Today we’ve got a bit of a quickie for you, mostly just because the clues that were dropped were extremely limited… but it also happens to be a stock I’ve looked at before, so I thought it was worth taking a second look today.

Paul Mampilly over the weekend was peddling his True Momentum service (“retail” is $5,000, it was being sold for $1,995 in this promo, no refunds) with a shortish email ad, and we got these clues about the “secret” stock being teased, a recommendation to his subscribers that was supposed to go out “next week,” so it is either out now or will be out in the next couple days.

And those clues?

“I’ve had my eye on a secret tech company for over a year now … biding my time…

“It’s a company that’s critical to the operation of the internet.

“It serves industries as varied as aerospace, defense, banking, health care and government, to name a few.

“Its sales are growing at a rate of over 18% per year.

“And just earlier this year, it signed 599 new contracts!”

So who is it? Well, I can’t be 100% certain given those limited clues… but the Thinkolator gives us a high degree of likelihood that this is the odd little data center company Switch (SWCH).

Which, yes, did announce that they had signed 599 new contracts with customers back in their second quarter presentation (and that they brought on 34 new customers) … and also that they have had a compound annual revenue growth rate of 18.3% a year over the past five years, though that also flags some of the challenges for SWCH (that their growth rate has slowed considerably, it’s under 10% a year more recently, and that their cash flow has not actually grown as fast as their earnings so there hasn’t been an obvious benefit from increasing scale just yet).

I added Switch to my watchlist in September of 2018, after they had seriously tumbled from their late 2017 IPO, though I’ve never bought shares.

Switch (SWCH) is a new data center company that went public about two years ago. They are small, still, with four campuses either operating or planned and three large data centers in operation, and you can get an idea of the way Wall Street is currently thinking of them by looking at their stock chart compared to the five major US data centers and one European one — for what it’s worth, InterXion (INXN), the Europe-focused data center owner, and Switch (SWCH) are the only ones that aren’t structured as Real Estate Investment Trusts (REITs — pass-through investment vehicles that are designed to distribute cash flow and all taxable income as dividends and thereby avoid corporate taxes).

Do note that most of those data center stocks trailed the S&P 500 over the past couple years, even with the relatively high dividends that most of them pay — that’s partly because they overshot in 2016 and 2017, when most of them did far better than the market (except for QTS), so the market went into that October 2017 SWCH IPO predisposed to adore data center owners… even if this new one wasn’t actually a REIT and was at a different point in its development phase. This was one of the bigger tech IPOs of 2017, and it definitely captured the imagination of investors with a big first-day IPO pop (from a predicted $15 a share to $20 or so)… though the valuation was pretty aggressive at that IPO, at least in terms of earnings, and, as you can see, the stock has mostly trended down since.

There are obviously some challenges for Switch, particularly because this is an industry where there is a strong network effect and some benefit for operating a big network of locations — if you’re a large company and can deal with one data center provider who can get you space in a dozen different places around the country (or the world) to provide fast colocation coverage, then that may be more appealing than dealing with half a dozen different smaller providers… Switch isn’t the smallest of the data center companies, but it is among the smallest (CoreSite, which I own, and QTS are of pretty similar size), and, because they focus on this “hyperscale” idea instead of on larger numbers of colocation facilities near key internet and telecom centers, it has by far the smallest number of locations.

Still, many of the data center companies work with a bunch of the same large-scale customers, and, indeed, in some cases even build their own centers (the big guys like Facebook and Google are on a massive building spree, too)… so there’s no real sign of data centers becoming a “winner take all” category, there are definitely unique advantages of particular locations if they can get the right power and telecom infrastructure in place to keep costs down… but there is generally a pricing advantage for those centers that can get you prime colocation space near major metropolitan areas and major telecom hubs, since that speeds up connections and everyone wants more speed.

So how is Switch different? Well, it trades at a much smaller multiple of sales — about 3.5X sales, versus more like 8X sales for the bigger players. And it’s focusing on what it calls “hyperscale” centers and is focused on building differently, with their roots not in services or real estate but in data center design and optimization. That hasn’t made a difference yet, they don’t seem to be getting premium prices, but it is still early and they are actively building so if they can continue to get cheap access to capital they may be able to dramatically ramp up revenue over the next few years if they can build quickly. That’s two “ifs”, which perhaps is part of why the stock is not doing very well.

