I wrote to you about Porter Stansberry’s “Boston Blackout” teaser pitch several times over the past six months or so, and the core natural gas investments he’s teasing haven’t changed since then… though the production value on the latest ads, and the investment in distribution, seem to have ramped up again, since more folks are asking about it.

I won’t bore you by going through the whole spiel again — you can catch that article here, and there has been a little bit of news since then, but nothing that really changes the story.

The latest ads in February come with political headlines like “Biden’s Forever Term” or “Obama’s Third Term” to get attention, similar to several other recent natural gas pitches we’ve seen which imply that US natural gas dominance will create another energy boom and lead to rewards for our current political leaders. We’ve also seen them test headlines that “Buffett wishes he could buy this,” and that’s obviously silly — Warren Buffett’s Berkshire Hathaway can’t easily buy stock in tiny companies, it’s true, and investment newsletters often pitch small caps as things that Buffett would love but can’t buy…. but the primary stock Porter teases here is valued at well over $10 billion — Berkshire could buy 10-20% of it easily if Buffett wanted to, and has done so with many similar-sized companies in recent years.

What particularly interested me, since I do love uncovering a “secret,” is that Porter added a third stock to the tease around the end of last year. So let’s recap and update the story on the first two picks before we look into that third one…

Last time it was all about natural gas and LNG (the “Boston Blackout” bit is about how we’ve been a little short-sighted in New England, simultaneously becoming more dependent on natural gas for electricity generation and blocking pipelines that would supply more of that gas to Boston and other growing areas — which means, in part, that Massachusetts, not unlike Europe this winter, might be uncomfortably dependent on LNG imports), and about the inevitability of the move to build more infrastructure and more LNG export terminals to supply the world with cleaner natural gas and profit from the big shale gas fields that are producing in the US.

In big picture terms, it’s basically “we went to far with environmental protection/ESG priorities, and that has led to a big imbalance. Here’s a little excerpt from the current ad:

“Within the next year, the entire world is going to realize that the best, safest, and cleanest way to grow the world’s economy is by using America’s natural gas.

“And after years of declining investment, it will take 3-5 years for America’s oil and gas companies to ramp up production to meet soaring global demand. That means investors in these firms are going to generate returns like they haven’t seen in decades.

“Overall, the demand supply and demand characteristics for U.S. oil and gas haven’t been this favorable since the 1970s…

“That’s why the world’s best investor – Warren Buffett – has been investing in oil and gas like never before. His investments during the first half of 2022 are among the biggest bets he’s ever made…”

The primary teaser pitch Porter spins is still for the US gas giant EQT (EQT), which has massive reserves in Appalachia and the Marcellus Shale and is pushing for more gas transport and export capacity to be built, and he also again pitches Tellurian (TELL), which is Charif Souki’s attempt to replicate the liquefied natural gas (LNG) export giant he built at Cheniere, though with the added bonus of producing some of his own natural gas in the Haynesville Shale to feed the Driftwood LNG Export project in Louisiana.

There’s been some news from both companies since we last wrote, but nothing huge — EQT had some very good growth in the third quarter last quarter, and made an acquisition that looks pretty appealing (adding more producing reserves, and some more pipeline capacity in Appalachia), but the results were in line with expectations. They reported their December quarter a week ago, falling short on earnings (42 cents in EPS, vs. 52 cents expected, with revenues down 6.6% from a year ago). Nobody was expecting good news, and none was forthcoming, so the stock didn’t react very dramatically. Any fluctuation in the share price is driven more by sentiment about future natural gas prices than anything else.

This is what the story looked like a few months ago — I wrote these words after their last earnings update in late October:

“The big driver of year-over-year growth has been the 50% jump in natural gas prices in the US — and because EQT has been good at keeping costs under control, that increase in prices doesn’t just trickle through the income statement, it gushes… production was more or less stable year over year (down about 1.5%), but their adjusted net income grew by 10X and their free cash flow by about 5X. They expect to finish out 2022 with about $2 billion in free cash flow, so that means they’re trading at about 7.5X free cash flow. Analyst estimates remain above $10 for 2023 earnings per share, so at $40 you’re paying a nice, low multiple… the primary risk is that if natural gas prices fall meaningfully from here, EQT will also probably fall. The relationship is not tight or instant, partly because EQT has become much more efficient in recent years and has done some hedging of natural gas prices, but it is quite clear.

