So… what’s a “Q-Share?” Are they some magical kind of stock that you can buy, through some secret method, that’s much better than the dumb old regular kinds of stocks you have in your brokerage account?

Um, sadly, no… not really — but there is a rationale worth investigating here, and a secret stock to reveal, so we’ll dig into this latest Jeff Yastine ad for his Total Wealth Insider and see what wisdom we might be able to share with you.

Here’s a little taste from the beginning of the “presentation” …

“‘Q Shares’

“The Profit Exploding Investment Brokers Refuse to Tell You About

“Here’s how you could book quadruple-digit gains from the opportunity no one talks about…

“Today, I am going to introduce you to something I call ‘Q Shares.’

“And even though they are similar to the typical shares in your portfolio, this class of shares is much, much more powerful.

“For example, let’s take a look at Johnson & Johnson’s Q Shares.

“Anyone who upgraded regular shares of Johnson & Johnson into Q Shares, would have made twice as much money today!

“Then there’s Walgreens Q Shares, which are paying investors 177% more than regular shares of Walgreens.

“And Coca-Cola’s Q Shares are making investors 2,769% MORE than Coke’s regular shares.”

These kinds of secret income/secret share pitches get sent around all the time, and that’s been true ever since Stock Gumshoe started publishing in 2007 — some of our very first articles were about deciphering the “secrets” behind schemes described as “801k Plans” (because they’re “twice as good as 401k plans“) and other terms that are lost to my faltering memory.

We’re told that “nearly 1,000 companies” that are offering these Q shares, letting you make 27X your money… and that it’s easy to “upgrade your regular shares” to get “supercharged Q Shares.”

Better still, they’re secret, we’re told…

“They aren’t just keeping it a secret, the companies offering Q Shares are legally barred from telling you they exist.

“When you understand exactly what a Q Share is, you’ll understand why…

“Again, there are two ways you can get Q Shares.

“Through your broker, or directly through one of the 1,000 or so companies that offer them.”

So what’s the big idea? This is just another iteration of the many, many teaser pitches about DRIP and DSPP investing — DRIP standing for Dividend ReInvestment Plan, and DSPP for Direct Stock Purchase Program. Anyone can engage in dividend reinvestment quite easily, just by telling your broker to reinvest your dividends, and they’ll likely do that for free and in perpetuity (some brokers don’t or charge a fee, but most of them offer that service for free).

Direct Stock Purchase Plans and the idea of DRIP investing directly with a company were really popularized thirty or forty years ago, when even a “discount” brokerage likely charged a $20 commission for a stock purchase. They let you buy stock direct from the company, usually through some clearinghouse like Computershare, and often without a fee or with a small fee, and they often also let you reinvest your dividends into fractional shares and even buy fractional shares if you wanted to set things up to invest, say, $150 a month into Coca Cola stock.

That was all part of a real revolution for individual investors, opening up the possibility of building wealth through ownership in solid companies that you can add to gradually over time while letting your dividends compound into more shares, without the high fees charged by full service brokers (remember, forty years ago you might have faced a $100 brokerage commission for buying $2,000 worth of stock — things were not always so easy for small or beginning investors).

"reveal" emails? If not,

just click here...

Now, though, these DRIP and DSPP options are largely dinosaurs — brokerage houses are climbing over themselves to offer you free stock trading, and free dividend reinvestment, and some of them (Fidelity just recently) are also offering fractional share purchases. All that without saddling yourself with the more cumbersome agreements and friction of the direct stock purchase plans you might want to have for a dozen different companies.

They’re not pointless, to be sure, but they’re nowhere near as compelling as they were even 20 years ago. You can do the same thing yourself, at little or no cost, and it might even be that the real value of the direct stock purchase plan enrollment is that friction itself — if it’s a little harder to set up and manage, and a little harder to sell, then maybe you’ll be less likely to trade in and out of positions, which, on average, would certainly improve your returns. There are still a few companies that offer dividend reinvestment at a discount to market prices, or let you buy direct a little cheaper than the live price, but I’d be surprised if there are many — that used to be a fairly regular thing companies did to attract DSPP investors, since they’re not allowed to advertise those programs, but I haven’t seen a discount like that in a long time.

