We first covered this teaser ad back in November, when gold was lingering around $4,000 an ounce, but we’re taking another look today as he pushes the “overnight mandate” aspect of this potential gainer, and particularly as he updates the important date from January 19, which was his initial “big gold reset” date, to April 13.

The ad has now been updated again, with July 4 the new “reset” date, and with some slightly different verbiage… I’ve updated the Quick Take above, but other than that what follows has not been updated since April, so you can slip in “July 4” in place of “April 13” throughout if you want to get yourself excited about near-term catalysts.

Here’s the lead-in for the latest version of the pitch:

“With a single stroke of the pen…

“The April 13 “Overnight Mandate” That Could Create A New Class Of Millionaires

“A rare $1 gold document could soar 3,400% the moment this mandate takes effect… giving anyone the chance to secure a lifetime of wealth in a single day”

So this is a two-part ad from Hodge, the big January 19 April 13 reset that he thinks is coming… and his favorite way to play that, with something called “Gold Scripts.”

Here’s how they sum it up on the order form for his Foundational Profits ($199 first year, renews at $249/yr, 30-day refund period):

“Gold is about to do something it’s only done twice before in the last 100 years.

“And when it does, Gold Scripts won’t just double or triple…

“They could deliver gains of 10x, 20x, even 50x.

“The kind of gains that turn $10,000 into $500,000.

“Or $50,000 into $2.5 million.

“And it could all kick off as early as April 13th – when insiders believe an emergency monetary summit could send gold to $15,000 per ounce.

“If gold reaches $15,000…

“And Gold Script companies can still buy at an 80% discount per ounce…

“They’d be making over $12,000 per ounce in pure profit.

“The stock prices would go absolutely ballistic..”

So shall we dig in and explain what he’s pitching? First, that “January 19” bit about gold soaring…

“The national debt has skyrocketed to an unsustainable $37 trillion.

“Currency wars are intensifying.

“Geopolitical tensions are at the highest level possibly since the Cold War.

“All this instability adds to the mounting pressure undergirding gold’s price.

“And as if that wasn’t enough…

“There is one more catalyst that could not only light the fuse… It could send gold to heights that don’t even seem possible.”

What’s that “catalyst?” A reset of gold…

“$20 trillion of that debt matures in the next decade at much higher interest rates.

“The interest payments alone could bankrupt the country….

“But there’s a solution.

“The U.S. government holds 8,133 tons of gold.

“Right now, it’s valued on their books at just $42.22 per ounce.

“That’s the official price set in the 1970s.

“If they revalue that gold to $15,000 per ounce…

“They’d instantly create $3.9 trillion in assets.

“Enough to pay down a huge chunk of the debt without printing a single dollar.”

How would that pay down the debt, you ask? It wouldn’t, of course, not unless you could sell the gold for $15,000/oz, and that would both be strategically questionable and hard to pull of, with market prices right now around 4,600/oz…. but it would possibly allow for an accounting reset, and allow the government to keep kicking the can down the road for another year, without making any hard decisions about raising taxes or cutting spending.

It’s kind of like the theoretical “trillion-dollar coin” that was talked up a few times as a way to do an ‘end around’ of the debt ceiling and create new money, by minting a trillion-dollar coin and sending it to the Federal Reserve to sit on their balance sheet and justify printing more dollars.

Let’s riff on that for a moment… but if you’re already bored and if you just want the “Gold Scripts” answer, scroll down and skip the next few paragraphs…

A balance sheet has two sides, liabilities and assets, and yes, the government could decide to “revalue” the gold that’s in Fort Knox and elsewhere in government vaults, setting a new “official” price and therefore creating a one-time paper windfall that could be used to cover perhaps a year’s worth of more budget deficits. It’s a little bit like when a company’s assets rise in value by a billion dollars on the balance sheet, and then they have to count that billion dollars of appreciation as a “profit” on their income statement that year — no new cash changed hands, but current accounting standards call it a profit and it therefore can give the current year an “income” boost.

How does that work? The U.S. Treasury owns approximately 261.5 million ounces of gold, and it is still valued on the books at the official price, which was $42.22 per ounce at the point when the U.S. fully dropped the gold standard in 1971. It has never been updated since then, probably mostly because the idea of an “official” price stopped meaning anything — during the time we were on a full gold standard, from the 1860s to 1933, anyone could redeem their paper money for gold at the official price, which was $20.67 in 1933, and when gold was seized from U.S. citizens and the redemption option ended in that year, FDR reset the gold price to $35 in 1934, creating a one-time windfall to help cover the costs of the Great Depression and the expansion of government coming out of that (Why seize the gold? Because the dollar was backed by gold, he couldn’t just call up the Federal Reserve and yell at them to do “quantitative easing” or something — the only way to get some inflation, to give them room to boost spending, was by resetting the price of gold).

