Jason Williams is out with another “power for data centers” teaser pitch, but this one focuses on a little company we haven’t looked at in years… so let’s dig in, ID the stock for you, and explain what he’s talking about.

The ad is for his Future Giants ($1,999/yr, 90-day refund period) newsletter, which is one of his “upgrade” services (most newsletter publishers use the $50-100 subscriptions to get people in the door, but make most of their actual money with the upgrades to $1,000+ letters… though over the years, we seen no real outperformance by pricier letters, which tend to recommend smaller and riskier investments).

Here’s the intro to the pitch, the basic gist is that President Trump and other leaders are pushing the hyperscalers to pick up more of the cost of new power generation, so that utility bills don’t spike higher for regular folks (ie, voters):

“President Trump, 13 state governors, and some of the most powerful energy executives in the country just forced a $15 billion bill on America’s biggest tech companies.

“Google, Meta, Microsoft, Amazon, OpenAI…

“These companies have been devouring America’s electricity to build their AI empires…

“Driving the energy bills of everyday Americans as much as 267% higher in the process.

“But now they’re being told to pick up the tab…

“Trade adviser to the president, Peter Navarro, didn’t mince words, saying: ‘These data center builders… need to pay for all — all— of the costs.'”

That’s from the meeting in March, where President Trump brought the biggest hyperscalers to the While House and had them sign the “Ratepayer Protection Pledge,” which essentially means they promise to cover the cost of their rising electricity demands by buying or bringing separate generation for the project. That didn’t have a firm October 1 deadline, and the hyperscalers are not responsible for all of the new data centers or the increased electricity demands (more like half, at the moment), it was more of a squishy PR pledge made at the White House (as President Trump noted last Fall, when saying AI electricity demand had a PR problem)…

… so we should take the “$15 billion arrives on October 1” bit with a big ol’ grain of salt… but there are some rule changes within the grids that will effectively drive hyperscalers to keep buying more off-grid power and/or absorbing higher grid costs. And many new data centers have been trying to do that anyway, as connections to the grid are facing longer and longer waiting periods or are just unavailable or unpredictable because there isn’t enough power generation.

And we get a good sum-up of the story about this company on the order form:

“… this mandate has created a $15 billion opportunity with a hard October 1 deadline.

“This money has to go somewhere…

“And thanks to Nvidia’s secret blueprint, it’s going to end up in the hands of our tiny PowerScaler.

“Why? Because it’s the only company with the technology to power Nvidia’s next-generation AI chips.”

Again, don’t get too carried away with the “hard deadline.” But Williams says that this company has huge opportunities to participate in the behind-the-meter generation needs of data centers — essentially the same story as every other “dark energy” pitch, with “dark” meaning that data centers have been unable to connect to the grid, because of limited power availability or long wait times, so because they’re “dark,” they have chosen to build their own power-generation on site.

That “dark energy” generally takes the form of natural gas turbines (like those made by GE Vernova and Siemens) or gas fuel cells (Bloom Energy), but apparently this penny stock Williams is pitching is an option, too… back to the ad…

“You’ve heard of hyperscalers — the Google’s, Microsoft’s, and Amazon’s of the world, who’ve built the most powerful AI infrastructure on the planet…

“But there’s a new category of company that hyperscalers simply cannot function without…

“I call them ‘PowerScalers’ ….

“Without PowerScalers, every single data center being built across America right now is just an extraordinarily expensive building that can’t turn on.

“At the center of this new category sits one tiny stock that almost nobody has heard of…

“Right now you could pick up a fistful of shares for less than $100 — but this won’t last.

“Because when $15 billion worth of contracts start flowing through this sector…

“And the market finally connects the dots…

“A stock like this doesn’t stay priced in pennies for long.”

The order form also highlights some of the “demand signals” this company is receiving:

“The CEO has confirmed demand “magnitudes” above anything the company has seen before…

“A major hyperscaler has asked the company to set up a dedicated manufacturing operation on its campus — for the next five years…

“Multiple power purchase agreements are in active discussion simultaneously…”

The most interesting part of the tease is the NVIDIA connection, with Williams asserting that NVIDIA’s latest rack designs will directly drive demand for this specific company’s power generation equipment… here’s how he puts it:

“Nvidia’s secret blueprint has already crowned this microcap the king of the PowerScalers (and made everyone else obsolete).

“Nvidia published a technical document that almost nobody outside of a handful of engineers ever read.

