don’t care how profitable Apple can remain by raising prices on phones, they only care how many phones are sold, so that has been a consistent fear for Skyworks over the past year or two: Phones are lasting longer, new models are no longer compelling upgrades after one or two years, obsolescence has slowed down, and many people are now happy to hold onto their phone for three or four years or longer.

That trend won’t get endlessly worse, of course, there will be future upgrades at some point that are genuinely compelling… and maybe it will eventually be 5G that spurs the next round of surging iPhone sales. That won’t be this year, we’ll see a few 5G phones introduced, but the networks aren’t there for them yet and the more appealing 5G use cases in this introductory cycle will likely be stationary (base stations for wireless broadband, laptops, etc), so it’s more likely that the mass market for 5G phones doesn’t really start to hit until at least 2020 or 2021, which is also when Apple will probably bring the iPhone into the 5G future.

But the good thing about 5G, as about each advancing iteration of technology, is that it needs more stuff to work. More base stations. More chips in the phones. More filters and antennas and amplifiers to handle the new radio wavelengths. And that’s the kind of stuff that Skyworks makes.

And yes, the little photo of the special cube in the ads is a SkyWorks product — the little techy-looking image on the top is part of the Skyworks logo. I grabbed a similar product image from their website here for you, just in case you’re curious.

And yes, the little photo of the special cube in the ads is a SkyWorks product — the little techy-looking image on the top is part of the Skyworks logo. I grabbed a similar product image from their website here for you, just in case you’re curious.

Skyworks’ big push is for front-end modules for cellular communications — combinations of chips that combine power amplifiers for multiple bands, switches, and filters to help phones reduce battery draw while also connecting across various bandwidths and networks, from WiFi to 4G to now 5G. I can see how these would be very popular products for developers, particularly as the world of bandwidths they have to deal with expands with the addition of 5G (all new 5G-enabled phones will still need full 4G connections for years, possibly forever), and it might be that their technology is the best (they say it is, at least), but Skyworks is not the only provider and their particular chips do not have to be used by the makers of every phone. Monopolies in semiconductors are extremely rare, and they have probably been built as much by branding (Intel in the 1980s) as they are by actual unique capabilities or patents (though that does come sometimes, with Qualcomm being a great example with their patent dominance in 2G and 3G and, to a lesser degree, 4G). I wouldn’t count on a monopoly for Skyworks.

Which doesn’t mean they can’t do well — the danger is that the stock will probably continue to be driven primarily by sentiment about Apple iPhone development cycles and sales volumes, so the pace of 5G adoption this year will probably not be as important for Skyworks investors as the popularity of whatever next iPhone Apple releases.

This part of the ad seems to be essentially invented out of whole cloth…

“If it costs a company $40 to manufacture a chip—that’s over $3 trillion dollars. If they sell it for a 400% markup or $150 which is relatively standard…that’s $12 trillion dollars in revenues.”

I don’t know where they get the $40 for manufacturing cost per chip, or the 400% markup. The best chipmakers get gross margins of about 60%, which is great, but that’s a 150% markup on manufacturing/design cost (not counting selling costs or overhead). And Skyworks doesn’t get anywhere near $40 making each chip, nor does it receive that for its most widely-used chips or for a per-phone sales number, even when, as with many iPhones, it supplies several different chips for each phone.

