“#1: Collect an unmatched 7.6% in tax-free dividends and save thousands of dollars on tax every year

“#2: Get in now at a 15% discount

“#3: Grab up to 87% in potential gains in the next 12-24 months“This is the BEST tax-free investment available in America right now”

That’s the lead-in to the latest ad for Tim Melvin’s Underground Income ($595, 60-day refund period — that’s “on sale,” though it’s also the same price it was offered at in all the previous ads we’ve covered for that relatively new “upgrade” service).

More detail…

“It pays 7.6% in tax-free dividends every month — which beats any other tax-free type of investment you can get….

“And this discount is highly likely to return to a regular price because of a unique business model behind this stock.

“This means that when you buy it now, it’s almost like getting a guaranteed 15% gain — simply by owning and holding this stock….

“But more importantly, this single stock can be your safe haven against ever-rising prices… inflation… growing property tax bills… and most of all…

“It can shield you against inevitable tax hikes caused by a massive, $33 TRILLION national debt”

And that’s a big part of the “scare you into this investment” pitch, that you’ve got to get ready for much higher tax rates…

“This debt is the biggest in our nation’s history. What’s worse, it is now spiraling out of control and forcing the government to reach deeper into OUR pockets…

“To pay for their reckless spending…

“Or else the entire country will be forced to declare bankruptcy — which would, quite literally, mean the end of America as we know it.

“Obviously, they will never default on this debt… that’s why they’ll choose the one option the US government always uses in situations like this one…

“They’ll introduce tax hikes which will kill your income, lifestyle, and retirement plans.”

And he puts it another way here:

“With $33 TRILLION in debt and growing, our government can’t default on it…

“Because that would mean, quite literally, the end of America

“So they have only two ways to solve this problem:

“They can either cut their expenses…

“Or…

“They can raise taxes….

Are you getting our free Daily Update

"reveal" emails? If not,

just click here...“Why would they cut their own spending… when they can force YOU to cut yours?

“How?

“Of course, with TAX HIKES….

“When the US national debt spiraled out of control before…

“The government ignored all the other options and chose to raise taxes on your parents and grandparents

“And they’re doing this again as we speak.”

OK, yes, it’s hard to argue with the logic of that… but do be careful, it has been obvious and widely discussed and a core part of investment teaser ads for almost 40 years that the US federal debt can never be repaid, and that the deficit is reckless and we’re all going to hell in a handbasket as a result. And that has been true, mathematically speaking, for decades — it’s pretty much impossible for the US to ever repay its sovereign debt, and has been for a long time, since well before the debt ballooned through the past decade of spending increases and COVID stimulus and tax cuts.

And yet, taxes are meaningfully lower now than they were when we started this borrowing binge in the 1970s and 1980s to pay for Vietnam and the promises of the Great Society and spending the Soviet military into submission, and the US has been able to service it’s debt and continue to grow that debt to pay for endless wars, and for major stimulus programs in times of peril (financial crisis, pandemic, etc.), and politicians have become accustomed to promising every voter the moon (we’ll spend on whatever you like, and we’ll cut taxes!).

Still, the tax increases that were squeezed through a couple times in our recent history, a little bit under Clinton and Bush I, then a little under Obama and Biden, interspersed with tax cuts, are really small blips on a pretty steady downward line in average individual income tax rates over the past 40 years (and average corporate tax rates have fallen more substantially, most dramatically under Trump’s tax cuts, though corporate taxes are a much smaller part of the pie than individual income taxes). And other than a brief period in the 1990s, when tax increases and spending cuts coincided with a windfall from the internet boom, which was partially luck and partially a brief moment of bipartisanship when government was sharply divided but Newt Gingrich and Bill Clinton found a little common ground, we’ve never really had a balanced budget or reduced the debt in my lifetime (I was born in 1970).

It does make logical sense that this will “break” at some point, and maybe this is that point, with interest rates soaring higher, faster, than at any time since the early 1980s. I’d just caution you that although the logic makes sense, essentially the same logic also made sense ten years ago, and twenty years ago, and even thirty years ago… predicting when the unsustainable will stop being sustained is not a job for the faint of heart, and if you had been scared out of more lucrative investments because of your worries about the debt even ten years ago, your portfolio would be the worse for it.