They’re also not growing as quickly, which deters investors — generally, we expect smaller stocks to have faster revenue growth, but in this case Switch has grown its revenues only about half as much as some of the larger competitors like Equinix and Digital Realty over the past couple years. That could change, of course, as they built out their fourth hyperscale center, or if they can get better pricing and higher occupancy, but so far they look like a laggard when you just skim through the numbers.

They do have some potential for strong branding, their centers do look distinctive — and they have at least one well-known building, their “east coast” hyperscale data center is in the Steelcase Pyramid in Grand Rapids, Michigan, so they got a little attention for saving and repurposing that iconic structure.

There’s very little institutional ownership of this one so far, partly because they aren’t in many indices so they don’t have that massive Vanguard/Blackrock/Fidelity etc. share holding at the top of their charts, though Vanguard has begun to move in over the past year. And I would guess that they’re at least a couple years away from considering a conversion to REIT status — mostly because they aren’t really paying taxes yet, so they don’t have a need to avoid taxes (and conversion is not as “automatic” at 21% corporate tax rates as it was at 35%, I expect, but we’ll see).

But since most of the large players in the space trade at premium valuations to Switch (perhaps deservedly so), and since most of them are REITs and are generally evaluated based on their funds from operations (a cash flow measure that REITs favor) rather than their earnings, I thought it would be interesting to see what Switch would look like as a REIT.

Switch would have had trailing funds from operations of $144 million over the past year, according to YCharts, so that’s dramatically more impressive than the $4 million they had in actual net income. From a market cap of $3.5 billion, however, that means you still end up with a pretty rich valuation — that’s 24X trailing FFO. By way of comparison, CoreSite would come in at a trailing 17X FFO, industry leader Equinix (EQIX) at 23X, Digital Realty at 21X. The only data center REIT that’s smaller than SWCH, QTS Realty (QTS), would have a trailing Price/FFO of about 18X and is also growing revenue faster than SWCH.

"reveal" emails? If not,

just click here...

So you can’t really argue that Switch is undervalued relative to the other big data center companies… to buy the stock, you’d have to be convinced that it’s at least as good as those companies despite its smaller size and lower growth rate, or that their future is substantially better because of their unique capabilities or footprint. It might be that they are better, but don’t skimp on the research or rush into it if you’re making that argument — usually those of us who are not experts on a sector or a business are better off letting the numbers tell us which company is better, and when it comes to margins and growth rates there’s no sign that Switch’s different “hyperscale” strategy or unique designs are helping them perform any better, at least so far, than their larger and arguably more boring competitors.

On that front, there is some hope — one analyst, Ari Klein from BMO, met with Switch management last month and came away somewhat convinced of their differentiation and their advantages… here’s a little excerpt that was posted by Benzinga at the time w(this was about six weeks ago, when SWCH was right around $16):

“BMO hosted investor meetings with Switch’s senior management with three main takeaways, Klein wrote in a note.

- Switch’s management emphasized how it stands out against the competition, especially at Tier IV Gold. For example, a contract with Switch includes a telecom cooperative that offers 30 to 50% savings on telecom bills and supports high power densities of 50kw-plus per rack. This results in “unmatched customer stickiness” as evidenced by a very low churn rate of less than 1%.

- Recent momentum includes large contract wins with a top five global cloud provider and FedEx, both of which can expand from the current 5MW agreement. Leasing remains “healthy” across open data centers and management will stand charging for cross-connects which it historically hasn’t done for CORE customers. These catalysts support the potential for 10% or more EBITDA growth.

- Capex levels are likely to normalize from as much as $402 million in 2017 to around $260 million. Leverage shouldn’t change from its current multiple of 2.3 times which is notably short the industry average of 5.3 times.”

