Yesterday I dug into Marc Lichtenfeld’s teaser pitch about his predicted “Commodity Supercycle” and revealed what he’s hinting at as the three “once in a generation” supercycle stocks… so today, it’s on to the “bonus pick” he talked about in that “presentation.”

And it’s that special bonus pick that’s actually the cheapest stock, with the most dramatic story… He says it’s a “$1 Investment That Could Be a Ten-Bagger During the Coming Once-in-a-Generation Commodities Supercycle.”

And, better yet… he ties it in with Tesla (TSLA), which always gets everyone hyperventilating a little. So what is it that he’s teasing in ads for his Technical Pattern Profits service ($1,450/yr, no refunds)? Here’s how he teases us about this $1 idea…

“… there’s ONE MORE special mining stock I’d like to share with you today…

“One that’s even smaller than the three I just described. It trades for less than $1.”

And it’s all about nickel, which, yes, is a key ingredient for EV batteries. There are a bunch of different widely-used battery designs and chemistries, but for most large scale batteries a good amount of nickel is used in the cathode, often along with lithium and cobalt and sometimes other metals (the anode is typically mostly graphite, the electrolyte is lithium salt).

More from the ad:

“As electric vehicle production boomed, nickel inventories plummeted.

“Over the last six years, nickel inventories have fallen 80%!

“We’re seeing a supply crunch in nickel similar to the one we saw in silver before it surged 2,800% in the 1970s.”