“I like what the company is doing recenty, buying up both future production at a reasonable price and reducing their future costs by buying another transmission network, and they’re being very cautious with their spending as they keep just a few drilling and completion crews operating to maintain a steady state of production… they’ve even got their landlord in Pittsburgh worried that they might not renew their headquarters lease when it expires in a couple years, and that landlord wrote down the value of the building by about a third this quarter, which probably means EQT can cut overhead costs there, too… in the end, however, those are efficiencies and smart moves that can help the bottom line, but it’s still a commodity bet. They can stay profitable if gas prices fall a bit, but to become a huge success story, as Porter Stansberry keeps promoting, they’d have to see rising natural gas prices over the long term. I still think it’s worth a bet, given their operational success and cost controls and their strong free cash flow, but don’t forget that it is a bet. If gas prices return to where they were five or six years ago, roughly half of the current levels, EQT’s stock price will very likely drop in a meaningful way.”

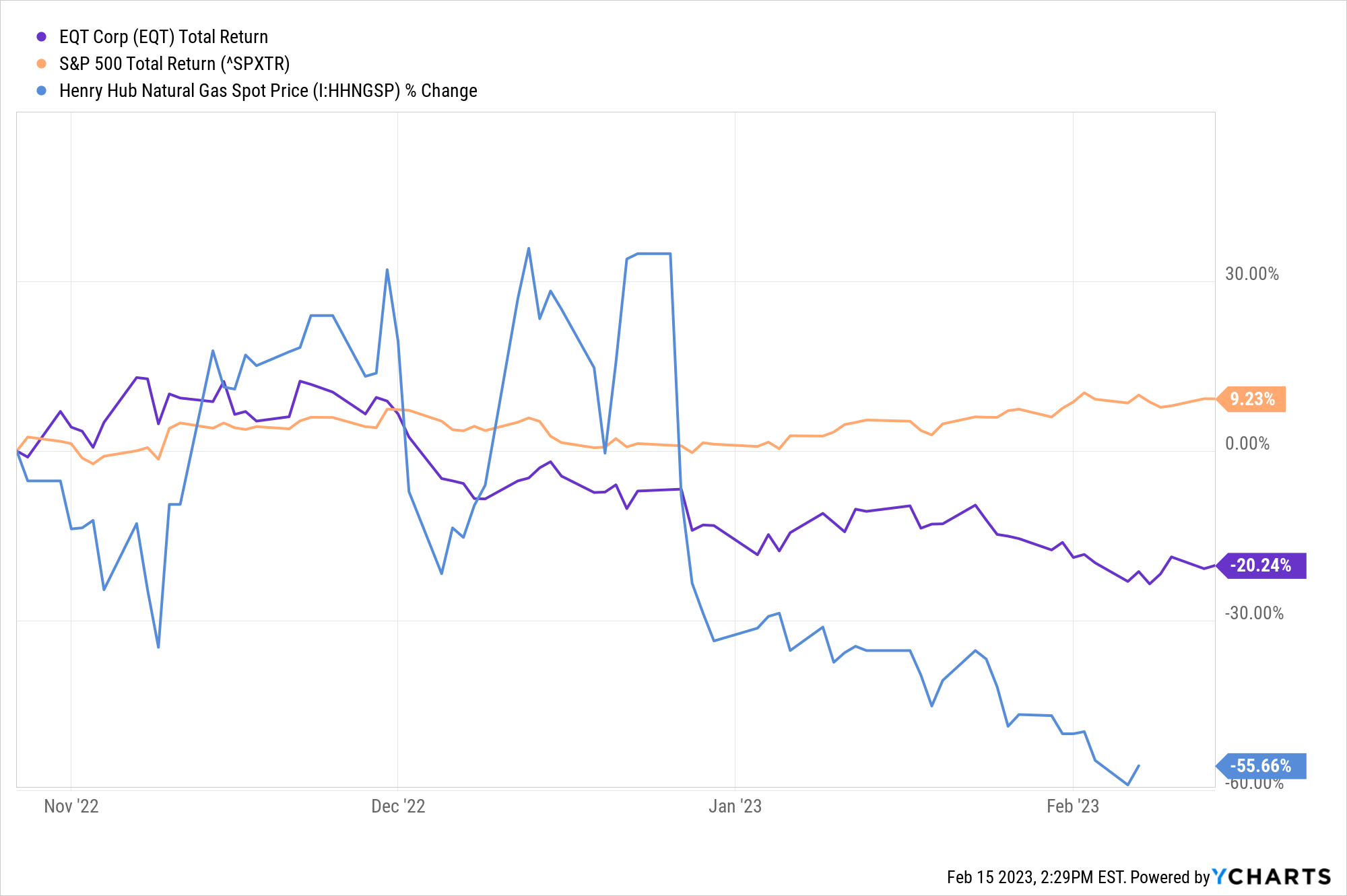

Things have changed pretty remarkably in the past few months on the pricing side… here’s how natural gas prices and EQT shares have done since then (data is a couple weeks old now) — that’s EQT down about 20%, driven by natural gas spot prices that are now down 56% (the orange line is the S&P 500, for context):

And those lower gas prices have, no surprise, brought down revenue and earnings expectations — they did still manage to hit (almost) $2 billion in free cash flow for last year, and they’ve now hedged 62% of their 2023 production at $3.37 per MMBtu, and 10% of 2024 production at $4.20, so they should be able to remain profitable and keep paying down debt this year…. but in order for them to get to $2 billion in free cash flow again in 2023, gas prices would have to jump back up by 50-100%. Things are not nearly as rosy as they were when gas prices were much higher six months ago… but they’re still pretty conservative, and should be able to keep plugging along. Their latest quarterly investor presentation is worth a read if you’re interested in the story.

And while EQT has been his most talked-up stock for about a year, he now says that his second one is maybe his best idea… here’s how he describes it in the latest ad:

“[EQT] is a great investment – as good as an investment as I have ever found in my 25-year career.

“But it isn’t even my best idea to profit from the global growth in demand for natural gas…

