This pitch is essentially a tacked-on update to a promotion that Garret Goggin and Porter Stansberry ran back in January, so the meat of the promo is royalties-update/">unchanged from what I covered then, hinting at the same stocks and the same basic idea (“buy gold royalty companies”), but Goggin also throws in a new “microcap” recommendation in his update that we can check on… and we should also update our thinking about those gold royalty companies, given all that has changed in the last six months, including some M&A in the space as well as the big rise and fall in the gold price during that time.

So let’s dig in.

Here’s how Goggin introduces this update:

“The last time we spoke about the gold markets, we said we expected our thesis to play out over the next couple of years, but something just snapped and it changes everything. I reckon this event just compressed our timeline by at least three years. It means all of this is happening now, and you should act immediately or risk being left behind as gold prepares to make its next explosive move higher.”

That’s a reference to the fact that the Iran War has accelerated the transition away from full reliance on the “petrodollar,” which has been fading for a couple years now (mostly because the Saudis are willing to sell some oil in other currencies, though the vast majority of oil is still transacted in US$), and the ongoing move by foreign central banks to commit a little less to US Treasuries and a little more to gold in recent years, which is either symptom of or cause of the dollar’s ongoing decline, depending on who you ask.

And then Goggin drops hints about his new recommendation:

“… the trades we call the single best way to profit from the dollar decline, they’ve all been turbocharged by all this….

“There’s a bigger part to the story that I bet you and your subscribers have never heard about.

“This angle is not a gold play. It’s a totally different category of investment, and it’s the kind that only shows up once in a generation. All the chaos in the Persian Gulf, the petrodollar dying, the smart money rotating, has blown the doors open to a new asymmetric opportunity.”

It’s a little strange to hear Goggin talk up anything other than gold, so that perked up my ears — what does he mean?

“All the chaos in the Persian Gulf, the petrodollar dying, the smart money rotating, has blown the doors open to a new asymmetric opportunity.

“Specifically, it’s exposed how broken the legacy financial exchange architecture really is, and it’s created an opening for something brand new… while every legacy exchange on Earth was closed during Operation Epic Fury weekend, this new platform stayed open….

“In the two weeks that followed, oil futures trading this platform exploded by nearly 250 times. By mid-March, they were clearing more than a billion dollars a day in oil contract volume, picking near 1.7 billion in a single trading day.”

OK, so it’s one of the 24/7 “exchanges” that are built on blockchain and have “tokenized” stuff like oil futures contracts. Other clues?

“… the operation’s tiny. 11 people run the entire thing. And those 11 people generated more than $700 million in revenue over the past 12 months….

“If I’m right, It could potentially deliver the kind of multi-year return that took Coinbase from startup to $100 billion valuation.

“… the catalyst is volume continuing to compound as the chaos in the world continues to accelerate in the need for 24-7, 365 trading compounds. Meanwhile, this company’s still small, unknown, needs only a dozen employees, and I think it’s going to be the best recommendation in my career.”

So that’s almost certainly Hyperliquid (HYPE), which is indeed a 24/7 exchange for tokenized trading of non-crypto assets, like gold and oil futures. And it has greater trading volume in recent months, as speculators try to profit from weekend news out of the Persian Gulf, at times when the main futures exchanges are closed.

And yes, Hyperliquid is available and easy to trade on the major crypto exchanges, so you’ll find it on Coinbase or just about anywhere else… and it’s pretty big, with a market cap of about $16 billion (so by that measure it slips into the top ten cryptocurrencies right now, just above Dogecoin).

But it’s also available in a few different ETF wrappers, so you can also buy HYPE indirectly, through the ETFs 21Shares Hyperliquid ETF (THYP), Bitwise Hyperliquid ETF (BHYP), and Grayscale Hyperliquid Staking ETF (HYPG).