So those are reasonable starting points for making a “Switch is better than the others” argument — not really the 10%+ EBITDA number, since that isn’t really better than their larger peers have been doing, but the low churn rate is good and provides hope for stability… and the low leverage number does stand out as a real difference, though that’s not likely to get investors excited in this environment (with low rates and peers that all have debt service that’s twice as high, it seems in part as though they’re just deciding to keep debt levels arbitrarily low and therefore make less money for investors, though that calculus changes quickly if people start to worry about debt again someday).

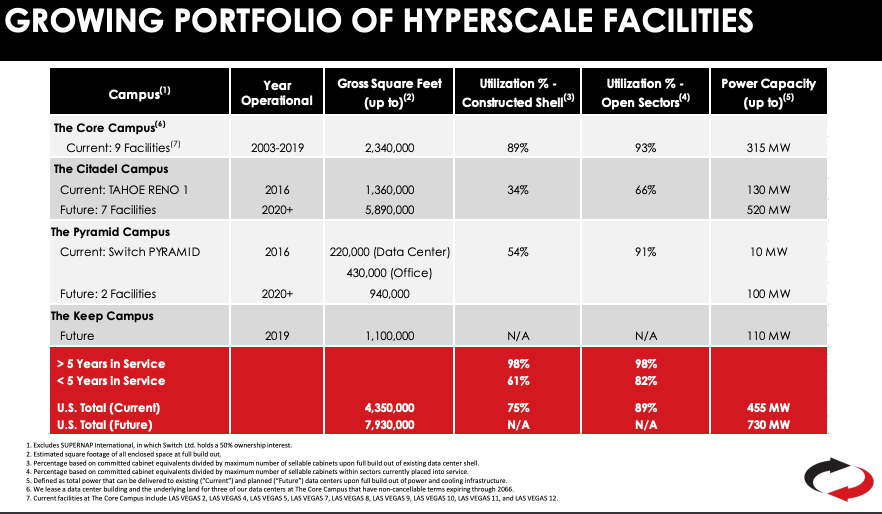

There is some growth in their plans, despite the small number of locations — they are adding space to their Core Las Vegas campus and in Tahoe/Reno, which is their largest facility by far (called The Citadel Campus, that’s the one with the largest growth potential as they envision expanding in the future), and they plan to open up their 4th location, the Keep Campus in Atlanta, before the end of the year. Here’s the page from their second quarter investor presentation that describes the current portfolio…

So that’s where the hope probably lies… the potential for leasing out current and new buildings in Michigan, Tahoe and Atlanta that still have vacant space, and for doing so at relatively low cost because Switch says one of the core advantages of their patented technology and process is an ability to quickly open up new areas of their data centers without substantial additional capital cost.

This is also one of those “dual class” stocks, with the founder having overwhelming voting control — and the founder is a bit unpredictable, Rob Roy describes himself as a futurist and a “inventrepreneur” and kept 68 percent of voting control after the IPO (Roy owns a little less than 20% of the shares, but most of those are Class C shares that have 10 votes each so he (and his heirs) have pretty much complete control of the company, perhaps in perpetuity). Perhaps that’s why SWCH pays a dividend, too, just the tiny dividend (just under three cents per quarter) on his SWCH shares should give Roy about $5 million a year in income should he need the cash flow (that’s more than twice his actual salary).

Guidance for the full year 2019 is for revenue of $445 million, adjusted EBITDA of $226 million — analysts translate that into earnings per share of 15 cents, followed by 26 cents in 2020 (on $498 million in revenue). At that rate, then, you’re paying roughly 50x forward earnings, which is again similar to the data center REITs, and for growth that is also likely to be similar.

There’s still some hair on this stock, in my judgement, particularly because outside investor pressure might have no influence on management, and there was also some pretty substantial selling by early venture backers earlier this year… but if they can lease up those new spaces more quickly than analysts expect their cash flow could get pretty compelling and make it worth the risk, and I think there’s some real potential to catch the eye of more investors if they also eventually convert to REIT status. It’s still on the watch list, I watched it fall below $10 and recover and did not decide to buy over the past year, but I’m still intrigued… and I’ll let you know if I end up buying the shares. To my mind, there’s still no real hurry… particularly because they report earnings tomorrow. I’ll let you know if my thinking changes.