After that, we remained technically on the gold standard until 1971, because the U.S., under the Bretton Woods agreement after World War II that reset and fixed global exchange rates, guaranteed to redeem U.S. dollars held by foreign central banks for gold, which is what held the Bretton Woods system of currency controls in place and essentially put the whole world on the “dollar standard,” which was technically also a gold standard because those dollars could be redeemed for gold. When the U.S. government under President Nixon effectively ran out of money to cover LBJ’s Great Society and the Vietnam War, Nixon “closed the gold window” and stopped offering redemption of dollars for gold to even those foreign central banks, so I believe $42.22 was the last price as which redemption was available in 1971. That number, the official U.S. government gold price, has since been irrelevant, so it hasn’t been updated.

What would happen if it were to be updated? Well, the current official value of the Treasury’s gold is $11.04 billion (261.5 million ounces at $42.22 per ounce). If they reset the value to the current market price, using $4,600 an ounce, then all the gold owned by the U.S. government would be worth roughly $1.2 trillion. That would create a one-time “paper profit” of a little over a trillion dollars. The U.S. government was expecting to spend something more than $7 trillion this fiscal year, which will be roughly $1.9 trillion more than it brings in (from taxes, mostly), so, even if we ignore the massive expense of the ongoing Iran war and whatever comes after that, which was not in the budget but does cost actual cash, that would “cure” the budget deficit for only seven or eight months.

That would be at least reasonably justifiable, and is no less insane than a lot of other government accounting, so it could be a political boon. If voters are fools, and I think we all know a few voters who fit that category, it might even let politicians claim they had cut the deficit for a hot second, maybe long enough to impress voters as we head into the midterm elections.

Sadly, it would not have any impact at all on the accumulated government debt, which since Nick Hodge wrote those words last fall has jumped another two trillion dollars, so it’s about $39 trillion today. The impact would wash away almost instantly, so I would assume that it would only be done during election season, when it might have the most political impact.

But is there anything to be gained, other than a reduction in government credibility, by setting the official price of gold above the current market price? That would mean we’re moving from mainstream (if misleading) accounting to outright fraud if a company did that… but could the government?

I have no idea, but the impact would theoretically be similar if they got away with it — for every roughly $4,000/oz increase in the official price of gold, the U.S. Treasury could “reset” the value of its assets by about $1 trillion. So sure, perhaps they could just make up a new price, say, $20,000/oz, and claim their gold is worth that much, and that would create $5 trillion in one-time “profit” for the government.

To balance out the full U.S. debt, all $39 trillion, they’d have to reset the price of gold to about $152,000 per ounce… or, to put it more honestly, they’d have to reset the dollar from 1/4,000th of an ounce of gold to about 1/152,000th. That would not mean that they suddenly don’t have to pay the $1+ trillion in debt service to bondholders every year… but it would presumably crush the value of the U.S. dollar, so that $1 trillion wouldn’t seem like such a big number. If all other assets inflated at the same artificial rate, to absorb this reset of the dollar, then the median price of a home in the U.S. would jump from $410,000 to about $15.6 million.

So you can see why politicians might be tempted… but can we set off hyperinflation just for the money we repay to our lenders, or does hyperinflation reduce the value of other dollars, too? Only one way to find out for sure, I guess, but I’m not sure I want to.

Yes, it’s all stupid and gimmicky, but U.S. government finances have also been stupid and gimmicky for 50 years, so who’s to say when stupid gets too stupid?

And while the U.S. government is the largest owner of gold in the world, it doesn’t get to decide what anyone else should pay for gold on the open market. So we should acknowledge that “resetting” the gold price to the market price is reasonably sensible, but resetting to something above the current market price is going into tierra incognita. That reset wouldn’t make everyone else agree to pay $15,000 per ounce, or whatever new price might be made up.

As I see it, the only way in which the government can really control the gold price is by controlling the dollar’s value in terms of gold, which they can really only do by going back onto some sort of gold standard, and offering to redeem dollars for gold at a set price again. Folks daydream about that happening someday, and who knows, maybe things will eventually get bad enough that they take that kind of action, presumably after some massive crisis that also includes a full reset of the economy and perhaps a real default on the Treasury’s debt — but at this point, institutions and governments and plenty of citizens are still willing to lend the U.S. government money at a super-low interest rate (4%ish), so there’s no indication that we’re anywhere near that kind of crisis point. Things can sneak up on you, and a crisis can quickly snowball into something more extreme, like we saw in 2008, or back in the 1930s, but if the dollar is going to crash in value, well, it will hurt almost everything. Except, perhaps, US exports.

