Seriously? Google’s obligated to pay you every month?

Well, kind of.

But no, not really.

This teaser pitch came in from Briton Ryle and the Angel Publishing folks a few times over the past week as they’ve been advertising The Wealth Advisory… and you might be thinking that it sounds kinda familiar. I thought so too, so I wanted to check and see if it’s just a revamp of their old “internet royalties” pitch that we’ve covered a few times over the years… here’s how the ad starts:

“Why GOOGLE is contractually obligated to pay you up to $2,058 per month

“Thanks to a small group of “tech heads” out of Denver, Colorado, EVERY American now has the chance to cash in on the third most valuable company on earth…

“Without owning a single share of its stock.”

Oh, who could these lovely “tech heads” be, I wonder? Apparently they’ve magically found their way into Google’s bank account? More from the ad:

“As long as Google remains in business, it is contractually obligated to disburse lump sum checks that give ordinary Americans the chance to pocket sizable piles of cash on a regular basis.

“The thing you need to understand is that the chunks of cash you could collect starting today — up to $2,058 per month — are all based on the amount of business Google does.

“In essence, every time someone sends an email through Gmail or uses Google to find the closest sushi restaurant, you get paid.”

THat’s some pretty over-the-top promising there — there’s some contractual obligation from Google for life? I really doubt that’s true, though the wording is squishy enough that they probably passed it by their lawyers before emailing it out.

A bit more…

“Get the idea? When Google gets used — even if it’s through one of its subsidiaries — you get paid.

“That’s why I refer to these payments as ‘Internet Royalties.’

“Of course, with the staggering numbers posted by Google, you only earn a very small amount of money each time its services are used.

“I’m talking about fractions of a cent.

“But those fractions add up extremely quickly.

“In fact, folks who’ve been using this loophole for some time now have banked some incredible sums of cash:

- Jerry L. Martin recently received a check for $153,406 thanks to “Internet Royalties.”

- Thomas Teague did even better, pocketing $265,213.

- And Robert Webb was the king of them all, raking in $287,751.

“If those numbers seem incredible, it’s because they are.

“But these guys have all been collecting “Internet Royalties” for quite some time now.

“When you start, it’s likely you’ll earn somewhere around the baseline “royalty” figure of $2,058 per month.”

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...

See what he did there? He made $2,058 per month seem like the very least you could expect the “baseline”… and he still hasn’t mentioned how much you have to invest to get that “royalty” income.

And yes, as we’ve now gotten partway through the ad we can see that this is indeed yet another variation on the “Internet royalties” spiel that Angel Publishing started running almost three years ago. Back then it wasn’t so much about Google being “contractually obligated” to pay you, it was about similar obligations from Netflix and Amazon. I guess they just tweak the ad when there’s a different company in the headlines (or when everyone’s already seen the old version and they need a new twist). That older article of mine has been updated a few times and is here, if you’d like more background.

So is it the same investment they’re still hinting at in the ad? I suspect so, but let’s run through the clues.

He implies that the returns were dramatically higher for this investment in 2015 than Google’s …

“Instead of forking over $25,000 and hoping Google’s stock does well, you could’ve made one-year profits of $50,000 by collecting ‘Internet Royalties.'”

Presumably he means you could have doubled your money, not that you would have tripled it (profits, after all, are only the part that’s an increase above your original investment).

And they’re still touting the fact that pretty much everyone is “contractually obligated” to “take part in these payments” ….

“Amazon… Netflix… Wal-Mart… Microsoft… Facebook… even Disney.

“You can collect ‘Internet Royalties’ thanks to ALL of them.

“Like with Google, they are all contractually obligated to take part in these payments. And if they want to stay on the Internet, they’ll continue paying for the foreseeable future.”

And apparently it’s not expensive to get your “baseline” of $2,058 in monthly payments…

“… you can begin collecting these payouts starting with less than $100….”

