The past few years have seen investors build a growing consensus… maybe even rising to the level of an investment mania… that nuclear power will enjoy a meaningful renaissance in the United States, driven by the need to produce more carbon-free electricity to fuel the hundreds of gigantic new data centers that are being built to house A.I. chips and build the artificial intelligence economy of the future.

It’s always a little challenging to weigh these things as an investor, because the growing interest in nuclear power is real, and both President Trump and President Biden before him have tried pretty hard to speed up permitting and construction of new reactors after decades of little to no activity in that space… but there is also very little that humans do on this earth that is as complicated and challenging (and expensive and slow) as building nuclear reactors. I think we’ve gotten to the point, with changing attitudes and ongoing government incentives and regulatory reform, that we’ll probably begin to see new reactors built over the next several years, most likely starting with a few of the small modular reactors that everyone hopes will simplify construction and eventually (maybe by 2040?) make building new reactors less expensive — but what that means about the revenue or earnings of the various companies in this space over the next decade is still very much an open question.

One thing that usually happens with these cycles of nuclear enthusiasm, though, is a pretty strong reaction in the price of uranium… and that often leads to a huge surge for small uranium stocks, which can be some of the most volatile and exciting names in the junior mining world if you’re fortunate enough to catch them at the right time. So the folks who like junior miners love to try to predict the next uranium price spike, and the next surge for junior uranium companies — everyone’s trying to find the next Paladin Energy, which Doug Casey and Rick Rule famously rode for a 1,000X return — that company has since been mentioned in just about every single uranium-focused newsletter teaser ad.

That surge in price for Paladin, which was a real “penny stock” junior that became a producer at just the right time, was during the 2007 uranium price spike, which was also historically the most dramatic move for uranium — and was caused largely by the flooding at Cameco’s Cigar Lake mine that cut supply, not as much by a surge in demand… though it was also driven by China’s move around 2005 to begin strategically ramping up their reactor fleet and prioritizing nuclear energy, (they’ve built roughly 50 new reactors since then, and the US has built three, all of them with massive construction delays and cost overruns). Paladin, incidentally, is still around and still a uranium producer, but they also went bankrupt and washed out their investors in 2017, be careful about falling in love with your speculative mining investments, they’re rarely the companies you want to own when the commodity price cycles back down… as it always does, sometimes when you least expect it (most uranium stocks washed out sometime around then, too — the Fukushima disaster sank uranium demand for a long time, with widespread reactor closures in Japan and Europe, and 2017 was roughly when uranium bottomed out, near $18/lb, it’s back to $80-90 now).

Uranium mostly trades on very long-term contracts between suppliers/refiners and utilities, with additional complexity brought by heavy regulation and strategic government stockpiles (and, for almost 20 years after the Cold War ended, the decommissioning of nuclear warheads, after which that uranium was downgraded for the commercial market). You and I can’t just buy a barrel of yellowcake and put it in our garage, so there’s not an active and liquid spot trading market like there is for most commodities, but the spot price, such as it is, has surged three times: once in the mid-2000s, when China started building lots of reactors and Cameco’s big mine at Cigar Lake flooded; then again when we were recovering from the global financial crisis in 2010 and reactor construction was growing again… until the Fukushima disaster and the subsequent closure of nuclear power plants in Japan, Germany and elsewhere in early 2011 led to a uranium glut for many years and stubbornly low prices for a decade; and then starting in 2022, when Russia’s invasion of Ukraine made the supply from disarmament and from the giant Kazakh mines uncertain, which fed through to the surge in SMR interest and US reactor restarts thanks to the AI story and rising electricity demand from data centers.

It’s been a wild ride, for sure — it was only less than a decade ago that Westinghouse, one of the global nuclear leaders, filed for Chapter 11 bankruptcy because of the ballooning construction costs for the last couple U.S. new reactor projects (exacerbated by the fact that natural gas got cheap thanks to fracking, and nuclear power just couldn’t compete — until these past couple years, nuclear plants in the US were closing down before they reached the end of their useful lives).

And now, we’ve had a couple years of money pouring in from big tech companies who want “green” electricity for AI data centers, and nuclear power has “gone green” after a decade of gradual acceptance that nukes are the only rational replacement for coal and gas if reducing carbon emissions and air pollution is the priority… so several old reactors are now likely to be restarted (including the surviving reactor at Three Mile Island, which was closed down in 2019 because cheap natural gas in Pennsylvania made it uneconomic, with the restart essentially sponsored by Microsoft).