There is, of course, a crisis brewing — but that has been true for more than 40 years, it was pretty early in Reagan’s presidency that it became almost mathematically impossible for the U.S. to ever repay its debt, and the only way to keep spending more than we collect is by continuing to borrow more money every year. That math doesn’t work now, and it has never really worked during my lifetime (I’m 55), but despite the fact that it’s clearly unsustainable and makes no sense, and the government obviously can’t afford to ever repay the debt, the ball just keeps rolling. I would guess that there are a bunch of other more obscure levers the government can keep pulling before a real reckoning arrives, probably beginning with a return to quantitative easing to essentially move more of the government’s debt over to the Federal Reserve, depressing interest rates and therefore making it possible to keep paying the debt service and kicking the can further down the road.

But who knows, this is also shaping up to be the most unconventional presidency we’ve ever had, at least in the past 100 years, and there has so far been no very firm check on the President’s executive power by either Congress or the Federal Courts, so perhaps they’ll push the envelope and try something dramatic that surprises us all… maybe that’s some new gold standard that provides a one-time reset, or maybe we’ll even threaten our trading partners into some new Bretton Woods agreement to reset the dollar much lower, which would likely lift the price of gold and other “hard assets” (and, of course, if we don’t see a prolonged recession as a result, also likely lead to even more asset inflation than we’ve seen over the past decade — which will make the gap between “haves” and “have nots” even more extreme, which isn’t good for any society).

Hodge pulls in some other pundits and analysts who also predict a major reset:many

“Many gold insiders are saying $15,000 gold makes sense…

“Geneva-based gold veteran Clive Thompson says $15,000 gold covers this year’s and next year’s deficits plus debt reduction…

“Precious metals analyst Craig Hemke views $15,000 gold as a way to counter China and raise funds…

“Swiss private banker Mario Innecco says $15,000 gold is certain due to increasing debt and geopolitical stress.

“And macroeconomic analyst Luke Gromen sees gold potentially going to $20,000 in order to bring the debt back down to more sustainable levels.

“Some people, like Jim Rickards and Trump friend Robert Kiyosaki, predict an even higher gold price…

“Up to $27,000 an ounce.

“Infamous resource speculator Doug Casey even says $40,000 gold is possible.

“The bottom line here is anyone holding Gold Scripts if and when this happens is going to get RICH.”

And this is what he says about that “April 13” date:

“And it could take off as early as January 19 April 13…

“That’s when insiders believe an emergency “New Bretton Woods” summit could convene.

“Just like the original Bretton Woods conference that reshaped the global financial system after World War II…

“This new summit could announce a complete monetary reset.

“With gold at the center.

“In essence, a new gold standard.

“Some analysts are calling it the ‘red button’ option.

“The nuclear solution to the debt crisis.

“And when it happens — if it happens — gold won’t just rise.

“It will be revalued overnight to $10,000… $15,000… maybe even higher.”

There wa no major financial event or meeting on his originally teased date, January 19, 2026, and there isn’t anything really on top for April 13, either. We probably won’t see the debt ceiling breached again until sometime after the midterm elections, there’s no Fed meeting, and nobody’s really focused on the budget or the deficit right now. I wouldn’t be surprised by a one-time reset later this year to update the “official” gold price to the current market price, which would be just a one-time “rescue” for a few months to give politicians something to talk about on the stump, but I’d sure be surprised by a new gold standard or a “Bretton Woods II” agreement (or even the oft-teased “Mar-a-Lago Agreement”) in January.

Frankly, with a mostly unpopular war raging, and with President Trump feeding volatility and getting distrust and/or pushback from some US allies as the war extends beyond original expectations, it might be hard to do anything at all on the diplomatic front, let alone a coordinated global currency reset.

OK, back to that “gold scripts” push…

But if we take Nick Hodge’s argument at face value, that gold should rise, regardless of the reason or timing… then what should we do with our money? What are those “Gold Scripts?”

“If gold is revalued to $15,000…

“And Gold Script companies can still buy at $400-600 per ounce…

“They’d be making over $14,000 per ounce in pure profit.

“That’s a 2,333% increase in profit margins.

“Overnight.

“The stock prices would go absolutely ballistic.

“We’re not talking about doubling or tripling your money.

“We’re talking about gains

“that could turn $10,000 into $500,000.