Obviously, there’s absolutely no chance that an investment of $100 will get you $2,000 returns every month. That’s wholly misleading, and just a wee bit of common sense would have you stopping your reading by now and saying, “phooey” to Briton Ryle’s pitch… but it wriggles its way in to those “greed receptors” in your brain and sometimes you just can’t stop daydreaming about your yacht and your Maserati (or, more prosaically, helping with your Childrens’ college education, rescuing your retirement, etc.).

So do the rest of the clues match the old “Internet Royalties” pitch from years past? Um, yep…

“So what are ‘Internet Royalties’ and how do they work?

“In September of 2010, the first ‘Internet Royalties’ were made available to the public.

“And on the very first day, investors spent a total of $270 million buying in.

“Ever since then, daily “royalty” payouts have ranged anywhere from a mere $840 to $94,350.

“That’s right… some folks have collected upwards of $90,000 in a single day.”

And we get a bit of the history of these “royalties”….

“… in five years, the payouts have skyrocketed by 223%.

“If you’d been collecting $2,000 per month in royalties five years ago, today you’d be making $6,460.

“Those who were making $10,000 are now making more than $30,000, assuming they’re still in the game.

“So if history is any indicator, if you get in today, you can look forward to payouts that will increase in price every single year from here on out.

“Thing is, you have to act fast because to make the kind of money I’ve shown you, you must get in as soon as possible. Every day that passes is another missed payout opportunity.”

So, yes, this is still a spiel about data center REITs, and the only specific hints still point to what also happens to be my favorite stock in that little sub-sector, Coresite Realty (COR)

So rub all of that money-lust out of your eyes for a moment, and let’s bring it back to earth.

Data center REITS are companies who build, own and operate data centers, which are the huge buildings that are filled with racks and racks of servers and provide power and huge connections to the internet. Each of the companies is a little different — some are more “retail”, some more “wholesale”, some have regional focus, some are international — but they all provide the same basic thing: Space for a company’s servers, lots of electric power, and a huge pipeline into the web with connections to the major telecom providers. Lots of companies also host their own servers, or even own their own data centers if they’re large enough for that to be feasible (Facebook, Google, Apple, Amazon all own data centers), but many of them also rent space in many other locations.

And because they’re REITs (that’s a Real Estate Investment Trust), they’re designed to be pass-through investments — so they have to pay out 90% of their taxable income in the form of dividends, and in return they don’t pay tax at the corporate level. That tax obligation is passed along to you, the shareholder (and REIT dividends count as regular income, they’re not “qualified” for any lower dividend tax if that’s available).

The data center REIT concept existed before Coresite, in the form of Dupont Fabros (DFT) and Digital Realty Trust (DLR), but this particular company was IPO’d by Carlyle in September of 2010, did indeed raise exactly $270 million in that IPO, and is priced at about $68 right now — it has roughly doubled since this newsletter ad first appeared 18 months ago, and just about quadrupled since I first called it to the attention of the irregulars when it was a “busted IPO” in 2010. I bought it myself eventually, though unfortunately not in the teens — and I’ve added to my position over the years, including a bit more at about $50 last Fall, so my cost basis is about $34.

CoreSite is a very good company, I think (obviously — I wouldn’t have bought shares and suggested it to the Irregulars otherwise), but it’s sure not an “Internet Royalty” in the way they imply in the ad. They lease data center space to tech customers large and small at well-located, well-powered, well-secured data centers, and supply services (interconnection, etc.) on top of that to clients who need more than just rack space.

It’s sort of a commodity business, in that there are lots of data centers, they sometimes get overbuilt in particular locations and occupancy levels drop (as Coresite saw in Northern Virginia a few years ago), and some clients are just looking for linear feet of space and an allocated amount of power and connection to the telecoms… but there is a premium put on those with the best “backbone” colocations with telecom hubs, geographic locations, power supply, security, and management, among probably other criteria I’m not mentioning. And the “cloud” and growing internet use means demand for more space keeps growing faster than memory and connectivity equipment is shrinking, so I consider it a pretty steady business within the very rapidly obsolescing technology sector.

