“Beginning June 9, a new AI IPO could

“12X your money as millions of Nvidia chips go DARK

“Two financial legends predict a paradigm shift that will reset the market, cause Mag Seven shares to plummet, and define the true winners of the next AI era.”

That’s the lead-in to this week’s ad for Exponential Tech Investor ($2,500/yr, no refunds but 90-day Brownstone credit “guarantee”, comes with 1 year of Chaikin’s PowerGauge Pro as bonus), which is essentially being pitched by Jeff Brown and Marc Chaikin in a staged “interview” by Tom Mustin, one of the rotating group of actors and former local TV anchors who get roped in for these events.

They refer to this sales pitch as the “Dark AI Summit,” and the basic idea is pretty simple: Jeff Brown says the hyperscalers and other AI leaders can’t get enough electric power, so they are going to have to leave all these gajillion-dollar GPUs they’ve bought “dark,” unpowered and unused. That is going to lead for weak results for the big tech companies, but it’s also going to create an opening for Elon Musk’s latest dream, which is building a network of orbiting data centers in space. That project will build on SpaceX’s Starlink constellation of broadband internet satellites, and become quickly viable as Starship helps the launches of these new data center satellites become much less expensive.

They keep throwing around the idea of a 10X disruption piled on antoher 10X disruption, which could create insane growth as Elon surprises the world again. And the key to the pitch is that the story will really catch fire when SpaceX has its IPO and more and more data comes out about what they’re doing… with Jeff Brown predicting that June 9 is the most likely date for that IPO.

The big picture theme is not new, that’s roughly similar to Jeff Brown’s “Orbital AI” pitch that we covered last month for his lower-cost Near Future Report… but he’s teasing and recommending different investments this time.

Here’s a bit of the hype from Mustin:

“June 9th isn’t just a day of reckoning for the old guard of AI. It also represents the single greatest wealth creation opportunity Jeff and Mark have seen in a combined 90 years of investing. On that date, Jeff believes the biggest AI IPO in history will open to the public. He’s even promised to share a way for you to get a stake in this company before the IPO during today’s broadcast. But first, what’s most important to understand, it’s a company with the power to solve one of the AI market’s most existential problems. And if he’s right, the investors who understand the gravity of what’s happening on June 9th will look back on this moment the way early Bitcoin buyers look back on 2015 and the way early Nvidia investors look back on 2016.”

And Marc Chaikin poured some fuel on the flames:

“It’s clear to me that June 9th will be a decade defining and possibly even a century defining moment for our country and our financial markets. I believe it could even restore a sense of national pride in America unlike anything I’ve experienced since before the Vietnam War.”

So what’s the “way to buy a piece of SpaceX before the IPO?” Well, we know that Jeff Brown has recommended the Ark Venture (ARKVX) fund in the past, which is one of many interval funds and closed-end funds that has invested relatively heavily in SpaceX (about 13% of the fund, in their case, the SpaceX exposure for most funds who own it has jumped a lot this year, just because those funds have updated the value of their SpaceX shares to reflect the higher and higher prices the company has been getting in secondary sales heading up to the IPO). I won’t go into this in too much detail, since I wrote a pretty exhaustive piece about all of the funds and companies who have meaningful SpaceX exposure earlier this year. SpaceX is the most liquid private company in history, I think, it’s been pretty available on the secondary market for many years as they continue to raise billions and billions of dollars, and there are a lot of ways to buy funds that have anywhere from about 8-20% of their NAV invested in SpaceX right now.

But Brown does say this about the company he likes for pre-SpaceX exposure:

“… last year, a public company made a deal with this private AI firm, selling them valuable assets that were difficult to find anywhere else. And in return, this publicly traded company received shares of this pre-IPO AI firm, which could triple in value on June 9 when it goes public for the first time.”