And you can get a little crazier than that if you like, there’s also a “crypto treasury” stock called Hyperliquid Strategies (PURR), which trades at a larger premium to the NAV right now but might be more actively managed… and there’s a levered ETF, too, 21Shares 2x Long HYPE ETF (TXXH). PURR attracts a bit of attention because I believe it’s still the only one of these single-crypto Hyperliquid funds/stocks/ETFs to have option trading available.

Who knows, by now we might have even more ETFs — a few minutes has passed since I checked, and new ETFs are spawning like mayflies these days (we’ll find out if they die as quickly — there are now more ETFs trading in the US than there are listed stocks, and a lot of them don’t last long).

But for now, Bitwise Hyperliquid (BHYP) is the biggest and most liquid of these ETFs, even though THYP was introduced slightly earlier, and it’s also the cheapest, thanks to a management fee waiver — though they’re all relatively low-cost ETFs, and Grayscale Hyperliquid Staking ETF (HYPG), the newest and smallest entrant, has the lowest permanent gross management fee, at least for now (0.35%).

I can see the temptation of Hyperliquid, the promise of blockchain has long been that it will allow for easy “tokenization” of everything, and make everything tradeable with much less friction than the big futures, options and stock exchanges. I don’t necessarily think 24/7 trading of everything is the best plan for sanity and rational thought, right now a lot of it is folks trying to gamble and/or sneak in some profitable trades when volume is low on weekends and the price can jump around a lot.

The big question is whether a real long-term leader will arise, and whether it will be able to beat out the incumbents, the big futures and stock exchanges who have been the gatekeepers to the financial markets for generations. They clearly hear the hoofprints coming behind them, and in some cases are pushing for the legacy markets to open up to more overnight and weekend trading, and they’re also opening up a lot of trading in private companies, to feed the demand for “pre-IPO shares” of the hot expected IPOs like SpaceX, Anthropic and OpenAI.

The “disruption” potential of the tokenization platforms like Hyperliquid is clearly very high, and they are attracting a lot of trading volume, though this is all quite new and I don’t have a sense of whether Hyperliquid or any of the other “tokenization/new exchange” upstarts can carve out a sustainable business. Seems like a fun speculation, but I don’t have a good enough handle on this to put money at risk — particularly given how much it bounces around… indications today are that HYPE is falling because of either profit-taking or some more “unlock” of new tokens, so if you’re excited about the opportunity in Hyperliquid, it is at least a bit cheaper today than it was a few days ago.

The longer sales pitch is unchanged, after that new introduction and the new pitch of Hyperliquid… and what they’re selling is still Goggin’s Golden Portfolio (still being sold this time in a package with Golden Portfolio IV, his smaller gold stock service, for $2,000/yr, 30-day partial refund policy after 25% “test drive fee”). What he mostly talks up is the “Gold Royalty Retirement Portfolio,” which is the heart of the Golden Portfolio service and, he says, includes 17 royalty stocks.

Which means, if you’ve counted the lines in our own spreadsheet of Gold Royalty Companies, that Goggin is recommending pretty much all of the viable gold royalty stocks. I only have 20 of them on my radar, several of which are tiny and/or pre-revenue, and that number is destined to shrink by two because of ongoing M&A activity (two of these firms are in the process of merging with or being acquired by other companies on the list).

But first, let me share my notes from this “presentation” by Goggin and Stansberry — some of this is direct quotes, some might be a little off:

“Better way to buy gold.

“Has outperformed every other asset class for the last 18 years. Including gold mining stocks, coins, Nasdaq, Mag 7, everything.

Goggin has “A highly-coveted list of more than 17 gold royalty stocks, these are the little-known royalty companies that compound year after year – and could deliver staggering returns as gold marches higher.”

You want capital efficiency — you want companies that don’t require lots of capital to fund their growth.

This kind of gold stock is the most capital efficient business in the world. The better the business, the better the returns.

Companies like this have compounded at 35.6% for 18 years. (Presumably a reference to Franco-Nevada, everyone’s favorite pioneer in this space)

They trade US Dollars that are guaranteed to be worth less, for streams of gold that are guaranteed to be worth more. A “can’t lose proposition.”