But the idea that you’re going to pull down massive $2,058 “royalties” per month is, well, balderdash… unless you start with a huge position, and people who put on $1-2 million positions in individual REITs are not (I hope) doing so on the hype-y advice of a $99 newsletter (on sale for $49!).

And likewise, Google and Facebook and all the other big internet businesses, along with lots of smaller businesses of all stripes, do sign contracts with their data centers for an allocated amount of rack space, power, or interconnection bandwidth, often averaging five years or so… so in some ways, you can extrapolate that and say that yes, Google (if they’re a COR customer, I don’t specifically know) is obligated to pay their monthly data center bill per their contract. So yes, they’re “contractually obligated” to pay their landlord for the space and services they use… and then that landlord, Coresite in this case, manages to cover their cash expenses and still pay out about 25-30% of their incoming revenue as dividends. That’s a good business if you can keep it going, but it sounds a lot less powerful than, “you earn a few cents each time someone opens gmail,” right?

This falls into the large pile of teaser pitches that imply a specific, huge cash return… but are generally quite mum about the initial cash outlay required to get that possible return. At the current yield, $2,058 in “monthly royalties” (COR pays its dividend quarterly, but we can do the math) would require starting with something like 7,700 shares — which, at the current price, would cost you about $750,000.

At its heart, this is a growth REIT with a good and growing yield, but at the current price it yields about 3.25% and I’d say it’s not terribly likely to have massive capital gains of 100% or more in the next year — it has gone from $13 to $98 in the six years I’ve been covering the stock, but that’s because we were lucky and bought a growth REIT on the cheap. We happened to find it when it was unloved as a “busted” IPO just a few months after it went public, and just as it was starting to pay a dividend, before they started their pretty dramatic series of annual dividend raises (at a time when interest rates were falling and investors were lusting after decent-yielding dividend growers).

That’s not as much the case now — I think it’s a good stock to own and is the class of the sector, partly because I expect the dividend growth to continue (they’ve raised the dividend sharply each year they’ve been public, an average of 25-30% a year and a huge 50% just last year), but I’d resist going “all in” at the current price, which is the all-time high, and wait for a bit of weakness (which does seem to come along every once in a while).

I’m looking for something like 15-20% annual returns from Coresite going forward, dividends included, and will let those dividends compound to boost multi-year growth, but if you can buy on dips (the shares last really dipped from $90 to $65 in 2016, but they also make sharp moves sometimes with interest rate panics in REIT-world), then things work out much better.

It’s possible, of course, that it will do better than that — I’ve been surprised by the rapid rise over the last six months, and I felt similarly when it was at $70 in the Spring of 2016, so it might just be that I’m blinded by my history with these shares. It’s a very well-run company, and they have been able to grow without being as dilutive (or debt-happy) as most REITs in other sectors, but the valuation is a little more challenging now. Low interest rates have helped, this is a REIT so it will often act like a REIT and go a little silly when fears of Fed interest rate hikes hit the market — but lately it’s been the opposite, with expectations of interest rates continuing to stay low, so a company that yields 3% and increases the dividend aggressively each year is pretty compelling.

When newsletter ads provide examples, I like to check the details. This version of the ad indirectly compared a $25,000 investment in Google in 2015 to a similarly sized investment in COR (or, if they’re being broader, one of their competitors or a basket of them) and implying that these data center REITs would have you sitting on “an extra $50,000.”

If you had put $25,000 into COR back in the early part of 2015, even giving you tremendous credit for catching it close to the 52-week low at around $40 per share, then you would have bought 617 or so shares. And if you held through the most recent dividends, you would have received a total of $3.12 in dividends per share, bringing you another $1,925 (or a bit more if you had reinvested all those dividends into new shares to compound your returns), so that’s a total of about $62,391 at today’s price of about $98. That’s a return of almost exactly 150%.