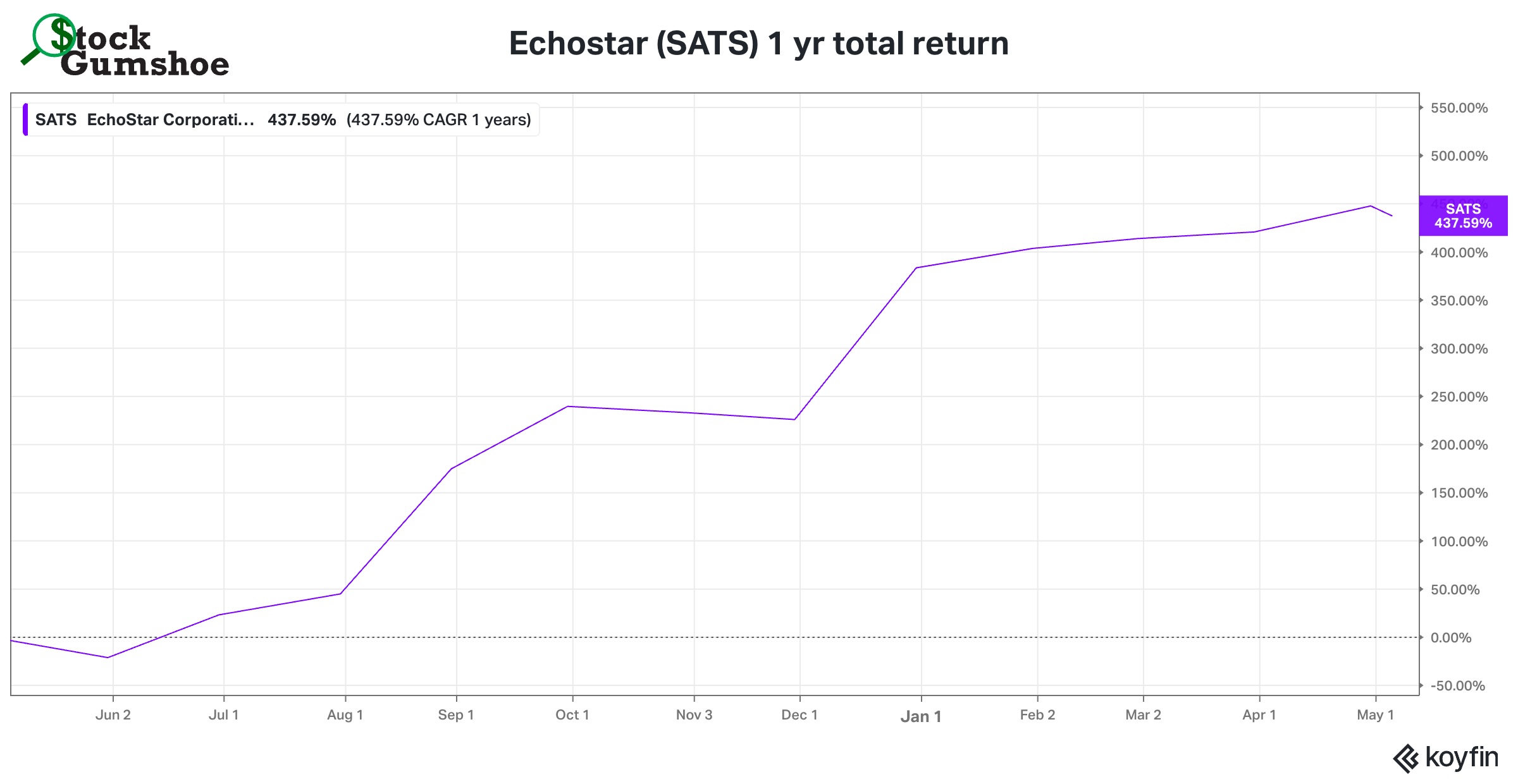

That’s very likely Echostar (SATS), which has essentially been trading as a SpaceX proxy since they traded their spectrum rights for SpaceX shares in a deal announced last year… though the deal hasn’t yet been finalized, so Echostar doesn’t actually have the shares yet (spectrum is highly regulated, so it has to go through approvals). This is going to take some time, with the deal expected to close in November of 2027, but EchoStar essentially sold spectrum to SpaceX in exchange for $11 billion worth of SpaceX stock, $8.5 billion in cash, and an agreement by SpaceX to cover a couple billion dollars in interest payments until the deal closes, really just to keep Echostar from defaulting on its debt before they can finish the transaction.