And for the past 2-3 years, just about any company associated with anything nuclear has surged to trade at historically rich valuations (GE Vernova (GEV), which is half-owner of GE Vernova Hitachi, the biggest competitor for Westinghouse, now trades at a crazy 60X earnings — but insane demand for new turbines for natural gas power plants means they’re booked out for years and might well be worth that much (despite the legacy of GE Vernova-Hitachi, which is also building the first SMR in North America right now, in Ontario, nuclear is still a fairly small percentage of the business). Westinghouse was bought out of bankruptcy by a Brookfield fund in 2018, then Brookfield sold 49% of it to uranium miner Cameco (CCJ) in 2023, and Cameco, a miner that didn’t see its 2007 peak again until 2025 and went nowhere for decades, now trades for 90X forward earnings… wouldn’t be surprising to see a piece of Westinghouse IPO again someday if the nuclear enthusiasm continues).

But back to uranium… Gerardo Del Real is pitching the idea of trying to catch that “next Paladin Energy” kind of return, which is how he believes we can get “Texas Rich” without oil or gas… and he’s been a “uranium bull” for many years — so what’s he teasing? Which uranium stocks should we consider?

Let’s check out the ad… here’s how it gets started:

“I want to help you become ‘Texas Rich.’

“I’m talking about having the kind of wealth where you don’t have to worry about money problems anymore.

“…The kind of wealth that allows you to enjoy all the finer things in life.

“…The kind of wealth that sets your kids – and even your grandkids – up for financial success, even long after you’re gone.

“I’m talking about making 30… 300… even more than 1,000 times your money… from a single investment….

“Nuclear Energy Stock Investors Became ‘Texas Rich’ 20 Years Ago… And… History Is About To Repeat Itself

So that’s a reference to Paladin Energy and a couple of those past uranium moonshot companies from 2004-2007 — yes, they happened, a couple hit those 100,000% gains and a handful of other uranium juniors gained 10-30,000%… but daydreaming about them is really just buying into investing pornography. It’s tempting, but not likely to do you much good in real life.

And the opportunity? It’s mostly coming from the combination of rising nuclear interest, which is leading to restarts of old reactors and (probably) the construction of some new ones, and a supply-demand mismatch in the uranium market after what was about 20 years of no real investment in building new mines. Here’s how he puts it:

“The United States Is Paving The Way For Nuclear Energy – And It Could Make You Exceptionally Wealthy….

“Globally, the world needs about 200 million pounds of uranium each year.

“Yet current production is only around 160 million pounds.

“That means there is already an annual supply shortage of around 40 million pounds”

That is the consensus in the nuclear industry — not the specific number, but that we are living with a structural supply-demand imbalance that started to become pretty clear around 2017-2018, when low prices really cratered any move to create new supply, and is likely to last at least several years. There has been a surplus of uranium in stockpiles for a long time, in large part because of the reactor shutdowns and the long-running decommissioning program for nuclear weapons, but no doubt those are being run down, too, so that’s why the uranium price has now recovered to something much more “normal” in the $70-100/lb range, a level that should be high enough to begin to spur more mine development (supply has begun to grow, led by Cameco, which owns the two biggest mines in the world, in Saskatchewan, dramatically increasing production in 2023 and 2024… and others are generally ramping up supply pretty steadily, mostly from in-situ production, which can often be started up more quickly than Cameco’s hard-rock mining).

And what are they teasing today? Let’s jump right into the “three stocks” bit…

“As Uranium Powers The Electric Grid… These 3 Nuclear Energy Stocks Could Power Your Portfolio – Starting Today

“After what we’ve seen with the various energy crises and widespread blackouts and rolling brownouts over the past few years… and including this summer…

“It’s clear that right now is the time to add carefully selected nuclear energy stocks to your portfolio.

“The opportunity for investors to take a small amount of cash like a single $100 bill and potentially watch it turn into a 6-figure payday couldn’t have come at a better time.”

And then the clues for those three picks:

“NUCLEAR ENERGY STOCK #1: America’s Next Uranium Producer

“Look at this picture… because it could be worth a LOT of money to you.”

Oh, for Pete’s sake… this one’s looking familiar! Again!

Let’s check the other clues beyond that photo, just to be sure…

“… there’s something currently hidden from view within this hill and beneath the prairie floor…

“A massive deposit of uranium that’s owned by the first uranium company Gerardo is recommending.

“How much uranium is there? At least 46 million pounds….

“A leading uranium analyst has called this site ‘one of the best… in the US,’ because of its large size and high grade.

“This company also has both its NRC license and all its final EPA permits after a decade of waiting. It’s perfect timing for this nuclear melt-up.

“And that’s just one of its projects.

“It has several other mining operations that look exceptionally promising and position it to become the newest major uranium producer in the US….