Really good returns, of course — but even that is not an “extra $50,000.” It is better, as promised, than the also nice return you would have gotten from holding Alphabet/Google (GOOG) shares over that time period (early January 2015 through today), which would have gotten you a return of about 75%.

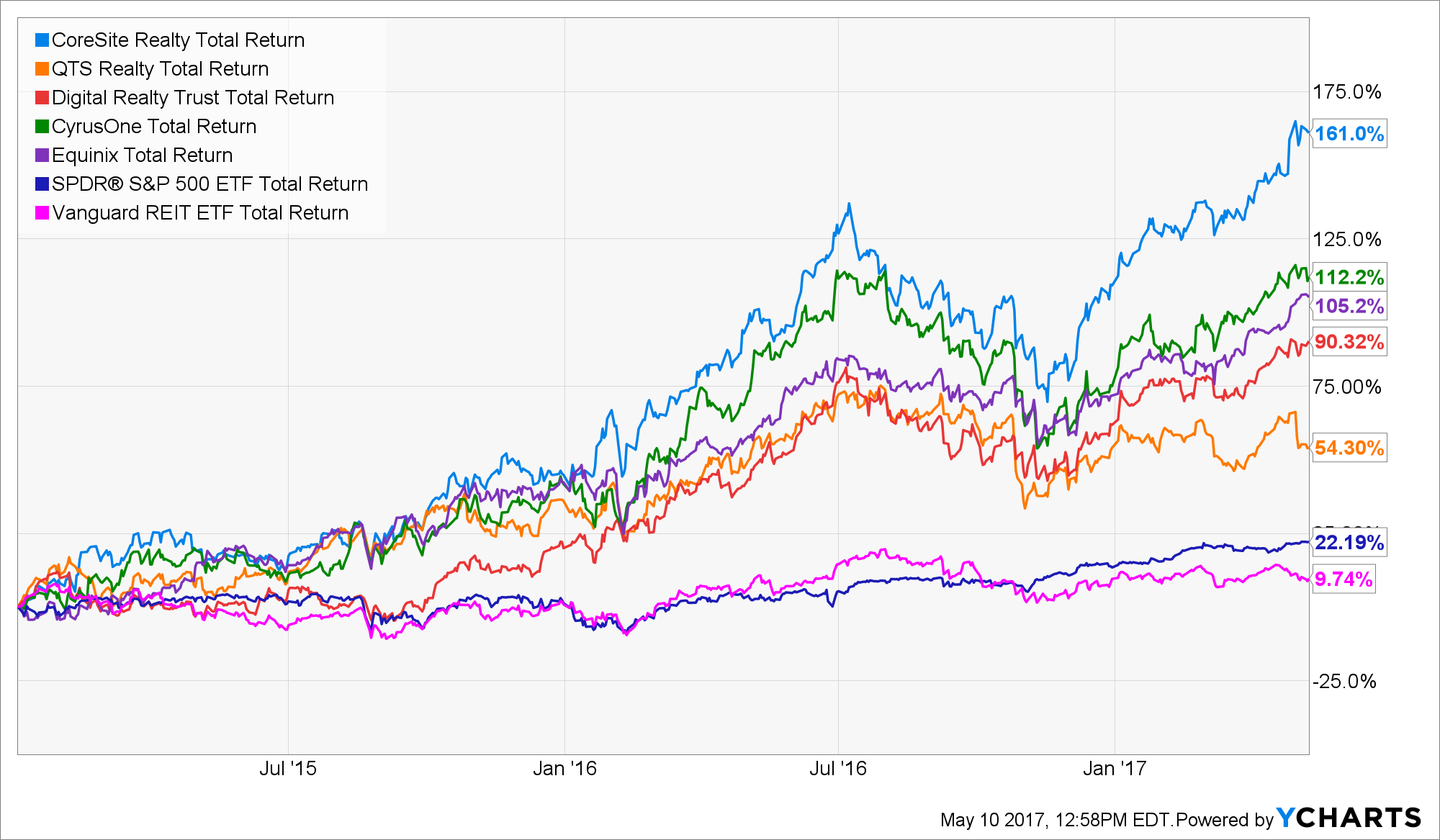

And, as I said, there are quite a few other players in this space now — the largest is a more recent data center REIT conversion, Equinix (EQIX), and the oldest and most well-known is Digital Realty Trust (DLR), and other growing companies like CyrusOne (CONE), QTS Realty (QTS) and perennial laggard (which also bounced back nicely in recent years) DuPont Fabros (DFT). Here’s how those REITs did in terms of total return (stock plus dividends) since January 2015:

So yes, they’ve all done quite well, much better than either the S&P 500 or the Vanguard REIT Index ETF (those are the two lines on the bottom) — and many of them have posted excellent dividend growth (none are as good as COR on that front, however)… but the valuations have also gotten more strained as those stocks have risen, because the basic earnings number for REITs, Funds from Operations (FFO) per share, has not risen as fast as the share price for most of them (FFO is sometimes thought of as “cash earnings” — you basically remove the appreciation, depreciation, and profit or loss from selling buildings or other assets).

This is what I wrote to the Irregulars (our paid members) after Coresite’s most recent earnings report a few weeks ago:

CoreSite (COR) — this largest REIT holding in my portfolio also reported this week, and continues to blow it out of the water when it comes to growth. Expectations continue to rise for COR, which means there’s some risk as investors get ebullient about the future and pay a much higher multiple, but the actual performance has backed up the rise in the share price and the huge dividend increases over the years, and this latest quarter was no exception. Continued year over year growth of 24% on the top line and 30% growth in both earnings per share and FFO per share makes Coresite an almost impossible stock to sell, particularly because they continue to move expansion projects ahead in almost all of their key data center locations and