That’s not true, of course, there are no “can’t lose” propositions — gold is not guaranteed to rise in value versus the dollar, even though it’s extremely likely that it will do so over long periods of time (it has done so since the end of the gold standard in the 1970s, but there have also been multi-year periods when gold has failed to rise against the dollar and has fallen in value, sometimes dramatically).

If you are 100% certain that gold will go up in dollar terms, and that your particular royalty company doesn’t really screw up in some shocking way and isn’t fraudulent, then yes, it’s “can’t lose” — but you probably shouldn’t be 100% sure about anything in the financial markets, stuff that has never happened before happens all the time.

Do they name any of the royalty companies? Porter reiterated that his number one is Franco-Nevada (FNV), which is of course the most popular and best-known gold royalty company, and has outperformed gold by ~1,000% since it went public (again) in 2007 (it has been around since the mid-1980s, but was owned by Newmont from 2002-2007).

And although he didn’t mention it this time around, we also know that Porter has been recommending Versamet (VMET) as a “next Franco-Nevada” more recently, in his “Trump’s New Dollar” ads.

More notes:

Regarding FNV: “This is the 800-lb gorilla, but there are other royalties with greater upside potential.”

Mining is about the worst business you can imagine, the opposite of a capital-efficient business.

Gold royalties don’t lose value to inflation, they compound in value thanks to inflation. Best investment on earth during times of a changing financial order, like we have today.

Porter thinks gold will go to $6,000 by 2028.

Gold royalty retirement portfolio, basket of world-class royalty companies you can hold for decades.

And Goggin does hint at one company:

Company O “one of my favorite royalties”

If you bought it instead of bullion in 2024, 410% vs. 100% for physical gold.

That one got bought out, so this is Orogen Royalties (OGN.V, OGNNF) again… and yes, by staking what is now called the Arthur Gold project, in cooperation with Altius Minerals, they turned $100,000 into $250 million when they sold that royalty to Triple Flag Precious Metals (TFPM). For what it’s worth, Altius also sold 2/3 of their royalty on that project last year, to Franco-Nevada.

It’s a compelling project, but Orogen Royalties no longer owns a piece of Arthur Gold, it is now the left over stub after their core asset was sold, so OGN has a little cash flow from their one producing royalty, but to me it is far less interesting overall, without much in the way of meaningful new royalties that could come online within the next few years.