“Or $50,000 into $2.5 million.

“From a single announcement.”

And he tries to explain the past big moves in the gold price using this idea of “Stages”:

“First, only early enthusiasts are courageous enough to invest in gold when everyone else thinks it’s dead money.

“That’s stage 1.

“Then, institutional investors – the smart money – jump in.

“That’s stage 2.

“Finally, the public joins the party, triggering a massive explosion in price.

“That’s stage 3.”

And he compares this to those historic moves, to make this seem somehow linear and sensible:

“In the 1930s, during the Great Depression, gold was stuck in stage 1.

“The economy was in ruins.

“Nobody wanted to invest in anything.

“Gold was ignored, left for dead.

“Only the smartest investors were quietly accumulating.

“Then in 1934, something changed.

“President Roosevelt revalued gold from $20.67 to $35 overnight.

“A 69% increase with the stroke of a pen…

“Pushing gold into stage 2.

“Suddenly, institutional investors realized gold’s true value….

“But the biggest and fastest fortunes were made when stage 3 hit.

“The public finally caught on.

“And gold mining stocks went wild.

“Homestake Mining, the largest gold miner of the era, saw its stock price increase over 500%.

“The company went from near bankruptcy to paying massive dividends.”

And we got something similar in the 1970s, with “stage 1” the reset of gold from the $35 official price to the new ~$42 official price and then quickly the abandonment of the official price, which sent gold climbing to $195… but he says the “frenzy” only came in 1979, when gold soared to $800+ — that was not happening in a vacuum, of course, that was during the oil crisis sparked by the Iranian Revolution, when inflation was roaring (following the end of the gold standard, we had double-digit inflation most of the time from 1975-1981, when Paul Volcker as Fed Chair finally killed it with a 19% Fed Funds rate and several years of recession).

So it’s a repeat of this “stage 3” mania for gold that he sees coming again, sparked by some new kind of Bretton Woods agreement… and he thinks we should buy “Gold Script” companies. So I guess we just have to take it on faith that somehow a government reset can turn the market price of gold from $4,600 to $15,000 “overnight” and somehow make that stick… which is really only possible if you do an instant devaluation of the US$.

If that happens, I would expect that pandemonium ensues and all banks and insurance companies, who are usually the biggest domestic holders of Treasury debt, would go bankrupt — but yes, gold stocks would probably do well.

Here’s how he describes the general idea:

“I discovered a new way to profit from rising gold prices.

“One that avoided the operational headaches of mining.

“It started when I began noticing certain companies outperforming everything else during gold booms.

“They weren’t miners. They weren’t selling physical gold.

“They were doing something completely different.

“These companies held special contracts — what I call Gold Scripts.

“And their performance was staggering.

“During the 2001-2011 gold bull market, while miners gained 200%…

“These Gold Script companies soared 1,000%, 2,000%, even 3,400%….

“Because Gold Scripts don’t face the same problems as mining companies.

“They don’t have to dig gold out of the ground…

“They don’t have workers who go on strike…

“They don’t have equipment that breaks down…

“They just collect gold at a fixed price

“and sell it for a massive profit.”

And he gives an example of what they can do:

“One Gold Script company I track has contracts to buy gold at an average price of $470 per ounce.

“Right now, with gold around $3,400, they’re making nearly $3,000 per ounce in pure profit.

“Last year, they bought 300,000 ounces through their Gold Scripts.

“That’s $879 million in profit.

“From contracts that cost them a fraction of that amount.”

So yes, clearly Nick Hodge is talking about the royalty and streaming companies, which most investors in the precious metals space have no doubt heard of… and which have gradually become quite popular in the decades since Pierre Lassonde pioneered the concept with Franco-Nevada (FNV) in the mid-1980s.

I won’t go into the full discourse about mining royalties, I’ve done that plenty of times before (and we’ve got a detailed table of all of the publicly traded royalty and streaming companies for our paid members, including their relative valuations)… but yes, I agree that these companies, who are essentially financiers for gold miners, putting up cash up front in exchange for a share of the gold produced, are the only kind of gold company that it’s reasonable to hold long term, through the up and down cycles of the gold price.

Gold royalty and streaming companies have historically provided excellent returns, mostly because they get double-leverage (they have low operating costs and buy a percent of a mine’s output at fixed prices and/or discounts to the gold price, so they benefit both from rising gold prices, and from the leverage of miners “discovering” more ounces and extending the lives of their mines — many mines end up producing for many decades beyond their initial mining plan, with that original royalty or streaming deal still in place). I went into the concept of royalty investing in much more detail in an article last month, if you’d like more of that discussion.