But wait, doesn’t Yastine imply that these stocks are a lot better than the ones you buy from your brokerage?

Yes, but in every case those are really just illustrating the difference between buying a stock and watching the share price appreciation, and reinvesting your dividends to let those returns compound. Dividend reinvestment does provide some magical leverage for long-term investors, but the dividend reinvestment you get from a special DSPP or DRIP investing strategy is identical to just buying the stock in your brokerage account and asking your broker to reinvest the dividends for you.

The rest of the advantage, if there is one, comes from the “regular investment” you make in that stock — so yes, obviously, if you put $50 into McDonald’s stock every month for thirty years you’re going to do dramatically better than if you just bought $50 of McDonald’s stock thirty years ago and waited. Investing more leads to much better returns, and investing consistently on a regular basis, preferably with larger amounts as your circumstances in life improve, is the gold standard… but again, it doesn’t matter whether you do it direct with McDonald’s through Computershare or you do it in your TDAmeritrade or Fidelity account.

And some of the examples are just misleading, like this one:

“Let’s say you put $500 into buying Q Shares of Raytheon on January 3, 2000.

“Your $500 would now be worth $6,600.

“That’s an increase of more than 1,200%.

“But if you put that same $500 into the stock market, your $500 would now only be worth $1,070.

“Meaning, Q Shares of Raytheon returned five times more than the market.

“That’s a good sum for such a small stake to test the waters.”

What is he really saying there? That Q Shares are somehow five times better? No, not really, he’s just saying that Raytheon did 5X better than the stock market over those 20 years. Which is true, here’s the chart of that total return for Raytheon (RTN) versus the S&P 500 (SPY):

But does that actually mean there’s something magical to “Q shares?”

No.

If you bought Raytheon shares in your brokerage account, you got a 1,300% return… if you bought direct through their direct stock purchase plan, you got a 1,300% return. It’s the same stock, traded on the same market. I guess if you bought 20 years ago, you might have saved a few bucks by buying direct… but with free and super-cheap commissions at so many brokerages now, that’s probably not true today.

So yes, the “magical” growth of income they tease in these pitches, with a single share of stock bought for $50 that turns into $80,000, is, for all real purposes, simply the most optimistic outcome from the combination of “buy and hold” and “reinvest your dividends,” with the kicker of “keep making regular small contributions” to sweeten the pot. The magic is in the compounding and, even more, in the consistent recurring investments most people make in these plans.

Which is all smart and wise, but it doesn’t mean that there’s a secret that we mortals can’t grasp. If you’d like to browse through the different direct stock purchase plans that are available, sometimes without fees, you can see most of them at Computershare (there are other clearing houses that offer these, but Computershare is the biggie). Most of these really tend to be “blue chip” stocks, the most active plans are always companies like Verizon (VZ), Exxon Mobil (XOM) and Wal-mart (WMT), though there are lots of smaller ones too, and super boring ones like utilities and little banks.

What is “secret” in the ad is the company he’s teasing as a favorite “Q Share” at the moment, so I thought I’d check that out for you and see if we can ID it… here are our clues:

“The 1 Company About to Dominate an Industry on the Verge of a 1,200% Breakout

“Headquartered on the West Coast, this small company … with just 95 employees … is perfectly set up to dominate the industry PricewaterhouseCoopers is calling ‘the biggest commercial opportunity in today’s fast changing economy.'”

Man, that sounds pretty cool — whatever could it be? More from the ad:

“… they are focused on using AI to improve health care.

“Here’s what I love … this company is already working with some of the biggest pharmaceuticals out there … such as Pfizer and Novartis, to name a few.

“But it’s not just Big Pharma rushing to use this company’s AI software … government agencies are knocking down its door, too.”