“… could potentially watch this uranium producer’s share price go from $5.00 or $6.00 to $200 over the next 12-18 months….

“A small mining company like this one could quickly go from being worth a few bucks to hundreds of dollars within just weeks.”

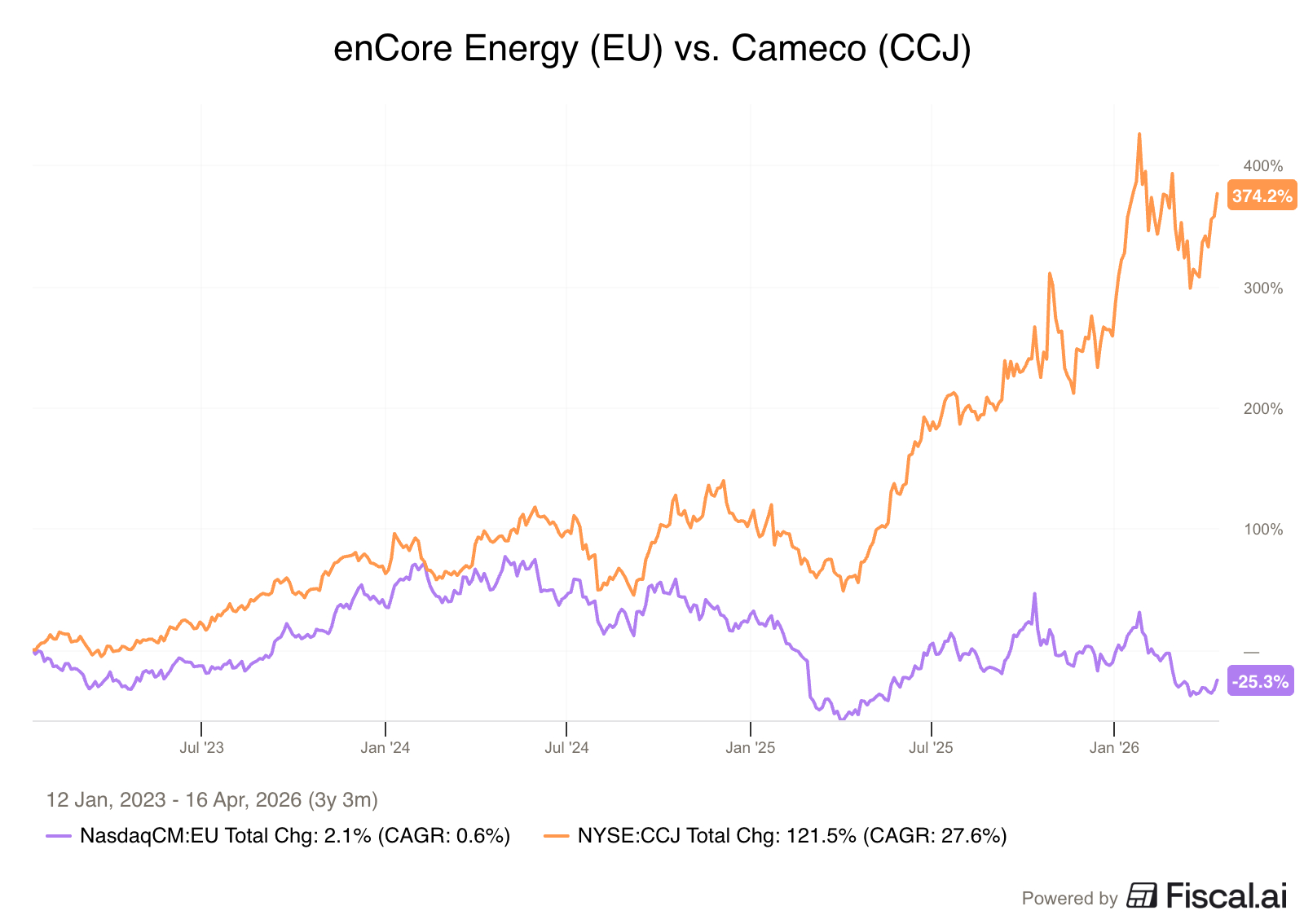

So yes, this is a repeat — Gerardo Del Real first used this photo to promote this “secret” uranium stock in 2022, we covered that ad in August of that year and then updated our look in January of 2023. He’s pitching eNcore Energy (EU in both NY and Toronto), which is a junior uranium story that went from potential in 2022 and 2023 to starting production in 2024. Though it hasn’t been without its hiccups, and the stock has so far failed to enjoy the uranium bull market of recent years — this is what it has looked like since Del Real started promoting it in early 2023:

Here’s how enCore describes itself:

“enCore Energy Corp., America’s Clean Energy Company™, is committed to providing clean, reliable, and affordable fuel for domestic nuclear energy. enCore Energy is the only uranium company in the United States (“U.S.”) with two operational Central Processing Plants (“CPPs”), both located in South Texas. The enCore team is led by industry experts with extensive knowledge and experience in all aspects of uranium In-Situ Recovery (“ISR”) operations and the nuclear fuel cycle. enCore solely utilizes ISR for uranium extraction, a well-known and proven technology co-developed by the leaders at enCore Energy.