“Buried inside it was a single requirement that instantly turned the tiny, obscure PowerScaler I’m about to reveal…

“Into the most mission-critical company in the sector.”

What’s that new NVIDIA design? Essentially, to build racks that use direct current (DC) instead of alternating current (AC), to make the movement of power to that rack far more efficient… here’s how he puts it:

“… there are two types of electric currents — alternating (or “AC”), which we discussed earlier, is the predominant source of power coming out of every power plant and plug socket…

“And there’s also direct current (or “DC”).

“DC can carry far more power through the same cable…

“So in theory, this should mean that as AI racks get bigger and more powerful, you just switch to DC and the problem disappears…

“Instead of adding more and more copper until the building buckles.

“In fact, that’s what Nvidia has just mandated — specifically, 800-volt direct current.”

And we’re told that the revenue growth from the deals they’re making isn’t hitting yet, but that the stock might take off once they do. And the ad notes a big chunk of insider buying at about $2 a share…

“If you need more proof that now is the perfect time to start taking a position, then you should know that this is exactly what insiders are aggressively doing right now. They’re buying tens of thousands of shares — on top of what they already own”

That leads to a little blurred out image of the “insider trades” being made in the stock… which helps us to confirm that yes, this is Capstone Energy+ (trades on the OTCQX at CGEH), formerly known as Capstone Turbine and then Capstone Green Energy (the latest name change was just last month)… they went through bankruptcy in late 2023, filing for creditor protection in September of that year because of a big loan from Goldman Sachs they couldn’t service (after almost twenty years of trying to build this business, but never making a profit), but it was pretty quick, with Goldman Sachs mostly just taking equity, and they emerging from bankruptcy protection by December of 2023. They really came back to life in January of 2025, and they are still burdened with a good chunk of debt, but they did just do a major refinancing last last year to reset the business, and raised a bunch of convertible debt last month, and their financial results are close to break-even now.

And yes, they have boomed quickly out of “penny stock” range, with the share price moving from $2 late last year, when they did some equity financing and also saw that insider buying, to about $10 now.

Perhaps more importantly, it looks like they have maybe gotten their act together at what might be a pretty good time, with now a couple quarters of pretty meaningful improvement in gross margins and some top-line growth that indicate that maybe their era of mismanagement is starting to fade, and the opportunity to capitalize on the “data centers need power” story.

That is, at least, the narrative… we’ll see if they can book those larger deals and operate profitably as this year chugs along, but some success is already reflected in the stock price now, even though it’s still a very small company, with a market cap of about $300 million.

And to be clear, data centers are nowhere near being the core of their business right now — but there is hope that will change, and data centers definitely represent the most dramatic growth market for them. The move to use more DC power, and simplify power systems in data centers, might create an opening for using Capstone’s microturbines to supply 800V direct power to NVIDIA racks, which is a big part of Williams’ argument… even if we’re not really talking about a company that can quickly provide power for megawatt-scale data centers right now. Here’s an excerpt from a local newspaper article back in January of 2024, about their emergence from bankruptcy:

“The Van Nuys-based microturbine manufacturer emerged from bankruptcy on Dec. 7, kicking off a restructuring to streamline its procurement and sales operations, keep up to date with nascent technology and cater to a global market in greater need of energy solutions than ever….

“Capstone, which was founded in 1988, offers a range of microturbine units designed to use a variety of fuel sources and run as either a stopgap measure or around the clock. Its units use thermal energy fuels such as natural gas, biogas, landfill gas, hydrogen and propane, which emit substantially less carbon than the typical diesel-powered generator.

“Since selling its first commercial unit in 1998, Capstone said it has shipped more than 10,000 units to 83 countries. The company also claimed its units have helped customers – typically remote industrial sites such as oil and gas platforms, landfills, agricultural operations, wastewater treatment plants and electric vehicle charging stations – save nearly $1.1 billion in energy costs and reduce emissions by 1.9 million tons of carbon in the last five years. The company typically charges about $1,250 per kilowatt; as an example, the smallest system, which produces 65 kilowatts of electricity, is priced at approximately $81,250.

“That said, sales historically have not been enough to prop up its operations, and while the onset of the Covid-19 pandemic certainly did not help, (Interim CEO Bob) Flexon hesitated to place much blame there.”

And yes, the image they show in the presentation is of the controller for one of Capstone’s microturbines, the C1000 (which is their biggest turbine installation, consisting of five 200KW microturbines in a box, for a total of 1MW — so, a good size for backup power for a smallish hospital, or for an edge data center, but it might be challenging and expensive to pack in enough of them to run direct or backup power for a 100MW hyperscaler data center).