OK, I don’t know much about improving health care… but I do know that companies that sell software have FANTASTIC margins. Software is a great business, you get to create a product and then, at essentially no extra cost, make thousands of copies for more customers to use. Better yet is subscription or “cloud” software as a service, with customers who pay you each year to keep using the same software (yes, there are updates and constant maintenance… but the margins can be amazing when it works out, if they have any pricing power at all).

What else?

“This company has collaborations with the National Institutes of Health and the National Cancer Institute. And they have licensing agreements with the Nation Institute for Food and Drug Control in China and the Pharmaceutical and Medical Devices Agency in Japan.

“Plus, this firm just entered into a five-year partnership with the Food and Drug Administration…”

And a few numerical clues…

“… this company’s revenues have soared nearly 400% in the last 13 years.

“Which is why I expect this $600 million company to soar in the coming years.”

Along with some jibber jabber about institutions buying in… which is usually completely meaningless, but does give us some more clues for the Thinkolator…

“The smart money has begun scooping up shares…

“Vanguard and BlackRock own a combined 1.5 million shares of this company.

“And the man the Financial Times calls “the world’s smartest billionaire” … owns half a million shares.

“But I don’t recommend you buy the ordinary shares of this company.

“Instead, I recommend the Q Shares.

“Because the Q Shares could turn every $35 invested into $350 over time…”

OK, so beyond that clue about it maybe being near $35 a share, that’s a reference to Jim Simons and his Medallion Fund — he probably is the smartest billionaire around, since he’s a math genius who has beaten the market by dramatic margins for decades with his quantitative systems and trading ideas, but his Medallion Fund also holds three or four thousand different investments in any one quarter and often trades in and out of the same stock many times in the course of a year or two. He’s not buying a particular stock because of its specific dividend growth potential, and whatever the stock is, his fund probably won’t own it for long and might well have already sold (institutional investors have to report their funds quarterly, with a six week lag from the end of the quarter, so when the new 13F reports come out in about ten days they’ll be telling us what they held on December 31).

And that’s kind of an embarrassment of clues, actually… but let’s put the Thinkolator to work. Things are pretty ugly around here, so I’ve got to shove the snowblower out of the way and put on my big boy boots, but I oughtta be able to get her fired up… and ta-da! Here’s our answer: This is Simulations Plus (SLP), a company I’d never heard of before this very moment.

Here’s how the company describes itself:

“Simulations Plus, Inc. is the leading developer of Absorption, Distribution, Metabolism, Excretion and Toxicity (ADMET) modeling, physiologically based pharmacokinetic (PBPK) & physiologically based biopharmaceutics (PBBM) modeling and simulation software for the pharmaceutical and biotechnology, industrial chemical, cosmetic, herbicide, and food ingredient industries today. Our software allows pharmaceutical scientists to predict certain key potential endpoints and dynamics, in silico, thereby reducing research & development costs and helping clients make better projects decisions… sooner.”

And yes, the clues all match perfectly — they’re reported as having 95 employees, Medallion Fund does own about half a million shares at the moment and Fidelity and Vanguard together own almost exactly 1.5 million shares… and, yes, the share price is right at $35 and they have a market cap of $600 million.

They also pay a dividend, and though it is of paltry size it has grown over the years — it was three cents a share in 2013, and it’s six cents a share now. That means the dividend yield is well under 1% (about 0.7%, if you’re counting), but it could certainly keep growing if they choose — they pay out a little less than half of their net income in dividends right now, and they don’t have a lot of demand for capital unless they want to acquire more businesses (they have no debt to speak of).

There are a couple analysts who provide some limited forecasts, and they think revenue and earnings will both be growing in the 15-20% neighborhood, but for a small company like this you’ll really have to build your own comfort level and your own future expectation — this is a little firm that’s grown through acquisition, with very high margins, and the numbers are not going to be easy to predict. The company’s goal is 15-20% growth, and they grew revenue at 25% and earnings at about 34% last quarter.