This was just after Echostar sold a bunch of wireless spectrum to AT&T (T), and all of this was essentially just Echostar monetizing a lot of spectrum they owned but were barely using (or not at all), and were at risk of losing if the FCC determined they were just hoarding spectrum. At the same time, Echostar had essentially been in survival mode because of its huge debt burden, so it wasn’t a big surprise that they sold stuff… but the fact that they sold to SpaceX in exchange for shares, partially, is what led SATS shares to really soar. They announced the AT&T deal in August, and the SATS sale in two tranches, first in September and then in November, and SpaceX went from a private-market value of about $400 billion over the Summer to about $1.75 billion as we head into the IPO, so that SpaceX reset is “in the stock,” that’s why SATS shares have jumped ~400%:

Might it soar higher still? Sure, if SpaceX rises dramatically into or after the IPO and heading into the close of the Echostar/SpaceX spectrum deal in probably late 2027 — Echostar’s other businesses have been in decline for years and are essentially irrelevant to investors right now, but the stock is likely to track whatever the value of SpaceX is, so you can think of it as being one way (among many) to get some exposure to SpaceX before the IPO, just remember that you’re effectively paying for SpaceX shares at a $1.75 trillion valuation (~100X trailing revenue, according to guesses), the price you’d pay for SATS today means you’re not getting the SpaceX exposure at some earlier/lower price.

The other big, liquid private owner of SpaceX, aside from the various pre-IPO investment funds, is Alphabet (GOOGL, GOOG), though even their large holding (they own about 7.5%, last I checked) isn’t big enough to really move the needle for that $4+ trillion company. Maybe someday, but for now it’s “only” $100 billion or so in hidden value for Alphabet.

Well, not really all that hidden — the ramp-up in the valuation did have to be reported in Alphabet’s earnings, so that was good for a bonus ~$2 per share worth of earnings last quarter, one reason for GOOGL’s shocking report that they earned more than $5/share, vs. the expected $2.50 or so (I’m rounding — I wrote about this on Friday when analyzing Alphabet’s earnings if you’d like more specifics).

And they move on to more details about the “dark” part of the story…

“June 9th could mark the high water line for many of America’s favorite AI stocks. So, for the last three years, tech stocks like Nvidia or Alphabet, the parent company of Google, Meta Platforms, Microsoft, and Amazon have carried the market to heights that most people would have thought unimaginable. And since the historic release of ChatGPT on November 30th of 2022, not that long ago, Microsoft is up as much as 135%. Amazon as much as 174%. Alphabet up as high as 264%. Meta platforms as much as 627%. And of course, Nvidia has risen 1,229%…. these five companies alone have added trillions in value to the market over the past three years, dragging the entire market upward on their shoulders. But the future of these companies is in danger like never before.

“We’re heading towards something that I’m calling the dark chip crisis, where the millions of Nvidia chips powering this revolution go dark and sit idle for months, collecting dust.

“Demand for AI chips far exceeds supply right now. But my worry isn’t that NVIDIA is building too many Blackwell chips. My worry is much more structural. Simply put, these AI companies are about to hit a brick wall… All this points to troubles ahead unlike anything that we’ve seen in over 25 years.”

The big picture, arguing against the idea that greater efficiency will save us:

“Over the last six generations of NVIDIA chips, processing efficiency has increased by one million times. If your car’s engine saw efficiency gains like that, one gallon of gas would get you to the moon and back.

“But at the same time, the amount of computation deployed to train AI models is also increasing exponentially. And this is where most people have the story completely wrong about the possibility of a dark chip moment for stocks.