Their core microturbine product has been pretty well-accepted for a long time, their basic story is that they offer up a more expensive microturbine with low emissions, and have long sold those for use in remote facilities or as essentially smallish generators that are fueled by landfill gas or flare gas… but also say that because of their design, which runs on an air cushion instead of using conventional lubricants or liquids, their turbines have lower maintenance and repair costs over time. From what I can tell, their actual products are successful and pretty well-accepted, but the company has nonetheless been a financial disaster for decades. Not sure why, whether that’s just because they’ve been sub-scale, or can’t compete on price, or poorly managed in one way or another.

The company has been a regular presenter at the LD Micro investing conference for more than a decade, and that conference has been the source of a huge number of over-hyped and over-promoted small cap stocks (and inspiration for a lot of penny stock newsletters), so that always makes me a little cautious… but every once in a while, an overhyped penny stock meets the right market environment and really does emerge as a strong growth company, so never say never. That latest presentation at the conference was just a few weeks ago.

Here’s a little part of what they said at LD Micro, emphasizing the move to DC power:

“I’d like to start out with an announcement that’s a pretty powerful announcement that we’d like to make, and that is the battle between Edison and Tesla is shifting. If we think back over 100 years when Edison believed that DC power in distributed generation form should win out over transmission of large-scale megawatts, we never would have thought we’d be here today. That truly is what’s happening as we look out….

“Let me spend a little bit of time on data centers ’cause I know that’s what a lot of people like to talk about. You know, we got to the dance late. We only started approaching the data center market about 1.5 year ago. But what we did, we brought in some experts from that data center space, who truly understood how the data center electrical topology works. Then we created a reference design that we call Energy Surplus Program. The whole idea there is that we’re using our microturbines to generate power on-site, but we’re recovering that waste heat, and we make chilled water that data centers need to cool all the servers and the GPUs. We make that chilled water at 1/10 the energy cost of an electric chiller that’s on today’s data centers.

“As we lower their electrical demand, we’re actually generating power, therefore, we create this energy surplus. That’s our approach with data centers, and we do this in 3 MW- 4 MW blocks that matches up with their IT load. We do this as an engineered equipment package to make it as simple and straightforward for those data center customers. We’ve got a number of opportunities in the pipeline, and it’s keeping us quite busy. Did wanna touch a little bit on the major shift when NVIDIA last year announced the 800-volt DC, and everybody started to scramble, “What does this mean?” Well, for Capstone, we were already doing that natively. We were actually generating 760-volt DC.

“With some software modifications and a couple of hardware modifications, we now have our prototype test unit with our Smart Power Switch that’s been operating at our factory for months now, and we’ll be ready for a real pilot by September. We’re pretty excited with where 800-volt DC is going to go. It’s not going to be tomorrow, but we’re going to be ready for it when the rest of the world is ready in the new data center designs. Believe me, this will be powerful and huge because the amount of copper savings and the amount of energy savings that going direct current does for a data center will be a big deal. So that’s why I say I think in this case, Edison was right and Tesla was wrong.”

And a few of the comments they made on their last earnings call jibed pretty well with what Jason Williams is pitching as their data center opportunity.

On capacity and the supply chain readiness, since so many deals are not necessarily just for power, but are for power RIGHT NOW:

“The data centers could be a huge opportunity. And some of these orders or some of the deals that are in the pipeline are very large MW-type projects. So the team’s been working on a new floor layout under lean manufacturing. We’ve talked about that, and we’re almost done. And when we’re done with that, we should be able to have 7MW on the floor at any given time. And since it only takes us about a week to build a C1000, if you’ve got 7MW in one shift per week, you multiply that by 50 weeks, you’re at 350 MW.

“And then if you go to two shifts, you’re at 700 MW. So you can do the math. But with that also comes the logistics and the challenges in the supply chain. And actually, we just recently had a dry run session with some of our key suppliers to basically say, ‘Okay, if we get this 100MW order, what does this look like, and how fast can we ramp up?’ So now the team is looking at all of those choke points, and we’re working on solutions to those so that we’re ready when that day comes, because we’re feeling pretty excited by it.”

What’s the story with that “major hyperscaler” hinted at by Williams? Here’s what they said in response to a question about capacity on their last earnings call:

“Q: What is your current potential annual capacity in MW, considering supply chain limitations, skilled labor availability, maximum output of your existing manufacturing lines, and any other relevant constraints? Additionally, how do you anticipate this annual maximum capacity evolving into the future?