And now, finally, we get to Hodge’s teased recommendation:

“I’m tracking a Gold Script right now that trades for under $1.

“This single $1 Gold Script could realistically hit $10… $20… maybe even $50 after Trump’s big move.

“That would turn every $10,000 invested into $100,000 or more.

“And that’s being conservative.

“Looking at maximum potential…

“You could start with as little as $1,000 if you want to.

“And if you take a position before the big announcement…

“You could cash out with $50,000 overnight.”

What other clues do we get?

“It checks every single box.

- Low cost basis

- Multiple producing mines

- Experienced management team

- Strong balance sheet

- Perfect timing for Stage 3″

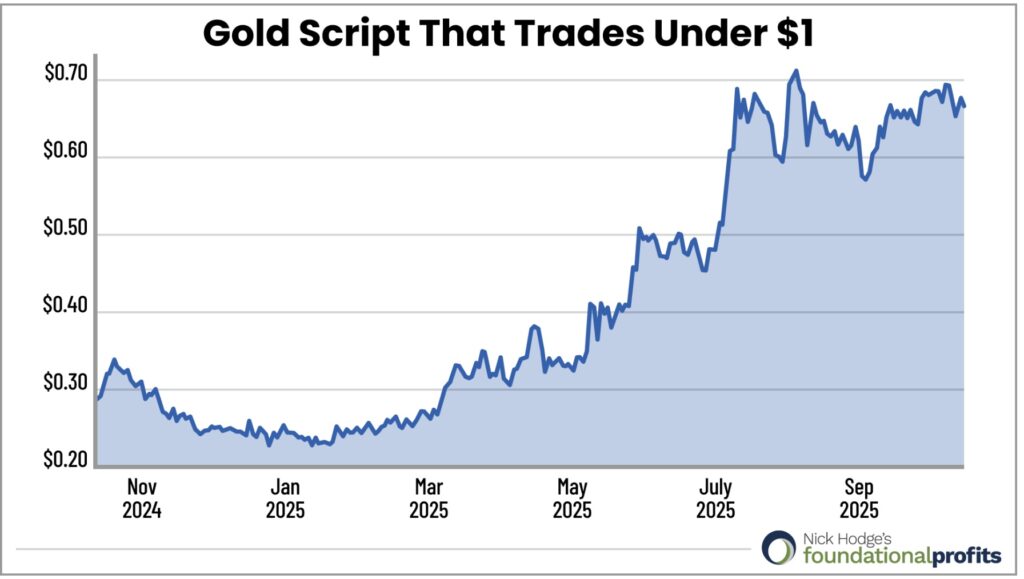

And one final clue… the stock chart. Here’s a screenshot of that from the presentation (you can see it cuts off last Fall, so this part of the ad is unchanged from when we first wrote about it in November):

So who’s that? Thinkolator sez this is (still) Empress Royalty (EMPR.V in Canada, EMPYF OTC in the US), which is one of the smallest gold royalty companies… and I think it’s the smallest publicly traded one that has positive operating cash flow, so that’s notable.

Empress today has a market cap of about $85 million, and it owns active royalties and/or streaming deals on four different mines. Their most productive asset right now, by far, is the Tahuehueto silver stream in Mexico, but they also have pretty consistent and mostly growing production from Sierra Antapite in Peru (gold stream), Manica in Mozambique (gold royalty), and Galaxy in South Africa (gold stream). This is still a very young and small company, the firm was only founded in 2020, so the primary risk is that they only have four producing royalties, which makes each of them critical. The benefit of that small size, though, is that each new royalty can bring pretty tremendous growth in cash flow, especially since they’ve been fortunate enough to have production begin to ramp up at their royalty properties at a time when precious metals prices are high and have been rising.

And there is a little caveat to the “small size,” because they have a partner in Endeavour Financial, an investment banker/advisor to the natural resources industry, which essentially helped to seed the launch of the company (Founder/CEO Alexandra Woodyer Sherron came from Endeavour, and they are a major shareholder and seem also to be a lead-generating partner, helping to steer deals to Empress).

