What’s that “The Big Long” pitch for a gold miner about?

by Travis Johnson, Stock Gumshoe | August 26, 2020 3:27 pm

Checking in on that "#1 Gold Mine that Nobody Knows About" teased by Nick Hodge's Wall Street Underground Profits

Here’s the headline of an ad that a few folks have been asking about recently…

“The man who made $4 BILLION shorting the housing market in 2008 goes all in on…

“THE BIG LONG

“This same legend just made an even bigger bet on the crash of 2020… only it’s NOT a short trade.

“Instead, he’s betting the house on a virtually unknown gold[1] miner.

“And my research shows it’s poised for a historic 10,000% surge… in the wake of a new gold bull market and coronavirus[2] economic fallout.”

The pitch is from Nick Hodge[3], in ads for his Wall Street Underground Profits[4] ($99/yr), and it’s an aggressive spiel about how his secret billionaire buddy, John Paulson[5], is piling into a gold miner:

“… he’s going all-in on a tiny gold miner that evidence shows could surge 10,000% as this mine gets permitted and comes online.

“And it doesn’t matter what the Dow does, or how long the coronavirus lasts and the fallout lingers.

“It doesn’t even matter the price of gold.

“Because this company is sitting on what I think will be the world’s biggest new gold mine.

“And NOBODY knows it.

“Nobody except for him, company insiders, me…

“And now you.”

This is, as many of you will already realize, yet another pitch for Midas Gold (MAX.TO, MDRPF), which Paulson & Co. has bankrolled for several years now. And this ad has been running for about six weeks, I first saw this version right before I went on vacation and included a quick note in my Friday File[6] as I headed out the door — so for those of you who aren’t Irregulars (for shame! Didn’t your parents teach you any better?), here’s what I wrote in mid-July:

“And finally, I just have to answer one final question that a few readers have sent in — yes, the new teaser pitch from Nick Hodge titled “The man who made $4 BILLION shorting the housing market in 2008 goes all in on… THE BIG LONG” is indeed just a mildly updated tease of Midas Gold, a stock he’s been touting for at least 2-1/2 years — I covered the original version of that same ad in January of 2018[7]. The John Paulson connection is not new, Paulson has been a major backer of this company for several years (though he did ante up more cash early in 2020).

“The latest news is that the USFS will be releasing the draft Environmental Impact Statement for public review in August, which is not a surprise (they announced earlier this year that the latest delay meant it would be released “in the third quarter,” and they still expect that environmental permitting process to be completed in 2021), but otherwise the story seems about the same as it was when I covered the stock for a pitch from Mark Skousen[8] back in May or, a little earlier, when Hodge’s colleague Gerardo Del Real[9] was pitching it as a “Tier 2 Gold” idea in March.[10]

“Midas is still a reasonable prospect[11], as such things go, with hopes for good permitting news and a solid feasibility study as soon as the end of the year, and like all miners if will look even better with rising gold prices… but there’s still meaningful risk since it’s still pretty early days, and permitting and development/construction can always surprise. Even with pretty fortunate and steady progress and a good feasibility study, none of which is guaranteed, it’s pretty unlikely we’ll see gold produced from a mine on this site before 2024. That’s the plight of all mine builders, the big costs and unpredictable delays come a long time before the payoff, but little companies with big potential mines can be big beneficiaries of rising gold prices… and soar if a real gold mania hits the markets.”

(I’m just kidding about the shame, by the way — we love our free readers too. Just not quite as much as we love the people who send us money).

Since then, the ad continues to circulate and there have been two items of note for Midas: The draft Environmental Impact Statement was finally released for comment by the U.S. Forest Service on August 14[12]… and then today, Paulson & Co. indicated that they will be exercising their convertible notes in Midas Gold[13], which the company says “simplifies the capital structure and demonstrates support for the Stibnite Gold Project.”