increase their occupancy rates and rents, which supports the assumption that they will keep the long track record of dividend hikes going and again increase the dividend dramatically at the end of this year… but it is, again, getting expensive. I’ve been wrong about CoreSite getting worrisomely expensive in the past, and am reluctant to predict when it might take a breather at this point.

Right now, the dividend of $3.20 is easily covered by the $4.40 in expected FFO for 2017 (they raised their guidance this quarter as well), and they have ample access to non-dilutive capital (that means “debt”) for their current expansion plans, but at $98 you’re now paying 22X FFO for the stock and, if you don’t like ignoring depreciation, almost 60X earnings. You can hold your nose and make that buy because of the 30% year over year growth in FFO and earnings, but there will be some points, most likely, when that growth hits bumps in the road and the shares come down sharply — I’d wait for those before buying in, but I’m unwilling to sell a stock with this record of phenomenal dividend growth… it’s too fun to watch it compound. And it’s still small enough at just over $3 billion to be easily acquired by a larger player if someone decides they want to buy scale and growth.

This is the challenge with a growth stock sometimes: How much do you “let it run” if you think the valuation is getting stretched? That’s a personal decision, and my personal inclination has often been to trim profits off on the way up… but that’s usually the wrong call of late, at least during this long bull market, and I try to fight that inclination when the only real concern I have is that “it’s getting a bit too expensive.” I try to look for an actual problem or a meaningful change in my opinion about a stock before I sell, and in the case of CoreSite the only real concern I have is that it has gone from having a completely clean balance sheet with almost no debt to being slightly more indebted than its competitors over the past couple years. The balance sheet is still fine, but it no longer offers the easy growth that it did in 2015 when they could grow simply by adding some leverage, so that makes me think the growth rate in both earnings and FFO per share will slow as they run up against a larger debt burden.