“CEO Vince Canino: Well, I think I answered some of this in an earlier question in terms of what our capacity is and some of the conversations we’re having with our supply chain. On the labor side, you know, it’s not hard to get to a second shift. A third shift always tends to be the difficult one. And so that’s what our VP of Operations, John Toor, is working on. But here’s the beauty of the way we do things. You know, at this point, what we can set up is what we call a final assembly and final test facility. So, you know, we do balance our rotor groups here and build our engines, and we test those, as well as our electronics, but we can feed multiple facilities.

“So we’re in talks with a customer who wants a mobile manufacturing facility, because they’ve got a five-year build-out for their data center. So we can do that, and that’s the beauty of the technology that we have and, and the way we’re set up versus some of our competition. So we’re not worried about running out of capacity here because we, we feel like we’ve got the flexibility to find a very simple warehouse-type space. We don’t need cranes or any special equipment, just some, you know, some air skates and some test equipment and gas lines.”

So sure, I guess they might build a satellite manufacturing facility on site at a hyperscaler campus, but I haven’t seen anything more detailed than that to confirm an actual contract or a facility being built.

And on the data center pipeline and the “magnitudes” of interest from the hyperscalers, which remains a good story but doesn’t seem to really be in the financials yet:

“And one of the things we’re doing is we’re keeping two separate pipelines, the what we call the C&I pipeline, and that’s your commercial and industrial pipeline, the traditional, distributed generation business. And we’re watching that pipeline grow. But as I mentioned earlier… you know, these deals, as they get bigger, they take a little bit longer, and especially when you’re dealing with some government agencies.

“In terms of the data center pipeline, you know, it’s magnitudes, magnitudes above what the C&I pipeline is. And that’s to be expected because these deals are so much bigger. And we’re just, you know, we’re working through it. It continues to grow, but the team is getting really good in qualifying and making sure they’re not chasing everything.

“So, you know, is the project funded? Does it have end users signed up? They’re asking all the right questions to make sure that we have a really solid and robust data center pipeline.

“Q: Do you think in the coming few quarters, we’ll see our first data center orders?

“CEO Vince Canino: Well, I sure hope so…. there’s some good deals out there. But the crazy thing about the data center space is that right, especially right now, where the currency for data centers is time to power. And so we’re getting phone calls all the time, “Oh, we’re short. Somebody wasn’t able to deliver.” And we want to be able to capitalize on those. Now, some of those might be, you know, four, five, 10 MW, and we’ll take them. But there’s certainly some other deals out there, too.”

So… does that lead to riches? It’s all still pretty hypothetical, but they are trying to address this larger data center market and build bigger installations for them (3-4MW, so more comparable to a diesel generator), and it seems likely that they will get some orders. Rising orders at a time when they’ve started to fix their long-lingering problems with excess inventory and inefficiency and low gross margins could certainly be a nice recipe for a recovery… even if it might also be a bit difficult to trust the ambition after so many decades of poor performance.