I do have a fondness for software companies, small-cap dividend payers, and dividend growth companies, so those are all ticks in SLP’s favor… which was enough to get me to read through their financials, and listen to their last conference call. And I kinda like it, largely because of the fact that they’ve had accelerated growth in several of their new businesses, and they expect strohg growth for the year driven by both software and consulting, with new models and new disease targets and therapeutic areas, and based on their current growth rate I think there’s a decent chance that their next couple quarters, which are seasonally their strongest, will be meaningfully better than they’re hoping.

So this time, I’ll buy a few shares and add it to the Real Money Portfolio to research it further — it’s expensive at 17X sales, even with those high margins, so I’m going in small here, and the stock could certainly fall back to the teens on any bad news… but they’re also already profitable with a 22% profit margin, they’re growing well and focused on that 15-20% goal for revenue growth, and they have growing cash flow and a great balance sheet built on that foundation of very close consulting relationships with customers, and very sticky software sales with 98% retention rates. Small, profitable and growing is a nice combination even if it’s a little expensive.

The growth will probably have to be in the 20% range for a few years to justify this valuation, but with the demand they see and their investment in the sales force that seems like a pretty reasonable forecast. This is not going to be a fast compounder, not with a very low dividend (if you buy 100 shares today and let the dividends reinvest, you’ll likely end up with fewer than 101 shares a year from now), but small growth companies with a history of dividend growth are generally worth considering, and this one appears to be run by grown-ups who are using cash rationally both for bolt-on acquisitions and for additional hiring to fuel future growth. This seems like a reasonable long-term investment to begin to nibble on… but not one that’s likely to generate a lot of leverage from compounding. And no, I don’t think they actually offer a direct stock purchase plan, so you’d have to follow this “Q-share” strategy through your regular old brokerage account if you’re interested.

If you want dramatic compounding of “Q Shares” or a Dividend Reinvestment strategy, you generally need to have at least two of these three things working in your favor: A very long period of time to wait and hold the shares; a high starting dividend; or rapid dividend growth. I’ve got plenty of time to wait, and SLP could become a meaningful dividend grower, but they’re really not there yet — growth here will come from revenue growth and net income growth, probably leading to more bolt-on acquisitions that will hopefully be accretive to earnings, it’s not going to trade at a dramatically higher valuation because the valuation is quite high already… you need just continued strong performance when it comes to sales and profits, nothing magical really at all. In the case of SLP, the dividend is attractive primarily because of the signal it sends: That they’re not wasting money, and they think it’s important to reward shareholders.

I’ll give you one example of how the magical math can work when things really fall into place for DRIP investing, which just happens to be probably my most successful DRIP investment over the past few years (oddly, I feel less inclined to share less successful examples from my own portfolio).