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“There’s a company that has even more upside – because it’s only beginning to assemble its acreage and build its pipelines and LNG facilities.

“The best part? Its founder is the man who started the entire LNG boom in the United States, building the first independent (non-major oil company) LNG export facility in 2010-2014 – and a stock that has gone from around $5 to over $150.

“Now he’s about to do it again…

“THE EMERGING LNG GIANT”

So yep, that’s still Tellurian (TELL).

What’s up with TELL? Well, they’re producing a lot more natural gas than they were a year ago, and still buying up some acreage to increase future production — but nobody’s really buying Tellurian because of their production in the Haynesville Shale, they’re buying Tellurian because of the Driftwood LNG Project, which hopes to profit directly from the (recently massive) differential between US natural gas prices and imported LNG prices in Europe… and that means investors are buying into something that requires billions of dollars in capital, since they’ve barely started to build the project and need to raise a lot of the money, at a time when borrowing is more expensive and more uncertain than it was even a few months ago.

Tellurian’s challenge last year was that they had to pull a billion-dollar bond offering, presumably due to lack of interest while inflation was raging, and they also lost one of their customers as a long-term purchase agreement was dropped — I imagine they can find other customers, and they will eventually figure out how to finance the project, but at this point it’s pretty high risk. There’s been no real financing news in recent months, but the early stages of construction (by Bechtel) are continuing.

The payoff is enormous if it works out, but in cash flow terms that payoff is also several years away, since the facility will take a long time to build… so if we’ve all made nice with Russia by then, and all is forgiven and forgotten, well, the price of natural gas in Europe or Japan might not be as high as Tellurian is hoping.

Maybe worth a bet, but far more volatile and uncertain than EQT — I’d think of the shares here as being more like a five-year levered option on LNG exports, and it’s not completely clear how much that leverage will cost (either through dilutive share offerings at low prices, some kind of strategic deal, or relatively expensive bond financing). If there’s a big surge to come in the share price at Tellurian sometime soon, it will probably be because they make some kind of financing deal for the Driftwood Project that delights investors — and they have enough cash for the early stages of the work that are happening right now, so they can probably afford to be at least a little bit patient.