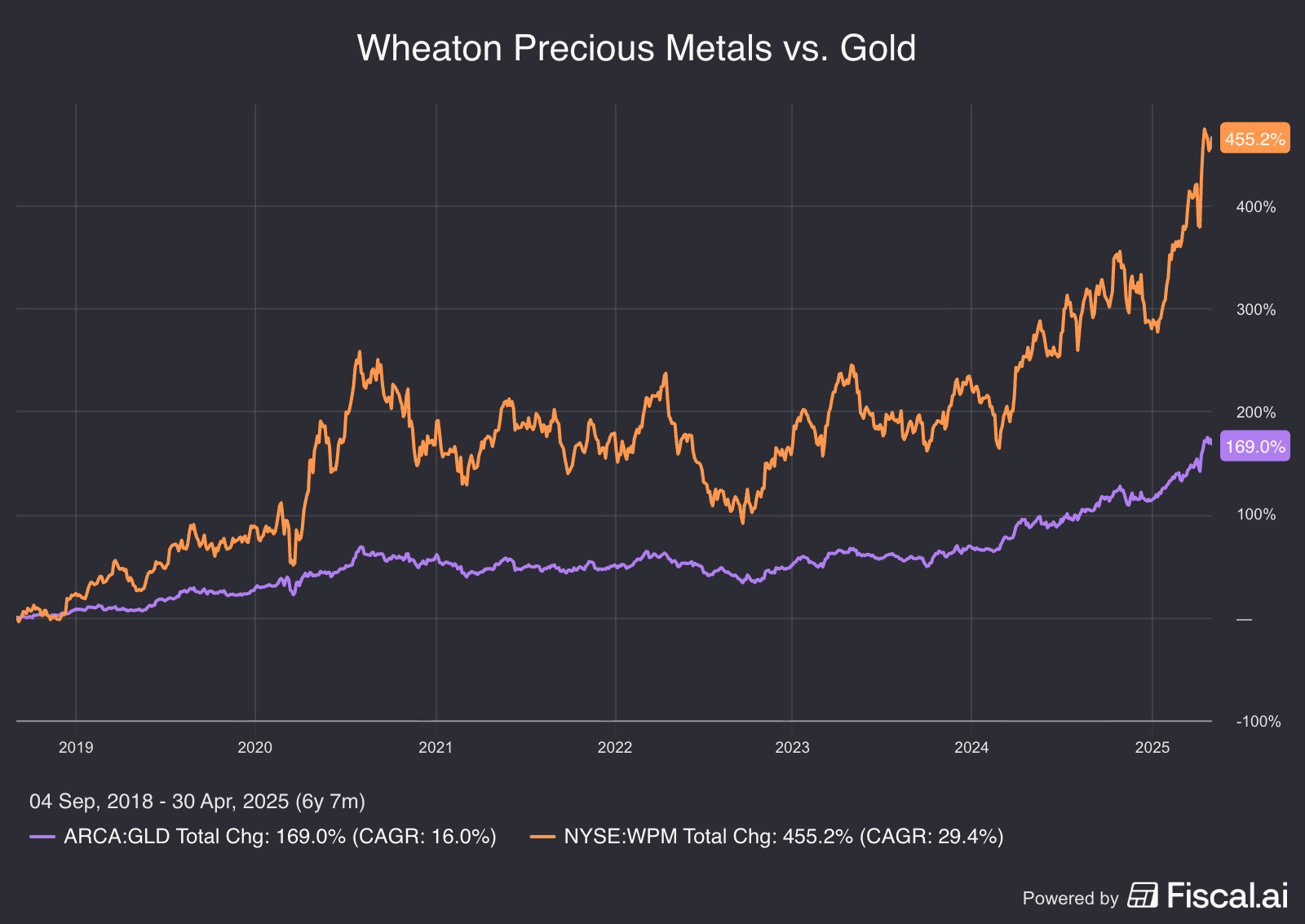

And what are Goggin’s other pitches? He does toss in a couple other unlabeled charts to show the performance of some of his favorites in this business, so we can try to name those for you, though he doesn’t drop any other clues about players beyond little Orogen.

Here’s the first one:

And the best match we can find for that 2018-2025 period, with roughly a 500% gain while gold is up about 150% (the chart is not super precise, and we might not have the start and end points exactly right), is the biggest royalty company, which means he likes Wheaton Precious Metals (WPM).

Wheaton has been a great performer for a long time, and has gradually become more gold-driven after starting out life as a silver streamer, buying up the silver portion of mines for pennies on the dollar in the early days… but it is still the most silver-driven of the major royalty companies, they’re about 60/40 gold/silver these days, so with silver usually more volatile than gold, and certainly outperforming gold as we rolled into the highs earlier this year, we might end up seeing a bit of a boost for WPM revenue.