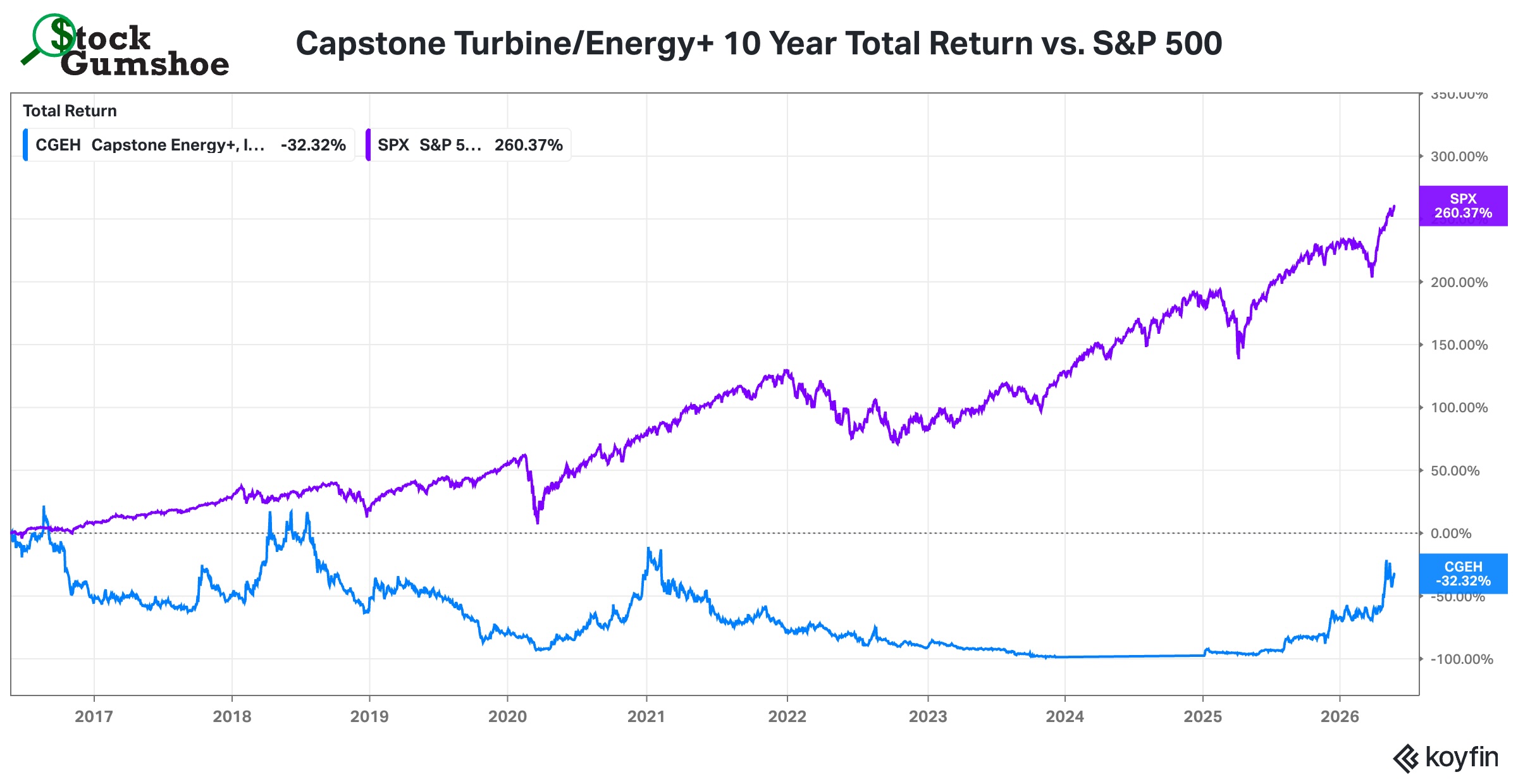

Just for a little context, this is what those overpromise/underdeliver decades look like — this is the past ten years, which shows the impact of promotional periods and good news press releases and gives some hope from the stock’s recovery over the past six months, driven by both new financing and the data center power story — the stock didn’t get zeroed out during bankruptcy in 2023, technically, though it did get heavily diluted and was close to a 100% loss if you sold back then:

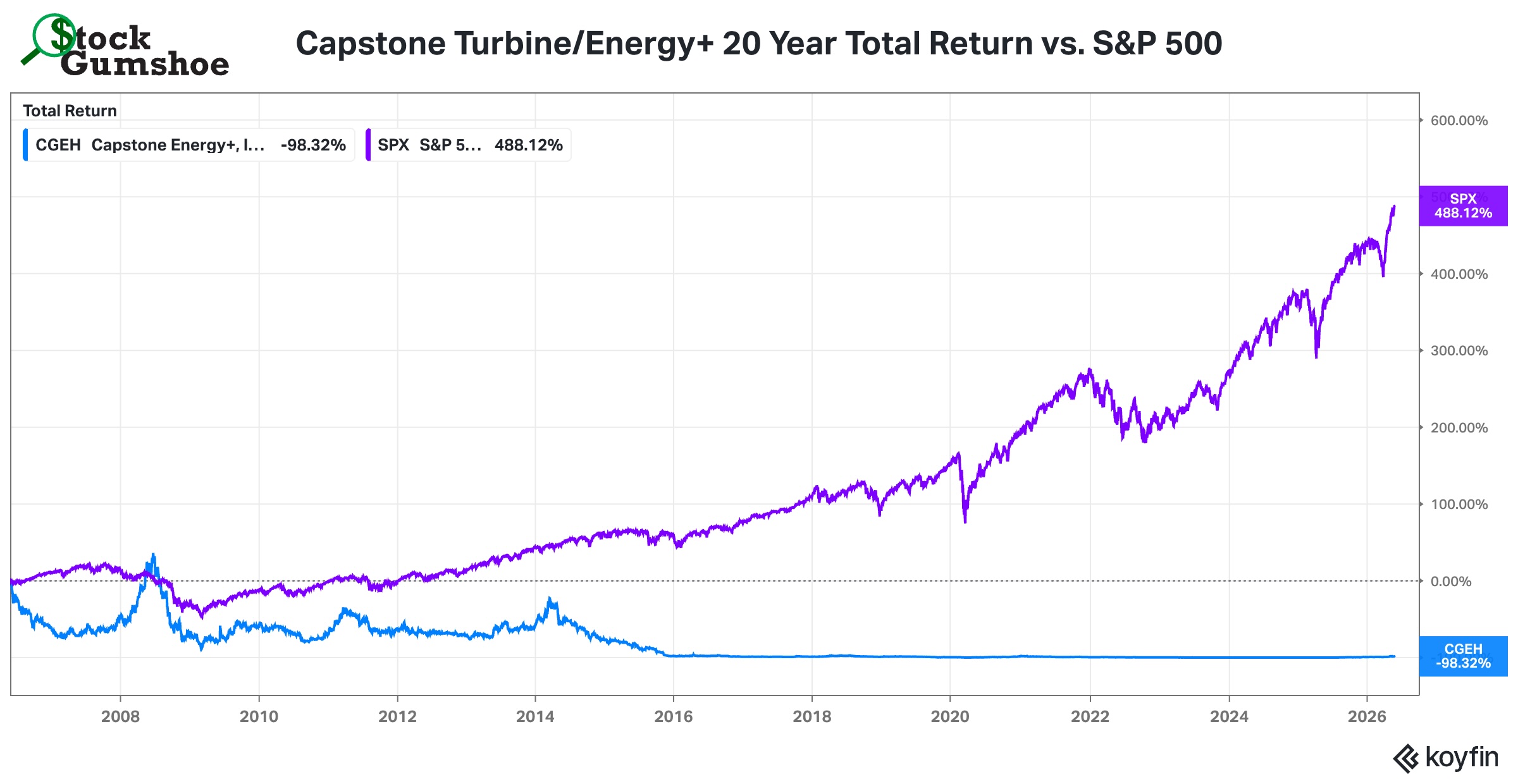

And here’s the 20-year history of this microturbine stock, which makes those past ten years look like a flat line:

I show you those not to try to convince you that Capstone will forever be a disaster, sometimes companies really do turn it around and meet a new moment with great performance. I show you those to remind you that a great story can fade quickly in the absence of actual earnings, and Capstone has often told a great story, and has been teased as a great pick by newsletters (we even covered it once as a teased solution to the Bakken “flare gas” problem, about a decade ago)… but hasn’t backed it up with earnings… yet.

Which means you get to make the call — it is, after all, your money. Are the folks who have bid Capstone up to $10 correct, is this a great opportunity for a still-small company that has reorganized and partially refinanced itself to post some explosive growth as they get into data centers over the next year or two? Think their direct power opportunity is especially going to lead to demand for their microturbines to power those next-gen 800V DC NVIDIA racks in the next year or two? Or are they maybe too small or too constrained to meet this need, and they’re going to be surprised at how much competition there is for remote on-site power? There’s no getting away from the fact that it’s a judgement call and a speculative company at this point, and we’re curious where you lean on this one — buy, sell or ignore? Let us know with a comment below. Thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of Google parent Alphabet, Amazon, and NVIDIA. I will not buy or sell any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Wish I’d heard about this stock a year ago! And then bought, of course…..

This is a pure gamble betting in Management to meet objectives. Im on the sidelines on this one1

Hello, there is a Project Phoenix teaser , any gumshoeing on that?

Who is the ad from? That doesn’t ring a bell.

Sean Brodrick

Have only seen gold pitches from him recently, but I’ll look for it — if you have the email, you can send to ILoveStockSpam@gmail.com (or just paste the link to the ad here)

Looks like a direct competitor to Bloom Energy. BE is much larger and has a long head start in contracts, etc. Think I will stick with BE for now, although the 800V backplane is an interesting angle.

It’s worth a small investment!

Have to laugh as I bought the original CPST in 2007 and sold half after it had tripled and been bagholding the rest ever since. Go CGEH lol

It was strange to take that trip down memory lane, I remember hearing a lot about it 15-20 years ago when they were first promoting themselves. Lucky break for you that they were able to go through the bankruptcy without zeroing out the public shares!