So the numbers today look pretty impressive — Empress Royalty has a market cap of about US$85 million, but generated $3.7 million in cash flow from operations last year… so if those mines are consistent producers and generate rising cash flow for them in future quarters, thanks to the higher metals prices, we can argue that Empress is by far the cheapest of the precious metals royalty companies right now — though it also probably should be the cheapest. Here’s an excerpt of what I wrote about them to the Irregulars after their Q4 earnings report last month:

Empress Royalty (EMPR.V, EMPYF) continues to stand out as a “value” among the other companies in the royalty spreadsheet, but I’ll again note, following earnings a couple weeks ago, that this is a more volatile company than most on the list, and has a lot more adjustments in its financial filings — particularly because by far their most important asset, a stream on the Tahuehueto silver mine in Mexico, which is something like 75% of revenue and cash flow for Empress right now, also generated a lot of adjustments to Empress earnings in the past because the operator, Luca Mining (LUCA.V), fell behind on payments and then caught up in past years… and also pays in silver, so Empress ends up holding a lot of metals at times… and, as you might guess from the wild moves in silver over the past year, the silver has sometimes shifted radically in value between the time they take ownership and the time they sell the metal.

If we combine that volatility with the fact that most of their royalty and streaming deals have a cap over time (maybe to pay out for a decade, or pay out to a set number of ounces), Empress should be cheaper than the more open-ended companies who can sometimes generate strong long-tail returns from assets over decades (indeed, it’s those royalties or streams that pay out over 20, 30 or more years that really generate the most dramatic profit, helping to cover for the royalties on mines which never get built, or which stop production early for any reason). That means Empress also has even more need than most to recycle its capital to invest in new deals, since they don’t last forever — all royalty companies are essentially financiers at heart, but Empress is even more like a merchant bank than most.

So while I track the cash flow for Empress, it doesn’t always mean as much — their accounting is different, and we should probably be more open to just using earnings to judge the value of Empress Royalty, perhaps using something like gross profit (their net streaming revenue) or earnings minus depreciation instead of cash flow from operations. That’s also somewhat risky, since it can obscure the fact that Empress sometimes looks better on a GAAP earnings basis than it does on a net cash flow basis, which feels wrong… but it’s worth considering a somewhat different valuation framework for a different company like this, even as we also remember that they only really have four royalties/streaming deals, and one of them matters a LOT more than the others right now (they announced a “binding term sheet” to buy a fifth royalty last Summer, on the Milford mine in the US, but I can find no further mention of that form the company, so they don’t seem to have followed through on the deal).

So for 2025, gross profit for Empress came in at $7 million, operating profit at $2.8 million, and net income at $7.4 million. Operating profit before depreciation was $4.8 million, and net income before depreciation was $9.4 million, but cash from operating activities was only $3.7 million, thanks to the so-far non-cash nature of some adjustments (especially the change in value of metals received but not yet sold, again, almost entirely that silver from Tahuehueto — that was $3.7 million in the fourth quarter).

I think, frankly, that I’m most comfortable sticking with net income, and paying a reasonably low multiple of net income, knowing that if metals prices stay elevated they will have high earnings this year, and maybe for many years if prices climb, but also remembering that these are not perpetual royalties but last an average of maybe 10 years, most likely (the Tahuehueto stream has a ten year term, so that’s the biggest impediment to longer-term daydreaming — their most valuable asset is about a third of the way through its financial life), and they’ll have to make new deals in this higher-price environment to keep growing and diversifying the base of streaming deals. I am also willing to use just the second half of last year for our income assessment, and annualize that, since I’m willing to assume that silver will stay at least in the $50+ range and gold will stay above $4,000, though neither of those assumptions is, of course, a guarantee.

That would mean the run rate of net income for Empress should be about $6 million a year right now, and more likely to rise from that level than to fall, given my metals price assumptions. Their tax rate was unusually high in the fourth quarter (55%), so we might be too conservative in annualizing those returns, but conservative is OK (the annualized EBITDA would be more like $7.5 million, just FYI). $6 million dividend among 128.3 million shares outstanding gets us just under five cents per share in earnings. There’s one analyst offering up estimates, and they expect nine cents in 2026.

Given the uncertain nature and the heavy reliance on a small portfolio of streaming deals, I’d like to pay less than 15X earnings, which would be $0.75/share for my estimate of real trailing earnings and $1.35 using that one analyst’s estimate for 2026 earnings. There are also at least 22 million potential shares of dilution out there in the form of options and warrants.

So Empress might well do very well, especially if gold and silver prices remain strong — they do have a nice niche in providing customized streaming deals for smaller and shakier counterparties that a lot of big royalty companies would never deign to work with, but my main point here is that Empress looks cheaper for a reason — it’s nimble, it’t got good deal flow, it might work out well, but it’s not the kind of persistent value creation that we see with the bigger portfolios of perpetual royalties on mines with mostly higher-quality operators. I think they’re much less likely to be acquired than the other smaller royalty companies who have assets which would fit more cleanly inside the portfolio of firms like Royal Gold or Franco-Nevada, and they’re also meaningful riskier than some of the other smaller royalty firms I own. It’s also cheaper, so that’s the draw.