That conversion is bringing a paper windfall for Paulson, though they’ve indicated they’re not going to sell — the conversion prices averaged about 40 cents, and the shares are now in the C$1.70 neighborhood… and Paulson & Co. will now be a 44% shareholder (they already had board representation as critical partners). That will also dramatically increase the market cap for Midas, and give the company more flexibility to take on construction debt without worrying investors, and the increase in the market cap might by itself help to spur more interest in the shares and get them included in some indices. If the other convertible note holders also exercise their rights (they don’t have to right now, but they probably will at some point), there will be about 518 million shares outstanding, of which Paulson controls 209 million. As of this Paulson conversion, there are 475 million shares outstanding, so the market cap is now about C$820 million, which translates to about US$625 million.

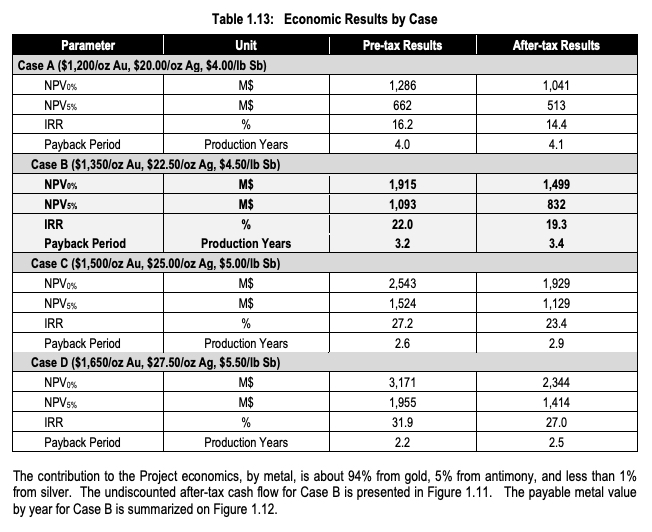

How much is the mine worth? Well, they updated the prefeasibility study in 2019[14], this is one of the valuation tables from that document:

"reveal" emails? If not,

just click here...

[15]

[15]

You can see that from the pre-feasibility study estimates, the investment still makes sense for those who can tolerate the variable return potential — at the highest gold price they model, $1,650/oz, the net present value at a 5% discount rate is $1.4 billion… which, if achieved, would bring a more-than-100% return from the current $625 million market cap (if that sounds like Greek to you, a discount rate is just a way to account for time — since your money is sitting there idly waiting for the mine to be built and produce something, while if used elsewhere it could generate a return instead… 5% a year is the number they use to represent that opportunity cost, with the general idea being that money in five years should be worth less than money today).

Still, there are a lot of variables — yes, $1,650 an ounce is 15-20% below current prices for gold, so we might add another $500 million in value if gold stays at these prices, or far more than that if gold shoots substantially higher… but if the performance of the mine is 20% worse than expected (lower volume, or slower rampup of production, neither of which is unheard of), and the gold price falls to $1,200, then the mine might be worth as little as about $300 million using similar calculations, a drop of roughly 50% in value. Any drop worse than that might even be enough to delay the project further, since they’ll have to borrow a chunk of money and perhaps also sell some more equity to actually build the mine (which will cost roughly a billion dollars).

Gold has seen both $900 and $2000 in the past five years, so I’d hesitate to be certain about exactly what the gold price will do in the four or five years before this mine is producing (assuming permitting and construction go very well), but it’s still at least a decent setup. Lower reward than a lot of mining projects that are at similar stages of development, since this one has gotten so much attention from speculators and has that Paulson imprimatur that help to elevate the share price during good times for gold, but probably lower risk as well.

And, of course, any evaluation that’s based on numbers is making the assumption that the permitting process will go well, and that they’ll get permission to build this mine. The big argument in favor there is that they’ve got a lot of influential local people on board, and that building this mine is designed to actually help clean up the environmental devastation that was wrought by decades-ago mining at this same site. That’s fairly compelling to me, but you can never be 100% certain what will happen in a permitting process — just look at Northern Dynasty (NAK) and its Pebble Project in Alaska, which is in an environmentally sensitive area but began to be seen as a “shoo in” following the Trump election victory and some permitting progress in 2016 and 2017… but then got slowed down by regulators again, lost another partner, and is now being criticized by Donald Trump[16], Jr., bringing yet another setback in their decades-long fight over this project. That’s admittedly an extreme example of a permitting fight, I don’t think anyone expects a showdown like that over Midas’ Stibnite project in Idaho, but it’s important not to be too optimistic about outcomes with any permitting process.