Logic should matter, but the global “macro” picture doesn’t care about your logic… at least, not when it comes down to very short time frames like “a decade” — that obvious logic you see in history was not generally obvious to people living that history at the time, or at least was not predictable when it came to the timing of major financial or political transitions that appear obvious and inevitable in retrospect. A person can be logical, but a crowd is unpredictable… and that’s what the stock market and the economy are, crowds, and the politicians cater to crowds.

But yes, I agree, it’s safer to assume that taxes will be higher in the future, not lower. The money has already been spent, and probably, at some point, we’ll have to pay the piper. And if interest rates remain “normal” (say, ~100 basis points above whatever the inflation rate is), then servicing the debt will gradually become the largest obligation of the federal government (it’s already catching up with the largest discretionary spending pool, which is defense spending, though it’s still far smaller than Social Security or Medicare/Medicaid). Since we’re nowhere near a balanced budget, and nobody in Washington really takes that seriously (which isn’t necessarily their fault, we’re the ones who sent them there and told them that they only keep their jobs if we get our spending and our tax cuts), we should assume that it will continue to get worse. We just shouldn’t try too hard to pinpoint the moment when it breaks, or bet our portfolio on that timing — not because being right wouldn’t be worthwhile, but because the odds of being right are so low. Leave the forecasting to the meteorologists, they’re a lot better at it than economic forecasters.

OK, lecture over… back to the tease.

“America’s #1 Tax-Free Stock — a true generational buying opportunity.

“It has an unmatched 7.6% tax-free dividend yield — which beats other tax-free investments by 32%

“And yet, this stock has nothing to do with your IRA/401k… or buying insurance.

“It’s NOT a municipal bond.

“And it’s NOT a mutual fund.

“It’s something WAY more exciting than that…

“And way more unique.

“In fact, more than 97% of Americans have no idea this stock exists…”

And he lays it on thick with the “no taxes” stuff…

“And you won’t pay a dime in federal taxes no matter if you make $10,000 or $100,000 with your dividends

“Pay zero taxes when you collect your income.

“Pay zero taxes when you withdraw it.

“Pay zero taxes when you reinvest, compound, or save.”

And says it has the endorsement of Morningstar, the personal finance and mutual fund analysis firm…

“… the company behind this stock just received the highest, 4-star rating from Morningstar — for their unique business model.”

Well, the highest rating from Morningstar is actually five stars… but we’ll leave that for a moment.

“Instead, with America’s #1 Tax-Free Stock, you collect 50% more income than you get in a savings account…

“And you’re not paying a penny in taxes.

“Keep money in your savings account or CD collecting 5%, and you’re paying capital gains taxes of 15-20%.

“But why do this? That money is yours.”

OK, I don’t know where he gets that from — you don’t pay “capital gains taxes” on your savings account. You do pay income taxes on the income you receive from your bank, so the interest is taxed, which means that if your combined federal and state tax burden is, say, 28%, then your 4.99% yield is really only a 3.59% after-tax yield. But there are no capital gains in a savings account, so you don’t pay taxes for withdrawing that money.

What other hints do we get about this investment?

“It’s a long-term buy-and-hold position…

“Remember, if you buy our #1 tax-free stock now, you’ll secure a juicy 7.6% dividend yield… paid monthly.

“Such a high yield and monthly dividends are a perfect scenario to compound your income for 12-36 months…

“And rapidly grow it to $4,579.01 and more — with just $50,000 down”

So you’re probably thinking, “this must be about municipal bonds,” since income from muni bonds (money borrowed by state and local governments) is not taxable at the federal level — and yes, he finally admits that this ‘stock’ is actually a municipal bond ‘fund’…

“How is this stock able to pay you tax-free money?

“I’m glad you asked.

“See, this stock is a very specific type of fund…

“But, as I mentioned earlier, it’s not a mutual fund.

“Instead, it’s a Tax-Free Fund.

“What is a tax-free fund, you’re asking?

“Well…

“It’s a rare fund that focuses solely on generating tax-free income for its investors.

“This specific tax-free fund was created with one goal — to create a highly diversified portfolio of municipal bonds…

“And pay us big, monthly dividends….