So I think Empress Royalty has some potential to add a little spice around the edges of a portfolio of precious metals royalty companies, but it’s more speculative than most and, I should note, if you’re relying on Nick Hodge as a neutral arbiter of the company, that Empress Royalty is also a paid sponsor for Nick Hodge’s company, Resource Stock Digest. My thinking is that even though this is absolutely a biased recommendation from Hodge, and we should never blindly trust the analysis of a company that’s paid for by the company… it’s still an interesting idea as they try to build their portfolio into something diversified and resilient. Mostly because they have real cash flow right now, so we can judge them based on numbers, not on any sponsored analysis.

Since the company is only a few years old, they don’t have the long-tail optionality of hundreds of royalties on properties that might someday become mines… but it’s impressive to have four producing royalties in a portfolio this small, and they have a pretty impressive investor base of not just Endeavour Financial and the Empress founders, but also the Sprott folks, including Rick Rule, which lends them some additional credibility in the resource space.

The big risk is that because they’re very small and have just a few producing royalties, they will not be nearly as resilient as the big royalty companies if there’s a problem with one of their mines or we have a prolonged downturn in the gold price… but the payoff for that risk is that for their size, they’re likely to make a lot of money. From looking at a few of their royalties, there are also likely to be step-downs in royalty production after an initial period, or cutoffs that we don’t always see in royalty deals, which have tended to be perpetual in the past (one recent royalty ends after they’ve gotten a 300% return, for example), so that is likely to hobble future growth, but shouldn’t have a cash flow impact for at least several years… by which time they will presumably have invested that cash flow to build a somewhat larger portfolio of producing deals.

In terms of that “possible fifth royalty,” all I know is that they agreed to buy a 5% gold and silver royalty on the Milford copper mine (for $3 million) — that’s an old copper mine that was restarted about a year ago, and has been expanded. We don’t know how much gold or silver it might produce (it’s not owned by a publicly traded company), but it is an operating mine, so if that deal is finalized they should start to see some revenue quickly. They haven’t mentioned it since, as far as I can tell, so perhaps the deal fell apart before it got “definitive,” or perhaps they’re still negotiating.

They also have one royalty that’s classified as “in development” — that’s on the Pinos project in Mexico, which was recently acquired by a new operator, Goldgroup, and is fully permitted and theoretically ready for construction, but will go through some more exploration drilling and a new feasibility study before it moves forward, so that means revenue should be at least several years away, which means any other likely revenue growth in the next few years would come from either increased production at their existing assets, higher gold and silver prices, or acquisitions of new producing royalties.

And, of course, royalties are more popular than ever, so if you’re trying to buy new ones right now, you might be paying a stiff price — the opportunity for Empress is that they’re so tiny they can make very small deals with junior operators that wouldn’t interest a larger royalty firm, but there are no doubt also other private buyers around. (Every royalty firm has its own strategy and advantage — Empress has the connection with Endeavour and the history of building its own flexible streaming deals with small operators, while another small royalty firm I like, Vox Royalty (VOXR), focuses mostly on Australia and on buying existing perpetual royalties… even within the world of small royalty firms, there are some distinct strategies and business models).

Sound like the kind of thing you’d like to own? I’m a sucker for a small and growing royalty company, so I did buy some Empress shares last year… but after thinking over their full year results and seeing a lot of much stronger royalty companies fall into my “buy” range, I sold Empress to add more to other, larger royalty companies where I’m a little more confident of the long-term trajectory.

But with your money, of course, you get to make the call — so do you want a piece of Empress? Prefer any of the other royalty firms? Think that royalties are too boring for this current gold market, and actual miners are where it’s at? Or, perhaps, do you disagree with Nick Hodge and think gold will fall substantially from here, making all of these companies look at least a little bit worse? Let us know with a comment below… thanks for reading!

Disclosure: Of the companies mentioned above, I own shares of and/or call options on Vox Royalty, Franco-Nevada, Royal Gold, Franco-Nevada, Wheaton Precious Metals, and Versamet Royalties. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

Quoting you, “so who’s to say when stupid gets too stupid? “. WELLwe do have STUPID in the Whitehouse , so I am sure STUPID will do a lot more STUPID stuff than he has already done.