Not so great for shareholders so far, though — here’s their share price added to that same chart I shared above (that’s Tellurian in green, it was down below $1.50 when I pulled this data — it has since popped back up a little):

Porter’s not the only one to get drawn into the excitement about Charif Souki trying to build another giant — I remember Dr. Kent Moors pitching them five years ago in the $10-12 range, and even more recently Whitney Tilson pitched the stock at about $4 last September.

Will it work out? So much depends on the construction cost, including the financing cost and whatever deals they have to make to get Driftwood completed over the next few years, that it’s really a pretty wild guess at this point… the good news, if Driftwood does eventually get financed and finished and is profitable at some point, is that it’s pretty cheap, and expectations are pretty low. They could go lower, for sure, it’s unlikely that Driftwood will have its first train operational before 2027, and a lot can happen in that time… but they’ve invested about a billion dollars into Driftwood so far, and even if you ignore their producing natural gas properties (which last quarter produced an operating profit of $48 million), the company is valued at less than their investment-to-date in Driftwood (TELL’s enterprise value is about $700 million). Really, Tellurian is a little $1 billion equity stub on the Driftwood project, and it’s likely that the price of that project is increasing pretty steadily these days (a year ago, it was expected that Phase 1 would cost about $12 billion, it must be higher than that now).

The big positive for Tellurian would be a farm-out of a big stake in Driftwood to a partner with deep pockets who can help bring down the financing costs, perhaps one of the big French or German energy companies, or even a US energy company who wants better access to foreign markets (the gas-only companies like EQT don’t have enough money for that kind of deal, but the big integrated energy majors like ExxonMobil do). I don’t see any sign of such a partnership yet, and you can certainly sense that trying to guess at what gas prices might be in Europe or Tokyo five and ten years from now is a tough starting point, especially at a time when prices are falling almost everywhere, but that’s probably the big hope for Tellurian… we just have to see if Charif Souki can sell someone on his vision. It makes some sense to me as a long-term strategic project, but I don’t have $10 billion to contribute… the amount of money it takes to build these projects is truly overwhelming, and the fact that money isn’t free anymore, with interest rates finally rising to somewhat rational levels, is probably a big impediment.

And the new stock being added to Porter’s stable at the end of 2022? Still some natural gas exposure, but also some oil, and a different kind of company… here’s how he teases it:

“I want to talk about one more important idea that every energy investor should know: there’s a way to own the energy – but not the production companies…

“There’s a way to separate the cash flows from the overhead and the risks. It’s a secret that I learned from T. Boone Pickens.

“HOW TO GET ALL THE PROFIT, BUT NONE OF THE HASSLE”

Having followed Porter’s writing for decades now, my instant reaction there is “he’s talking about royalties” — and that is indeed the basic idea. More from the ad:

“T. Boone’s revolutionary idea was to separate the income streams from proven and operating fields from the costs of finding and developing additional fields.

“These kinds of royalty-holding companies still exist today, and the best one on the market is a leading royalty holder in the Permian Basin, which is America’s most prolific oil field.

“T. Boone created the first energy trusts primarily for tax reasons, but the advantages of these kinds of structures go well beyond tax benefits.”

The basic argument for royalty companies is that they are passive top-line participants — they get a share of everything that is produced from a particular field (or mine, or whatever), and they don’t have to worry about whether production costs go up or the developer lied about how much it would cost to build the mine. Their exposure is mostly just to how much oil (or gold, or whatever) is produced, and what the market price is for that commodity — they still can’t control market prices, and they are passive participants so they don’t get to decide how much production happens, but they at least know that they have essentially no operating costs or carrying costs on the royalties, they just sit back and collect their share. And when commodity prices rise, like they did this year, they collect more money per barrel of oil produced… and the total production also often grows, increasing the size of the pie and therefore making their slice larger, since higher prices drive producers to want to produce more.

Every deal is a little different, and every royalty company has a slightly different strategy and a different portfolio of assets, but that’s the basic idea. Royalty companies tend to be relatively expensive, compared to operating companies, but they’re still pretty easy to love.

Which one does Porter like? More clues in this bit from the ad:

“How profitable can these investments be? Well, the leading Permian Basin royalty company has averaged an incredible 77% free cash flow margin over the last five years.