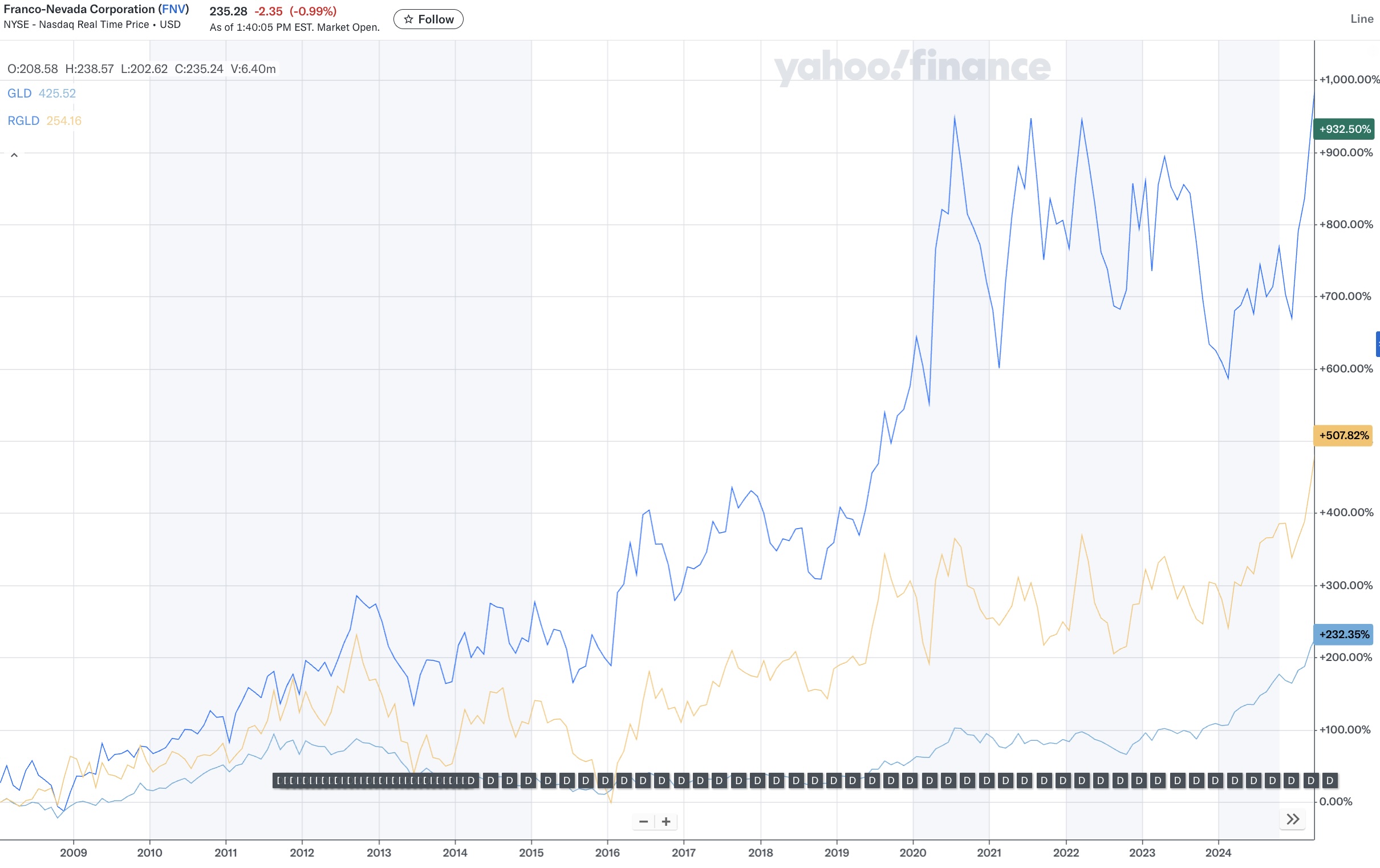

And the other mystery chart?

That one goes back to about 2008, which cuts into the available list of companies pretty dramatically — and that means we’re pretty much choosing between Franco-Nevada (FNV) and Royal Gold (RGLD). Here’s the chart for both of those for roughly that time period:

So yes, it seems like that unnamed “Royalty Company 3” is really just Franco-Nevada, despite the fact that they talked about that particular stock for most of the presentation.

Hard to argue with those two leading firms in this space, but they’re also the two largest of the precious metals royalty firms, by far, so we’re not exactly sharing secrets here. And they’re falling back to reasonable prices these days, at least relative to expected cash flow over the next couple years — but they’re still pricier than many of their peers.