With zero contructive to add to the conversation You choose to Pivot and Change the Subject, just to get your TDS jabs in on The Pesident. Like the Dem stooges blocking the funding for our CYBER SERCURITY TEAMS OPENING IRAN to attack Our Power Grid and Water Supplies. SMH

Things have only gotten worse since you posted this, pal. The most corrupt President of all time, rotten to the core. And people like you know it, but don’t care. The guy most associated with the term TDS was arrested for soliciting a minor and child porn, FYI. This regime and all its minions are vile, corrupt scum.

Joe Biden is gone, was gone!

He was never all there to begin with.

I’d rather have him then an insurrectionist, rapist and pedophile.

And what do we have now? A walking, sleeping, endlessly talking disgrace.

Thanks Travis. Always appreciate your detailed analysis and your personal opinion.

Have you looked at Versemat. (VMET)? They just announced a new royalty deal on Eskay Creek and the market seems to like it.

I bought some last month. Impressive growth profile over the next few years, particularly with the new deal announced this week — though that is a big deal for them, and a meaningful chunk of debt, so they are a little more fragile now if we happen to run into a crash in gold prices over the next year or two.

I believe we all paid for financial information on this site. I, and apparently 5 others, don’t appreciate your political comments, so please keep them to yourself. Thanks!

I appreciate them; a bit closed minded of you as trump is stealing from the public, hoarding emoluments (illegally), not honoring his campaign statements (of course he was lying-because he is a liar ), cheating people of health care-here and abroad-, robbing people of food, killing and deporting people-llegallly and trying to wipe out a civilization, meddling with the stock market, faking being a Christian and denying being a pedo, and on and on it goes..and your’e a fan? Why? Because your’e at the top of the food chain?

Justify, you are so typical of the people who suffer from TDS and it is sickening. You obviously watch MSMedia, read radical left crud and find no value to anything Trump has done because it contradicts the lying radical agenda. Trump is no saint that’s for sure-he bloviates, exaggerates and likes to pat himself on the back,agreed. But the border is secure, drugs and crime are down (except in places of sanctuarey ) he has pushed for peace and this temporary war will end this month. But to you and others who are so short sighted, you are doing all you can to cause even more of a divide than you could ever accuse Trump of. Where is your proof of him depriving people of food or molesting children? He has had very few people deported that shouldn’t have been considering the 20 million let in in the last 4 years unchecked, undocumented and just released into our country. What civilization is he wiping out? The Iran clerics who say “death to america?” “On and on”-a favorite expression of the media who live in their own reality bubble.

BTW, we have more serious problems that have nothing to do with Trump or anything he can even remotely be blamed for. Since 2001 we have been getting deeper and deeper in debt, Our Bonds are shaky and sometime this year the market will slide and of course you will say that Trump is to blame. He and others thought they could fix it but you need politicians to stop spending our money and printing more to keep the party going. WE need to pass a b alanced budget and stick to it which neither party can or wants to do.That campaign promise he can not fulfill, I grant you.

So lighten up and so will I . give all of us including yourself a break from this and come to realize that this time there is no government agency that can save us from what we will go through in the next 4-5 years. Not the Dems not the Reps not Trump or anyone else. A better day is coming but not before we go through a bad time of it.

In good faith Justify, and apologies if I offended-not my goal. Peace brother.

RN

It’s one thing to thought a fool and another to open your mouth and remove all doubt. Thanks for proving it. But it was entertaining to see you talk out of both sides of your mouth and arse at the same time. Now back to the intent of this forum, Financial reviews not political.

I think I will stick with ETFs that own gold mining companies and royalty streaming companies.

Thanks Travis.

I do not think Royalties are a the best bet if you want to make GOOD money in this commodities market. But having said that, safe bets would be ETFs and some Royalties, of course.

I have never trusted Nick “boots on the ground ” Hodge. Your write up here smaks of bias on his part.

Better people to listen to are Don Durrett, John Feneck, Mike Oliver, Rick Rule and Bald guy if you want to make some serious money especially in Gold and Silver stocks. Too many people want the grand slam short term home run when reality says be Knowledgable be patient, place your bets , buy dips and wait. Guys kike Hodge sell short term get rich schemes that sell subscriptions.

My strong advice is to connect with THE guru of gold and silver stocks, Don Durrett. He is on youtube often with John Feneck-He has a service called Gold Stock Data that is so detailed and covers over 850 miners. PLEASE check him out. I did and am way ahead using his analysis. He does not “sell” picks-he advises and has written a book called “How to Invest in Gold and Silver that is quoted by anyone who knows anything as THE source.

Thanks again Travis for what you do. Always informative.

RLN

Hi Travis the latest article about a pitch from Porter has comments turned off

Thanks for letting me know… fixed now.