“Since going public in 2014, the Permian’s leading royalty company production figures have grown nearly 10-fold, from average daily volumes of 3,000 barrels of oil equivalent (“BOE”) eight years ago to 28,000 last year….

“Investors have reaped the benefits, with the stock outperforming the broader energy sector by a factor of 3.5 to 1 since its inception as a public company. This is an incredibly efficient and safer way to own a huge stake in America’s most prolific oil field.

“The company owns mineral rights spanning across 930,871 gross acres, with over 9,000 producing wells.”

And the reserves are growing, we’re told:

“And this royalty company continues to grow, by continuously buying more mineral rights on proven oil fields. Reserves have grown by an incredible 7-fold from 18 million BOE in 2014 to 128 million at the end of 2021.

“The best part of this company, given the current volatility in the stock market, is that it offers remarkable resilience against the inherent volatility of oil and gas prices….

“For such a compelling business model, you would expect the stock to command an extremely high valuation premium. And yet, with a market capitalization of roughly $5 billion, the company trades at less than 10x free cash flow today.

“The best part? Without needing to recycle earnings back into expensive equipment and other operating costs, that cash flows right back to investors. That’s how the company pays out a current distribution of $3.24 annualized, for a yield of nearly 10%.”

So what’s this Permian Royalty Firm? Thinkolator sez Porter is pitching Viper Energy Partners (VNOM), which is indeed a major owner of royalty interests in the Permian Basin, spun out of Diamondback energy back in 2014. They have been pretty consistent producers, and have had excellent cash flow of late, though back in November, Viper announced a much lower dividend than expected, and the shares dropped about 10%. The stock has held up reasonably well since then, it’s still close to $32 (for a 6% yield, at the current distribution rate), probably in large part because it’s more of an oil and yield play than it is a natural gas play.

As of the second quarter of 2022, when they were enjoying windfall oil and gas prices, the distribution was 81 cents per share, so that matches the “$3.24 annualized” in Porter’s ad, and would have been nearly a 10% yield… but the last dividend was 49 cents, which would annualize to $1.96 and, at the newly-lowered share price of about $32, a distribution yield of only about 6%. That’s the challenge of a variable dividend — even if they tell us it can change, we tend to think that means it only goes up, particularly for a stock like VNOM which has raised the distribution steadily over the last couple years. Many of us are accustomed to thinking of dividends as being somehow sacrosanct, so sometimes we tend to get too confident about the future payouts, and eat our chickens before they’re hatched.

VNOM is still generating a rising amount of cash flow, their guidance for production over the next couple quarters is roughly in line with what their operator produced on their royalty lands last quarter, and they have more cash available for distribution than they’re distributing… but last quarter, they spent more of that on unit repurchases (buying back about 1% of their shares in the quarter) than on cash distributions. They’ve committed to spending 75% of “cash available for distribution” on returning capital to shareholders, and the math probably works out just fine to make the buybacks seem reasonable… but usually buyers of MLPs like VNOM want high current cash income, and the immediate reaction of shareholders seemed to be that they liked the higher cash distribution and were perhaps less enthused about higher share buybacks.

To be fair, it was not a violent reaction — so shareholders must have bought into the prospects or expected the reduction to some degree. For most income investments, a 40% cut to the dividend would have brought a much bigger share price drop than the ~10% haircut VNOM received this week. There should be some visibility in the company, because they’re controlled by their operator, Diamondback Energy (FANG), so they’re not entirely passive or in the dark — they know what Diamondback is likely to be doing in terms of investing in new production… but that relationship means that they are also effectively dependent on just one operator, which is unusual for a royalty company and means you don’t get any benefit of diversification in the unlikely event that Diamondback does something stupid or fraudulent and stops producing. FANG has also held up reasonably well in the past few months, following their November swoon.

Viper is a partnership, not a corporation, so the tax consequences are a little different than some shareholders are accustomed to — they refer to units and distributions instead of shares and dividends, and they usually distribute much more than they are legally required to distribute (like REITs, MLPs get to pass through their tax obligation to unitholders as long as they also distribute most of their earnings… but they typically distribute a lot more than they earn, since depreciation/depletion charges are big for energy companies). It works out nicely in the end, because often the distribution is more than half tax-deferred, which is nice (it’s effectively return of capital that reduces your cost basis, so you don’t owe on that capital gain until you sell)… but they also require some additional tax reporting, which can be a (small) headache.