We’ll probably know some more once the comment period is complete for the Stibnite Project, which will be in mid-October — that’s the big opportunity for local or environmentalist opponents of the project to really get some attention, so I’d guess that Midas management is crossing their fingers that the days pass quickly until then, with no surprises. Final word will be much longer in coming, though — the actual final Environmental Impact Statement and the Record of Decision that lets Midas move forward, assuming things progress nicely, won’t come until sometime next year. The latest Midas Investor Presentation[17] continues to indicate that they see 2021 as their decision year, so they’ll probably also have to raise construction funding at some point, and maybe even raise some more equity funding (and presumably will completely a final feasibility study before that, which will give new numbers for the project), and then they still see a ~3 year project to do their site restoration (of that old mining project) and build the new mine, so 2025 or so is probably the earliest date you might foresee for gold production.

And that’s all I’ve got for you on this “Big Long” and the prospects for Midas — we’ve covered this one many times over the years, and I don’t think I’ve ever owned it personally but I’m sure a lot of readers have invested in this one… so if you’ve been following the story or have anything to add, or a different favorite little gold miner to recommend, I’m sure your fellow investors would appreciate hearing your thoughts. Just use the friendly little comment box below.

P.S. As always, readers want to hear what actual subscribers to newsletters think — so if you’ve ever tried out Wall Street’s Underground Profits, please click here[18] to share your experience with your fellow investors. Thanks!

- gold: https://www.stockgumshoe.com/tag/gold/

- coronavirus: https://www.stockgumshoe.com/tag/coronavirus/

- Nick Hodge: https://www.stockgumshoe.com/tag/nick-hodge/

- Underground Profits: https://www.stockgumshoe.com/tag/underground-profits/

- John Paulson: https://www.stockgumshoe.com/tag/john-paulson/

- Friday File: https://www.stockgumshoe.com/tag/friday-file/

- I covered the original version of that same ad in January of 2018: https://www.stockgumshoe.com/reviews/underground-profits/hodges-nobody-knows-about-americas-biggest-gold-discovery-pick/

- I covered the stock for a pitch from Mark Skousen: https://www.stockgumshoe.com/reviews/forecasts-and-strategies/skousens-under-a-buck-potential-10-bagger-in-gold/

- Gerardo Del Real: https://www.stockgumshoe.com/tag/gerardo-del-real/

- pitching it as a “Tier 2 Gold” idea in March.: https://www.stockgumshoe.com/reviews/resource-stock-digest-premium/whats-this-final-chance-to-buy-1600-tier-2-gold-for-8-10-per-ounce/

- prospect: https://www.stockgumshoe.com/tag/prospect/

- draft Environmental Impact Statement was finally released for comment by the U.S. Forest Service on August 14: https://www.midasgoldcorp.com/investors/news/2020/regulators-release-draft-environmental-impact-statement-on-stibnite-gold-project/

- today, Paulson & Co. indicated that they will be exercising their convertible notes in Midas Gold: https://www.midasgoldcorp.com/investors/news/2020/paulson-co-provides-notice-of-intention-to-exercise-convertible-notes-in-midas-gold/

- updated the prefeasibility study in 2019: https://www.midasgoldcorp.com/site/assets/files/2119/amended_techreport.pdf

- [Image]: https://www.stockgumshoe.com/wp-content/uploads/2020/08/midaspfs.jpg

- Donald Trump: https://www.stockgumshoe.com/tag/donald-trump/

- latest Midas Investor Presentation: https://www.midasgoldcorp.com/site/assets/files/2399/2020-08-18_midas_gold_presentation_short-final.pdf

- Wall Street’s Underground Profits, please click here: https://www.stockgumshoe.com/reviews/underground-profits/

Source URL: https://www.stockgumshoe.com/reviews/underground-profits/whats-that-the-big-long-pitch-for-a-gold-miner-about/

Permitting in Idaho is probably better than most places, but with everybody from California moving there who knows if/when that could change. This is a big mine and if gold prices stay high then great. But the duration risk is large, even with the big money lending credence. I’m betting there are better entries than here, for me.

Forget Midas…….Follow the big boys (Rule & Casey)…….get into Goldmining (GLDLF) asap…….