Following upon enCore’s demonstrated success in South Texas, future projects in enCore’s planned project pipeline include the Dewey Burdock Project in South Dakota and the Gas Hills Project in Wyoming. The Company holds other assets including, non-core assets and proprietary databases.”

ISR production is likely to be the dominant form of uranium production going forward, and it’s a little bit more like oil and gas production (or lithium) than it is like traditional hard rock mining, they pump fluid into uranium-rich rock, then pump out the uranium-enriched fluid and extract it to make yellowcake. So it’s much faster production than mining, with a much smaller environmental footprint than the big hard rock mines that Cameco operates in Saskatchewan, but it’s still not cheap to run these operations. I think all of the U.S. uranium operations that are either producing or likely to produce in the near future, from UEC and Cameco and others, are ISR projects. Here’s a page from enCore’s latest investor presentation that illustrates how it works:

Once you start producing, you tend to get valued based on your cash flow, and that has been the problem for enCore — they’ve been generating actual revenue since the end of 2023 from their two Texas ISR production sites, but for the first 18 months or so it was not enough to generate even a gross profit, let alone cover their administrative expenses, and they have been dealing with still-high capital commitments to build up capacity. They’re a uranium producer now, and have been for more than two years, but they’re still burning cash, even with high spot prices for uranium.

There is some analyst coverage for enCore now, much more than there was a year ago (partly because they’ve sold shares and sold convertible bonds to raise cash — those are the activities which attract and enrich investment banks), and they expect revenue to begin growing this year, but now don’t expect the company to report an actual profit until maybe sometime in late 2027 (the lone analyst covering the stock last year expected 50 cents in GAAP earnings in 2027, now the expectation is that they might get to ten cents in earnings by 2028).

The bigger potential production growth would be from new projects in the future, including Dewey-Burdock in South Dakota in 2028 (that’s where the photo that the ad uses comes from), and a couple Wyoming projects in the year or so after that (which, like Dewey-Burdock, came as part of enCore’s acquisition of Azarga Uranium, a company that this newsletter publisher had also promoted, back in 2020). The South Dakota/Wyoming projects together are where that estimate of “at least 46 million pounds” of uranium came from, though I don’t think that’s actually a formal resource estimate yet, total resources for Dewey-Burdock are now around 17 million pounds. For the next few year’s, the goal is mostly to ramp up more of their Texas projects to generate more production. The news there is that Dewey Burdock has been approved for “fast track permitting” as of last August, but they’ve had a bunch of their permits for a while without moving forward with much work (their estimate is that the initial capital cost of Dewey Burdock will be $264 million, with a rapid return on investment thanks to a post-tax internal rate of return of 33% if uranium stays in the $80s, so it’s at least a financially appealing project).

What else is Del Real recommending these days? Next clues…

“NUCLEAR MELT-UP STOCK #2: An Unhedged And Production-Ready Uranium Rocket Ship Ready To Soar

“During the last nuclear melt-up, this stock went from 16-cents… to nearly $7.50 – for a gain of 4,587% in only two years….

“The company has a suite of production-ready assets in the US.

“It’s also been on an acquisition spree – adding assets in the US and Canada that give it millions of uranium pounds in the ground.

“In fact, the company has nearly 300 million pounds of uranium across all its projects.

“At my predicted uranium price of $200 per pound during this nuclear melt-up, that has an in-situ value of $60 billion.”

And they say the company has a market cap of $1.4 billion, so that $60 billion stands out as a big number. What else?

“… those resources are completely unhedged…

“Plus, this company has zero debt.

“And it’s also been warehousing uranium – in anticipation of higher prices – to the tune of 1.7 million pounds.

“Today, it’s trading under $10.00 per share.

“But a run like it had last time could take it close to $200 per share.”