What, then, is an investor to do? I think we buy solid cash-flowing and diversified royalty companies with the intention of holding them through whatever the gold price cycles might be in the years ahead, and we look to buy more when good companies trade at a good value, either relative to their peers or relative to the growth in “ounces” that we see coming.

A little history of these kinds of companies…

The world of precious metals royalties has exploded over the past 40 years, ever since the pioneers bought/created their first royalties in the mid-1980s.

Franco-Nevada (FNV) bought into what became the Goldstrike Mine in 1986 for $2 million, a mine that’s been the heart of the prolific Carlin Trend for decades… and though they’ve also paid to buy neighboring and supplemental royalties on that same mine, they’re still getting more than $20 million in royalties every year from that project, and have now taken in more than $1 billion in royalty payments from that one mine (and their royalties on Goldstrike are probably still worth close to a billion dollars, given expectations of continuing production).

Franco-Nevada founder Pierre Lassonde looks like a genius now, and is credited with inventing the precious metals royalty business, but he had no idea in 1986 that Goldstrike would become one of the largest mines in the world — he just borrowed the royalty financing model from the oil & gas business, and took a chance on a project that looked like it would probably work out as a small near-term producer. It just turned out that small operation had one of the biggest gold deposits in the world sitting underneath it.

Similarly, Royal Gold (RGLD) bought their first royalty on the nearby Cortez Pipeline complex about a year later, in 1987, after they had spent a few years trying to be an oil company but been destroyed by the oil crash in the early 1980s, and briefly thought of becoming an actual miner before wising up. That mine took longer to get built, it didn’t start generating royalties until 1995… but Royal Gold has now earned close to $500 million in royalties from that initial investment, and it continues to produce (like FNV, they’ve also paid much more to buy other royalties that are either overlapping or nearby, keeping up with the mine’s expansion and the discovery of neighboring deposits). We don’t know what the real cost of that 1987 acquisition was, it was a little more complex than Franco-Nevada’s initial purchase of their first royalty, but Royal Gold’s market cap in late 1987 was only $29 million, so they certainly couldn’t have paid very much. (Yes, the dollar has lost a lot of value since 1987 — but even in 2026 dollars, $29 million would be the equivalent of about $85 million.)

Franco-Nevada’s investment paid off faster, but both have done exceptionally well from those relatively humble beginnings — and few people really celebrated them or understood the huge potential for more than a decade after those first royalties were purchased, partly because gold prices were moribund for a lot of that time.

But one common theme emerged: Unlike mining companies, who are always hungry for financing and often go bankrupt if their commodity price collapses, diversified royalty companies who are disciplined with cost control can survive long bear markets.

And if you can get a piece of the upside of a business, without having to worry about operating costs or downside or making additional capital investments, then just surviving the inevitable downturns means that your returns over a long period of time can be exceptional. This is just the 15-year total return for the big three, FNV, RGLD and Wheaton Precious Metals (WPM), which includes a bear market for gold and silver from 2012-2015, compared to the S&P 500 (these charts were pulled in January, using the same timeframe as Goggin’s spiel, so they’d look a bit worse now, with all of those stocks coming back down):

But if we skip that bear market and just go back 10 years, all three have been far more impressive than the S&P 500.

This doesn’t match up with the crazy returns cited by Goggin, but that’s because these have been the biggest and highest-profile players in this space for decades. The most extreme returns have come from investing in these companies much earlier on, before they became popular and compounded through up and down markets and grew their portfolios dramatically in the 2000s.

That’s not to say that royalty companies don’t fall in price when gold falls — they definitely do. But the companies don’t generally lose money. They can turtle up, be careful with expenses, and wait for markets to turn, in part because most royalties are perpetual (they last forever, even if the mine doesn’t get built this time around and it ends up being built by some other company 20 years later) — a royalty or streaming company is really a financier, it consists of a few lawyers, geologists, and accountants, for the most part, they don’t need to spend hundreds of millions of dollars on exploration and drilling and mining equipment, they just put up some cash for a share of the top line, and sit back and wait for their returns to come in.