GoldMining, which has recently tried to jump on the royalty bandwagon as well, is a pile of hope and sentiment that’s been just waiting for a spark from higher gold prices — I speculated on it back in the 2015-2016 run, when gold last surged, and they are great at selling the potential, but I would not be all that confident about their ability to actually develop anything. I don’t have a position on that one personally, and haven’t looked at the recent filings, but I’d urge folks to remember to take some profits along the way on names like GOLD.TO — they’ve been good at building a story that becomes appealing when gold goes up, but not so good at actually doing anything that creates value with their assets.

OK, maybe I’m just a little too cynical after watching Amir Adnani build this name over the past decade. Now that I’ve said all that, it will probably surge to $20 🙂

i’m hoping it goes even above $20!! their proven gold is worth quite a lot not to mention the inferred. I personally like the idea of the royalty aspect as well especially since they have quite a few different mine sites. time will tell i guess….it always does.

thanks for your brilliant $0.02 worth. (it is actually worth more but that’s the saying…dont think that cliche has adjusted for inflation!!)

Travis, agreed GOLD.TO for the same reasons. I have $ 100k in that stock and of course it isn’t going to the moon, but pays regular dividends and will likely double as /when American helicopter money ignites REAL inflation.

I’m in on Midas… I hope all goes well! We will see.

Unless you are very knowledgeable about mining, stay away from the small miners, most of whom are not mining but exploring. Iff you are interested in them , listen to Eric Sprott on YouTube Friday mornings. He tells you what he’s buying and why. No charge, either. Two other items. Never listen to what politicians have to say about mining or anything else. The don’t produce any thing and never have. A related point. NAK holds one of the largest Cu/Au gold deposits in the world. It will be developed. Perhaps after the U.S. ceases to exist.

Could be, but, as you know, “will be developed someday” doesn’t necessarily do much for investors. Since they announced the most exciting part of the discovery at Pebble, starting to claim huge discovery numbers in the Fall of 2007 (like 40 million ounces of gold), the shares of Northern Dynasty have lost 93% of their value.

That stock has been teased and promoted by a number of newsletters over the past dozen years, since the project is just so potentially massive, and I even traded it myself a few years ago, but I think it’s at best a coin flip whether anything is built there in my lifetime (I’m 50). And, of course, building a mine there would take close to a decade and a bazillion dollars, maybe two bazillion if they have to build a Hoover Dam to keep their cyanide from killing all the salmon 🙂

Travis, have a read of two companies that are beyond field trial-stage in biologically nullify ing mining tailings in both the areas of arsenic & cyanide separator use: Enviroleach Technologies (cyanide) and BAC Environmental (arsenic), both of which are exciting remedial and waters mitigation technologies that WILL become a staple technology within the mining sector in years to come.

Also, as a corollary to my last comment missive, over-population is the real enemy of mining advancements. Many Americans want more National Parks and spared public lands. Alaska traditionally, for example, has Ben called “America’s Last Frontier”.

Well said Carl

Travis: How can you ignore Junior gold miners like Midas. Nancy P is spending trillions of $$$. Price of gold is now going skyward. Chase says its going to $$3000. Others say silver is a better investment and it already has almost doubled. You can go to the websites. I picked a handful of Junior gold miners mostly those where Eric Sprott owns a chunk of.. In 3 months I am close to doubling, most still under a few bucks, others still under a buck. There is a deficiency of silver in the world this year.

I don’t ignore them, but I don’t often buy them either. I do occasionally speculate on small miners, but as of now more than 10% of my portfolio is in either gold or gold/mining related equities (mostly physical gold and shares of royalty companies), and I don’t feel compelled to go dramatically above that.

You are wise to take your investment investigations to Robert (Friedland), Keith (Neumeier) Eric, Rick, Doug & Nick’s crowd, not forgetting McKewen. Easier to parallel those guys. But if you are obsessed with geology & precious metals mining, then of course, you can invest thousands of hours studying thousands of exploration & development projects. In Travis’ defence, however, he is correct to laud proven success as opposed to promising speculations. As he pointed out above, and as I have too, investing in & on American soil is far different than say Canada, Chile, Australia. Notably, many mining champions hang around Vancouver & Toronto, where most mining symposiums also occur. So naturally, you are wise to attend those conferences or follow those who do.