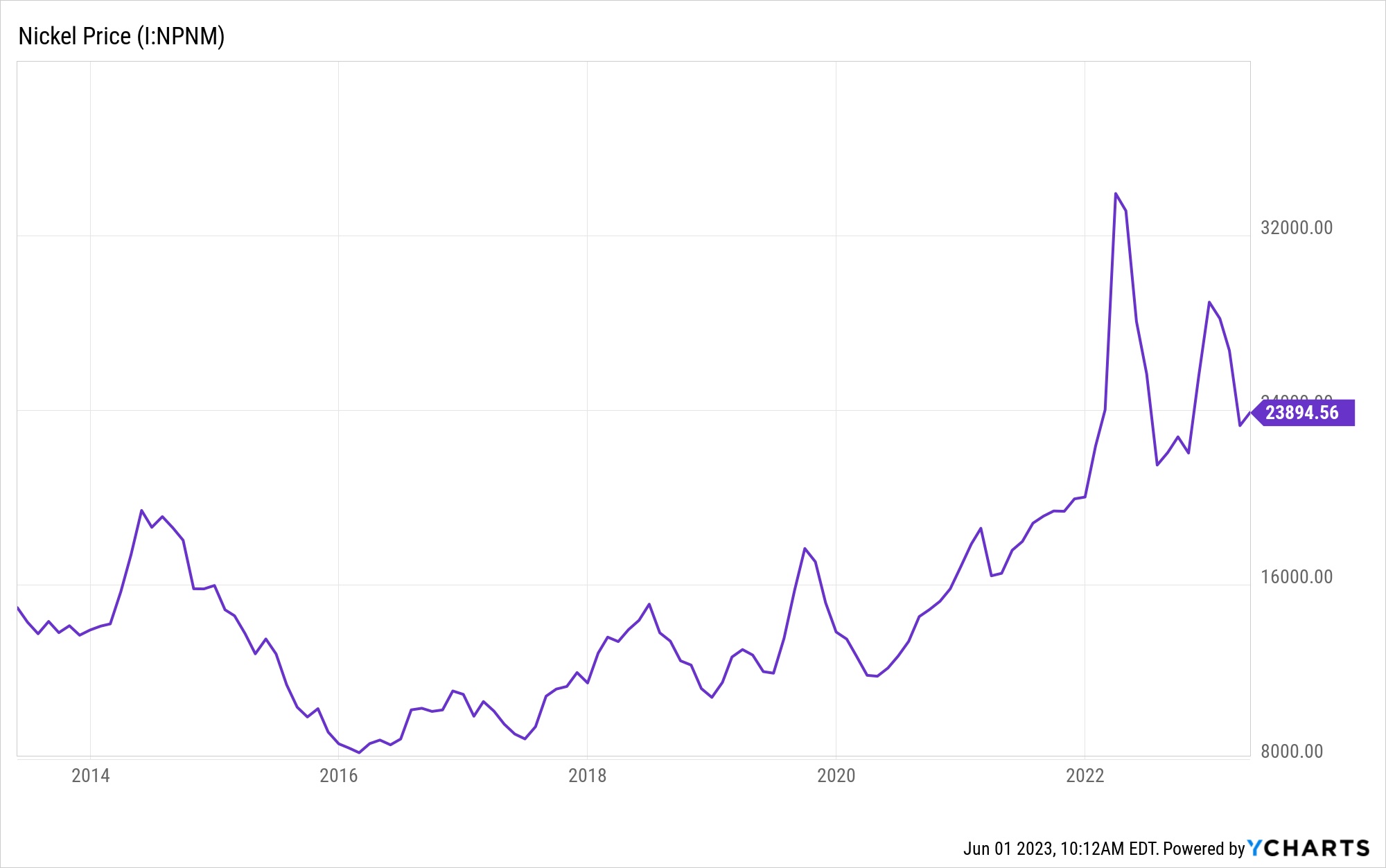

There is a widely perceived inventory shortfall, or at least an expected shortfall, but that hasn’t sent prices soaring — most nickel is used in steelmaking, so slowdowns in stainless steel production in China over the past couple years did more to depress nickel prices than could be made up for by a gradual rise in demand for EV batteries. That may shift, there are lots of moving parts in the market and the big wild card in recent years has been Indonesia, which has the largest nickel reserves in the world, banned the export of unprocessed ore a few years ago to encourage local development, and has signed a lot of nickel mine development deals with major mining companies and battery hopefuls (not without local controversy, as is typical in mining).

Nickel has been on an uptrend, gradually speaking, over the past six or seven years, but it hasn’t been a straight line — these are the monthly prices, which smooth out a lot of the volatility:

So… what’s the nickel stock? Here are our clues:

“… my #1 way to play this boom is a company that’s extracting battery-quality nickel in the Midwest.

“You see, while a lot of nickel is mined in places like Indonesia, this is one of the few companies with a foothold in the U.S.

“That gives this company a HUGE advantage.

“It is the ONLY company that owns undeveloped high-grade nickel reserves in the USA.

“This is important, because not all nickel is of high enough quality to use in EV batteries.

“It needs to have at least 99.8% purity.

“That makes this company’s reserves very valuable…

“So valuable that the company just entered a contract with Tesla to supply nickel for their battery production.”

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...

And there’s our Tesla connection… OK, what other clues do we get?

“This nickel miner has a market cap of just $200 million.

“I’m sharing all the details on it in my special report… ‘Tesla’s Partner: Discover This Tiny $1 Stock to Profit From the Nickel Boom.’

And that’s it… so, answers? Thinkolator sez this is Talon Metals (TLO in Canada, TLOFF OTC in the US), which is the majority owner and operator of the Tamarack Nickel Project in Minnesota (Rio Tinto is the JV partner). They describe the project as “one of only three high-grade nickel sulphide deposits discovered globally in the 21st century” (the others they cite are both already operating — that’s the Eagle Mine, a small Michigan copper/nickel mine owned by Lundin, and IGO’s Nova mine in Australia). And yes, it’s way less than a dollar (the US shares are around 23 cents at the moment, and have mostly drifted lower since the brief period of excitement over their Tesla deal 17 months ago).

The company has worked the EV angles well, they got a grant from the US Department of Energy to develop a processing facility in North Dakota (not far from the mine, which is in central MN, but also, importantly, moving the dirty and intensive processing and tailings management to a much drier industrial location, away from the waterways near the mine site), and they also, after Elon Musk’s very public plea to “mine more nickel” a few years ago, and his push to develop battery mineral production in North America, signed a supply agreement deal with Tesla in January of 2022 to be their “foundation customer” for the startup of the mine. They say they are working with Tesla, as partners, to reach commercial production by 2027, which is expected to be a period of major ramp-up in nickel demand, and Tesla has committed to buying 75,000 tonnes of nickel concentrate over the first six years of the project (at prices “linked to the LME price”).

The plan is very much a “reshoring” of US nickel production, though it’s not a particularly massive amount of nickel from just this one mine — right now, the nickel production supply line doesn’t make much geographic sense, with the smelting and refining and battery production often taking place on different continents, with the metals making a round trip of the globe, and they’re hoping to build a project where all the work is done fairly nearby, with easy transport of the metal and ore by rail.