Which doesn’t mean they can’t screw up. They can… and we saw that firsthand with Nolan Watson’s empire-building ambitions at Sandstorm Gold at times over the past decade — the advantage of a royalty company is built over time by patience and top-line exposure, but if, like Sandstorm, you either borrow too much money or issue too many new shares to finance new royalty purchases, and those mines don’t actually get built on time (or at all), investors can lose patience and the cash flowing from whatever royalties are producing ends up being diluted by debt payments and spread among a larger number of shares. Impatience, or big bets on “empire building” acquisitions at high prices, can put a meaningful dent into the magic of compounding royalty returns.

And they can also run into the same problems that might plague any individual mine — a flood, a permitting delay, a tailings dam collapse that closes operations, equipment failure, labor stoppages, even asset seizure, if governments decide to take control of a particular project. We perceive different areas as being at greater risk for those things, either because of shifting politics or because of environmental impact, but those perceptions can also change in a hurry — nobody thought Panama was an especially high-risk country to operate in when Franco-Nevada invested heavily in a big streaming deal to support the development of the Cobre Panama mine, but it also wasn’t a country with a long tradition of mining, and Cobre Panama got shut down by the Panamanian courts after a wave of protests… which meant that ~20% of Franco-Nevada’s cash flow evaporated overnight. For precious metals royalty companies, the solution to that problem is diversification, but most royalty companies have at least some concentration in a handful of projects that are especially important (and some smaller companies only have one or two paying royalties), and closure or permanent damage to those mines can certainly have a major impact on the company’s valuation, especially in the short term.

Royalty owners also really need to balance building a long-tail portfolio of less expensive exploratory projects that might create future growth 10-20 years or more down the line, and paying higher prices to generate cash flow today to reward shareholders and allow the company to continue reinvesting that cash into new royalties. The lesson of Sandstorm’s challenging times is that if you buy into big projects, relative to your company’s size, you better hope they really stay on schedule. You can’t spend 5-10% or more of your market cap on a potentially big royalty that’s early-stage in nature, and might take ten years to come to fruition — that’s a sure way to anger shareholders and earn yourself a discounted valuation.

And the promise, of course, is that for investors who aren’t interested in evaluating specific mining projects and judging the trustworthiness of management in the gold mining sector, which is chock-full of mostly-terrible companies, precious metals royalty companies represent the only real “buy and hold” diversified strategy if you want equity returns that are levered to gold prices. The average mine is a terrible business, capital-intensive and subject to many forces beyond its control, and therefore the mining ETFs tend to be pretty terrible, too. The average mining royalty business, though upside depends on commodity prices, is, relative to just about any mine operator, a great business, and that means it should be easy to buy them when they trade at rational valuations.

You do give up the stratospheric short-term returns if you stick with diversified royalty companies, they don’t have sudden discoveries that send the stock soaring by 1,000%, as sometimes happens with junior miners, and they’re not quite as levered to rising gold prices as a good producing miner can be… but the mining business is so terrible that buying into it through royalty companies gives you a huge advantage over time, mostly because there’s a lot less need for capital and a lot less downside risk during times of weaker commodity pricing.

Here’s how Royal Gold has done when compared to the gold price itself and to the average gold miner over the past 20 years (miners represented by the GDX ETF, gold by the GLD ETF, S&P 500 by SPY) — you got most of the upside of the stock market, plus some excess during boom times for gold, and you are reminded of how tough the actual mining business is (this one is updated, so it’s the past 20 years through today — which means you can see the downturn in gold and RGLD over the past few months, too):

So that’s why we buy royalty companies — any business where you can get a share of the top line (revenues or ounces sold), without having to pay a share of capital costs or operating costs, is a good business.

And on top of that, gold royalty companies should get double leverage — they are exposed both to the rising price (if it rises) of the underlying commodity, and to the likelihood that most mines, once they’re in operation, will become much larger and produce for longer than originally estimated (miners are incentivized to drill enough to justify building a mine, but not more… so additional exploration and mine expansion often happens years into production, once they’re incentivized to expand their reserves to extend the mine life).