Dear my friend

In which junior silver and gold prospectors Eric Sprott owns large stakes and is under a dollar. That my pension went with the subscription and recommendations of “Merchant № 1 of America” Tom Gentile / merchant № 1 of ballots and not of winning recommendations / and I can not buy more expensive

BGMilitaryUnion@gmail.com

Travis, thank you for saving me the last dollars of your pension thanks to your extremely useful research.

John Paulson is the Largest Stockholder currently with an investment of close to $4 Billion Dollars now. He has extensive experience investing in the Mining Industry! Also, the Stibnite Mine has the Only significant amount of Antimony in North America. China currently supplies our U.S. Military the majority of this Rare Earth mineral and Midas has a projected quantity of close to (20)Million Oz. of Gold at the Idaho location. Barrick Gold recently invested $4 Million into this project as an investment! Midas shares (MDRPF) currently sell at $1.37 per share. And, Yes, I recently bought several Thousand Shares.

Not sure where that $4 billion number comes from. Paulson’s firm manages about $8 billion overall, but the total value of their Midas investment now (which has been very profitable so far, Paulson first financed them with a convertible bond purchase back in 2016) is about $200 million recently.

In 2019 I purchased Midas Stokes at $0.42 and sold half when it doubled. I recovered my Investment . Today price is $1.30. I bought it after reading about it here. Thank you Travis.

I also bought then, upon reading it here. Thanks, Travis

contractorr- hang on to the other half of (MDRPF); because, Midas will be making several BIG announcements concerning the Antimony on their 1500 acres in Idaho and the U.S. Pentagon.

This scarce mineral is absolutely critical to the weapons currently being used to defend the USA, and China currently has a choke hold ( 80%) on the World Wide production of this rare earth mineral.

Hi all! As usual, splendid commentary Travis! For quite awhile — year’s in fact —- I read Nick’s Midas promotion. His hints are easily dissected, so in a few google search minutes I worked out this behemoth gold prospect sandwiched in the Idaho woods. Eventually I did put $ 2k into this one. Nick & Gerardo’s PUMP has had dramatic results since gold price onset. I agree with you of the uncertainties that environmental opposition routinely imposes to bedraggled gold development mining projects. In the context of Idaho, however, the Idaho state politics are slanted more towards traditional conservatism. This should result differently than say Northern Dynasty’s Pebble project, not forgetting that environmental extremism finds listeners there in Alaska with the sockeye fisheries.

I have probably $200,000 in Northern Dynasty shares & frequently am in dialogue with senior management there in BC. In general, Pebble has become THE flagship whipping boy prospect for environmentalists. Over a $ billion has been spent attempting to bring Pebble into production through the US permit gauntlet. In general, compared to say China, where deposits are identified & single-tracked into production, Northern Dynasty, in the American context, is finding that American mining is growing more arduous. Americans don’t like mines, unless, of course, they lie in some obscure desert landscape!

The overall problem facing investors in American-based mines, other than say Nevada, increasingly the American people have been relying on natural resource extraction overseas. As we know, most persons don’t want a mine in their back garden.

Since the realisation of Chinese controls of vital elements by the Trump administration, and the ensuing December 2017 Critical Elements Index Congressional ratification, at least American leadership has awakened to the resource vulnerability that extra-US resource acquisition bates (recollecting the oil shortages imposed by OPEC in ‘73 & ‘79). But still, the American people do not seem to realise that the overall lack of critical thinking in the electorate, coupled with syndicated media often leads to cult-like followings & ideologies composed of & by persons who often lack the intellectual grasp of contemporary science & technology. Northern Dynasty’s Pebble project is showing the international investment community just how increasingly uncertain & high political risk the USA is today… and moreover, will be. As it is, over some 70% of mining companies are lodged in Canada —- not the US, as there are various reasons and factors that are driving mining out of the US. In one word: “disincentives”!

So yes, your caveats to investors in Midas are well-founded, in general, while anything outside Nevada deserts, which don’t feature in “Outside Magazine”, are vulnerable to opposition by the American populace — of which more than 75% hold residence in urban America.