“And because it’s a fund, it’s more diversified than just buying a handful of municipal bonds, which is something a lot of retirees do for tax-free income…

“Buying this tax-free stock is like owning thousands of different municipal bonds, like:

“General obligation bonds — Typically issued by state and local governments to finance a variety of public projects, such as schools, roads, and bridges.

“Revenue bonds — Also typically issued by state and local governments to fund projects that are expected to generate revenue…

“And mortgage-backed bonds — They provide more capital for lenders to issue more loans, and help people buy more houses.”

And, like most closed-end funds, it currently trades at a discount, which is where he gets that “15% discount” part of the tease…

“See, when you buy this stock right now, you’re buying the bonds this fund holds for 15% OFF their market value.

“This means that if a single bond traded for $1 — you’d get it for $0.85 if you bought this stock today.

“How is this possible?

“Because contrary to all the other funds out there, our tax-free fund has a fixed number of shares”

And he says that people panicked and sold out of this fund when interest rates spiked higher, which caused that discount to rise, and now it’s a bargain…

“They’re selling our tax-free fund at the absolute worst time possible.

“Because of that, they’re driving its price to the bottom…

“And this is where we step in to buy the fund at 15% BELOW its asset value…

“Which means we’re buying the bonds it holds at a discount.

“AND, because the price is so low — it unlocked this ultra-high 7.6% tax-free dividend yield for us!”

Yes, closed-end funds are like ETFs or mutual funds… except the closed part really matters, they can’t easily create or destroy shares, so the price doesn’t automatically adjust to the fair net asset value every day, like it does for open-ended funds or most ETFs, it is determined by supply and demand. When people want to sell, they’ll give up the shares at a discount to the value of the portfolio, and when they want to buy, they might pay a premium price.

Most closed-end funds are bought for income, and many of them also manage the income they generate, to help it appear stable and reduce fluctuation to please investors, though the actual income they receive from their portfolios (mostly bonds, in this case), and the market value of those bonds, fluctuates all the time… particularly now, with rates changing so quickly.

To make it more complicated, most closed-end funds also use leverage to try to generate a higher yield (meaning, they might have $100 million in investor money, but also borrow another $30 million so they can manage $130 million and earn more income and distribute a higher dividend), which is why bonds that might pay an average of 4-5% coupons can be boosted to create what Melvin says is a 7.6% yield — but sometimes, we should remember, the cost of that leverage can rise dramatically, particularly if it’s borrowed short-term, and it can eat up more of the income from the bonds they hold, which also scares investors away (money market funds pay almost 5% now, remember, and money market funds are really just the source of cash for the short-term borrowing by governments and corporations — if a closed-end fund’s cost of leverage goes from 2% to 6%, for example, that eats up a lot of the income from those 3-4% municipal bonds, even if the leverage is only supporting 20-30% of the portfolio).

“And apparently this is a fund which has an end date, which is a little bit unusual…

“This tax-free fund is paying a guaranteed profit!

“Why guaranteed?

“Because this fund holds bonds — and all the bonds have an expiration date.

“When bonds expire, you get back the money you paid for them.

“So when the bonds this fund bought expire, the fund will be liquidated…

“And you’ll be paid the real value of the bonds assigned to your shares.

“So if you buy this fund and the bonds it holds for 15% OFF now… you’ll gain this 15% when the fund is liquidated!”

He also believes that interest rates will drop sometime soon, and that would create the potential for big capital gains…

“Thanks to the low price, we collect the incredible 7.6% tax-free dividend that will play a major role in preserving our income in the coming years!

“But this won’t last long because as I’ll show you in a moment, the Fed is about to cut interest rates…

“And when they do this, the price of our fund will take off… and the 7.6% dividend yield will be gone.

“On that note — there’s one more reason why now is the absolute best moment to buy our tax-free stock.

“It’s because, thanks to high interest rates…

“It offers you an opportunity to collect up to 87% in capital gains…”

And more on that, including a couple clues…

“… before the interest rates madness, our stock traded for about $24.

“Right now, it trades around $15.

“The difference is 46% — so that’s a minimum of what this stock can grow.

“But I think it will go WAY beyond that…

“As the Fed will bring the interest rates back down, people will want to hold onto the juicy 7.6% dividend this fund offers…

“Because there’s simply no other tax-free investment available that pays such high dividends.