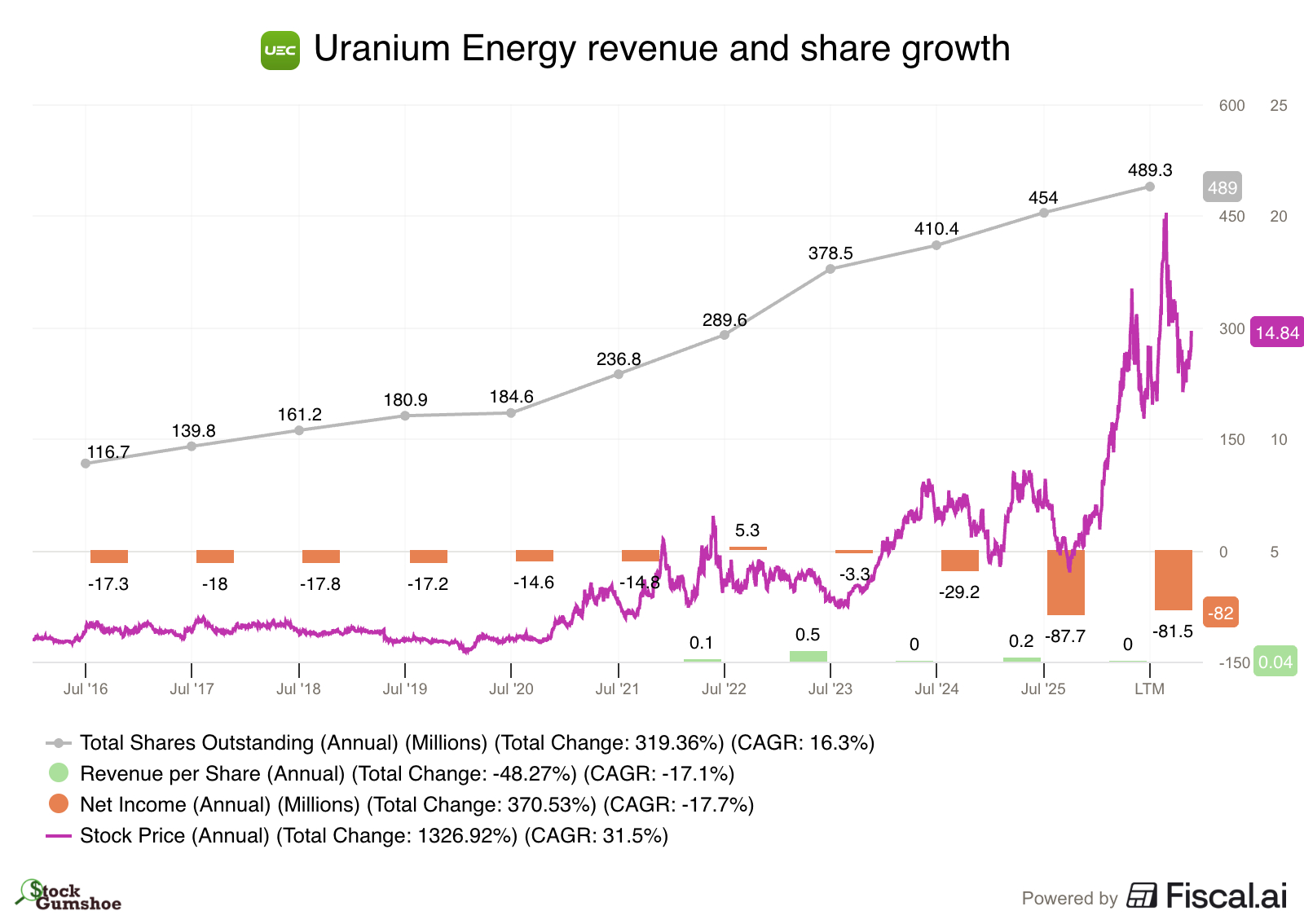

Well, OK, Del Real says it’s still a “strong buy” at $10… but this is also a repeat, that’s almost certainly Uranium Energy Corp (UEC) — which hasn’t been near $10 for a while now (it topped out near $20 in January, and is around $15 today.

This stock has been pitched as a uranium play for more than a decade now, by a variety of newsletters, and the company was essentially built to load up on potential uranium resources without spending too much money on developing those resources, in the hope of being ready for a surging uranium market someday — so this is the world they’ve been hoping for.

And it has gone well, so far — if we go back to that mid-2022 return of interest to the uranium names, this is how UEC has looked during that time… they, too, have issued tons of shares, both for acquisitions and for stock-based compensation, and the stock has come down from its recent highs, but it’s still well above where it was a few years ago… and it has almost kept up with market-leader (and large cap producer) Cameco:

I’ve got a personal history with UEC that gives me a sour taste when I write about them, so I won’t be buying the stock… but they were certainly built for the improving uranium market that has emerged over the past few years, and it might work out very well.