And usually, gold offers a good ballast to the stock market — we’re seeing that right now, with correlation pretty low as gold has fallen in recent months and the S&P 500 has hit new highs again. That’s somewhat reassuring, actually, because for a lot of last year gold and the S&P 500 were just going up in lockstep, and that felt wrong. Usually, if gold is soaring it’s because investors are terrified of everything else, but the dynamic has been a bit different during these past few years of inflation, US dollar weaponization, war, and balloonoing deficits.

So… which of the royalty companies look good now? Well, the Irregulars know my favorites, and I write about them pretty regularly, but this is the list of the dozen largest precious metals royalty firms, with their basic info and valuation today (using cash flow from operations as our yardstick):

The Irregulars have access to our more thorough and updated Royalty Company Data page, with all of the stocks and with live prices and new data added pretty regularly, and with my own growth-adjusted valuation metrics that I think make comparison easier… and I updated that page earlier today. But that table above shows the basic valuation picture right now.

Anything stand out for you?

I’d say that Royal Gold (RGLD) remains the best combination of value and growth among the large royalty firms, and this does also highlight that growth expectations for Triple Flag Precious Metals (TFPM) are relatively low over the next couple years, particularly as they wait for Arthur Gold to start construction, so investors aren’t currently willing to pay up much for that growth.

But much of this is subjective, and depends on an assessment of a company’s portfolio, their historic performance, and the “ounces” growth they’re likely to see from their mining partners in the future — over the very long term we’ve seen very similar performance from the largest players, with Royal Gold and Franco-Nevada each growing their cash flow from operations at similar rates since 2008 (average of 16%/year for FNV, 17% for RGLD), but FNV has gradually grown to trade at a higher multiple to that cash flow than its near-peer RGLD. Part of my argument is that I think valuations will normalize, and I think it’s rational for WPM, RGLD and FNV to all trade at pretty similar price/CFO multiples much of the time, given their similar size, diversification, and growth potential… but I don’t know whether the market will choose to agree with me on that point, or will continue to pay a bigger premium for the “blue chip” name in the sector. We’ll see.

But that’s just what I think, and I own a lot of these stocks… and probably will own them in perpetuity, I don’t know whether gold will keep falling this year, or will rise up and hit new highs in the next year or two (Porter’s Austrian model predicts gold hitting $6,000 in 2028, for whatever that’s worth), but I know that the diversified royalty companies are the safest way to have gold exposure in an equity portfolio, and I want to have gold exposure. If gold does well, the royalty companies will almost certainly do better. If gold does poorly, the royalty companies will fall… but will fall a lot less than the mining companies, most likely.

Have a favorite? Avoiding gold entirely? Any interest in that Hyperliquid story? Let us know with a comment below… thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of and/or call options on Wheaton Precious Metals, Franco-Nevada, Royal Gold, OR Royalties, Triple Flag Precious Metals, Versamet Royalties, Elemental Royalty, and Vox Royalty. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

The HYPEs seem like the flurry of coins of different flavors that followed in the wake of Bitcoin, 90% of which failed.

I understand why, in the short term, that gold goes down in the short term as interest rates rise. But it seems like some account should be given to why interest rates are rising. If its because inflation is out of control, the decline in the value of the dollar should push gold prices higher.

I agree, but that’s not how it usually works in the short term. We’ll see if the sentiment shifts again, but I expect gold to do well over the next decade as the impact of deficits and excessive spending eventually have an impact on confidence in the dollar. Could certainly crash along the way, though, too.

What is trump 2 dollar stock jim Richard is talking about??

Covered that “Trump Secret $2 Gold Mine” pitch here… might be that Trump, Jr.’s fishing hobby sinks that one for good someday, but never say never.

Thank you, again. Very insightful as always. I appreciate your work and your writing.