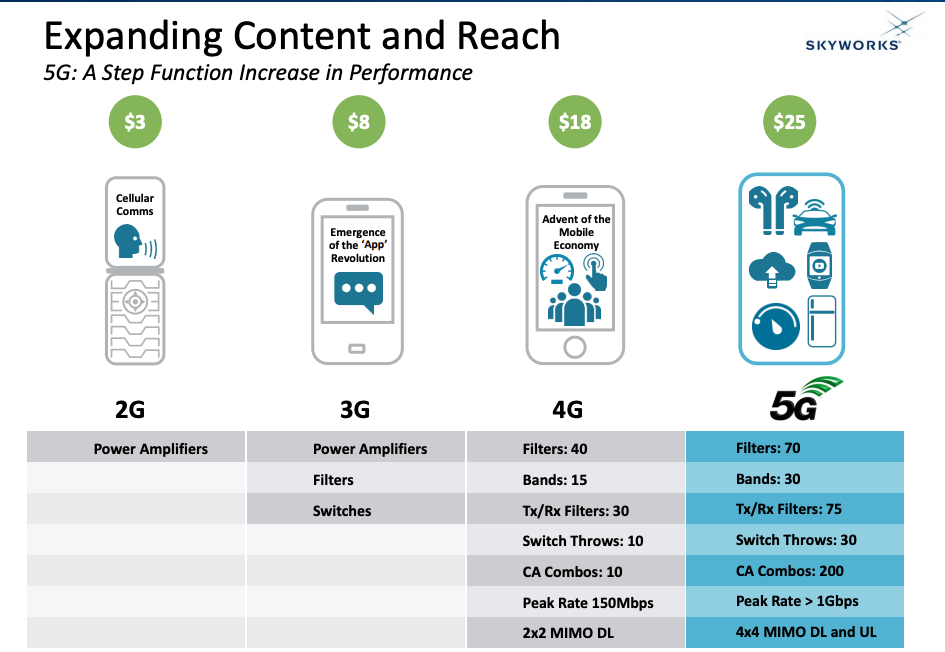

It is getting closer, though — Skyworks earned about $8 per device that included its chips a decade ago, more than doubling with wide adoption of 4G, and Skyworks is reportedly projecting that they will put $25 in content into each 5G phone they outfit. That’s a great driver of revenue growth as long as they also see increasing (or at least flat) volumes — and it’s all driven not by more advanced chips, necessarily, but by more stuff on each phone… more filters, more modules, more amplifiers.

They outline their plans in their latest investor presentation here, which might help to give you a better overview (it’s a little old, from November)… here’s a little excerpt outlining that “revenue per device” number and how it has changed with each generation:

That’s their wholesale selling price, though, it’s not their profit and it’s not their cost of production. They have pretty consistently had profit margins in the high-20s (27-30% or so).

So yes, Skyworks is hoping for substantial gains in 5G, and they have been working on advanced front-end chips for 5G devices (phones and other stuff) in addition to chips for 5G infrastructure equipment… though consumer devices for 5G likely won’t sell in big volume this year. And in the meantime, their revenue for this year mostly depends, one would guess, on how many iPhones Apple sells.

Analysts are expecting 2019 to be a pretty tough down year for SWKS earnings, dropping 10% or so from the 2018 EPS to earn about $6.60 this year, then resuming growth and posting earnings growth of about 10% next year and almost 20% in 2021. Those won’t be exactly accurate, of course, but it gives you an idea of what folks think is happening — a lull this year followed by another growth spurt as 5G and/or new phone models spur sales growth. And the stock has started to recover a bit recently, which matches that story, the share price rises not because of what’s happening this year, but because of what’s expected to happen next year.

Will it work out that way? That’s your call to make. It’s a good company, it’s rationally valued at about 15X earnings so is notably cheaper than a lot of “story” stocks that have a 5G angle, it is buying back some stock and trying to grow in 5G… but it’s also in a very competitive business where taking the lead in technology means being a few months ahead, and as long as half of revenue comes from Apple they’ll be at the mercy of iPhone volumes and a huge customer who pressures them on their profit margins. I haven’t bought back in to SWKS after stopping out of my shares last year, but I wouldn’t call it a crazy idea. Skyworks is expected to report their next quarterly earnings in about two weeks, so the story could change pretty quickly.

My thoughts don’t matter as much as yours, however — it is, after all, your money. So what do you think? Want to bet on Skyworks becoming a growth darling again? Think another disappointing wave of iPhone sales this year will crush them? Let us know with a comment below.

P.S. This newsletter seems to be new on the scene, so our readers want to know what you think — like it or loathe it? If you’ve subscribed to The Sniper Report, please click here to share your thoughts with your fellow investors.

Disclosure: Among the stocks mentioned above, I own shares of (and/or call options on) Apple and Qualcomm. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

$6 Stock, all this is BS, just to make you join some forum. Everybody talks about it, everybody knows it, but didn’t see any name yet.

$6 Stock, all this is BS, just to make you join some forum. Everybody talks about it, everybody knows it, but didn’t see any name yet.

Paul_sm, What in heaven’s name are you commenting on?

LOL, my thought exactly!

Hi travis as you mentioned Qualcomm what are your thoughts on the settlement and the impact it will have on that company going forwards? It presumeably also means bad news for most of their competitors.