“My worry isn’t that NVIDIA is building too many chips or that the Magnificent Seven are building too many data centers. The risk these companies are facing…

“…we are now up against a limitation that can’t be designed away in a lab by NVIDIA’s engineers. Simply put, it’s energy.”

And Chaikin chimes in to note that those “Mag 7” stocks are also getting less attractive in his system:

“After maintaining a bullish rating for the majority of this bull market, Amazon and Microsoft recently flipped to bearish ratings, while Google, Meta, Nvidia, and Apple are now rated neutral, which is the last step before a bearish rating.”

And then Brown sums up his SpaceX pitch:

“… the new AI company going public on June 9th promises to eliminate the threat of dark chips forever, create thousands of millionaires overnight, and usher in the next era of the AI market.

“I’m talking about Elon Musk’s SpaceX.

Mustin: “SpaceX? I mean, isn’t SpaceX just a rocket company, though?”

Brown: “Well, I think that’s what most of the world thinks. I mean, they also believe that Nvidia just made chips for video games when I first recommended it in February of 2016, and that Tesla was just an electric vehicle company when I first recommended it in early 2018….”

Brown describes SpaceX’s Starlink as the way that Elon has funded the investments in his ambitious launch vehicles, but it has now become a meaningful telecom supplier:

“Starlink has over 10,000 of these satellites orbiting earth… a literal world wide web which I often refer to as an orbital internet backbone that this has made Starlink, a subsidiary of SpaceX, the most innovative telecommunication company in history.

“Today it has more than 10 million customers in 150 countries around the world. It allows you to connect to the internet from rural communities, far from the grid, on Ukrainian battlefields, even out in the middle of the ocean. Now, I’ve used it myself on commercial flights, on private flights, in the field, and even at my home when my fiber line has gone down from a storm. Now, it is phenomenal. The performance is undistinguishable from a wired broadband device. And Peter Ingram, the CEO of Hawaiian Airlines says, SpaceX really cracked the code literally in terms of technology to be able to deliver a wide bandwidth of very high quality connectivity to an airplane within global reach.”

And Chaikin chimes in, though it’s really not clear why he’s in this “Dark AI summit,” beyond the publisher’s interest in cross-selling these two publications (both Brownstone and Chaikin are owned by Marketwise (MKTW), Porter Stansberry’s old company).

“Starlink created a global internet provider without laying a single mile of fiber anywhere on Earth. So it’s no surprise that my power gauge gives the entire communications sector a weak grade right now.”

And Brown says that although Starlink will generate about $19 billion in revenue this year, and is by far the most profitable part of SpaceX’s business (essentially subsidizing both the SpaceX launch programs and Musk’s xAI company, which he merged into SpaceX recently), that this broadband constellation is really just the first step:

“Starlink is simply a proof of concept for what SpaceX is about to do next. Elon Musk has known for years that energy would be the ultimate bottleneck in AI. He built the solution to this problem at SpaceX, a technology even more valuable than the Starlink constellation. It’ll create a paradigm shift in AI that changes everything, an innovation that could help avert the dark chip crisis companies like Amazon, Meta, Google, Microsoft, and Nvidia are facing in 2026….

“… all the costly problems that AI firms face disappear if they send their AI chips to outer space. I’m not kidding. There’s no land to buy. There’s no permitting requests. There’s no pushback from local communities or environmental groups. At negative 455 degrees in orbit, no water or costly cooling equipment is needed at all. And most importantly, there’s no energy bill. In space, solar-powered satellites in a sun-synchronous orbit can capture energy basically 24 hours a day. Outside of the interference of Earth’s atmosphere, solar panels are roughly twice as efficient. And given other restraints on Earth, like weather and the fact that solar can’t generate energy at night, obviously, space-based solar panels can produce about six times more energy a day than terrestrial solar panels.