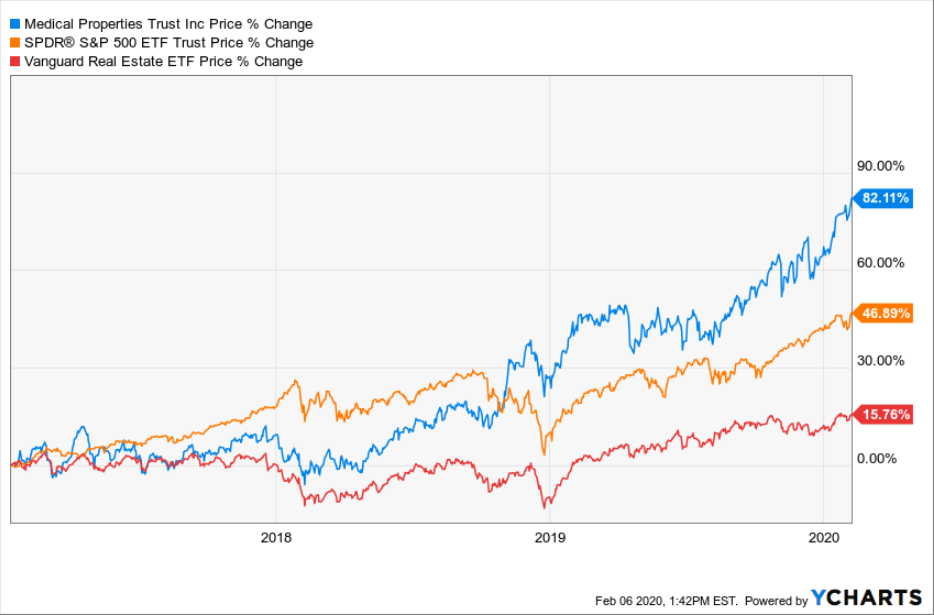

I’ve owned Medical Properties Trust (MPW), a REIT that primarily owns hospital properties, for about seven years now, and it has compounded to provide an exceptional return over that time… but that’s largely because the dividend yield is and was quite high, and also because there was quite a bit of room for the company to get a richer valuation over time as investor sentiment about their prospects improved. Let’s just look at the past three years, since that simplifies things and I know a lot of investors have trouble envisioning 5-10 or 20 year holding periods.

As of January, 2017, I held a position in MPW that at the time was worth about $12.50 per share. It had a trailing yield of about 7% at the time. It was seen as fairly risky because a few of their tenants were in some distress, but not super risky (2016 had been worse), and they had a couple years under their belt of very gradual dividend increases after a long period of flat dividends following the financial crisis (and a cut during the crisis). It was appealing to me because I thought hospitals would remain critical real estate and local infrastructure assets so were unlikely to become worthless except in a few extreme examples, and they were doing some appealing things to improve their portfolio, mostly by diversifying with new tenants… but it was certainly not a guaranteed winner, and the highish yield reflected that general concern.

Since then, the dividend has continued to gradually grow, they’ve diversified further, and investors have decided they can accept a lower dividend yield so the stock price has surged quite a bit higher, particularly in the last year. That may not last forever, of course, but it means the performance has been good. The stock price has risen 82% in those three years, but if you include the cash dividend payments you received over that time (I can’t chart that, sorry), the total return was about 97%.

Not bad, right? The S&P 500 had a return of 47% in those three years, and the average REIT (going by the VNQ ETF) about 16%. Multiple compression and dividend growth can be powerful drivers of outperformance.

But they’re not the only drivers — the other big one is compounding. What if you let those dividends get reinvested (for free, with almost any broker) into new shares, and those shares then generate more dividends in future quarters? Then you get a dramatically better total return over time…

And it’s not just with stocks that happen to have a pretty high dividend when you start investing, though both the starting yield and dividend growth are powerful factors in leveraging that total return — here’s that same chart with the broader indexes added in for total return as well.

So yes, reinvest your dividends. Try very hard not to interrupt that powerful compounding force if you don’t have to. MPW looked terrible at several points along the way, both in the past three years and in the seven years or so that I’ve owned it, but the basic operations of the business never fell apart and the capacity to pay and even raise the dividend was never really in question.

Sometimes a stock looks great and makes you feel good, sometimes it looks ugly and makes you nervous, but if the company is in decent shape and not doing anything stupid or getting mired in a secular downtrend of some kind for its real operating business (like, say, some shopping mall owners right now), and management isn’t doing something dramatic that loses your trust, then don’t try to sell the top and buy the bottom and worry about the stock price every week… just let it keep compounding. Time is your friend. You made a good decision buying that dividend growth stock that looked capable of compounding your investment over time, try not to rush another decision and mess that up.

There are exceptions to that, of course, but it rarely benefits us to look for them. Yes, sometimes a company is paying a dividend that really can’t be sustained, or sometimes they’re paying out a lot more cash than they’re earning and it’s obvious that the dividend will have to be cut dramatically at some point soon — that’s often worth either avoiding or, if you like to dance on the tightrope, cashing your dividends as long as they can keep the music going but not reinvesting those dividends in more doomed shares. But that’s not usually the kind of dividend stock most of us are looking for most of the time, and if you see a 15% dividend these days you already know that trouble is brewing and investors expect bad news.

But yes, the “Q Shares” are just the latest variation of trying to make DRIP and DSPP investing seem mysterious and secret to try to get you to subscribe to a newsletter. If you’ve got a favorite DRIP stock to share, thoughts about Simulations Plus or Jeff Yastine’s newsletter, or a particular strategy or plan that works for you, please do let us know with a comment below.