The overall debates & delays to US-based permits — and extraordinary costs — are placing the US increasingly behind their Chinese competitor. Antimony , copper, molybdenum, Rhenium — all of which feature in tge Midas & Pebble deposit inventories — in China, would be fast-tracked into extraction & employment, as they are vital towards placing China in the lead in such areas as aerospace, electrical vehicles, battery technologies, computers, phones, etc. — so in the context of the United States of America, mining isn’t seen as a priority to the average citizen, when in fact, historically, resources have always been key to any nation’s wealth & dominance.

Somehow, one senses here outside the US, that the Citizens of the US are not any longer a “collective”, United in anything, but single-most themselves. The notion of “community”, of “neighbours”, of “charity” are lost in the fabric of diminishing functional communities and cities. This is stifling the aggregate growth potential of the US, with the mining -resource extraction sector as its engine. I see the debates in newsletters & financial advisories and in forums engendered by mining analysts. Investors are seeking profits and debates are primarily over this. Those who aren’t business-minded are the opponents of anything that traditionally has been seen as “progress”. There is no “collective reasoning” — only warfare! Lawsuits are the staple mechanism of resolving American conflicts and increasingly are going to unravel its future.

American leadership woes, if the US is still to be viewed as a credible “representative democracy”, will continue to persist. The “Me” generations have come to the fore. The United States of America is virtually no more.

Travis, you are a profoundly thorough investigator & writer, so again compliments. In the greater picture, however, the American Civil War is real and very actively defining lines in the sand… or in many cases “the rock”!

Well said Fred, A most intelligent and reasoned response to our “Un”United States of America. The ungirdled greed and Political bullshit of our leadership and destruction of family values is a future sign of where this nation is headed. Gold will prevail in the end , paper toilet money will be part of history. IMO .

Well, Fred, part of your 200k is being continuously spent on filling my Alaska mailbox with junk mail.

Thanks a lot!

“But still, the American people do not seem to realise that the overall lack of critical thinking in the electorate, coupled with syndicated media often leads to cult-like followings & ideologies composed of & by persons who often lack the intellectual grasp of contemporary science & technology.”

So smoothly said. 🙂

Outstanding explanation of the Midas delays that have halted progress thus far at this mine for nearly 5 years as of 2020 ! That said, current mining site completion plans are being reviewed at the EPA and the Idaho state legislature is backing this project .

GLDLF & MDRPF Travis? Neither are royalty stocks, your favorite Travis! With gold breaking out this year, WHERE;S THE BEEF??? Yep, I’m really surprised. Sue me!

I don’t own either of those, personally.

I recommend Hecla mining. I bought it for $4.00 four months ago -today it sells for @5.77.I’ve traded it of f and on for several years and have not been disappointed. As with any(almost) gold stock, when the gold market goes south ,run away!!

So far so good

midas gold up 82.6%

sandstorm up 33.23%

silver elephant up 34.25%

ishares silver up 21%

drd gold up 50%

i hope they keep on shinning (pun intended)

i recently bought barrick gold just to follow Warren’s move 🙂

be safe you all

Doesn’t Barrick have a stake in Midas too?

Midas has a good project..4.57Moz/0.047g/t , but there are other projects that might warrant a close look…eg Vista Gold(VGZ) Mt Todd project in Australia..5.85Moz/0.82g/t. is flying under the radar..!!

Could someone please point me to a platform that offers this stock? Etoro and Trading 212 don’t have it. Thanks!

Re VGZ: Interactive Brokers, USD1.21 a few minutes ago

TDAmeritrade

I bought 1,000 shares of MDRPF in July of 2019 at approximately $.54 per share and still own it. I believe that I bought it after reading what you wrote about it, but I still remember how you said that it would be years before the actual mine was built, so I was real hesitant about making the purchase. I’m glad that I bought it, but I wouldn’t have bought it if you hadn’t written about it because I don’t trust most of what Nick Hodges writes. He’s great at hyping things, but I trust your objective analysis. Thanks.