“So…

“People will start buying the shares of our stock by the thousands…

“And whenever this happens, the stock price launches like a rocket and breaks all the records.”

And he sees that “rocket” launch coming very soon…

“… this scenario will most likely play out within the next 12-24 months…..

“Because the Fed MUST decrease interest rates.”

And while this particular ‘secret’ fund is apparently Melvin’s favorite, he says he does also recommend other municipal bond closed-end funds…

“Apart from this stock, I have a collection of 6 tax-free funds like this one in my portfolio…

“Which all pay tax-free dividends…

“And in some cases, they’re even free from state taxes, too

“Their dividend yields oscillate around 4%…

“And just like our #1 tax-free stock, when you get in now, you’ll buy them at a discount…”

So he’s pitching what must be one of the more aggressive funds in this group, if the yield is so much higher. Which one?

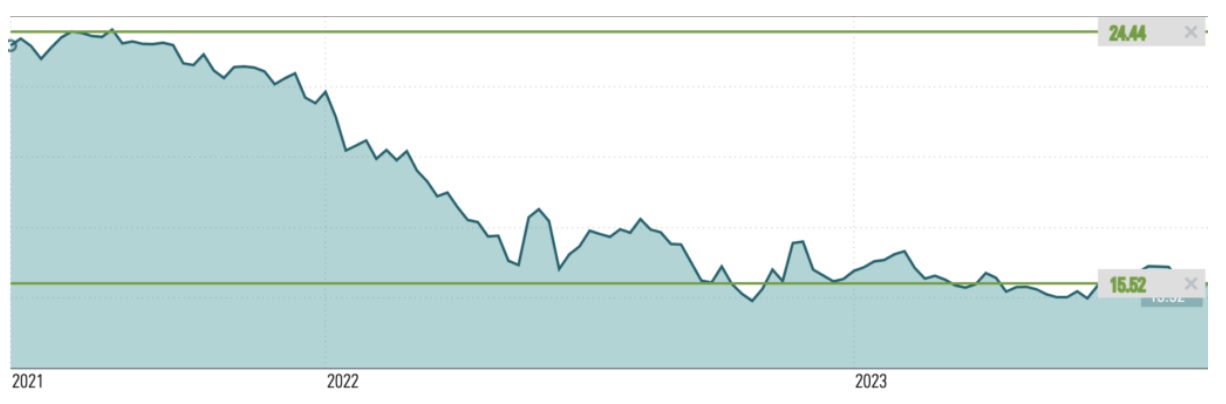

Well, he includes a little chart of this company’s price movement since 2021, which should be a decent clue — it looks like he cut the chart off sometime in early August, for whatever reason, but it’s something:

So… what’s our “tax-free stock?” Thinkolator sez it must be the RiverNorth Municipal Income Fund (RFM), whose chart is a good match for that clue…

Though this particular fund has its own challenges, and doesn’t match the spirit, at least, of some of the loftier promises from Melvin, so we should retain a little bit of uncertainty (if you’ve got a better match, do let us know)… but we’ll look into this one, and what we learn should be generally applicable to most closed-end muni funds. The fund’s strategy and terms are detailed on their website, but here are the basics:

It’s an actively managed fund, and quite small (less than $150 million), though RiverNorth manages a bunch of similar funds (including RMM, RMMZ, RMI and RFMZ), most of which seem to have the same managers, and have similar performance. They use roughly 40% leverage in this fund as of last quarter, and they have a managed distribution at a rate of 9.85 cents per month, so the expected yield when it was at about $15.50, which seems to be when Melvin pulled his data, was just about exactly 7.6%. Again, nothing we can find matches the clues this perfectly. The dividend was slightly higher for the first couple years of the fund (10.4 cents), and it has paid a couple special dividends along the way, but the dividend is managed, it’s not directly driven by their income yield from the bond portfolio in any given month.