“So on Earth, energy is constrained. But in space, it is literally infinite. And it’s a heck of a lot easier to transmit data from space to Earth than it is to beam energy from space down to Earth….Let’s get those data centers into space and take advantage of all that free, clean energy and, of course, free cooling We are talking about a 10X convergence in how energy can power AI. It is a complete paradigm shift.”

Jeff also says that the other big tech companies are chasing this story, too, with Google wanting to move some data centers into space, and Jeff Bezos suggesting that the big training clusters of GPUs be moved to orbit, so they’re all trying to catch up with SpaceX’s ambitious “put a million orbital data centers in space” plan. And none of them will be able to match SpaceX’s cost advantages:

“Today, a SpaceX launch is 30 times cheaper than NASA’s space shuttle in 1981… and nine times cheaper than what was possible before SpaceX existed. So before SpaceX, it cost roughly $13,000 to just get a single kilogram into outer space, which is the equivalent of just a little bit over two pounds. And today, that price is down to about $1,500… before the end of 2026, I predict that SpaceX, with its Starship, will drop launch costs 10x again down to just about $100 a kilogram….”

And apparently NVIDIA is getting ready to provide hardware for these orbital data centers:

“NVIDIA just announced the Vera Rubin Space One AI computing module explicitly for orbital data centers. And in March, NVIDIA CEO said space computing The final frontier has arrived. But Musk has known it all along. He’s built the first completely vertically integrated orbital AI company in the world.”

There are lots of plans to launch “data centers” in space, whether built around NVIDIA’s Vera Rubin processors or something else, though it seems like we’re pretty early on in the “how to make cooling work” part of the satellite data center projects — I guess they’ll end up having to have some kind of copper radiator system to disperse the heat, since it’s not clear how viable active cooling is in space, but I’m sure there will be more innovation, and that I won’t be the first to know.

More from the ad:

“SpaceX’s Starship will carry its own orbital data centers into outer space, but the Starship will also help countless innovative companies get their technology up into the stars as well. And, you know, at just $100 per kilogram to orbit, even smaller startup companies will be able to afford launches into space. In fact, there’s one small firm at the center of this story that could make you even more money than buying SpaceX as it sends its AI data centers into orbit.”

So now we begin to get into the hints about what stocks he likes:

“… my favorite ways to take advantage of the SpaceX IPO trade for about $10 and 25 respectively right now and i can tell you from an engineering standpoint that both are at the bleeding edge of technology and positioned to grow exponentially when SpaceX IPOs and companies like Amazon and Google race to get their own ai chips into space… the technology world is evolving so quickly today it’s leaving most industries completely behind….

“I also have to be realistic. SpaceX’s most recent private market valuation was at $800 billion. Now, I believe it will be a $10 trillion company. That’s about 12x upside over the long term. So you can still do very well by holding it from now until the IPO in the months and years beyond and make huge gains if you hold on for the long term. But current estimates are that SpaceX will IPO at $1.75 trillion valuation… that’s fully valued, based on future growth, so there is a natural limit to how high SpaceX stock could go if it debuts at a $1.75 trillion valuation in the short term, which is why my number one way to play the spacex ipo is another much smaller company You can buy shares today for around $25….

… as SpaceX’s Starships launch the first orbital data centers into outer space, I believe this company’s technology will be riding along with it.”

Hmmm… other clues?

“50% of space-based spending today is government spending on defense applications. SpaceX is laser-focused on building orbital AI data centers, so they’re unlikely to build the next-gen defense and communications satellites that our country and allies will need. This provides us with an under-the-radar investment opportunity that could offer one of the highest returns on our investment over the next 12 months….

“The firm that I’m talking about supplies the core spacecraft platforms and mission infrastructure for our country and our partners, civil and defense orbital infrastructure. And because it was founded specifically to mass produce high-end satellites in the same way that the auto industry mass produces cars, it already has the manufacturing capacity to do so at scale.