Great for Qualcomm, not as good for Broadcom and Intel… but more a positive for Qualcomm just because the uncertainty was lifted. I was shocked to see the stock respond quite that favorably, but it tells you what a disaster a bad legal outcome would have been for them.

tried to ask this question before. I would like to find out about a company being teased allover the place called XYO

The patent settlement was very favorable for QCOM calls and I unloaded most of mine yesterday. I thought it was interesting that a number of analysts said this event was negative for INTC, however INTC stock spiked almost $2 on the news. I talked to 3 former INTC engineers today and they understood the spike in the SP claiming that INTC was losing money on this communications chip endeavor and this is the 6th time INTC has gotten into and out of communications chips business.

Thanks Travis for your previous comments on QCOM.

Regards,

Frank

Hi Frank, I am also holding QCOM calls . Don’t you think that this settlement clears the way for QCOM to be an active participant in 5G development and thus has more upside?

tanglewood, you may be totally right but $QCOM SP jumped 60%+ in 2 days and the calls I had went up 1,500% so I took profits on 80% of the one’s I owned and kept 20% of them . I’d rather take significant profits than be greedy, if you know what I mean, Thanks to Travis.

Regards,

Frank

Think Inseego (INSG).

What about Inseego?

it is not the stock name or $’s to be made but the impact on health that I am concerned. If I am told not to stand in front of my microwave when running for health reasons, how will 5G effect you/me? The scuttlebutt says there will be “cube and pole” on every street in every neighborhood but not a word about its health effect on the human body. Could it be mind altering, carcinogenic, snooping or even person controlling? Until I hear from the medical community as to it’s safe or nonsafe usage I shall do everything in my power to halt its use.

Elissa your concerns are warranted. The Bio Initiative Report evaluated 1800 recent studies confirming major health issues attributed to “Electro Smog” caused by EMF radiation. Doc Gumshoe has been curiously silent in what maybe the biggest health issue of the 21st century.

C.B. Right on, the biggest health issue! But there is another issue…SECURITY. China’s biggest tele com , HUAWEL is producing 5G componants Sure as “God made little green apples,” you know their price will be lower and their heaviest distribution area covers both Asia and Europe. Think how easy it would be for this company to slip in a ‘Back door” for snooping and they would hold the only key. Now every country’s security becomes null and void! Health and security does change the meaning of “A killing” doesn’t it.

EJ–Your evaluation is spot on. I’ve been screaming from the mountain top for years about this possibility. When IBM sold Lenovo to the Chinese it was the beginning of the end IMHO. I believe they already have a “Back Door” in ALL OUR MILITARY & INSTRASTRUCTURE ready at the appropriate time to pull the plug. Color me a conspiracy theorist— I hope I’m wrong. Nice to meet a critical thinker, they are few and far between!!

BJ- The air on mountain tops is pretty thin for screaming. I have been there several times. Conspirasy is a harsh word, I prefer contrarian. One must use simple words when dealing with the “Bean Counter” mentality. Would love to continue conversation further, if you desire. I can be reached ej2@yahoo..

New info on 5G, Ericsson, ERIC, is also getting to be a supplier.

your welcome

Late last year was a good time to buy Skyworks. It was around $60 then, and now it’s back to about $90.

I haven’t been able to separate the hype from the substance about 5G. I’m still using a 15 year old 3G flip phone, because I’m talking and sometimes texting.

In fairness, late last year was a great time to buy almost anything. “I missed it” is never a particularly helpful feeling in investing, try to think more about what the company is doing and how it’s valued today and less about what the stock price was before — the future matters far more than the past.

Thanks Travis — another clear and balanced analysis.

Wow I tried to get this but not enough $$ but he’s offered it very low only it’s not like his style he teaches options? I’m curious to know

Nice summary. Wish I’d followed you into QCOM. Doh.

Travis,

I like to subscribe to this article but there is no way to subscribe. No little box that i could click. Does it effect everyone or just me?

Great article as usual. So glad I went back into Qualcome. A while ago I was quite frustrated because there seemed no end in site with all these lawsuits. Got so tired of it. Not anymore, at least for now. Sometimes it pays to be patient.

While the problem of competition is certainly real, SWKS appears to have a pretty good balance sheet for a small company. Does anyone know if the data on Yahoo Finance is correct? According to it, they have more cash than debt, trailing PE of 14 and PEG of 1.2, all with a market cap of only 15B. If the hype is right, it’s obviously good, and if the hype is wrong, it still has pretty strong fundamentals. Am I wrong?

Sounds not far off, though semiconductor companies are often on the cheap side.