And they’re pretty good at communicating their detailed operations to shareholders (sorry, unitholders), so you can check out Viper’s latest investor presentation if you’d like to see more detail on how it all works. They should report next week, which might change the story a bit.

It’s a relatively interesting company, but there are a lot of oil and gas royalty firms that have similar or higher income yields and also offer meaningful exposure to appealing areas like the Permian Basin — if you want to sniff around for comparison, and maybe get some context, other names that come up somewhat regularly are Sabine Royalty (SBR), Permian Basin Royalty Trust (PBT), San Juan Basin Royalty Trust (SJT), Mesa Royalty Trust (MTR), Dorchester Minerals (DMLP), Freehold Royalties (FRU.TO, FRHLF), and Black Stone Minerals (BSM), and there are plenty of others as well.

If you don’t necessarily need to maximize your income yield or care much about volatility, then it could also be that the operator, Diamondback Energy (FANG) could be interesting — here’s the total return chart for the two in the eight years since FANG (purple) spun out VNOM (blue), with the S&P 500 in orange and TWI Crude Oil spot price in green (the first half of 2014 was a tough time to buy an oil stock, oil prices didn’t get back to that level again until the Russian tanks crossed Ukraine’s border last year).

In case you’re curious, Diamondback also has a high dividend right now… and also lowered that dividend this quarter (this quarterly payout is $2.26, down from $3.05… but it was also much lower a year ago, down at just 50 cents). FANG is trading at a forward PE of about 6, with analysts expecting next year’s earnings to be similar to this year — if they keep paying at the same level as they announced this quarter, $2.26 per share, that would annualize out to $10.04, for a yield of about 6%… pretty similar to VNOM, but probably less reliable. I haven’t looked into Diamondback’s financials beyond noticing that similar yield.

So there we have it, Porter’s repeatedly touted “Boston Blackout” portfolio… ready for last year’s resurgence in the energy sector to continue and lift all these (and other) stocks to unprecedented heights over the next decade? Think the energy-stock fun is over and we’ll soon go back to trash-talking natural gas and building nothing but windmills? Something in between? (Spoiler alert, it’s almost always “something in between.”) Let us know with a comment below (I’ve attached the comments from an earlier article on this topic, too, if you’d like to see what other readers thought about those companies).

P.S. Porter’s new publishing house is now close to a year old, so it would be interesting to hear from any early subscribers — how does it compare to his old stuff at Stansberry Research? Worth the money? Fun or infuriating? If you’ve subscribed, please share your thoughts on our reviews page for The Big Secret here. Thank you!

P.P.S. Yes, Porter’s “Two Men Destroying America” pitch, and the “Forever Term” pitch about Joe Biden becoming “The Fracker” and embracing LNG exports to get reelected and become one of our most popular presidents, those are both also essentially touting these same themes and teasing these same stocks — just testing out some different narratives to see what works best to get attention and recruit subscribers.

Among the companies mentioned above, I own shares of and/or call options on EQT and Warren Buffett’s Berkshire Hathaway. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Travis, your mention of SJT, an old holding of mine and profitable during the early “oughts” (I sold before the financial crisis…wisely, it turned out) caused me to check up on it. It seems to have survived the oil/gas market ups and downs since then and now looks interesting with a current 15% payout, albeit variable along with its volatile price. I won’t bite, because I’ve learned to hate K-1’s, partly because with SJT, they arrived in early May, several weeks after the April 15 FIT filing deadline, and partly because I’ve also learned that at least one of the federal tax return reviewers was apparently not properly schooled on how to read them. Took me anyway six months to straighten that out.

TY Travis. The overriding question you could have asked would be: “Has a rotation started that will take down the many successful Energy stocks of 2022, just in time for a year of gains that stock traders might want to take – Especially if they have losses to take in taxable accounts before year end!”

I did just that this week, taking profits on several oil and gas stock investments to counter balance the losses I had on several tech stocks. Today, we had a rally that helped the Motley Fool/Cathie Wood style Tech stocks move up, while some of the energy stocks were flat on the day ( a few were down, others up, but not like the 5-12% movers in tech!).

What can we all do to better prepare for a rotation? Can we have some kind of forum to share ideas?