And they’re still trying to grow — the massive share issuance to build the company and cover their overhead during the past 20 years or so means the company is much larger than during past spikes — this was a $100-400 million company from 2007 to 2021, when it was just sitting and waiting for a better uranium market, and today that market cap is up to $7 billion (so they needs to update this tease a little bit, the market cap hasn’t been $1.4 billion in a long time). And even with the uranium price finally recovering quite dramatically over the past few years from those 2017 lows, UEC hasn’t produced that much just yet — their revenue over the past decade has grown much more slowly than their share count:

Which doesn’t mean it can’t or won’t work out well, they’ve built up a lot of potential production capacity — but it means that as has always been the case, their profitability is in the future, not in the current income statement. Analysts now forecast that they’ll have a drop in revenue this year, but will burst into pretty dramatic revenue growth over the next couple years… and that this will lead to profits down the line. So UEC is currently trading at about 50X forecasted 2028 earnings, though I don’t know what uranium prices will be for the next couple years — if uranium soars to $200, maybe those estimates are far too low, we’ll see.

So… coiled spring? Or a company that has accumulated tons of resources and will never spend much on bringing those projects toward production? Could be both, I suppose — so far they’ve built a large company through share issuance, including stock-based compensation, but whether or not it turns into a great deal for shareholders today probably depends on whether they become a sustainable producer at scale… and, of course, on what the uranium price is when that happens.

So that means this pitch so far has re-teased two of the stocks that Del Real pitched in the first big uranium spiel that we covered during this “nuclear renaissance”, back in late 2023. How about number three, is that also a repeat? Let’s check the clues, this one’s pitched as being maybe even more exciting than the first two:

“NUCLEAR ENERGY STOCK #3:: The Uranium Stock That Could Deliver 30-Times Your Money In Just Weeks

“This Canadian mineral company is engaged in the acquisition, exploration, and development of uranium assets in the pursuit of a clean-energy future.

“And while I’m excited about the previous two companies, this one here could quickly turn $1,000 into $30,000 or more in just a matter of weeks.”

So… why, you ask? From the ad:

“… it’s currently exploring a massive, underexplored land package.

“Originally, the area was known for its copper deposits. And the land position was owned by over a dozen companies.

“But today — for the first time ever — in anticipation of this nuclear melt-up, this company has become the sole owner of an entire district that hasn’t seen a modern mining approach in over 50 years.

“There is abundant infrastructure supported by a network of roads, rail, deep-water ports, airports, service centers, hydroelectric power, and a skilled workforce.

“And it’s in a politically stable mining jurisdiction of Canada with a transparent permitting process and established mining and taxation laws.”

Other clues? They’ve got “over $5 million in cash,” and “may be only weeks away from the next big discovery.”

More detail:

“… just last year, the company announced the most significant exploration program to date targeting Canada’s most prospective regions for high-grade uranium discovery.

“That’s why I recommended it to my readers of Junior Resource Monthly while it trades below a dollar per share.

“They’re not buying this tiny uranium explorer to just potentially double their money. They’re in it to make many multiples, like the one-stock millionaire “Texas Rich” gains that uranium stocks are known for.”

Now that we know the first two are re-teases, and that their data was very out of date, I suspect that this is also still the stock that we thought it was when I covered Del Real’s first “three uranium stocks” pitch, when this newsletter dropped similar clues — at the time our best guess was Latitude Uranium, which was exploring primarily in the maritime provinces, but they have since been acquired, so the best guess is now ATHA Energy (SASK.V, SASKF), which acquired both Latitude Energy and an Australia-listed firm called 92 Energy in 2024… . Back then they were claiming “$50 million” in cash on the books, which is close to where the combined company maxed out… but yes, as of about a year ago that was down to $5 million, and they raised some more money in mid-2025 so that total cash on the books was back up to about $10 million at the end of the year. Probably lower now, of course, since they’re an exploration stage company, which means they’re a cash burner.

Here’s how ATHA describes itself now:

“ATHA Energy is a uranium mineral exploration Company focused on advancing exploration at scale at its flagship Angilak Project in southern Nunavut, where ATHA controls 100% of the Angikuni Basin. ATHA offers significant exposure to uranium discovery, controlling the largest cumulative prospective exploration land package (>7 million acres) across Canada’s most prominent basins for uranium discoveries, and 10% carried interest exposure in key Athabasca Basin exploration projects operated by NexGen Energy Ltd. (TSX: NXE) and IsoEnergy Ltd. (TSX: ISO). ATHA is institutionally backed, led by a strategic investment from Queens Road Capital Investment (TSX: QRC).”