That doesn’t mean they have to collapse, though, it just means I’d be surprised if they can boost the dividend by 50% again this year… and that I don’t expect them to triple in the next three years, like they have in the past three years. But, heck, I didn’t expect them to triple when I bought in 2013 and 2014, either, and I didn’t expect a $98 stock price when I first wrote about them in the mid-teens back in 2011. I was and am happy with a 3-4% yield that grows at 25% a year… that’s pretty awesome, but when the stock has jounced from $90 to $65 and back to $98 in the course of a year it doesn’t mean you have to buy it at all-time highs. I’d be much more comfortable buying at $80 with a 4% yield, but I might just be a fuddy duddy with CoreSite because I’ve watched it rise so rapidly. We all have a tendency to “anchor” our sentiment about a stock to the price when we bought, so seeing the stock a couple hundred percent higher makes it really, really hard to buy that stock. With stocks like CoreSite, where I like the management and the plan and the long-term performance and don’t have any real operational concerns, I’d probably be better off just dollar cost averaging to increase my holdings as I add cash to my accounts, and not putting too much emotional weight on any given share price.

That goes for many growth stocks, though the emotional wear and tear on a buyer of growth stocks who cares about valuation can be great when we’re looking at a loooooong bull market (eight years now, assuming you count back to the bottom in 2009), and when almost all stocks are trading at pretty lofty valuations relative to the history of the market, especially when economic growth in both the US and worldwide is fairly tepid.

And, of course, your opinion might differ wildly — if you’ve got a thought about CoreSite or any of the other “growth REITs,” let us know with a comment below. We’ve seen other newsletters pitch data center REITs a few times over the past few years as well, which probably isn’t a surprise given the phenomenal performance of this little subsector — the one we covered most recently was Personal Finance‘s pitch about “Digital Rent Checks” if you’d like some perspective from another pundit on the stocks (they were teasing Digital Realty Trust (DLR) at the time). Since this ad is essentially the same as the one they were running back in the Spring of 2016, I’ve attached those older comments on that article to this new piece so you can get that perspective as well.

And, as always, if you’ve been a subscriber to The Wealth Advisory your fellow investors would love to hear your opinion of the service — just click here to share your thoughts with a quick review. Thanks!

P.S. And yes, in case you’re checking all those details, at least a few of Coresite’s “tech heads” are indeed at their headquarters in Denver, Colorado — though their 17 data centers are spread around the country and are mostly focused in the big hub areas of LA, Silicon Valley, NY, Northern Virgina and Chicago.

Disclosure: As mentioned above, I do own shares of CoreCite personally, and Stock Gumshoe currently happens to “live” in a CoreSite data center. I also own shares of Alphabet, Facebook, Amazon and Disney, which were mentioned briefly above. I don’t have direct interest in any other stock mentioned, short or long, and won’t trade any covered stock for at least three days after publication of an article per Stock Gumshoe’s trading rules.

Off this subject, do you have any idea what those “$25 Retirement Notes” are that all the Agora letters are pushing?

I sure enjoy your newsletter!

Thanks,

Jimmy Dunn, the Olwreckdiver

Covered that one here: http://www.stockgumshoe.com/reviews/safe-haven-investor/what-are-the-25-retirement-notes-teased-by-unconventional-wealth/

I find all of the listed data center REiTs COR, EQIX, DLR, CONE, QTS, & DPT very unattractive. COR, EQIX, CLR, & QTS have P/Es between 54 and 104 — CONE & DFT have P/Es of zero. P/S, P/B & P/CF are similarly at levels that are much too high for me. The dividends are also not so hot: 2.2 to 4.7. Believe that I had looked at them some time back and found the whole lot less than attractive so I did not buy at that time. Each to its own, Travis

It’s true, they’re at the expensive side of their historical valuations — though most folks wouldn’t use PEs to evaluate REITs. Maybe they should in some cases, but almost all folks who follow REITs use FFO instead of earnings. Curious to see how these work out over the long term.

As Travis was hintitng, in the case of REITs earnings are impacted by financial items such as depreciation, which reduce earnings for taxation purposes. Funds from operations is therefore a better yardstick.