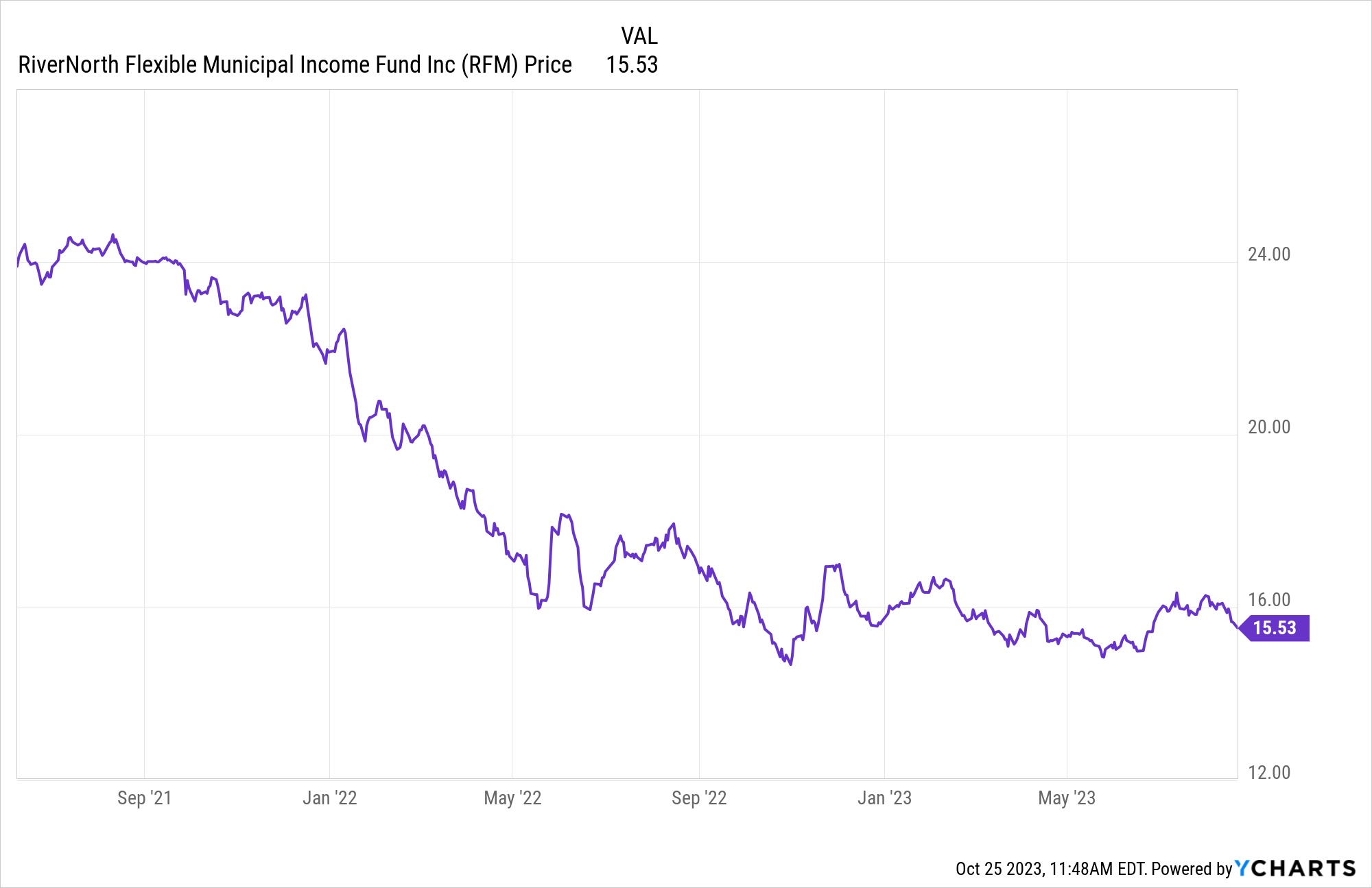

The bond washout from rising rates wasn’t just a thing that drove RFM down in 2022, though — it’s gotten worse in the past couple months, since that chart was created, so now, in late October, here’s what the chart looks like if you extend it out a bit further:

So today RFM is priced at about $13.23. Exciting, right? It’s falling even further, and the distributions for the rest of this year have already been declared, so the expected yield is more like 8.9% now. And it still trades at a pretty big discount to net asset value (NAV), though that discount is about 12.5% today, not quite 15%. That’s one way in which this doesn’t match the clues, this particular fund wasn’t at a 15% discount to NAV in August… though I suppose it could just be a math error from Melvin, the discount is roughly 15% of the share price (you should calculate the discount as a percentage of net asset value, not of the current share price).