And yes, ATHA Energy did initiate their “most significant exploration program to date” back in March of 2024. That led to an “exploration target” of 61-98 million pounds of U308 at their Lac 50 deposit and “district-scale” potential across the Angilak Project (which includes Lac 50, part of an area in Nunavut that they’re pitching as a “geological analogue” to the Athabasca Basin in Saskatchewan, where Cameco operates McArthur River and Cigar Lake, the premier high-grade uranium mines in North America). ATHA also has exploration targets in the Athabasca, as well as the Latitude projects in the Central Mineral Belt in Labrador.

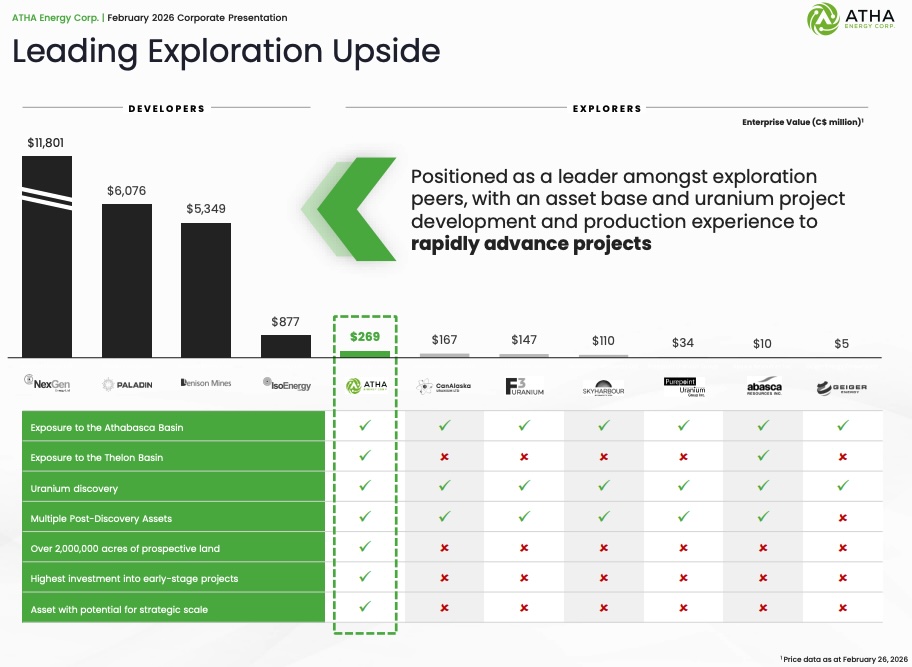

Here’s the page of their Investor Presentation where they stake their claim to being uniquely positioned in Canadian uranium, on the cusp of going from an exploration company to a developer…