“This company’s technology isn’t theoretical. It’s already being deployed by the Pentagon, and this firm’s technology is a critical piece of Project Maven, the Pentagon’s flagship AI program. So this positions the company as the foundational supplier for the next era of proliferated, autonomous, and resilient space architecture.”

And one final clue:

“… it recently reported revenue growth of 52% by creating a manufacturing process where thousands of interoperable satellites can be built quickly, affordably, and reliably. This company is positioned to do for spacecraft what TSMC, Taiwan Semiconductor, did for semiconductors and what Tesla did for electric vehicles. If, as I expect, this company becomes the go-to source for the Pentagon’s orbital defense infrastructure contracts, this could be like buying Boeing or Lockheed when they were still small, innovative companies.”

So what’s that “Top Stock for the SpaceX IPO, the Tesla of Spacecraft?”

Brown sums it up:

“This firm’s founders believe spacecraft should roll out of factories like cars and not emerge as just one-off engineering marvels that take years to design and build. They essentially took Elon’s Tesla playbook and are using it to build orbital satellites at scale. And in the early days, that idea made it a curiosity. But today, It makes this $25 stock a cornerstone of the Pentagon’s national defense strategy. It’s become a system-critical defense supplier capable of building satellite constellations faster and cheaper than the old legacy aerospace giants ever could. And because most analysts think of this company simply as a manufacturer and not as a company building the next generation of autonomous AI-enabling spacecraft, we can still get a stake while it’s completely under the radar.”

And he says that “10X your money this year wouldn’t surprise me if it wins more government contracts, thanks to the enthusiasm that we can expect the IPO to create. And that is just the baseline.”

There are a bunch of companies in both the US and China who are trying to “productize” satellite production and make it less one-off and less artisanal, with higher-volume assembly lines, and SpaceX has already done that to some degree with its production of Starlink satellites and terminals, though a lot of that was outsourced to STMicroelectronics (STM)… so we could even consider some smaller private companies to be decent matches, like Terran Orbital (which is a Lockheed Martin subsidiary) or Apex (which is private)…

But if we’re talking about 52% growth specifically, then that pretty well has to be either RocketLab (RKLB), which reported 52% growth for the year ending in the third quarter last year, or MDA Space (MDA), which was at 51% for the full year in 2025.

Rocket Lab is probably the better match for that conceptual tease that the “founders believe spacecraft should roll out of factories like cars,” and in fact has built some satellites for MDA Space, but MDA, though it was founded more than 50 years ago and is a leader of the Canadian space industry, is also firmly in the “mass produce satellite stuff” category now, and they’re being called upon for a lot of non-SpaceX LEO projects, particularly for Canadian and European companies (though they’re also a big contractor in the US, including for defense projects like the Golden Dome).

For those who’ve been following the space business for awhile, MDA Space was initially well known for the development of the Canadarm robotic arm for spacecraft, and has had a bunch of different names — they were acquired by Orbital Sciences about 30 years ago, then went through some M&A to become Maxar Space, which was a popular teaser target before it was taken private in 2020 and brought back under Canadian control, then turned around and IPO’d quickly in Canada in 2021, followed by another IPO and equity raise in March of this year in the US. Their “mass produce satellites” ambition is much more recent, so it’s hard to say it’s a “founders” thing, but perhaps that’s just hyperbole from Brown.

If we go by recent prices, then MDA is a much better match, it has traded below $25 within just the past month (it’s closer to $32 at the moment)… but there’s also a possibility that Jeff Brown is re-promoting Rocket Lab using the same language he was using last year, since Rocket Lab was in that $25 neighborhood as recently as… well, about 11 months ago. Still, not sure how we can jibe the $25/share tease with the 52% growth tease, since by the time RKLB reported 52% growth it was firmly into the $40s.

So… we can’t be certain about this one — numbers are a better match for MDA, “vibes” perhaps a better match for Rocket Lab. Our best answer right now is MDA Space, but I’ll take the unusual step of putting both into our teaser search system for tracking purposes, and will update that in the future if we get additional clarity.