Why the discount? Well, like most closed-end funds, it pretty much always trades at a discount — that discount has widened and narrowed at times over the few years this fund has existed (it launched in 2020), but generally speaking, bonds have been terrible investments over the past three years, so nobody wants to own them, so there’s been more selling interest than buying pressure, which drives discounts higher. That could change, particularly if rates stop rising, but I don’t know what’s going to happen to interest rates in the next few years — for whatever reason, Melvin seems confident that the Fed will cut rates next year and interest rates will fall, as the economy weakens, and that’s absolutely possible and was a consensus forecast a few months ago, but the outlook of many strategists, following the latest Fed commentary, seems to be that they’re believing the Fed’s assertion that rates will be “higher for longer.”

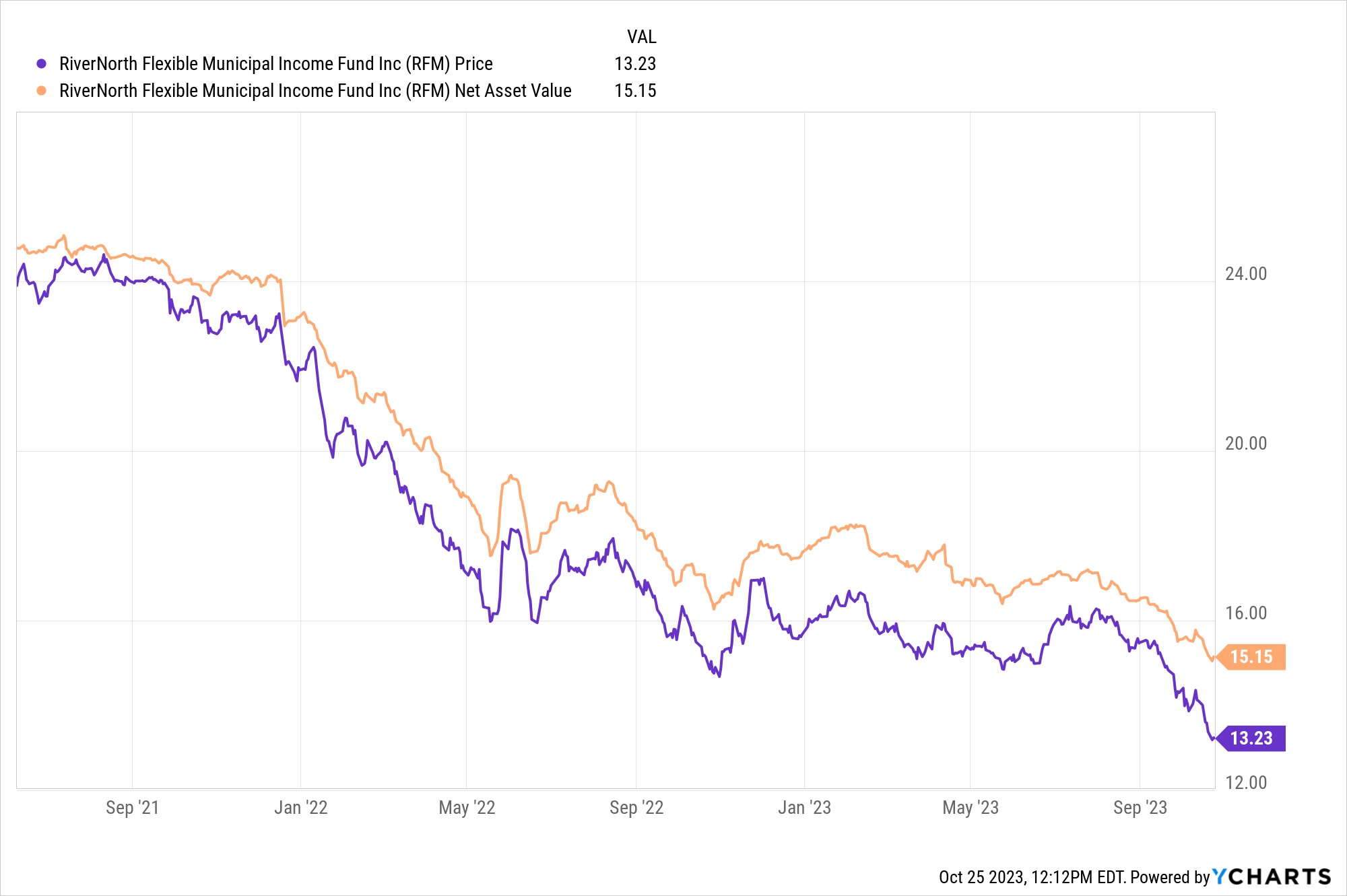

Here’s that same chart, with the net asset value added in as well (that’s NAV in orange, current price in purple).