P.S. I always like to point out when a newsletter offers a “teaser price” or otherwise has a built-in escalator for your subscription, and Total Wealth Insider does just that — they use the same basic subscription model as the other entry-level Banyan Hill newsletters, including the one from Charles Mizrahi that we looked at recently: They offer a basic $47 e-subscription, but once on the order form they push the $79 subscription that includes a print newsletter and some special reports, and include in the small print that you’re also getting a “free trial” to a second newsletter, and that both of those newsletters will autorenew at the then-current price… so as of today, your payment of $47 for the first year, if you ignore it and let it autorenew, will add $97 after the “free trial” of Automatic Fortunes expires in three months and then balloon to $194 a year for both letters. They’re not hiding this, though you might need to pull out your reading glasses to avoid missing it.

What would you say are your top stocks / ETF / trusts with dividend compounding potential? Is Medical Properties Trust still up there despite a hefty valuation?

MPW is 5-10% over my preferred buy point after another good quarter, but dividend stocks have almost all been bid up pretty aggressively in the last six months, haven’t been finding a lot of appealing ones recently.

Interesting read Travis, i think i will pass on this one though. It is too small and an upstart company i don’t really like the thought of selling something like this to anyone willing to pay you a subscription fee etc. I have 4 DRIP plans, i’ve had Home Depot for about 20 years now and it has done very well. The thing with these reinvestment plans is to stay true to the plan and invest new funds monthly or at least quarterly over time. Shares owned are in my name, not in “street name” as with any stock brokerage.

if you had purchased slp at $35 per share, it is currently worth over $54 per share – an increase of over 55% in about four months while the majority of the market tanked.

Intel used Computershare when I first joined back in 1996. In 2000, they transferred stock admin to UBS, but I left my original shares in Computershare with DRIP enabled with no further contributions. I now have 55% more shares than when I started. I believe wholeheartedly in taking full advantage of DRIP!

Looked at the Q shares beginning to ending! I call these pumper information for big cash info paks!

Well after following it through one thing you already pointed out as “great-deal behavior*” is two years for the price of one!! There is a 60 day return on your money on this one, not the case before when Casey was on his own!

The double your value at a preset cost for the extra years behavior has been pointed out by Dr.Thinko before*!

The sample free to audience listeners’ “OMEGA share” is for a code they give out for a sold, rejuvenated, reconstructed company name (to protect employees) I will not reveal here!

But that code has one more letter than the regular ticker that is alphabetized next to it in a stocks one can trade!

The special Omega code share ticker shows a stock share price amount about 1/11th of the regular ticker stock price! It becomes clear how it is set up when one looks up the actual company’s disclosed name (they shared) on one’s trading site where you find it has the pumper’s referred to Omega secret backdoor bargain priced version of the stock ticker listed with its similar full open market non-omega code, just below it is listed its similar regular ticker symbol! The trick seems to be if one can afford the $ 1.39 a share that is the Omega code price, one can buy them and then take that quantity of shares and sell them at the full price at the regular stock ticker price about $14.30 a share!

Another twist! And if one is not rich enough to pay the $2K info pak going price tag one can cover the cost after buying then full price re-selling about the quantity of cheap shares ($1.39) spending from about $185. spent on the $1.39 shares! Then one collects about enough new cash so one can afford to buy the $2,000. cost of the “info pak”!

If this is not the “Q” shares story, IT IS ANOTHER STORY- the Omega shares concept-, if it seems different it may be; but was just out there a 1+ hour presentation on about 2/5/20?!

Just wonder how the poor Co involved can afford this and the risks potentially inherent in the rest of the picture! The pumper interviewer mentioned $6M of the pumper’s own cash in tge picture, could be that!? Hope so!

➡️FYI ?…If not same as the Q shares it could be a separate gimmick!?

Got your bird dogs fed and watered?

Wow! Hope it is all righteous!