Travis – Has this ever been considered for the Stock Gumshoe? We might find many people interested!

I just bot VNOM 6 weeks ago & I see it’s up 8%.

Thanks for further popularizing it! CS

Royalty trusts are a great idea. Though being dependent on solely one operator brings in all sorts on concentration risks.

You do know Turbo Tax can’t even begin to process these royalty trusts across the years, even if they’ve access to all your returns going back decades(?) – like these returns do sit on my PC.

YOU’VE GOT TO MANUALLY, TAKING LITERALLY HOURS AT STARING AT THE CALCS AND DETAILS, FOLLOW THE PAYOUTS EVERY YEAR TILL THE SUM OF PAYOUTS HITS THE INVESTMENT AMOUNT (can happen in the middle of a div payment, so you then have to prorate), AND ONLY THEN DO YOU START PAYING TAX ON ROYATIES, DIVIDENDS RECEIVED.

At least that’s what I think I’ve learned one must do. And I did it for several year over year (VOC, MVO, WHZ…), till it looked so stupid and an IRScum idea, I threw all these trusts straight overboard. Wouldn’t smell ’em with an iron mask at light years again. Thank you IRScum for your awesome, typical meddling and scum.

The programmers at Turbo Tax could really use some help, but the swamp spewers then might just renew some new convoluted “tax treatment” from their towers – the object is being a nuisance disguised as government – the sly flesh-side of capitalism and exploit, not just “always money” by any means – what you’d expect sooner or later IF Turbo could handle it.

They don’t? 2 shares of GBTC generated 42 errors on the Turbo Tax Return this year. Another jerk spew-nuisance of “tax treatment.” Overboard with that nuisance too. It’s the gov-spewers stirring the shly. I hold Turbo in pretty high regard; wish they could follow these nuisance spewers better tho.

Current have small holdings in several Permian Basin royalty “companies”. Most issue K-1 s. Like one of the other commenters, I previously sold out of SJT for the very reason cited. But later re-purchased “shares”. Lately the K-1 s have been arriving (or available on-line) in time for the normal April 15 tax submission date. Even so K-1 s are still a bit of a pain for individuals at tax time. Also as Travis commented, “dividends” can be and are usually variable. And also “share” pricing seems seems to be unrelated to returns. I personally, put up with this as the almost all pay monthly and the these “companies” are most run by banks and therefore have very low costs.

Not until we get rid of Brandon . Porter forgot that we watch the news. NO PIPELINES

I wonder long term about all this talk from the government and environmental groups wanting to ban natural gas stoves and furnaces ? Personally I’ll go down fighting and kicking as I can’t stand electric and it’s way more expensive.

Not sure that I would go quite far as Mr, Baratta is regards to natural gas vs. electric in the residential setting. But with I recent solar installation, would consider replacing my gas water heater with electric one. My only gas appliance in the kitchen will remain the range top as I too do not like electric burners. Would not consider the replacement of gas heating with heat pump at high current costing of a “new and improved” models. Historily, heat pumps here Northern Virginia are very marginal in performance and hence not very popular,

I remember another teaser of Porter’s, I think that it was just before Trump got elected. He said that whatever political party was in power when America became the #1 energy producer in the world would stay in power for decades. Obviously, he was wrong.

Travis – for VNOM this is the comment on their website “Effective May 10, 2018, Viper is a 1099 security and investors will not receive a K-1” So they are no longer issuing the treated K-1.

Hadn’t noticed that, thanks!

As you may know Porter Stansberry is an accomplished story teller who loves hearing himself talk. I would place him on the extreme side of the political spectrum and he is committed to exploiting any possibility to criticize, rip apart and demolish any ideology that conflicts with his beliefs.

He wraps his pitches in this divisive political gift wrapping. Despite his ability to make money and attract certain audiences, I find his choice of human relation skills an interesting and important piece to keep in mind when understanding his thinking.

He is a great storyteller and salesman, he learned at the feet of Bill Bonner and Mark Ford and spun those stories into gold at Stansberry, where more than most newsletter guys he knew that pushing as hard as possible on sales was the core of the business.

I still like to read his free emails… all of his recommendations start with some kind of anecdote from business history these days, and they do suck you in.