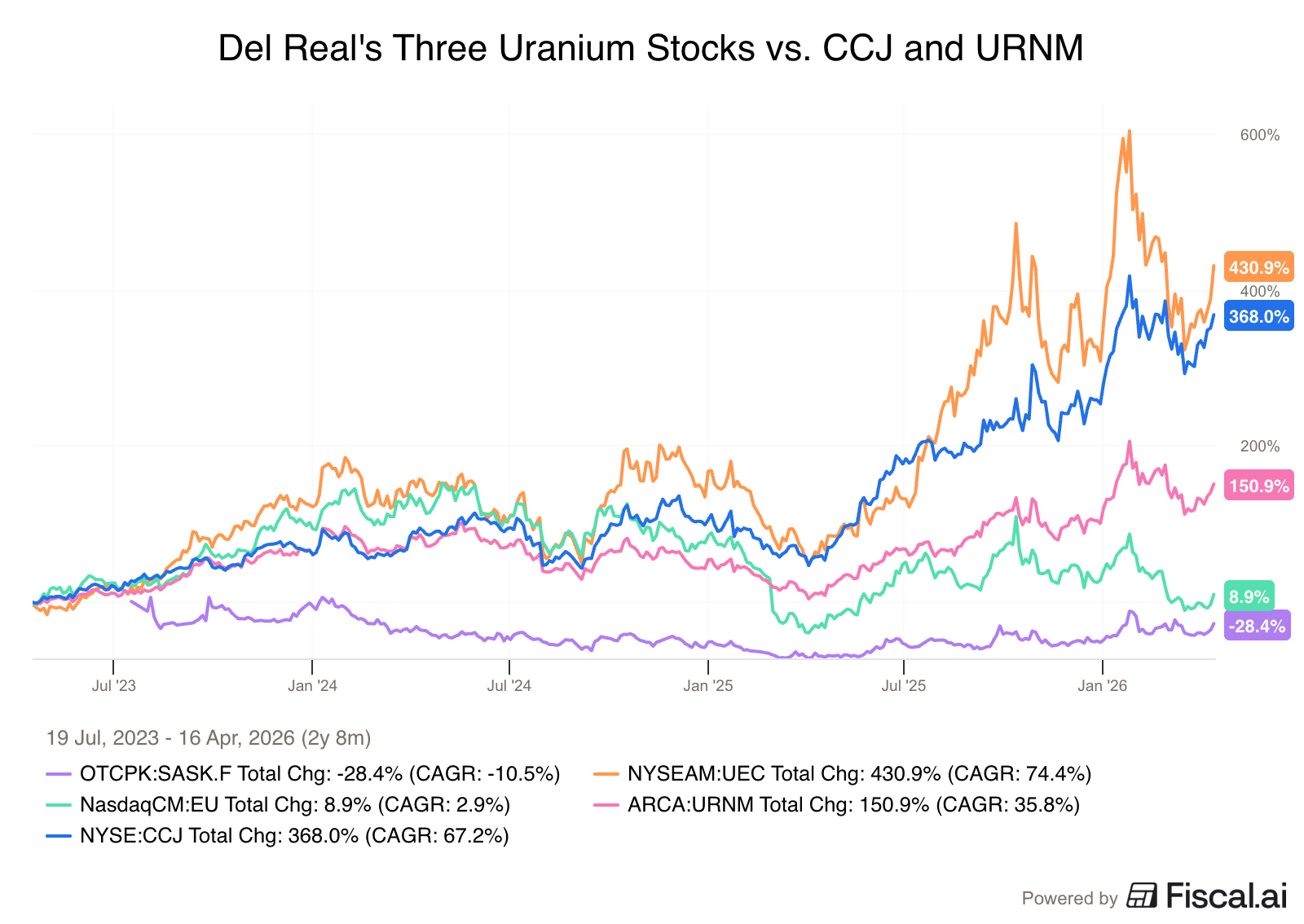

So yes, I’m afraid that this Junior Resource Monthly ad seems to just be repackaging the same three uranium companies they’ve been promoting for a few years, since the Spring of 2023. As I said, it’s been a pretty wild ride for these three, and for just about anything in the nuclear/uranium space since then, but here’s how that looks on a chart — this is the performance of those three stocks going back to our first copy of this “three uranium stocks” tease (ATHA acquired Latitude, so we’ve used ATHA on the chart), compared to Cameco and the Uranium Miners ETF from Sprott (URNM), which would have always been the two easy “knee-jerk” buys to make if you wanted to bet on uranium becoming more valuable:

None of that tells us what will happen next, of course, and the future is always in the eye of the beholder — so I’ll leave that to you to divine. But it is a reminder that speculating on junior miners, even in a good commodity market, does not guarantee a great outcome.

I’m not interested in speculating on the next great junior uranium story, mostly just because I have no skill at trading those story-driven peaks and valleys, and I know that millions of pounds of uranium have been discovered over the years which haven’t been worth digging up out of the ground… but I also tend to be pretty cautious with junior exploration and development stories in general, given how financial fragile they usually are, and stock market history tells us that these kinds of companies can certainly fly higher when investors get excited.

And for those who, like me, prefer investing in royalty stocks over producers… there’s been some recent news on that front, too, with Uranium Royalty Corp (UROY, URC,TO) agreeing to merge with/acquire the private royalty company Sweetwater Resources. I haven’t dug into the details yet (investor presentation on the deal is here, it was just announced today), but they believe that the combined company is currently being valued at an enterprise value of about $2.2 billion (thanks to a meaningful slug of about $625 million in debt), which means they’re valued at a little over 30X their trailing EBITDA. They do expect meaningful growth from Sweetwater’s Wyoming production, including both future uranium royalties and sales of soda ash, so perhaps that will be interesting. Not smack-you-in-the-face cheap, at first glance, but maybe interesting nonetheless — for what it’s worth, Uranium Royalty was created by Uranium Energy Corp, and UEC remains a major shareholder and partner.

Sound like the kind of trade you’re looking for? Have a favorite among those uranium juniors we glanced at, or others that you think are better-prepared for the next wave of enthusiasm? Please let us know with a comment below. Thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of Brookfield Corp., Brookfield Asset Management, and BWX Technologies. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

What do you think about URAA?

Any thoughts on SRUUF?

I still like Dennision – DNN

I hold a group of Uranium stocks including UEC, Encore, Cameco and I held UROY for a while. UEC has really run, but it has the liquidity you need for a lot of investment firms to take notice. Cameco is the one stop shop and has the most liquidity and institutional attention . I’m up on both. Encore is a dog that’s had deadline, management, and balance sheet problems. It’s kinda stuck in the starting gate from where it should be as a producer. Thus, It still has upside. Buyer beware. this sector isn’t as bad as nat gas, but it is a widow maker.