Best, Marion

Nancy, I sat through the same video for Omega shares but it was with E.B. Tucker, not Jeff Yastine and talking about warrants, not DRIPs. Maybe the computations for these two assets follow the same or similar formulae?

In fact, I was waiting for someone to start a discussion on the Omega shares. Seeing none, I posted one myself a few minutes ago.

Sounds like call options.

What is this Dark Hours Trading scheme by Boill Polus?

Correction, Dark hours trading is by Bill Polue, head of Profits Run.

I’ve been ready Gumshoe for years now, and it’s the VERY first I’ve seen Travis “I’m going to buy a few of these (SLP)…” johnny-on-the-spot. Somehow Yastine needs to be considered for some entry in Guinness!

Ha! It’s true, I don’t often have an immediate positive reaction to a teased stock… but of the 48 stocks currently in my portfolio, I originally learned about ~15 of them from a teaser ad, and some of them I bought almost immediately upon researching that teaser pitch.

DRIP INVESTING ISN’T AS GREAT AS IT MIGHT SEEM. FIRSTLY WHERE DOES THE MONEY TO PAY THE TAXES ON THESE REINVESTED DIVIDENDS COME FROM? YOUR BUTTER AND BREAD MONEY? SECONDLY, MOST PEOPLE INVESTING FOR DIVIDENDS WANT THEM TO SUPPLEMENT THEIR INCOME, RATHER THAN REINVESTING. THIRDLY, DO THE PROJECTIONS ON LONG TERM GAINS REDUCE THEIR PERCENTAGES BY DEDUCTING THE TAX PAID ON THOSE DIVIDENDS? OF COURSE NOT. THAT WOULD DISMANTLE THE PIE IN THE SKY HOOPLA.

DRIP investing is definitely not an effective strategy for those who need the dividend income in cash. My assumptions do not include taxes, I assume these are held in tax sheltered accounts… yes, taxes would generally eat some of the dividend, though dividend tax rates are fairly low for most people.

No strategy works perfectly for everyone, that’s for sure. DRIP investing may appeal is greatest if it has a few decades to play out, and with DSPPs more specifically, if the discipline of a regular investment strategy helps you to invest more over time without the temptation to trade in and out regularly.

And, of course, the biggest risk of them all is that you have to pick the right stocks that can grow for decades without imploding.

You don’t have to reinvest the dividends, I don’t need the income yet. I get a 1099 for tax purposes every year so pay tax as i go. My 89 year old mother opts for a quarterly dividend check and pays tax yearly as well and yes the income helps meet her expenses which is why we all invest isn’t it?

I looked at SLP and it seems to have a good wedge pattern in the price action. I will be watching it, and may even get interested if the volume increases a bit. Thank you for the article.

Thank you for the nice sleuthing and this website in general. I’m in one of the Banyan Hill upsell bundles and can confirm that #SLP is one of the three ideas in the bonus stock report.

Travis, what is the $3.00 stock being pushed by Alexander Green of the Oxford Club organization….this one stock can fund your retirement, he says?

A. GREEN WANTS $444.00 IN ORDER TO TELL YOU HOW TO BUY IT….is it a Biotech stock or a different tech. stock?

Bob Hahn, irregulars member. 02/17/2020.

For the past few years that’s been a pitch about FoxConn — I’ll look to see if there’s a new “$3 stock” tease from them recently.

Bought SLP three times since reading this article… Great returns

Thank you for the information, however I didn’t get how to buy the q shares of this company or is it the actual qqq shares? I am not getting it. also I am wondering if it is wise to drip my dividends automatically. My point being after the dividend the stock dips to accomodate the pay, but is it better to take your dividends and buy during the dip?

“Q shares” is just a reference to

Warrants — they trade like stocks, but review the details carefully (strike price, expiration date, other terms). QQQ is just an index ETF that includes the largest 100 companies on the Nasdaq, mostly tech and biotech stocks.

Some people trade around dividends, which can work if you have discipline — but don’t try it in a taxable account, you’ll hit wash sale rules and probably end up with a lot of short-term taxable gains.