Why has the net assert value been dropping? Well, we don’t know exactly what changes management has made to the portfolio, but the main reason is, “rates have been rising.” The average term of the bonds in the portfolio is 7-10 years (10 years for the actual bonds, seven years if you account for the net effect of their hedging short position in Treasuries, which helps to manage the interest rate risk), and even if you take them at the hedged term, seven years, the impact of rising rates on the trading value of a bond can be huge.

The turnover has been very high for this fund, with 95% of the holdings changed over the past year according to the Closed-End Fund Association, so perhaps they’re building a more robust portfolio of higher-yielding bonds as rates are rising, but it’s still a dance — a 10-year municipal bond that they owned a couple years ago with a 2-2.5% yield is worth a lot less money now that new bonds are being issued with yields of 4.5-5% (depending on exactly how long is left until maturity, that bond would have gotten a haircut of about 25%).

That explains a lot of the falling net asset value, I’m sure, though if they’re turning the portfolio over rapidly and trying to sell that bond at a loss to buy one with a higher yield, but rates keep going up, they’re just locking in more and more capital losses with each trade, so you’re trusting the management team to really do well at managing that interest rate risk as they recycle the portfolio.

Will the dividend/distribution be all tax-free income? I don’t know. It wasn’t last year. The “income only” yield for the fund, according to the CEFA site, is only about 2.5%, so the rest of it is probably capital gains from trading in and out of bonds and their other investments (part of the strategy is to also buy other closed-end funds as a bet on their discount to NAV shrinking). For 2022, 40% of the dividend was “tax-exempt interest” from municipal bond income, (about 10% of which was subject to the Alternative Minimum Tax), and the rest was roughly split between non-exempt dividends (from other closed-end fund distributions, I imagine) and capital gains (from selling bonds or funds), both of which are generally taxable, though treatment varies. And to be clear, no matter what Tim Melvin says, closed-end funds themselves are not automatically “tax free” in every way — if you sell shares of the fund for more than your cost basis in those shares, you would owe capital gains taxes. Same is true of municipal bonds — the income you earn from them is not taxable at the federal level (and sometimes at the state level, particularly if it’s a bond from your own state), but if you sell a municipal bond for more than you paid for it, that’s a taxable sale.

So this probably won’t be all tax-free income, but some of it will be. The bigger question for investors is, can they keep paying the dividend at this level? They declare their distributions a quarter at a time, so the next announcement is likely to be in the first few days of January, covering the first three distributions of 2023.

How might it look now? Well, if we ignore the ~35% or so of the portfolio that’s invested in other closed-end funds now (that fluctuates, too, based on how “defensive” or “aggressive” management is), and just assume this is a 7-10 year muni bond portfolio that has an average yield of 5% (that’s about what their largest holdings have as a coupon right now), then the $150 million or so they manage should generate about $7.5 million in income. That’s pretty simple math. The management fee (2.3% of net assets under management, so about $2.4 million) and the cost of the leverage they use (about $2.5 million recently, though that could change), would eat almost $5 million, so you’ve got $2.6 million left to distribute as income to shareholders. There are 6.1 million shares outstanding, so that leaves something like 35-40 cents in income to be distributed per share. That’s not exactly how it will work out, and this is not a static bond fund that just holds the bonds and collects the income, they’re also trading in and out of bonds, and the portfolio also includes that second strategy of harvesting closed-end fund discounts at other funds, but it’s the best ballpark I can come up with. Particularly if rates are rising and they’re not going to be able to book capital gains from trading bonds or funds (because they’re dropping in value).