On a strategic basis, I would not risk long-term investments in data-center REITs — because The Cloud Is Coming, and I believe more and more firms will gradually realize how substantial the advantages are (in total costs to own and operate, first and foremost — but that’s just for starters!) in leasing infrastructure in the Cloud, from the major suppliers (Amazon, Google, Microsoft; not sure if any of the others currently trying to catch up will make it), rather than leasing datacenter space, purchasing and installing equipment, employing operators in the DC, etc, etc. Each of the three, BTW, far prefers to build, own and operate its own data centers (Google’s DC complex in Council Bluffs, Iowa, is believed to be the biggest DC complex on Earth). Of course I may be biased as I do work for Google — and specifically, for the last 1.5 years (out of the 11 I’ve been with Google), I work on the Google Cloud Platform (by my own choice — I find it among the most exciting challenges of my long Google careers!-).

You could be right in the long term, we’ll see — though I expect there will also be reluctance for many companies, as there has been, to rely so fully on the big three and to give up physical control… and the surge of data and demand for rapid access to data in the cloud is keeping demand high, which so far has kept all the boats floating.

I don’t expect that outsourced cloud evolution, if it progresses as it has been, to change the marketplace in a year — I expect it will be gradual, and investors will have time to see falling renewal rates or occupancy levels if and when it becomes a concern. At the moment, I’m more concerned about relatively high valuations than about any fundamental lack of demand for these centers so far.

Well Harry Dent, Mr Dow 40000, is a clown. People should be doing exact opposite of what he preaches. The reason he managed to do interviews in TV channels is because Wall Street needs clowns to intentionally confuse and derail investors so Main street can never make money. People who listened to Harry Dent will have lost out in the entire bull market after 2009.

His basic letter (Boom and Bust) for ca $ 50 a year gives good advice, like a 30% gain on NLY.

$FB – Like it or not, Mark Zuckerberg is now Silicon Valley’s ambassador to the rest of the world – Yahoo Finance: http://finance.yahoo.com/news/not-mark-zuckerberg-now-silicon-123201248.html;_ylc=X1MDMTE5Nzc4NDE4NQRfZXgDMQRfeXJpZAMwaTdiMnQ1Ymg1bWhpBGcDZFhWcFpEeHVjejQwTVRoaFpEZ3pOeTFtTVRJekxUTTBPRGt0WVRnME55MW1NV016T0RCak16UXlabVU4Wm1sbGJHUStabUk9BGxhbmcDZW4tQVUEb3JpZ19sYW5nA2VuLUFVBG9yaWdfcmVnaW9uA0FVBHBvcwMwBHJlZ2lvbgNBVQRzeW1ib2wDRkI-?.tsrc=applewf

did i hear right? $100 a day!

interesting angle, as far as income stocks are concerned, plenty of solid performers when looking at big global ADR’s , Telecoms and Utilities continue to outperform http://eqibeat.com/top-40-global-big-cap-adrs-dividend-yield-may/

All I can say is thanks, Travis, for putting me onto this one back in 2014 when it was still an incredible investment!

So how do become Internet Royslty provider. No BS please

The short answer, using the inaccurate “Royalty” terminology from the ad, is “Buy the stock of a data center REIT.” There are a handful of them — DLR, COR, DFT, QTS, CONE, EQIX, none are particularly cheap or high-yielding at current prices.

If you live in Canada can I join to do this?Regards,Nancy

REITs are not restricted to just US citizens, though there may be different tax implications across the border.

Do you know what the device is that Will Power The 21st Century according to Investment research expert E,B, Tucker? China is opening a factory that will need the $35 billion deposit bought out?

That’s a teaser pitch that has been around for a few months, the “device” is just the lithium ion battery — haven’t written about that particular pitch or dug into the details, but from a quick scan it’s probably yet another ad touting eCobalt (ECS.TO, ECSIF), which we’ve covered a few times (just click the #topic below to see our articles and other comments on the stock). Could be a different small cobalt explorer, but eCobalt is the one that tends to get newsletter pitchmen the most excited and it’s roughly the right size to match the quick clues I skimmed.