The deposit is not yet really “proven” — they’re drilling actively to flesh out the ore body, but right now it’s all in “indicated and inferred resources,” not yet in “reserves,” but they did add considerably to the resource base with their update last October, and they’ve continued to find more high-grade nickel-copper mineralization zones. They’ve also bought a land package near the Eagle Mine in Michigan, across Lake Superior from their Tamarack project, so they’re exploring for other potential deposits in that area in hopes of a second discovery.

This is a tiny company, with a market cap of just under $200 million, and it does have some solid long-term shareholders (a couple big private equity funds in the natural resources area, plus now Rio Tinto, as it has taken its JV payments as shares), and it’s in the middle of a process that will be time-consuming and expensive, further defining reserves at Tamarack and financing and then building the mine, but it is certainly a nicely situated story.

They’ve both raised and used about $50 million in cash in the past year, mostly on capital expenditures (buying drilling rigs, etc., in total they’ve now capitalized $172 million worth of exploration costs at Tarmarack), and I don’t know what their spending is likely to be for the rest of this year, but they should, logically, be spending more as they ramp up to delineate reserves and eventually get to a preliminary economic analysis of the mine, then a feasibility statement (and reserves declaration) in a few years, and as of last quarter they were sitting on about $23 million in cash, so they’ll almost certainly need to raise a good chunk more money at some point (the “recommended budget” in their resource statement six months ago was $33 million for the next stage of work, though I don’t know how realistic that is, or what time period it covers). If that fundraising happens to be at a time when nickel prices are rising and everyone’s excited about the nickel “story,” great… if it happens to come when Russia has re-opened to the world, and Norilsk Nickel and new mines in Indonesia are ramping up the supply, or when some new battery chemistry has everyone excited about a different metal, well, who knows. Being early in the development process means you ride a lot of waves of sentiment as you’re trying to raise money to move forward, and it often takes some luck.

Right now, Talon is in early-stage engineering for the potential mine, which will feed into the environmental review and permitting process, and at the same time they’re continuing to drill, with several rigs running on various parts of the project for the rest of the year to both extend the potential area of the mine and find new ore bodies, and to further “de-risk” the nickel they’ve found so far.

I’m not an expert on mining, but I do have to confess that the plan to be producing nickel by 2026 at Tamarack sounds wildly optimistic — they’ve still got to get permits and government approvals, provide some sort of preliminary economic analysis, move on to a bankable feasibility study that will let them raise construction financing, raise that money, and then build the actual underground mine. Even if it ends up being a relatively simple project, with good local partners and no major hiccups in permitting (it is in a historic mining area, though mining permits in the US are rarely simple), that strikes me as an extremely tight three year timeline, and we still don’t have any outside estimate of the economic potential of the project. I don’t think I’ve ever heard of a mine going from a resource estimate to production in four years, even with government support and some good partners in Tesla and Rio Tinto.

Just to give you an idea of the possible timeline that this kind of project might follow, Rio Tinto also did the initial commercialization work at the Eagle Mine in Michigan, which is the most recently built “near peer” nickel mine in the US, and that began commercial production at the end of 2014, about 18 months after Lundin bought the under-construction project for $325 million. The deposit was discovered in 2002, with a pre-feasibility study in 2005 and a bankable feasibility study in 2007, and, after everything was put on hold for a couple years in the 2008 financial crisis, Rio Tinto committed to invest $469 million in the project in 2010, which was effectively the green light for construction. So that’s four years from financing to production, and seven years from feasibility study to production. There were some permitting problems and objections, including lawsuits over a road over some wetlands, so maybe Talon’s project can be built faster than that, but we probably ought to expect any project to have some speedbumps… and we have no indication of when we might see even a preliminary feasibility study for Tamarack. Tesla has the option of pulling out if the project isn’t producing by 2027, though they obviously still want a lot of nickel so they may well be more patient.

Personally, I’d probably be more comfortable with more established players. The most appealing nickel producer for me would likely be Vale (VALE), partly because of the imminent catalyst of some kind of partnership deal for their copper/nickel operations in the near future. There’s nowhere near as much upside with Vale as Talon could have if they really find a “district size” nickel deposit and can build a large mine at some point, but there’s also nowhere near as much patience and financing required.