Oh, one more thing. I was watching one of those online presentations by a small gold miner a month or so ago, and something very interesting occurred near the end of the question and answer session after the presentation. Earlier in the presentation, the CEO of the small gold miner had mentioned how their land package bordered the land owned by a company operating a very profitable, well-run gold mine. The listener’s question was something like, “Okay, that’s all well and good, but I see that Spearmint Resources just bought a large adjacent land package, too. What do you think about that?” And the CEO’s response was something like, “No comment.”

That really intrigued me. I had never even heard of Spearmint Resources, Inc. (SPMTF), but I got the distinct impression that the CEO didn’t want to talk about them because he might have to admit that their story was more compelling than his own. He acted swiftly to defuse the situation, hoping that the listeners weren’t really paying too much attention.

I checked on Spearmint and bought 1,000 shares at $.0315 per share. This company is the moon shot of all small mining explorers. They have land packages for cobalt, and platinum and palladium, and lithium, and … You get the picture. They don’t just focus on one area of expertise. They focus on EVERYTHING! If I didn’t know any better, I would think this is just a shell company for some Pump and Dump outfit. But that’s why I only spent a grand total of $31.50 for my teeny tiny slice of the company.

I also watch Spearmint. When small, to diversify is expensive. You may have seen Albert Matter, CEO of NuLegacy. He has linked up with Metalla Royalty to get his company, next door to Barrick in digging around and under an anticline that likely will jettison something VERY promising —- if you are an exploration buff and lotto ticket buyer. Quinton Hennigh (google him to be impressed!) is now one of the directors, and has great ideas in his various consultancies — ideas, that lie outside the box of PhD precious metals geologists. Have a look at Lion One, Thinderstruck (Fiji), Novo Gold (Western Australia), Irving Resources, even in Hokkaido, Japan. If you are wanting to learn more about epithermal geology or what makes porphyry, follow Quinton. There are dozens of others. But he is more self-promotional (being American) than the average smart geo.

Oh, and by the way, Spearmint is best poised to get on-board with the hype that will likely surround a renewed Lithium price hike in 2022-23. The Clayton Valley stuff is grand! All one needs is heat & faults to make this ancient salt beds viable —- and investor support too!

I did a quick read of the comments but not seen anything about Tribal lands. I bought Midas Gold around $.54 and after holding it for over a year and reading the News I got the feeling the Indians were not going to let it happen. I think a good portion of the project is on Tribal Lands.

Don’t know anything about that, I’m afraid, but thanks for the heads-up.

Indians give approval before the Miner gets on board. They usually get a payment or royalty.

LOL, Indians. I’m an “Indian”. Yes our people receive pre-payments, payments, interest payments, and royalties on Gold & Oil “black gold” and other resources: land sales & land leases. In the beginning the original intent (purpose) of treaties were: for settlers to pass through territories with the permission of leaders in those territories, and for a 60/40 split of resources (60% settlers & 40% indians) with settlers getting (or keeping 10% of our 50/50 cut as expense to develop those resources). Thus… whether these payment/ royalty formulas do in fact equate to 60/40, I don’t know, I’ve never done the math on any. So, the treaty “passage” is the “permitting” process: consultation & approval — then follows development, construction, sales, marketing, supply & demand etc.

Well said, Jean!

When my fellow “White” grumps about “The Indians” blocking him from whatever he wants to take from the land next — I often suggest he use the word “Landowners” instead. That’s somehow a little easier for white guys to understand.

Has anybody else noticed the divergence of the S&P from the VIX ? Simular to 2007/2008 ?

Thanks Travis for your articles. I am really new on this and I am really enjoying every single piece you are posting. I am quite skeptical investing on this small mining companies were I do not have enough data or track and the only thing I see is hope. I was contacted last May by an investing company to buy shares of a Chinese company based on Hong-Kong. I did not invest and the company has almost doubled since then. The financial data indicates that they have even positive EVITdA. The company is Zijin Mining Group with a market value above 3,5B. Are you tracking this company? Anything I am missing?

any thoughts about Kirkland Lake gold?

Gold bug starting to heat up with minerals in bulk market, for multiple reasons. Lot of potential stocks.

I like TRQ, which I have a large stake.

Gold production for 2021 est. at half a million oz. , Copper output 140- 200,000 tons. Surface mining.

Completion of underground mine 2022-23.

These mines take 8-10 years to develop.

So in other words this is a Long Long