When it comes to valuation, Rocket Lab is much tougher for most investors to swallow — RKLB is expected to roughly double revenues from 2026 to 2028, but also currently trades at about 30X expected 2028 sales (80X trailing sales). They expect to report a profit in 2027, but it won’t be meaningful anytime soon. This stock looks appealing only in comparison to SpaceX, or if you just buy into the idea that Rocket Lab will dominate space a decade from now with their satellite manufacturing and launch capacity, which is expected to be second only to SpaceX, so we should ignore valuations for now. I wrote quite a bit about Rocket Lab when Tom Gardner at the Motley Fool was pitching the stock as a high conviction buy in March.

MDA Space is much more of a legacy contractor in space projects, and has a much more mundane-looking valuation — they trade at about 30X forward earnings, and are expected to grow earnings by about 30% between 2026 and 2028 (total, not annually). It’s a little hard to imagine this one being sexy enough to get the “10X” treatment from Jeff Brown, but not impossible… sentiment can change quickly when investors get their claws into a new favorite story stock.

And there’s a second stock as well…

“You’ll also receive a brand new report on the company that manufactures all the critical hardware and systems that Google and Amazon will need as they race to catch up to SpaceX and launch their own AI satellites. You can buy shares for just around $10 for now, but Jeff expects that to change very quickly in just the next few weeks.”

So this is more about building parts and components for all these “orbital AI” satellites…

“SpaceX builds about 85% of its own parts for everything that it makes. But Google and Amazon don’t have the engineering expertise that Elon developed building Tesla and SpaceX. That means they will have to source their hardware from another company. And given how far behind both Amazon and Google are, they will need to launch a lot of rockets quickly to try and catch up. And that means they’ll need to buy a lot more hardware. So, luckily for us, there is one company positioned to supply a large portion of the specialized hardware that Amazon and Google will need for their satellites and orbital infrastructure….

“This is my second favorite idea to make gains in 2026 as SpaceX IPOs and the market wakes up to the massive potential for AI chips in space. But the company is still tiny…. it’s about 1,000th the size of the smallest Mag7 stock, yet it literally holds the key that lets companies like Amazon and Google realize their ambitions.”

And some specifics about what this company builds:

“… specialized hardware that enables spacecraft to generate power, navigate in space, communicate with Earth, and deploy instruments once they reach orbit. Everything from power systems to star trackers, which allows spacecraft to determine their precise orientation in space, to control systems and hardware to integrate the spacecraft’s subsystems.

“Keep in mind, even though SpaceX has lowered cost to orbit by a factor of 100x, space missions are extremely complex, and yes, they are expensive. So, proven flight-tested components are the safest choice for new projects. And the company that I’m talking about has incredible pedigree. Its hardware is used by NASA, the United States Space Force, companies like Boeing, Blue Origin, and many more. And the company has already established a meaningful presence across a number of high-profile space missions. And like the Tesla of spacecrafts, the market is valuing this company like a small-cap terrestrial manufacturing company. It does not trade at an elevated valuation multiple, like most space companies do today.

“It grew revenue last year by 56%. But I have to say, if a company like Amazon, Google, or Relativity Space announces a big deal with it, there is no telling how high the stock could run. Now, I expect at least one major deal announced within the next six months. And if that happens, this could easily be another 10X recommendation. So, you want to make sure that you’re in it before that. Right now, you can get shares for less than $10.”

So that one, sez the Thinkolator, is almost certainly Redwire (RDW), which did indeed report 56% growth last time they reported (though that was for the fourth quarter, not for the full year). And they’re reporting again tonight, after the close, so the story might well change quickly.

The company started out as a private equity rollup in 2020, and grew very quickly with a bunch of smallish acquisitions that led into a SPAC merger to take them public during the SPAC boom, but, like so many SPACs, had a rough go for a few years after that as the financials failed to keep up with the story. They are still unprofitable, but they have also steadied things somewhat, including with another acquisition, and they are growing the top line pretty fast (40% this year, 20% next year, roughly speaking), and expected to get to roughly break-even at some point this year (not “profit,” to be clear, but positive cash flow so they can perhaps stop burning cash).