Vale is aiming to spin off or find a big partner for its large copper/nickel portfolio (they’ve been saying that a decision on that should come in the first half of the year, which is quickly running out now, though delays would be surprising). The latest news I saw is that they’re still evaluating possible partners, including GM, and that the initial partner will own 10% of the company, which theoretically will help investors put a higher value on those assets, which will be separated out into a business called Vale Base Metals. We don’t know if they’ll really go so far as to spin it out into a separately traded stock, but for now it looks like they want to maintain control. Vale is probably the largest miner with major nickel production, largely coming from its acquisition of INCO many years ago and including big projects and mines in both Canada and Indonesia, and it has never really gotten credit for that push into nickel — it’s also the cheapest big miner right now, largely because of challenges with their iron ore production in Brazil (especially the disastrous collapses of their tailings dams).

All the mega-sized iron ore-fueled mining giants are cheap, including Rio Tinto (RIO), BHP (BHP), Glencore (GLEN.L, GLNCY, GLNCF) and Anglo American (AAL.L, NGLOY), and they’re all driven to a meaningful degree by shifting demands from steelmakers, which means they’re driven mostly by Chinese industrialization still, not directly by battery production… and they all pay pretty solid dividends, which make it easier to wait for any potential “supercycle” to drive their profits higher… but in that group of established multinational leaders, Vale is the cheapest, and the most exposed to nickel and copper (with the possible exception of Glencore), and I think it’s also the only one that’s not heavily involved in stuff that’s much less “green” and forward-looking, like coal.

Not a recommendation, of course, and I don’t currently own any of those mega-miners… but whenever I think of nickel these days, my mind drifts first to Vale. It may not be the sexiest nickel stock, but I think it’s the big and profitable company whose nickel production is probably least appreciated by investors. If you’re interested in nickel we’ve also looked at a couple smallish royalty companies who are trying to build nickel businesses in recent years, like Nova Royalty (NOVR.V, NOVRF), which has had a hard time getting up to scale and is “exploring options to maximize shareholder value,” or Nickel 28 Capital (NKL.V, CONXF), which has a joint venture project which is actually producing and generating cash flow along with a “maybe someday” portfolio of royalties.

So… whaddya think? Ready to bet on an early stage nickel project in Minnesota? See huge gains ahead for nickel as it recovers from recent volatility? Think the nickel story is overdone? Let us know with a comment below…

Disclosure: I am not invested in any of the companies mentioned above, and will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Is this a new name for a company called Duluth Metals (or D Mining, can’t recall)? Duluth and Polymet had properties adjacent to each other and next to, unfortunately, the Boundary Waters Canoe Area (BWCA). 10 to 15 years of wrangling, so far, between environmentalists and the companies with no end in sight. Don’t know if we’re talking about the same property though.

Polymet is still there, though the name of the project might have changed. Duluth was bought by Antofogasta, both are active in that big belt of mineralized deposits that’s sometimes called the Duluth Complex between the Boundary Waters and Lake Superior. Talon’s project is quite a bit west of there, I think about 75 miles west of Duluth — there may be different environmental challenges, but they’re not near the lake or the boundary waters park area.

PolyMet and Teck formed a 50:50 joint venture called NewRange Copper Nickel LLC, which will include PolyMet’s NorthMet Project and Teck’s Mesaba Project and represent two of the largest undeveloped clean energy mineral resources in the U.S.

https://polymetmining.com/investors/news/polymet-strikes-5050-joint-venture-agreement-with-teck-resources/

Not about Nickel but Lithium. 60 Minutes did a story about a practically endless supply from the Salton Sea in SoCal and I haven’t heard anyone else writing or talking about it since. Elon is starting a mining operation of some kind near Corpus Christi, Tx. Just curious why this isn’t common knowledge. You can see it on YouTube.

Truthfully, it is fairly well known. Bill Gates has also been trying for 3 years to get a mine up at Salton Sera. Just Google his name with Salton sea to see the story. Environmeltalists are major obsticles to most US miners. I have 12 Lithium stocks. PILBF & LLKKF are among my favorites.

You may be right about battery components changing in the future. Most if not all the companies in the space seem to be trying to eliminate not only nickel, but also cobalt and graphite from their batteries. At least nickel has other uses besides batteries, such as in stainless steel, etc.

This may be the answer, rather than bigger batteries.

https://electreon.com/

As of Friday Oct. 272023 Talon Metals (TLO on the TSX) in the last year has gone from .54 cents a share in Oct. 2022 to .23 cents today. Small company as it is, it lost $4 million in 2019, $2.73 million in 2020, $5.5 Million in 2021 , (no profit so far), and it looks like it was close to breaking even in 2022. The only positive I can see here is that it seems to trade with an average volume of around 240,000 a day, not a lot I know, but better than many of the other “under a dollar” stocks.