P.S. Want a final match to back up the Thinkolator’s answer? Switch did have a surge on Tuesday at about Noon, jumping 5% in the space of a few minutes on no news as the stock absorbed trading volume that was about 3X recent levels — and that could easily have been caused by a recommendation from a newsletter from a larger publisher. As is very often the case with newsletter recommendations, it came right back down — so the shares are now down about 2% in the past week, more or less in line with most of the data center stocks… a reminder that even if you’re excited about a new recommendation, there’s usually no need to chase it.

P.P.S. I don’t think we’ve seen any reader reviews of True Momentum at this point, though it is discussed from time to time on the site, so if you have ever subscribed and would like to share your experience, please click here — your fellow investors would love to know what your experience was like. Thanks!

I took his news Profits unlimited for a short time . Stopped it in less than two month. Only get emails to up grade to a higher price news letter. No grate stocks to buy. I did get my money back. Maclin

I was an original subscriber to Profits Unlimited and I agree with maclin, but unlike maclin i stuck around for about 9 months before i deeped it and there is no way I would take a more expensive publication from this former darling of wall street. Travis is it just me or is there a real trend that so-called superstars on Wall St. gther their milions and then to be stressed out by all the pressure of wall street only to quit and then reappear as the hot new newsletter writer and analyst peddiling mostly garbage for main street? Excuse my jaded view but I believe that the whol lot of these guys are no more informed than all of us, but thank God for you. I always get the skinny from yur comments and research . Carry on sir.

It’s certainly true that hundreds of newsletter editors claim to have been hedge fund stars and now just want to help the little guy 🙂

Investment banking and asset management can be a punishing and high-stress business, I’m not surprised that some of those folks find the idea of writing a newsletter more appealing.

Looks like it was a pretty nice quarter from SWCH, mostly because they raised their guidance for EBITDA growth.

Travis, I will never consider joining a newsletter without checking in with the Gumshoe. I just joined your site this week. The main reason I found you is because I have my own site and I was considering a “Scam Watch” page. In my research I came across the $tock Gumshoe. In just 1 week I think you’re the best! I will no longer consider adding my new section. If it’s OK with you, I’ll still have a section where my readers can investigate if a teaser ad is legit or not, but I link them to your site. Like I said, you’re the best! Plus I’m a one man operation, you’ll save me a lot of work lol.

With my site Main Street beats Wall street, I teach how to trade options. I’m completely free and always will be! And I’m yet to find anyone one who has my results. As of Friday, up 78% year to date. But I’ve been doing this for 30 years. I love to teach! I post my trades the minute I make it and the minute I get out. Please check out my site and approve me to link $tock Gumshoe to my scam watcher section.

http://www.mainstbeatswallst.com

If you want a really good REIT to buy look at SUI – it has a no loss 10 history, around 30% average return over those years and pays a dividend of around 2% per year.

This in my portfolio and the best REIT I have found so far

New one for me, thanks — Sun Communities has had a great few years, for sure, looks like they aim for the retiree and entry-level buyer with RV parks and manufactured home developments, which probably keeps their costs low.

Am a subscriber to Profits Unlimited on automatic renewal but have changed my credit card details so am being asked to update. NOPE ! It is a hard road to travel and realise the learning curve you need to take before you can be consistently successful’ Have lost money on Kiyosaki ,$1999 no refund . Am learning and have narrowed my n/letters to Altucher, Alimetry ( basic} as well as Jeff Clark and Boom & Bust which I have let slip in for another unwanted year Irregulars is one of the most informative. In general am oversubscribed to too many n/letters, banyan hill and agora are the ones that have taken a toll on my subscribing dollars. Rickards and Bauman takes me where I cant make money. God Bless

@hanalei214 I get it, I did the same and have been dumping them like a bad habit. I finally learned some skills in tech and fundamental analysis and I am working on the skillset to be a better trader. Plus, Stock Gumshoe is amazing of any service. Good luck on your trading future.

I like the articles of this publisher. But all of them are toooo long. Please forgive me. This is just a matter of time… nothing personal.