Which means this will probably work out well as an income investment if interest rates fall meaningfully next year — they would probably be able to sustain the dividend and reduce their cost of leverage, and the fund would also look more appealing to investors, so the discount might shrink. It is pretty clearly a bet on rates falling at some point over the next couple years, though, because otherwise they’ll probably have to eat away at their capital to pay out dividends anywhere near the current level — or do some fantastically profitable trading, which I’d hate to ever count on from a closed-end fund. If rates stay stable, I don’t see how they can expect to pay out a distribution anywhere near as high as it is right now… and if rates rise further, it will probably be a disaster for them unless they’re doing a lot of behind-the-scenes hedging (which would also be very expensive, if the hedge isn’t needed).

And yes, this closed-end fund does carry four stars from Morningstar (four out of five, to be clear, not Melvin’s claimed four out of four). That’s because it is a top-quartile fund within the municipal bond category over the past three years, meaning that it has an average total loss of only 5.14% per year, versus -5.4% for the category (and -2.5% for the index). They’ve been in the bottom quartile for the past year, but those star ratings are only based on 3, 5 or 10 year performance. It’s been a historic bond rout over the past few years, and this fund has held up OK because it had a great 2020 and 2021, much better than other muni bond funds (which also did well during that time, as rates went to zero and stayed there), but it has roughly tracked the index through the past year or two of pain and rising rates.

Melvin also noted that you will get paid when the fund terminates, and that’s likely true — the RiverNorth closed-end funds are not generally perpetual, they have a limited term, which should theoretically mean that the discount closes over time because the funds can be liquidated at net asset value when the term ends. That doesn’t mean the net asset value at the end of their life will be anywhere near what the net asset value is today, though — the funds all have different terms, this one ends in 2035 (there are ways they can extend it for a little while, too, depending on what the board does, but if it’s trading at a discount then, the discount should close). Twelve years is still a pretty long time, so that eventual liquidation won’t likely impact the value of the shares much in the next few years.

So there you have it… our best match is a partially tax-free income fund from RiverNorth, most likely RiverNorth Flexible Municipal Income, and it does indeed have a high yield and a monthly dividend right now, though there’s some possibility that the dividend will be lower next year, or that they’ll continue to struggle if rates stay at these levels or rise further. Sound like the kind of investment you’d like to count on as a bedrock income strategy? Prefer other municipal bond funds, or other income funds in general? Do let us know with a comment below.

VWIUX from Vanguard if you have 50K to leave for your heirs.

Yep, that’s probably the cheapest of the intermediate-term muni bond funds, though it’s open-ended so of course no discount, and it’s just an index fund so no juicy (or dangerous) leverage. Annualized yield could inch up to close to 4% if rates stay where they are for a while, the average coupon in the portfolio is 4.58% (and yield to maturity 3.5%), with management fees extremely low, though officially the fund’s distribution yield is only 2.9% right now.

BIV is the roughly equivalent ETF, though ETFs and regular mutual funds do behave a little differently.

It’s easy to get lost in the weeds of “tax free”. If any readers of this blog haven’t yet figured out how to avoid federal income taxes, you have some homework to do. Most municipal bonds are paid off with property taxes. What happens if the housing market goes to hell and people can’t pay their property taxes? Oh, the banks will foreclose. Will the banks then pay the property taxes? The banks are already in bad trouble. Besides, most of the mortgages were sold to the government backed agencies. Most banks are not “servicing” the loans themselves. Will the federal agencies foreclose?

Always a ray of sunshine, Carl 🙂

I don’t have any favorites, though I’m reasonably happy with how my REIT stocks–AVB, ESS–have performed. Not tax-exempt, of course. I’ve got hope for DEI, but wouldn’t put more in there than I’d want to stop loss out of. Their office buildings are well-located and their multifamily is also, but I’m not sure I have a lot of faith in office going forward. Some of their stuff could be converted to residential, though.

Regarding interest rates, CBRE has data out that says that the average time between the last rate increase and a significant drop in rates by the Fed is 7.4 months. We’ll see if that holds or not.

Travis,

Amazingly quick and significantly detailed analysis of another teaser that lacks full disclosure with sensational “prospects” but that misrepresents rather thoroughly. It was too good to be true, and while it may perform well, it won’t be as presented. Tax free at that high of a rate with cap gains going forward was the draw for me, and why not.

Thank you.

Impressive as always.