So I don’t know if it’s “cheap,” but almost everything looks cheap compared to companies like SpaceX — even RocketLab looks like a bargain compared to SpaceX, using any kind of current or near-future financial measures, and RedWire, though the growth is much slower, trades for probably less than 4X 2026 revenue, so that looks like a bargain compared to RocketLab or most of the better-known space companies (50X 2026 revenue estimates).

Redwire has also been diversifying the business over the past year or so, particularly with the acquisition of the drone company Edge Autonomy, which has led to a lot more contract and revenue growth on the defense side than on the space side recently — as of last quarter, about half the revenue comes from defense tech, half from space work, but their space work does include some relevant specialties in power, docking and communication, and low earth orbit satellites, so that fits with Brown’s vision of major space data center expansion.

This one is not a clean rapid-growth startup story, mostly just because of a complicated balance sheet that they’ve been cleaning up, with a bunch of old convertible debt and preferreds that they’ve been selling down… but it is looking better than it did when I last looked at the stock a couple years ago, they have a growing customer base and some capacity to increase their workload both for drone manufacturing and for new satellite projects. I don’t know if they’ll get big orders from any of the commercial space competitors or hopefuls to raise their profile, but it’s possible, and it might not take much to light a fire under the stock as everyone drools over the SpaceX IPO and looks for the next space story that hasn’t had a wild run yet.

And given how closely the Redwire story matches up, including the current share price, I suspect that makes it a little more likely that Brown is pitching MDA Space for that “$25” stock, not the “hasn’t been at $25 in close to a year” Rocket Lab.

So… as we head into more SpaceX excitement, and wait for the S-1 registration filing and the investor roadshow leading up to the SpaceX IPO, it comes down to where do you want your money? Trying to ride along with the enthusiasm directly in a fund that owns SpaceX shares, or a company like Echostar (SATS) that primarily exists to (eventually) own SpaceX shares? Buying into “next SpaceX” stories like Rocket Lab (RKLB) that are already extremely poular and richly valued? Or perhaps investing further down the food chain with some space “picks and shovels” companies that do contract work for governments and commercial space projects, like MDA Space (MDA) or Redwire (RDW)? Have a fondness for others that we haven’t mentioned, or better matches for those clues than the Thinkolator was able to provide?

Or, of course, you can also sit back, watch the crazy IPO unfold, and see if any bargains emerge when the first bit of bad news comes out, in the years between the spark of imagination and the actual testing and buildout of any potential future “data centers in space” business. That’s mostly what I’m doing so far, but I’m not always all that fun. Let us know what you’re thinking with a comment below… thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of NVIDIA, Alphabet and Amazon. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Hi Travis. Thanks for revealing this Marc Chaikin related teaser.

Speaking of Chaikin, can you or anyone else on this board please figure out the annoying teaser commercial that Chaikin and the options guy Jon Najarian are running every day on CNBC? The teaser says that Chaikin reveals “the one stock that should be bought immediately.”

The commercial also has a web link http://www.answermarc100.com I see this every day so perhaps you’ve seen it also. Thanks in advance for your time!

Hi Travis, In your Irregulars member summary writeup you have the stock symbol for Redwire wrong. It is RDW not RDWR for Radware LTD. I do own RDW from Brown. I hope this helps. Thank you.

Right you are, sorry about that. Fixed above.

I watched the looong video on this. I fell asleep once! Maybe you did, too.

At the very end, after well over an hour, they named SATS. I don’t think I dreamed it.

SATS shares rose for a few days after, then fell back. I filled yesterday. Today, it was up over $8/share.

Thanks Dagmar. I just wanted to confirm that you’re talking about the Chaikin/Najarian video advertised on CNBC, not the Chaikin/Jeff Brown teaser that Travis has addressed in this post. Thanks!